Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Asia Pacific aircraft manufacturing market is experiencing significant growth driven by the expansion of the aviation sector and increased demand for both commercial and military aircraft. Based on a recent historical assessment, the market size is valued at approximately USD 120 billion, with a focus on both regional and international travel needs. The demand for air travel in the region has led to an increase in production capacity by OEMs, with major players ramping up efforts to meet the growing demand for new and replacement aircraft. The market’s growth is also supported by government-backed defense contracts and rising military spending.

Key countries in the region, such as China, India, and Japan, have become central to the market’s dominance. China leads in aircraft production with its substantial investment in aerospace technology and manufacturing infrastructure, while India’s growing middle class has significantly contributed to the demand for commercial aircraft. Japan, with its robust technological capabilities, focuses on the production of both civilian and defense aircraft. The dominance of these countries is fueled by strategic government initiatives, strong manufacturing capabilities, and the continuous development of aerospace technologies.

Market Segmentation

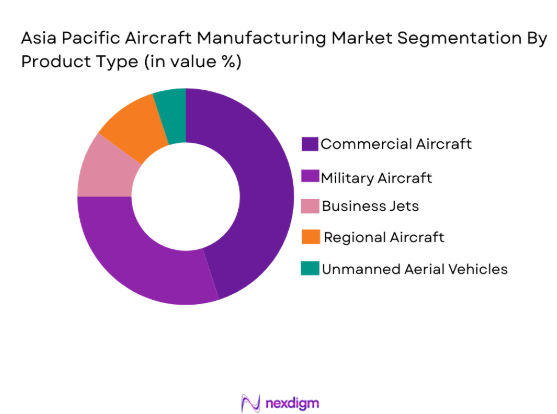

By Product Type

The Asia Pacific aircraft manufacturing market is segmented by product type into commercial aircraft, military aircraft, business jets, regional aircraft, and unmanned aerial vehicles (UAVs). Recently, the commercial aircraft sub-segment has a dominant market share due to increasing air travel demand driven by the growing middle class and expanding tourism industries across the region. The expansion of low-cost carriers in countries like India and China has significantly boosted the need for more cost-efficient aircraft. Additionally, the growth in regional trade and connectivity demands aircraft with varying capacities, further strengthening the position of the commercial aircraft sub-segment.

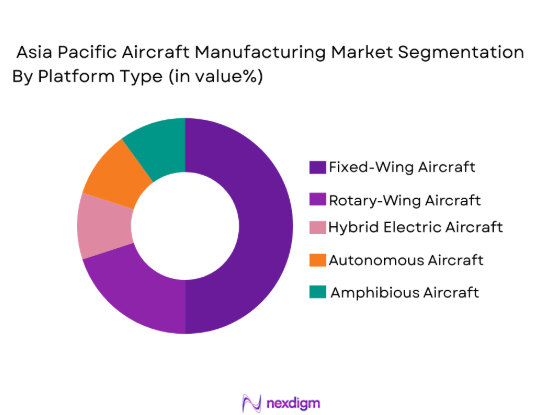

By Platform Type

The Asia Pacific aircraft manufacturing market is segmented by platform type into fixed-wing aircraft, rotary-wing aircraft, hybrid electric aircraft, autonomous aircraft platforms, and amphibious aircraft. Recently, the fixed-wing aircraft sub-segment has dominated the market due to the increasing demand for long-haul and regional air travel. Fixed-wing aircraft offer greater efficiency and are better suited for a wide range of commercial and military applications, which has contributed to their widespread adoption. Additionally, technological advancements and reduced operating costs have further strengthened the position of fixed-wing aircraft in the market.

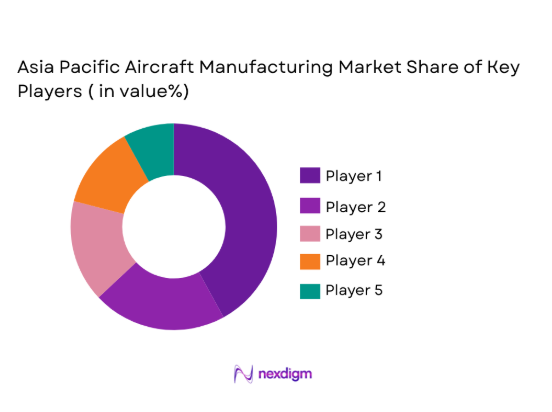

Competitive Landscape

The competitive landscape of the Asia Pacific aircraft manufacturing market is highly concentrated, with major players engaging in strategic collaborations and joint ventures to expand their manufacturing capabilities. The industry is characterized by a blend of large-scale OEMs and emerging regional manufacturers. With the rise of advanced aerospace technologies and a push for sustainability, the influence of leading firms in the market is crucial in determining the pace of innovation and growth. Major companies are focusing on increasing production capacity and improving aircraft fuel efficiency, further intensifying competition in the market.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Market-Specific Parameter |

