Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Asia Pacific Air Defense Systems market is experiencing significant growth due to increasing military investments and the ongoing modernization of defense infrastructures. Based on a recent historical assessment, the market size is driven by growing geopolitical tensions, technological advancements in defense systems, and increasing demand for air defense solutions in the region of USD~ billion. The market’s expansion is fueled by the need for advanced air surveillance, interception systems, and enhanced radar technologies to counter rising threats. Major investments in national security by countries such as China, India, and Japan are also contributing to the market’s growth.

The dominant countries in the Asia Pacific region for air defense systems include China, India, and Japan. These countries have strong defense budgets and a clear focus on strengthening their air defense capabilities. China leads with its robust investment in modern technologies like anti-aircraft missile systems and cyber defense capabilities, while India and Japan follow with significant investments in advanced radar systems and air defense platforms. These countries are highly competitive in both domestic and international markets, with their strategic geographic locations adding to their dominance in air defense systems.

Market Segmentation

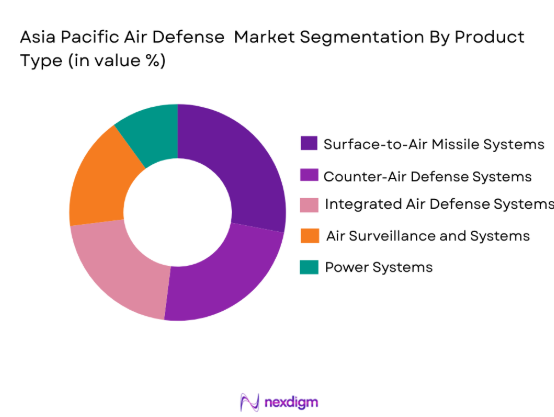

By Product Type

Asia Pacific Air Defense Systems market is segmented by product type into surface-to-air missile (SAM) systems, counter-air defense systems, integrated air defense systems (IADS), air surveillance and targeting systems, and command & control systems. Recently, surface-to-air missile systems had a dominant market share due to factors such as technological advancements, increased military budgets, and the demand for reliable defense against air threats. SAM systems are highly sought after for their cost-effectiveness and ease of deployment, making them a preferred choice for many defense agencies in the region.

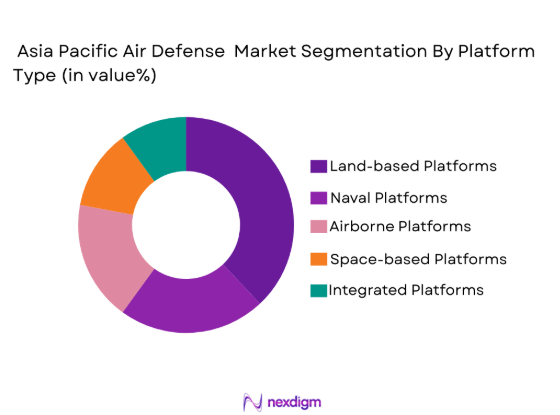

By Platform Type

Asia Pacific Air Defense Systems market is segmented by platform type into land-based platforms, naval platforms, airborne platforms, space-based platforms, and integrated platforms. Recently, land-based platforms have had a dominant market share due to factors such as their versatility, cost-effectiveness, and the ability to cover large areas. With rising regional threats, many countries prefer land-based systems, which can be deployed more efficiently and offer robust protection for critical infrastructure, military bases, and key assets.

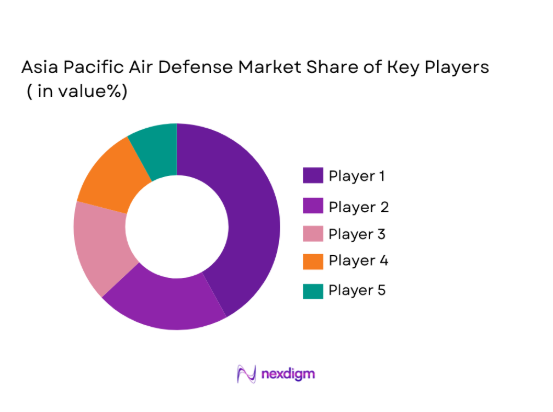

Competitive Landscape

The competitive landscape in the Asia Pacific Air Defense Systems market is characterized by consolidation, with major defense contractors driving technological innovations and expanding their market influence. Key players have established long-term partnerships with government agencies and military forces to secure major contracts. The dominance of these players is further reinforced by their continuous R&D efforts, resulting in state-of-the-art air defense technologies. Companies like Lockheed Martin, Thales Group, and Raytheon Technologies lead the market, pushing for advanced solutions that enhance air defense capabilities for their clients in the region.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Market-Specific Parameter |

