Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Asia Pacific Armored Fighting Vehicles market is expected to see significant growth, driven by rising defense budgets and modernization initiatives within the region. Based on a recent historical assessment, the market size for armored fighting vehicles stands at USD ~ billion, with an expected increase due to growing geopolitical tensions and the need for enhanced military capabilities. Governments are heavily investing in upgrading their military fleets, bolstering the demand for advanced armored systems. Key factors such as the development of more mobile, adaptable, and technologically advanced systems contribute to the market’s growth, further boosted by national security concerns.

The dominance of countries like India, China, and South Korea can be attributed to their significant investments in military modernization. These nations are focusing on strengthening their defense capabilities amidst rising regional tensions, which drives demand for advanced armored fighting vehicles. China’s ongoing military modernization, India’s defense procurement reforms, and South Korea’s emphasis on defense technology are major factors that solidify their dominance. Additionally, these countries’ large-scale manufacturing capabilities and strategic geographical positions contribute to their pivotal roles in the market.

Market Segmentation

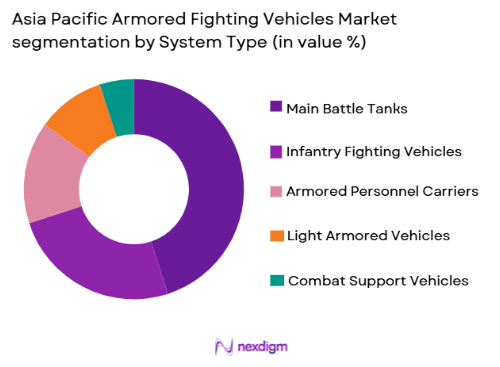

By System Type

The Asia Pacific Armored Fighting Vehicles market is segmented by system type into Main Battle Tanks, Infantry Fighting Vehicles, Armored Personnel Carriers, Light Armored Vehicles, and Combat Support Vehicles. Recently, Main Battle Tanks have a dominant market share due to factors such as the increasing demand from military forces for superior combat vehicles that provide high firepower and protection. The effectiveness of modern main battle tanks in various combat scenarios and their adaptability to evolving military needs make them crucial in many countries’ defense strategies. Additionally, the long lifecycle and capability upgrades of these vehicles enhance their market presence. Main Battle Tanks continue to dominate due to their multifunctionality and critical role in modern warfare.

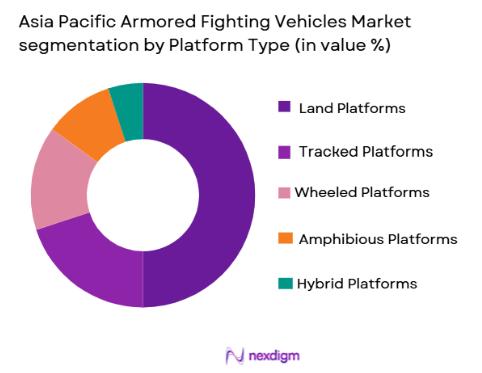

By Platform Type

The Asia Pacific Armored Fighting Vehicles market is segmented by platform type into Land Platforms, Tracked Platforms, Wheeled Platforms, Amphibious Platforms, and Hybrid Platforms. Recently, Land Platforms have a dominant market share due to the expansive terrain and the heavy reliance on land-based military operations across the region. The adaptability of land platforms to different terrains and their suitability for both offensive and defensive operations have made them essential. Additionally, land platforms often have a broader range of deployment options, further boosting their prominence in the market. With advanced technology and robust designs, land platforms cater to diverse operational needs across various defense forces.

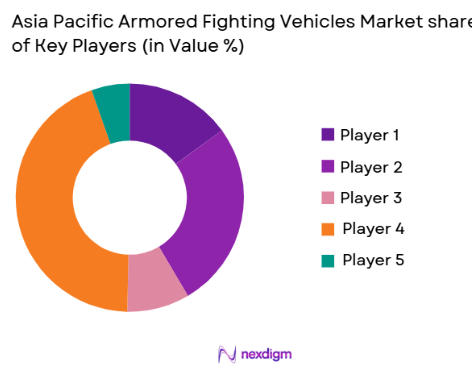

Competitive Landscape

The competitive landscape of the Asia Pacific Armored Fighting Vehicles market shows significant consolidation, with a few major players dominating the market. The market is driven by advanced technological innovations and a high demand for reliable, efficient, and durable vehicles. Companies are increasingly focusing on improving vehicle capabilities, integrating AI-driven technologies, and ensuring high protection levels against various threats. Major players in the market continue to expand their footprints across the Asia Pacific region, capitalizing on defense procurement policies, military modernization programs, and government-funded defense projects.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD Billion) | Additional Market-Specific Parameter |