| Boeing | 1916 | USA | ~ | ~ | ~ | ~ | ~ |

| Airbus | 1970 | France | ~ | ~ | ~ | ~ | ~ |

| Mitsubishi Heavy Industries | 1884 | Japan | ~ | ~ | ~ | ~ | ~ |

| China Aviation Industry Group | 1951 | China | ~ | ~ | ~ | ~ | ~ |

| Embraer | 1969 | Brazil | ~ | ~ | ~ | ~ | ~ |

Asia pacific Aircraft Manufacturing Market Analysis

Growth Drivers

Technological Advancements in Aircraft Manufacturing

The rapid pace of technological advancements in aircraft manufacturing has been a significant growth driver in the Asia Pacific region. Innovations in materials, such as carbon fiber composites, have led to lighter, more fuel-efficient aircraft, which are increasingly in demand by airlines seeking to reduce operational costs. Furthermore, the integration of advanced avionics and automation has enhanced aircraft performance, safety, and passenger experience, further driving the demand for new aircraft models. Manufacturers are also investing heavily in electric propulsion systems, promising to further revolutionize the industry by providing greener alternatives to traditional aircraft. These technological advancements are allowing aircraft manufacturers to meet evolving consumer needs and regulatory demands, contributing to sustained market growth.

Government and Private Sector Investments

Government policies in the Asia Pacific region are another major growth driver for the aircraft manufacturing market. Countries like China and India are significantly increasing their defense budgets, thereby expanding demand for military and surveillance aircraft. Simultaneously, the expansion of low-cost carriers in emerging markets and the growth of regional connectivity are creating a surge in demand for commercial aircraft. Government-backed initiatives, such as manufacturing incentives and infrastructure development, further stimulate the market by facilitating smoother operations for manufacturers and airlines. This push for aerospace growth is complemented by the private sector’s increasing focus on fleet modernization and expansion, making aircraft production a priority.

Market Challenges

Supply Chain Disruptions and Material Shortages

One of the primary challenges facing the Asia Pacific aircraft manufacturing market is the ongoing supply chain disruptions, particularly the shortage of raw materials. Aerospace-grade materials, such as titanium, aluminum, and advanced composites, are essential for producing high-performance aircraft. However, delays in the global supply chain, exacerbated by the COVID-19 pandemic, continue to cause production delays and rising costs for manufacturers. These shortages have been further compounded by geopolitical tensions and trade restrictions in the region, which have disrupted the smooth flow of essential components. Manufacturers are finding it increasingly difficult to maintain production timelines, leading to delays in fulfilling aircraft orders and reducing operational efficiency.

Regulatory and Certification Hurdles

Aircraft manufacturers in Asia Pacific face complex regulatory and certification hurdles that slow down the pace of innovation and production. Each country has its own set of regulations, with authorities such as the Civil Aviation Administration of China (CAAC) and the Directorate General of Civil Aviation (DGCA) in India imposing strict airworthiness standards and certification processes. These requirements can take years to complete, especially for new aircraft designs. While necessary for ensuring safety, these regulations add considerable time and cost to the development process, making it challenging for manufacturers to quickly respond to market demand or introduce new models. The constant evolution of aviation standards, such as emissions control, also adds complexity and costs to aircraft design and manufacturing processes.

Opportunities

Sustainable Aviation Technologies

As environmental concerns grow and governments enforce stricter emission regulations, there is an opportunity for aircraft manufacturers in Asia Pacific to lead the charge in sustainable aviation. Manufacturers are increasingly investing in electric and hybrid propulsion technologies, which aim to reduce the carbon footprint of the aviation industry. Furthermore, sustainable aviation fuels (SAFs) are being explored as a viable alternative to traditional jet fuel. These developments present significant opportunities for manufacturers to innovate and tap into an eco-conscious market, addressing both regulatory pressures and consumer demand for greener solutions. By focusing on sustainable technologies, companies can gain a competitive edge in an industry that is under growing scrutiny for its environmental impact.

Regional Aircraft Expansion

With the growing demand for air travel in emerging markets like India, Southeast Asia, and parts of Oceania, the demand for regional aircraft is increasing. Manufacturers have an opportunity to capitalize on this demand by designing and producing smaller, more fuel-efficient aircraft suited to regional routes. These aircraft are needed to cater to short-haul flights, which are expected to grow rapidly due to rising urbanization and the expanding middle class. Regional aircraft offer better flexibility, lower operational costs, and the ability to serve smaller airports with limited infrastructure. As the demand for more localized and affordable air travel increases, regional aircraft manufacturers have a promising opportunity to expand their product offerings and cater to this growing market segment.