| Lockheed Martin | 1912 | USA | ~ | ~ | ~ | ~ | ~ |

| Thales Group | 2000 | France | ~ | ~ | ~ | ~ | ~ |

| Raytheon Technologies | 1922 | USA | ~ | ~ | ~ | ~ | ~ |

| BAE Systems | 1999 | UK | ~ | ~ | ~ | ~ | ~ |

| Northrop Grumman | 1939 | USA | ~ | ~ | ~ | ~ | ~ |

Asia Pacific Air Defense Systems Market Analysis

Growth Drivers

Technological Advancements in Air Defense Systems

The rapid pace of technological advancements in radar systems, missile interception, and surveillance technologies has significantly contributed to the growth of the air defense systems market. As threats from adversarial airspace activities evolve, nations across the Asia Pacific region are heavily investing in cutting-edge air defense solutions to maintain strategic dominance. The integration of AI and machine learning into defense systems has enhanced the capability of platforms, improving their effectiveness in detecting and intercepting enemy threats. Additionally, the growing use of advanced sensors and command-and-control systems has enabled air defense forces to respond faster and more accurately to threats. With these innovations, air defense systems are becoming more sophisticated, offering enhanced reliability and efficiency. These factors are driving strong demand for modernized defense infrastructure that ensures protection against the evolving nature of aerial threats. Governments are prioritizing the procurement of advanced technologies, accelerating the adoption of these systems within the defense sector.

Increasing Geopolitical Tensions

Rising geopolitical tensions in the Asia Pacific region, particularly between neighboring countries, have significantly contributed to the increasing demand for air defense systems. As regional threats intensify, countries are ramping up their defense capabilities to safeguard their borders and airspace. For instance, territorial disputes in the South China Sea have prompted nations such as China and Vietnam to enhance their air defense infrastructure to protect vital trade routes and military interests. Similarly, tensions between India and Pakistan, as well as the strategic importance of countries like Japan and South Korea, have made air defense systems a top priority. The ongoing security challenges in the region further highlight the need for advanced defense solutions that provide real-time threat identification and interception capabilities. The necessity to deter air-based attacks and safeguard national sovereignty has fueled a surge in demand for state-of-the-art air defense systems across these countries.

Market Challenges

High Cost of Air Defense Systems

One of the most significant challenges faced by countries in the Asia Pacific region is the high cost of acquiring and maintaining air defense systems. The initial investment required for state-of-the-art systems such as surface-to-air missiles (SAMs), radar systems, and advanced interceptors can be astronomical, especially for developing nations with limited defense budgets. Additionally, the ongoing costs of maintenance, training, and system upgrades further strain government finances. These high costs often prevent smaller nations from fully upgrading their defense infrastructure, as they are forced to prioritize other areas within their military budgets. The financial burden of implementing these complex defense systems also limits the ability to deploy them across vast geographical regions, which is particularly challenging in countries with large and remote areas to defend. Furthermore, the procurement process is often delayed due to lengthy budgetary approvals and government procedures, causing potential security gaps in the meantime. This challenge requires governments to make tough decisions regarding the allocation of resources and often results in delayed or incomplete upgrades to national defense capabilities.

Integration and Interoperability Issues

The integration of advanced air defense systems with existing infrastructure is a critical challenge in the Asia Pacific market. Many countries in the region operate a mix of legacy systems and newer technologies, and ensuring compatibility between these different platforms is often a complex and time-consuming process. The lack of interoperability can lead to delays in response times, reduced effectiveness of defense strategies, and complications in collaborative defense operations with allied nations. Additionally, the integration of newer technologies such as AI, advanced radar, and cyber defense systems with older infrastructure requires significant effort and investment. This presents a barrier for countries that lack the technical expertise and resources to perform these integrations seamlessly. Furthermore, the varying standards and specifications across different manufacturers’ systems complicate efforts to create a unified defense network. The difficulty in achieving smooth integration increases the vulnerability of defense systems, particularly in fast-evolving threats where real-time communication and coordination are vital.

Opportunities

Growing Defense Budgets in Emerging Markets

The rising defense budgets of emerging markets in the Asia Pacific region present significant opportunities for growth in the air defense systems market. As nations like India, Vietnam, and Indonesia prioritize strengthening their military capabilities, they are increasingly turning to advanced air defense systems to protect their airspace and critical infrastructure. These countries are seeking to modernize their existing defense infrastructures and are willing to invest in cutting-edge technologies to keep pace with more developed nations. Moreover, these defense budgets are supported by increasing foreign investments and collaborations with global defense companies, which are eager to tap into the rapidly growing markets of the Asia Pacific region. As these emerging markets continue to expand their defense spending, they will likely drive significant demand for advanced air defense systems, presenting lucrative opportunities for manufacturers and technology providers to secure long-term contracts. The expanding middle class and increasing national security concerns in these nations further amplify the need for advanced defense solutions, creating a favorable environment for continued market growth.