| BAE Systems | 1999 | United Kingdom | ~ | ~ | ~ | ~ | ~ |

| General Dynamics | 1899 | United States | ~ | ~ | ~ | ~ | ~ |

| Rheinmetall AG | 1889 | Germany | ~ | ~ | ~ | ~ | ~ |

| Lockheed Martin | 1912 | United States | ~ | ~ | ~ | ~ | ~ |

| Hyundai Rotem | 1977 | South Korea | ~ | ~ | ~ | ~ | ~ |

Asia Pacific Armored Fighting Vehicles Market Analysis

Growth Drivers

Government Military Modernization

A key growth driver in the Asia Pacific Armored Fighting Vehicles market is the ongoing modernization of military forces across the region. Countries like China, India, and Japan are heavily investing in advanced military systems to enhance their defense capabilities and preparedness for emerging threats. These modernization initiatives focus on replacing outdated equipment and improving the overall effectiveness of their armed forces. The increased demand for advanced armored fighting vehicles is primarily driven by these defense modernization programs, which are set to continue for the next few years, boosting the market for next-generation military platforms. Countries are also upgrading their current fleets to include more capable and survivable platforms, driving a shift toward advanced main battle tanks and infantry fighting vehicles that can meet modern battlefield requirements.

Technological Advancements in Armored Vehicles

Another growth driver is the continuous advancements in armored vehicle technology. Innovations in armor materials, active protection systems, and vehicle mobility are enhancing the overall effectiveness and survivability of armored fighting vehicles in various combat scenarios. The development of lighter yet stronger materials, such as composite and reactive armor, and the integration of cutting-edge technologies such as autonomous navigation and enhanced communications systems are playing a key role in the market’s expansion. As these technological advancements become more accessible and cost-effective, they are expected to drive the demand for next-generation armored vehicles, further contributing to the market’s growth over the forecast period.

Market Challenges

High Production and Maintenance Costs

One significant challenge for the Asia Pacific Armored Fighting Vehicles market is the high production and maintenance costs of armored vehicles. The cost of manufacturing advanced military systems, coupled with the ongoing expenses of maintaining these vehicles in operational readiness, poses a financial burden for defense agencies in the region. While defense budgets are increasing, they are often allocated across multiple needs, and the cost-effectiveness of armored vehicles must be carefully weighed against other military investments. Additionally, the long-term costs associated with maintaining sophisticated armored platforms, including repairs and upgrades, can limit procurement opportunities for smaller nations, reducing market potential in some parts of the region.

Interoperability and Integration Issues

Another challenge the market faces is the difficulty of integrating advanced armored fighting vehicles into existing military fleets and ensuring interoperability across various platforms. The challenge arises from the differences in technology, design, and operational procedures between various countries’ armored vehicles, which complicates joint operations in multinational military alliances. For countries with legacy systems, the integration of newer technologies can be time-consuming and costly, requiring extensive training and adaptation of existing infrastructure. As military forces aim for more networked and interoperable systems, overcoming these integration barriers will be critical to achieving the full potential of new armored vehicles.

Opportunities

Adoption of Autonomous and AI-driven Armored Vehicles

One key opportunity in the Asia Pacific Armored Fighting Vehicles market is the growing adoption of autonomous and AI-driven armored systems. As military forces seek to reduce human casualties and improve operational efficiency, the development of autonomous vehicles capable of performing complex tasks in battlefield environments presents a significant opportunity. These vehicles can be equipped with advanced sensors and AI systems to navigate and engage targets with minimal human intervention. The increasing interest in autonomous systems, combined with technological advancements in AI, is expected to drive the demand for these vehicles, especially in conflict zones where risks to human soldiers are high. Governments in the region are already investing in research and development to integrate AI into armored fighting vehicles, opening up new market opportunities.

Partnerships with Private Tech Firms for Advanced Solutions

Another opportunity lies in forming strategic partnerships between defense contractors and private technology firms to develop advanced solutions for armored fighting vehicles. The rapid advancement of commercial technologies such as sensor fusion, cybersecurity, and machine learning offers immense potential for improving armored vehicle performance. By leveraging the expertise of private firms in cutting-edge technologies, defense companies can enhance their vehicle systems’ capabilities, making them more agile, adaptable, and capable of handling future combat scenarios. This collaboration between defense contractors and tech companies will lead to the creation of highly advanced, smart armored systems that can meet evolving military needs.

