Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The APAC commercial aircraft market is projected to reach approximately USD ~ billion based on recent historical assessments. This growth is driven by the region’s increasing demand for air travel, which is fueled by rising disposable incomes and greater connectivity. Significant investments in airport infrastructure, coupled with a push for low-cost carriers, have accelerated market development. The market expansion is further supported by technological advancements aimed at improving fuel efficiency and reducing operational costs. Additionally, government initiatives and partnerships between airlines and aircraft manufacturers are expected to bolster the region’s aviation sector.

Key players in the APAC commercial aircraft market operate primarily in countries like China, India, and Japan, where government-backed aviation programs are shaping growth. China leads the region with massive investments in airport facilities and a burgeoning middle class, driving demand for both domestic and international air travel. India’s fast-growing aviation sector benefits from rising consumer affluence and infrastructure development. Japan maintains its leadership with a focus on technological innovations in aviation, enabling its airlines to adopt the latest fuel-efficient aircraft. These nations dominate the region’s commercial aircraft market due to their strong industrial infrastructure and consumer demand.

Market Segmentation

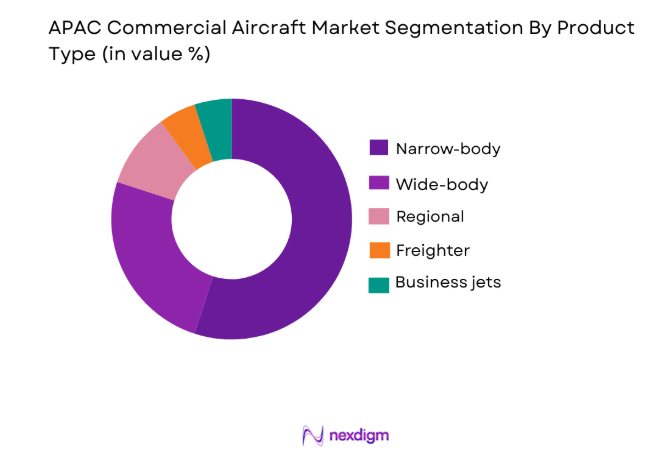

By Product Type:

APAC commercial aircraft market is segmented by product type into narrow-body aircraft, wide-body aircraft, regional jets, freighter aircraft, and business jets. Recently, narrow-body aircraft have a dominant market share due to their cost efficiency and versatility in serving both short-haul and medium-haul routes. This product segment’s dominance is driven by the growing preference for budget-friendly travel options across the region. Additionally, airlines favor these aircraft for their ability to cover a broad range of routes while maintaining low operational costs. Infrastructure availability and regional demand for point-to-point travel also play critical roles in this sub-segment’s expansion.

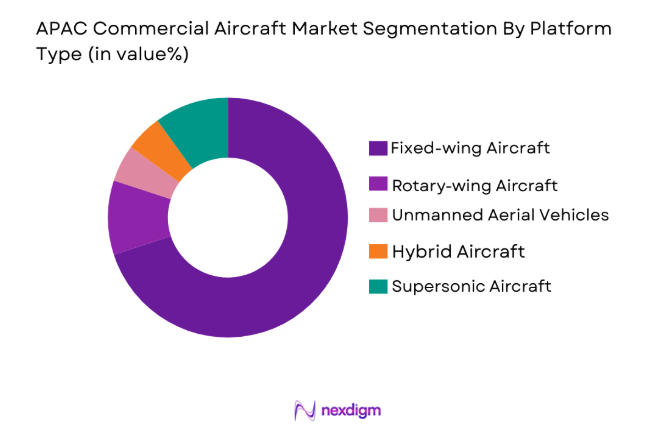

By Platform Type

APAC commercial aircraft market is segmented by platform type into fixed-wing aircraft, rotary-wing aircraft, unmanned aerial vehicles (UAVs), hybrid aircraft, and supersonic aircraft. Fixed-wing aircraft dominate due to their broad application across short and long-haul routes, favored by airlines for their versatility and efficiency. The growing demand for both regional and international air travel in the region contributes to the dominance of fixed-wing aircraft, supported by expanding airport infrastructure.