Technological Innovation in Autonomous Air Defense Systems

Another key opportunity for the Asia Pacific Air Defense Systems market is the growing demand for autonomous defense systems. As technology advances, countries in the region are increasingly investing in unmanned aerial vehicles (UAVs), autonomous missiles, and AI-powered systems that offer enhanced operational capabilities with reduced human intervention. Autonomous systems have the potential to significantly improve the efficiency and response times of air defense operations by quickly analyzing data and making real-time decisions without waiting for human input. These systems can be deployed in both combat and surveillance scenarios, providing a multi-layered defense strategy that is highly adaptive to evolving threats. The ability to integrate autonomous systems into existing air defense infrastructures also allows for cost-effective solutions, as they often require less manpower and can perform tasks continuously without fatigue. Additionally, the potential for these systems to work seamlessly with other advanced technologies, such as cyber defense and integrated command-and-control platforms, makes them an attractive investment for nations looking to future-proof their defense strategies.

Future Outlook

The future outlook for the Asia Pacific Air Defense Systems market is poised for significant growth over the next five years. With rising defense budgets and increasing geopolitical tensions, countries in the region are focusing on enhancing their air defense capabilities to counter growing threats. Technological advancements in missile defense systems, radar technology, and AI-driven platforms will continue to drive market innovation. Additionally, strong regulatory support and defense policies aimed at bolstering national security will further encourage investments in advanced air defense systems. As demand for modernization grows, particularly in emerging markets, the market will witness a steady expansion of air defense solutions to meet diverse security needs.

Major Players

- Lockheed Martin

- Thales Group

- Raytheon Technologies

- BAE Systems

- Northrop Grumman

- Saab Group

- General Dynamics

- Rheinmetall AG

- Leonardo

- L3 Technologies

- Harris Corporation

- Elbit Systems

- Hewlett Packard Enterprise

- Boeing

- Saab Group

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Military contractors

- Aerospace and defense companies

- System integrators

- National defense ministries

- Defense technology developers

- Aviation safety regulators

Research Methodology

Step 1: Identification of Key Variables

The identification of key variables involved in the air defense systems market, such as market value, product type, regional demand, and technological innovations, is essential for laying the foundation of the research process.

Step 2: Market Analysis and Construction

In this step, market data is analyzed using both qualitative and quantitative techniques to construct a comprehensive market model. This includes evaluating industry trends, regulatory policies, and technological advancements.

Step 3: Hypothesis Validation and Expert Consultation

Expert consultations are carried out to validate hypotheses and ensure that the market trends align with real-world insights from industry leaders and stakeholders.

Step 4: Research Synthesis and Final Output

The findings from the previous steps are synthesized to generate a final report, which is used to provide actionable insights and strategic recommendations for stakeholders in the air defense systems market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increasing Military Budgets in Asia Pacific

Geopolitical Tensions in the Region

Technological Advancements in Air Defense

Rising Demand for Modernized Air Defense Systems

Government Policies Supporting National Security

- Market Challenges

High Cost of Air Defense Systems

Technological Integration Challenges

Vulnerability to Cybersecurity Threats

Political and Economic Instability in the Region

Regulatory and Compliance Barriers - Market Opportunities

Integration of AI for Enhanced Air Defense

Rising Investments in Autonomous Systems

Expansion of Air Defense Systems in Emerging Markets - Trends

Shift towards Integrated Defense Systems

Increased Focus on Cyber-Resilient Systems

Rising Adoption of Unmanned Aerial Vehicles (UAVs) in Defense

Growth of Multi-layered Air Defense Systems

Strategic Partnerships in Air Defense Technologies - Government Regulations & Defense Policy

Export Control Regulations on Defense Technologies

National Security Policy Reform in the Region

Government Investment in Defense R&D - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Surface-to-Air Missile (SAM) Systems

Counter-Air Defense Systems

Integrated Air Defense Systems (IADS)

Air Surveillance and Targeting Systems

Command & Control Systems - By Platform Type (In Value%)

Land-based Platforms

Naval Platforms

Airborne Platforms

Space-based Platforms

Integrated Platforms - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Hybrid Solutions

Modular Solutions

Integrated Solutions - By End User Segment (In Value%)

Military Forces

Defense Contractors

Government Agencies

Security Services

Private Sector / Technology Firms - By Procurement Channel (In Value%)

Direct Procurement

Government Tenders

Private Sector Procurement

Online Bidding Platforms

Third-party Distributors - By Material / Technology (In Value%)

Electromagnetic Weapons

Cyber Defense Technology

Advanced Radar Systems

Smart Missile Technology

Artificial Intelligence in Defense Systems

- Market share snapshot of major players

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Lockheed Martin

Raytheon Technologies

Thales Group

BAE Systems

Northrop Grumman

Saab Group

General Dynamics

Rheinmetall AG

Leonardo

L3 Technologies

Harris Corporation

Elbit Systems

Hewlett Packard Enterprise

Boeing

Saab Group

- Increased Demand for Air Defense Systems from Military Forces

- Growing Role of Government Agencies in Air Defense

- Private Sector Engagement in Modernizing Air Defense Capabilities

- Security Services Advancing Air Defense Technologies

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now