Banking choices in Saudi Arabia are shifting faster than ever, redefining how institutions compete for attention and trust. Mobile first platforms, open banking initiatives, and fintech collaborations are accelerating digital adoption across segments. As interactions migrate online, banks must track evolving preferences to capture share in a rapidly expanding digital ecosystem.

Yet gaps persist in seamless onboarding, personalization depth, and cross channel continuity that shape perception. Trust signals, data transparency, and responsive support still vary across digital journeys. A focused consumer preference survey uncovers friction points and priorities to guide targeted digital improvement investments.

Areas of Digital Improvement in KSA Banking

-

Onboarding Friction Reduction

Banks must shorten digital application journeys, enable instant verification, and remove repetitive data entry to improve conversion and first experience satisfaction across mobile and web channels.

-

Personalization Depth Enhancement

Institutions need unified behavioral and transactional data to drive tailored interfaces, contextual product prompts, and lifecycle communication that increase relevance and sustained engagement across segments.

-

Channel Continuity Integration

Customers expect progress continuity across app, branch, and contact center interactions; synchronized systems should preserve context, documents, and history to eliminate repetition and frustration.

-

Privacy Transparency Strengthening

Clear consent flows, visible permissions, and understandable data usage explanations reinforce trust, encouraging customers to share information required for advanced digital services and personalization.

-

Intelligent Support Responsiveness

AI assisted chat, smart routing, and real time status visibility reduce effort and resolution time, sustaining satisfaction during critical service and transaction moments across channels.

-

Inclusive Experience Accessibility

Interfaces must support language diversity, accessibility standards, and varied connectivity conditions to ensure equitable participation across demographic and regional segments.

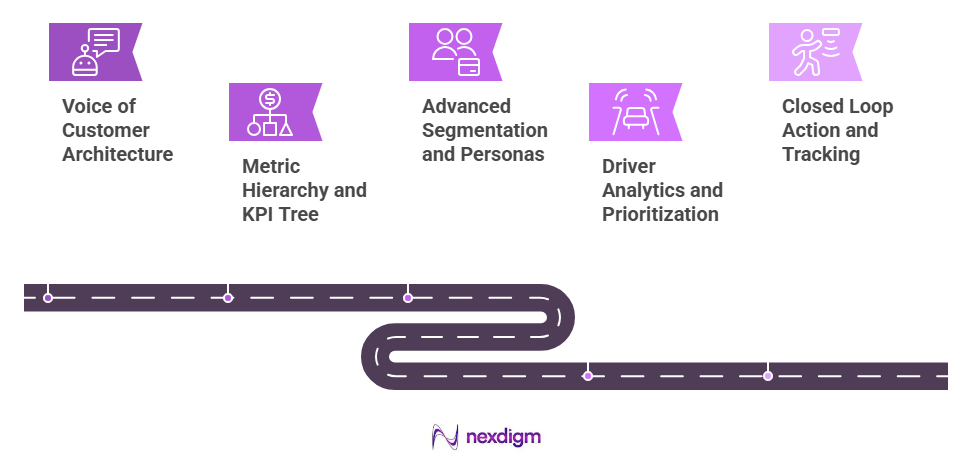

Nexdigm Framework to Define Digital Preference Metrics

-

Voice of Customer Architecture

Nexdigm structures surveys across acquisition, onboarding, usage, and service stages, linking preference signals to journey moments and quantifiable experience metrics for prioritization and governance.

-

Metric Hierarchy and KPI Tree

The framework defines loyalty indices, diagnostic drivers, and operational indicators, enabling attribution from survey responses to product, process, and channel improvements with standardized ownership.

-

Advanced Segmentation and Personas

Nexdigm applies attitudinal and behavioral clustering to reveal preference cohorts, guiding differentiated digital features, messaging, and investment allocation across lifecycle stages.

-

Driver Analytics and Prioritization

Statistical modeling isolates attributes with highest impact on preference and share, translating findings into ranked initiatives with benefit, effort, and feasibility scoring for roadmap sequencing.

-

Closed Loop Action and Tracking

Governance assigns owners, timelines, and verification checks to each improvement area, while pulse surveys track outcomes and recalibrate metrics as digital maturity advances.

Nexdigm Case

A mid sized Saudi retail bank faced declining digital engagement and weak product penetration despite high mobile adoption. Nexdigm deployed a KSA Banking Consumer Preference Survey spanning onboarding, payments, lending, and support journeys, isolating onboarding delay, fragmented channel continuity, and low personalization relevance as primary barriers. Over nine months, digital onboarding completion improved 34 percent, mobile product cross sell rose 27 percent, service resolution time fell 22 percent, and overall digital satisfaction increased 18 points.

To take the next step, simply visit our Request a Consultation page and share your requirements with us.

Harsh Mittal

+91-8422857704