Competitive Landscape

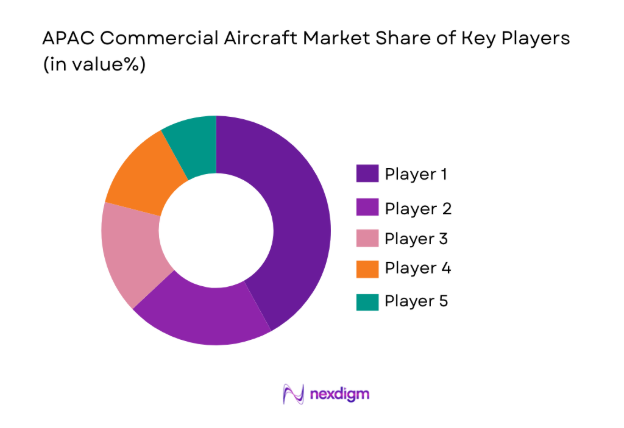

The APAC commercial aircraft market is highly competitive, with key players leading innovation and driving industry growth through strategic partnerships and acquisitions. The market is experiencing some degree of consolidation, as major players continue to innovate with new aircraft designs and manufacturing technologies to enhance fuel efficiency, safety, and operational costs. These efforts are supported by increased government spending in the aviation sector and international collaborations. Global manufacturers are competing for market share, with increasing pressure to meet stringent regulatory standards while expanding their presence in the growing APAC region.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Additional Parameter |

| Airbus | 1970 | France | ~ | ~ | ~ | ~ | ~ |

| Boeing | 1916 | USA | ~ | ~ | ~ | ~ | ~ |

| Bombardier | 1942 | Canada | ~ | ~ | ~ | ~ | ~ |

| Mitsubishi Aircraft | 2008 | Japan | ~ | ~ | ~ | ~ | ~ |

| COMAC | 2008 | China | ~ | ~ | ~ | ~ | ~ |

APAC Commercial Aircraft Market Analysis

Growth Drivers

Rising Air Travel Demand:

The increase in disposable income, especially in developing countries within APAC, has led to a significant surge in air travel demand. As economic conditions improve, more consumers in countries such as China, India, and Southeast Asia are now able to afford air travel, leading to a steady rise in passenger traffic. The expansion of low-cost carriers (LCCs) has played a pivotal role in making air travel more accessible to a larger population by offering affordable ticket options. Governments in the region, particularly in India and China, have heavily invested in improving aviation infrastructure, including the construction of new airports and upgrading existing ones, which has facilitated the growth of air traffic. This demand is especially strong in short-haul and medium-haul routes, where narrow-body aircraft are particularly in demand. The rise of urbanization and the expansion of the middle class across APAC are expected to sustain this growth trajectory for the foreseeable future. In addition to passenger air travel, the growing e-commerce sector has boosted the demand for air cargo services, leading to an increase in freighter aircraft operations. With the increased demand for air cargo due to the rise of cross-border online retail, the commercial aircraft market is witnessing a parallel demand for specialized cargo aircraft. This growth trend is further supported by favorable government policies in several countries aimed at boosting the aviation sector, including tax incentives, subsidies, and trade agreements that help facilitate market expansion.

Technological Advancements:

The APAC commercial aircraft market is benefiting greatly from continuous advancements in technology. Aircraft manufacturers are focusing on innovations such as fuel-efficient engines, lightweight composite materials, and more efficient avionics systems that reduce operational costs and improve overall performance. Manufacturers are also making significant strides in developing electric and hybrid aircraft that produce lower emissions and operate with reduced fuel consumption. These technological advancements align with global sustainability goals and are becoming increasingly important to both manufacturers and airlines looking to reduce their environmental footprint. Moreover, improvements in aircraft design and manufacturing techniques have resulted in greater aircraft durability and reliability, which in turn leads to reduced maintenance costs for airlines. These innovations have allowed airlines to offer lower ticket prices while maintaining profitability. Additionally, the push for greener technologies has opened the door for government incentives and regulatory support for airlines adopting such solutions. The growth of air passenger and cargo traffic, combined with advancements in aircraft technology, is expected to continue to drive the APAC commercial aircraft market forward, making it one of the most dynamic and rapidly evolving sectors in the region.