Future Outlook

The future outlook for the Asia Pacific aircraft manufacturing market is optimistic, with continued growth expected due to increasing demand for both commercial and military aircraft. Technological advancements in aircraft design, fuel efficiency, and sustainability are expected to shape the industry’s trajectory, with electric and hybrid aircraft technologies gaining momentum. Strong regulatory support for sustainable aviation practices and infrastructure development will further propel market growth. Additionally, rising disposable incomes, urbanization, and regional trade will continue to fuel demand for air travel, creating favorable conditions for market expansion in the next five years.

Major Players

- Boeing

- Airbus

- Mitsubishi Heavy Industries

- China Aviation Industry Group

- Embraer

- Hindustan Aeronautics Limited

- Aviation Industry Corporation of China

- PT Dirgantara Indonesia

- Kawasaki Heavy Industries Aerospace

- Shenyang Aircraft Corporation

- Chengdu Aircraft Industry Group

- Xi’an Aircraft Industrial Corporation

- Tata Advanced Systems

- Mahindra Aerospace

- ST Engineering Aerospace

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Aerospace manufacturers

- Airline operators

- Commercial airlines

- Defense contractors

- Aircraft leasing companies

- Aviation consultancy firms

Research Methodology

Step 1: Identification of Key Variables

Identify the core factors influencing market dynamics such as technological trends, regulatory changes, and economic shifts.

Step 2: Market Analysis and Construction

Analyze market trends, historical data, and forecast future market trajectories using industry reports and expert opinions.

Step 3: Hypothesis Validation and Expert Consultation

Validate market hypotheses by consulting with industry experts, stakeholders, and conducting surveys to gather insights.

Step 4: Research Synthesis and Final Output

Synthesize research findings to create comprehensive market reports, detailing growth drivers, challenges, and future forecasts.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising passenger air traffic driving fleet expansion

Government-backed aerospace manufacturing initiatives

Expansion of low-cost carrier networks

Increasing defense aviation procurement

Localization strategies reducing import dependence - Market Challenges

High capital intensity of production facilities

Supply chain disruptions for aerospace-grade materials

Stringent certification requirements

Skilled workforce shortages in precision manufacturing

Program delays due to technological complexity - Market Opportunities

Development of sustainable aviation platforms

Expansion of indigenous aircraft programs

Growing demand for next-generation narrow-body aircraft - Trends

Adoption of digital twin technologies in aircraft design

Shift toward fuel-efficient aircraft architectures

Integration of automation in assembly lines

Increasing partnerships between global OEMs and regional firms

Emergence of electric and hybrid propulsion research

Government Regulations & Defense Policy

Offset policies promoting domestic production

Airworthiness standards harmonization across regional regulators

Defense industrial corridor development initiatives - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Commercial Aircraft Manufacturing

Military Aircraft Manufacturing

Business Jet Manufacturing

Regional Aircraft Manufacturing

Unmanned Aerial Vehicle Manufacturing - By Platform Type (In Value%)

Fixed-Wing Aircraft

Rotary-Wing Aircraft

Hybrid Electric Aircraft

Autonomous Aircraft Platforms

Amphibious Aircraft - By Fitment Type (In Value%)

Original Equipment Manufacturing

Line Fit Installations

Retrofit Manufacturing

Modular Assembly Integration

Custom Configuration Manufacturing - By End User Segment (In Value%)

Commercial Airlines

Defense Forces

Charter Operators

Cargo Carriers

Government Aviation Agencies - By Procurement Channel (In Value%)

Direct OEM Contracts

Government Acquisition Programs

Leasing Companies

Joint Venture Production Agreements

Third-Party Aerospace Integrators - By Material / Technology (in Value %)

Aluminum Alloy Airframes

Carbon Fiber Reinforced Polymer Structures

Titanium Component Manufacturing

Additive Manufacturing Technologies

Advanced Avionics Integration

- Market share snapshot of major players

- Cross Comparison Parameters (Production Capacity, Aircraft Portfolio Diversity, Technological Capabilities, Strategic Partnerships, Regional Presence, Order Backlog Strength, R&D Investment, Manufacturing Automation Level, Aftermarket Support)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Commercial Aircraft Corporation of China

Hindustan Aeronautics Limited

Mitsubishi Heavy Industries Aerospace

Korea Aerospace Industries

Aviation Industry Corporation of China

PT Dirgantara Indonesia

Kawasaki Heavy Industries Aerospace Company

Shenyang Aircraft Corporation

Chengdu Aircraft Industry Group

Xi’an Aircraft Industrial Corporation

Tata Advanced Systems

Mahindra Aerospace

ST Engineering Aerospace

Fuji Heavy Industries Aerospace

Aerospace Industrial Development Corporation

- Airlines prioritizing fuel-efficient fleet modernization

- Defense agencies investing in locally produced platforms

- Cargo operators expanding wide-body aircraft adoption

- Government bodies supporting aerospace industrialization

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now