Future Outlook

The future outlook for the Asia Pacific Armored Fighting Vehicles market is positive, with continued demand driven by increasing defense budgets and technological advancements. The shift towards more versatile and adaptable systems will likely lead to greater adoption of hybrid and autonomous vehicles in the region. Governments will continue their investment in military modernization, focusing on enhancing armored vehicle capabilities. Technological developments in areas such as AI, mobility, and active protection systems will enable better performance on the battlefield. Regulatory support for defense procurement will also play a significant role in shaping the market, driving further growth over the next five years.

Major Players

- BAE Systems

- General Dynamics

- Rheinmetall AG

- Lockheed Martin

- Hyundai Rotem

- Oshkosh Corporation

- Navistar Defense

- Elbit Systems

- Thales Group

- KMW

- Saab Group

- L3 Technologies

- Rosoboronexport

- Northrop Grumman

- IVECO

Key Target Audience

- Military and defense agencies

- Government and regulatory bodies

- Defense contractors

- Security and surveillance organizations

- Manufacturers of military vehicles and systems

- Research and development firms

- Technology providers for defense systems

- Investment firms and venture capitalists

Research Methodology

Step 1: Identification of Key Variables

This step involves identifying the main factors that influence the market, including regional dynamics, technological trends, and defense policies.

Step 2: Market Analysis and Construction

We analyze current market trends and construction methodologies to estimate the market size and future forecast using both primary and secondary data sources.

Step 3: Hypothesis Validation and Expert Consultation

At this stage, we validate the identified trends and assumptions by consulting industry experts and analyzing past market performance.

Step 4: Research Synthesis and Final Output

We synthesize the information collected through all stages to create the final report, which includes a comprehensive analysis and forecast of the Asia Pacific Armored Fighting Vehicles market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increase in Defense Budgets

Geopolitical Tensions in the Region

Modernization of Military Forces

Technological Advancements in Armored Vehicles

Government Initiatives in Defense Procurement - Market Challenges

High Production Costs

Complex Maintenance and Operational Costs

Regulatory Constraints

Interoperability Issues

Supply Chain Vulnerabilities - Market Opportunities

Technological Integration of AI in Armored Vehicles

Partnerships with Private Sector for Advanced Solutions

Emerging Demand for Light and Mobile Armored Vehicles - Trends

Increase in Use of Hybrid Armor Technologies

Rising Demand for Autonomous Combat Vehicles

Focus on Modular Armored Vehicle Designs

Advancements in Active Protection Systems

Shift Towards Low-Cost, High-Efficiency Armored Vehicles - Government Regulations & Defense Policy

Export Control and Compliance Policies

Government Funding for Modern Defense Solutions

Regulations on Military Procurement

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Main Battle Tanks

Infantry Fighting Vehicles

Armored Personnel Carriers

Light Armored Vehicles

Combat Support Vehicles - By Platform Type (In Value%)

Land Platforms

Tracked Platforms

Wheeled Platforms

Amphibious Platforms

Hybrid Platforms - By Fitment Type (In Value%)

Combat-fit Armored Vehicles

Logistics-fit Armored Vehicles

Special-purpose Armored Vehicles

Retrofit Armored Vehicles

Customized Armored Vehicles - By End User Segment (In Value%)

Military Forces

Defense Contractors

Government Agencies

Private Sector

Security Services - By Procurement Channel (In Value%)

Direct Procurement

Government Tenders

Private Sector Procurement

Online Bidding Platforms

Third-party Distributors - By Material / Technology (In Value%)

Steel Armor

Composite Armor

Reactive Armor

Active Protection Systems

Hybrid Materials

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Material/Technology, Government Regulations, Pricing, Competitor Size, Regional Coverage)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

General Dynamics

BAE Systems

Lockheed Martin

Rheinmetall AG

Saab Group

Thales Group

L3 Technologies

Elbit Systems

Navistar Defense

Oshkosh Corporation

Rosoboronexport

Northrop Grumman

ST Engineering

IVECO

KMW

- Military Forces’ Shift Toward Advanced Armored Vehicles

- Defense Contractors’ Role in R&D and Manufacturing

- Government Agencies’ Influence on Procurement Policies

- Private Sector’s Involvement in Commercial Armored Vehicle Solutions

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now