Market Challenges

High Operational Costs:

One of the key challenges facing the APAC commercial aircraft market is the high operational costs associated with running airlines, particularly in emerging markets. The cost of fuel is one of the most significant contributors to these expenses, with fluctuations in global oil prices directly affecting the profitability of airlines. In addition to fuel costs, airlines must also manage the ongoing costs of aircraft maintenance, parts replacement, and regulatory compliance, which further strain their financial resources. The capital investment required to procure new aircraft is another substantial financial challenge, with airlines needing to secure financing for the purchase of expensive new fleets or lease agreements. The long payback period associated with these investments adds another layer of financial pressure, especially in markets where competition is fierce and ticket prices are under constant pressure to remain low. Many airlines in the APAC region are heavily reliant on government subsidies to help offset some of these costs, which adds an element of uncertainty. In countries like India and Indonesia, where low-cost carriers dominate, the margins are typically thinner, making it more challenging for these airlines to remain profitable. This reliance on subsidies also makes airlines vulnerable to changes in government policy, which could negatively impact their ability to manage operational costs effectively.

Regulatory Compliance and Safety Standards:

Navigating through stringent regulatory environments is another key challenge for the APAC commercial aircraft market. Airlines and aircraft manufacturers in the region must adhere to a complex set of safety, environmental, and operational regulations imposed by both domestic and international aviation authorities. These regulations can increase the time and cost involved in the production, certification, and operation of commercial aircraft. Airlines must also ensure that their fleets comply with evolving environmental standards, which often requires costly retrofits and upgrades to meet emissions targets. Additionally, the rapid pace of technological innovation means that regulations must constantly be updated to keep up with new developments in the industry. This creates additional challenges for both aircraft manufacturers and airlines as they work to balance regulatory compliance with the need to stay competitive in a fast-moving market. For airlines, the continuous need to upgrade their fleets to meet safety and environmental standards adds further financial strain. The market also faces challenges in terms of the varying regulatory standards across different APAC countries, which complicates the harmonization of aviation policies and increases operational complexities for regional carriers.

Opportunities

Development of Sustainable Aviation:

As environmental concerns continue to rise globally, the APAC commercial aircraft market is experiencing a significant shift toward sustainable aviation solutions. Governments across the region are increasingly prioritizing green policies and encouraging the development of technologies aimed at reducing emissions and improving fuel efficiency in the aviation industry. The integration of sustainable aviation fuel (SAF), hybrid propulsion systems, and lightweight materials in aircraft design are expected to be key drivers of future market growth. Airlines are exploring alternative energy sources to reduce their reliance on fossil fuels, while manufacturers are adopting innovative solutions to increase aircraft efficiency and reduce carbon footprints. This shift to sustainable aviation not only addresses environmental concerns but also presents long-term operational cost savings for airlines, as fuel is one of the largest expenses for commercial aircraft operators. With growing environmental awareness among passengers, airlines that invest in sustainable aviation technologies can also gain a competitive edge by attracting eco-conscious consumers. Furthermore, governments are supporting the transition to greener aviation technologies through subsidies, incentives, and regulatory frameworks, making it a favorable environment for the development and adoption of sustainable aviation solutions. As more countries commit to reaching net-zero carbon emissions in the coming decades, the demand for green aviation solutions is expected to grow significantly, creating new opportunities for manufacturers and airlines in the APAC region.

Expansion of Low-Cost Carriers:

The rapid expansion of low-cost carriers (LCCs) in the APAC region presents a major opportunity for the commercial aircraft market. LCCs have become a dominant force in many countries, offering affordable air travel options to an expanding middle class with rising disposable incomes. The LCC business model focuses on reducing operating costs while offering no-frills services, which has made air travel more accessible to a large portion of the population. The growth of low-cost carriers has been particularly prominent in Southeast Asia, where LCCs such as AirAsia and Lion Air have revolutionized air travel by offering budget-friendly options for short-haul and regional flights. This expansion is driving the demand for narrow-body aircraft, which are ideally suited for the short-haul routes that LCCs typically operate. With the rising number of budget-conscious travelers and the continued growth of the middle class in countries like India, Indonesia, and Thailand, the market for low-cost carriers is expected to expand further. Additionally, the low operational costs of narrow-body aircraft and their efficiency in regional routes make them a popular choice for LCCs looking to maximize profitability. As these carriers continue to expand their fleets, the demand for commercial aircraft, particularly in the LCC segment, will continue to rise, presenting a significant growth opportunity for manufacturers and suppliers in the APAC region.

Future Outlook

The APAC commercial aircraft market is poised for significant growth over the next five years, driven by the continued expansion of the middle class and increasing air travel demand. Key factors influencing this growth include technological advancements in fuel efficiency, a strong push for sustainability, and supportive government regulations. The rise of low-cost carriers, along with investments in aviation infrastructure, is expected to make air travel more accessible to a broader audience, further stimulating demand for aircraft. As environmental concerns rise, the market is likely to see greater investments in green technologies and the adoption of sustainable aviation fuels, which will help reduce emissions. Furthermore, increasing collaboration between private and public sectors in the aviation industry is likely to lead to new opportunities for aircraft manufacturers and airline operators.

Major Players

• Boeing

• Bombardier

• Mitsubishi Aircraft

• COMAC

• Raytheon Technologies

• Embraer

• Textron Aviation

• Lockheed Martin

• Honda Aircraft

• GE Aviation

• Rolls-Royce

• Thales

• L3 Technologies

• Safran

Key Target Audience

• Government and regulatory bodies

• Commercial airlines

• Cargo carriers

• Aircraft leasing companies

• Private operators

• Aircraft manufacturers

• Aviation infrastructure developers

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves defining key market variables, including the market size, growth trends, and segment breakdowns, to ensure a targeted approach.

Step 2: Market Analysis and Construction

This stage focuses on collecting both primary and secondary data, analyzing current trends, and building the market structure.

Step 3: Hypothesis Validation and Expert Consultation

Consulting industry experts and validating initial hypotheses are key to refining the research model.

Step 4: Research Synthesis and Final Output

The final output synthesizes all collected data and insights, providing a comprehensive analysis of the market and its future outlook.

- Executive Summary

- Research Methodology

(Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increase in Air Travel Demand

Rising Disposable Incomes in Emerging Economies

Government Support for Aviation Infrastructure

Advancements in Aircraft Technology

Shift Towards Sustainable Aviation - Market Challenges

High Capital Costs for Aircraft Manufacturers

Stringent Regulatory and Certification Processes

Impact of Economic Downturns on Air Travel

Supply Chain Disruptions

Maintenance and Operational Challenges - Market Opportunities

Rise in Low-Cost Carrier Models

Expansion of Regional Air Services

Growth of Private and Business Jet Markets - Trends

Increasing Use of Electric Aircraft

Advancements in Aircraft Materials and Design

Focus on Sustainable Aviation Fuel

Growth in Urban Air Mobility (UAM)

Digitalization of Aircraft Operations - Government Regulations & Defense Policy

Aviation Safety Regulations

Environmental Regulations and Carbon Emissions

Defense and Military Procurement Policies - SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Narrow-body Aircraft

Wide-body Aircraft

Regional Jets

Freighter Aircraft

Business Jets - By Platform Type (In Value%)

Fixed-wing Aircraft

Rotary-wing Aircraft

Unmanned Aerial Vehicles

Hybrid Aircraft

Supersonic Aircraft - By Fitment Type (In Value%)

OEM Aircraft

Aftermarket Aircraft

Fleet Upgrades

Maintenance & Repair

Refurbishment - By EndUser Segment (In Value%)

Commercial Airlines

Cargo Carriers

Government & Defense

Private Operators

Leasing Companies - By Procurement Channel (In Value%)

Direct Procurement

Government Tenders

Private Sector Procurement

Third-party Procurement

Online Bidding Platforms - By Material / Technology (in Value%)

Lightweight Composite Materials

Titanium Alloys

Hybrid Propulsion Systems

Advanced Avionics

Fuel-efficient Engines

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type)

SWOT Analysis of Key Competitors

Pricing & Procurement Analysis - Key Players

Airbus

Boeing

Bombardier

Embraer

Mitsubishi Aircraft Corporation

Sukhoi Civil Aircraft

COMAC

Dassault Aviation

Lockheed Martin

Honda Aircraft Company

Raytheon Technologies

Saab Group

Textron Aviation

GE Aviation

Rolls-Royce

- Increasing demand from commercial airlines

- Leasing companies’ growing role in fleet management

- Rising investments in cargo aircraft

- Private operators’ interest in business aviation

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now