Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Asia Pacific Civil Aviation Simulators market reached approximately USD ~ million based on a recent historical assessment, supported by expanding airline fleets, increasing pilot shortages, and heightened regulatory requirements for structured flight training. Rising regional connectivity and new route development have accelerated simulator adoption, as airlines prioritize cost-efficient training environments that replicate real-world flight scenarios. Technological advancements such as virtual reality integration and AI-enabled analytics further strengthen operational efficiency, encouraging training providers and airlines to expand simulator infrastructure across major aviation economies.

China, India, Japan, and Southeast Asian aviation hubs dominate regional activity due to rapid commercial aviation expansion and strong pilot training demand. China operates more than 270 simulators while India exceeds 185 certified units, reflecting substantial investments in training capacity tied to airline growth. Regional facilities collectively recorded over ~ million simulator training hours, demonstrating intensive utilization driven by fleet modernization and workforce development strategies that reinforce these countries as operational centers for civil aviation training ecosystems.

Market Segmentation

By Product Type

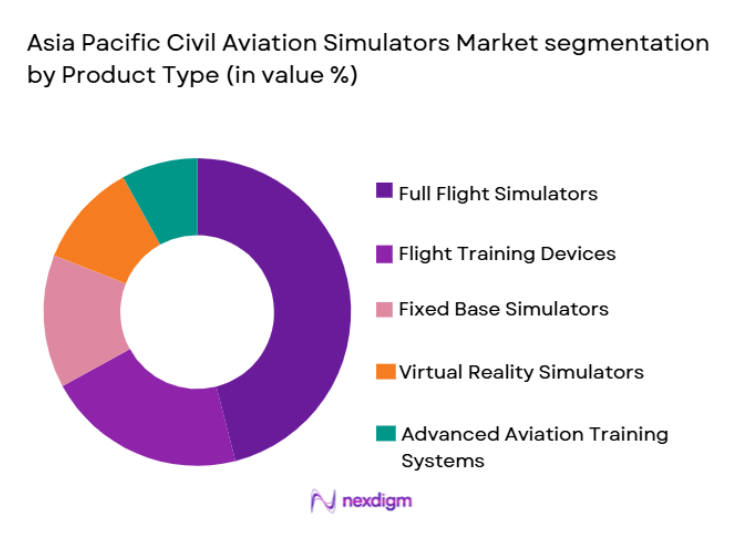

Asia Pacific Civil Aviation Simulators market is segmented by product type into full flight simulators, flight training devices, fixed base simulators, virtual reality simulators, and advanced aviation training systems. Recently, full flight simulators have a dominant market share due to their ability to replicate complete cockpit environments with motion feedback, regulatory acceptance for certification training, and strong airline preference for high-fidelity training. Airlines favor these systems because they reduce operational risks while supporting recurrent pilot assessments. Training centers also invest heavily in full flight simulators to meet stringent compliance requirements and attract global airline clients seeking standardized training capabilities across multi-aircraft fleets.

By End User

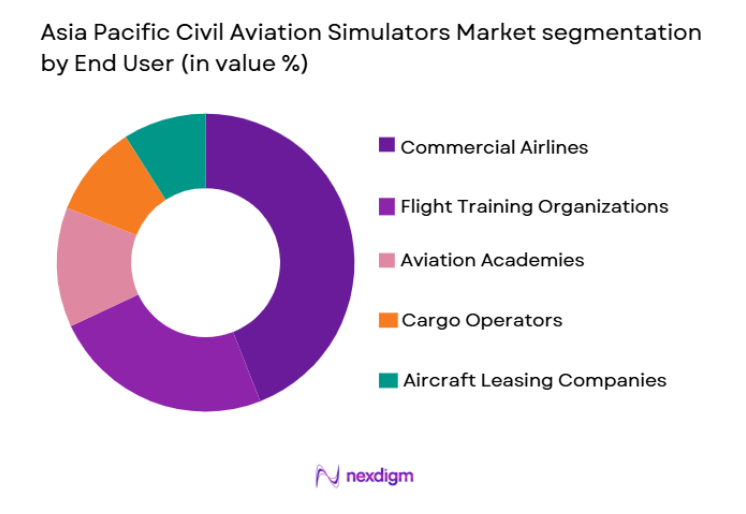

Asia Pacific Civil Aviation Simulators market is segmented by end user into commercial airlines, flight training organizations, aviation academies, cargo operators, and aircraft leasing companies. Recently, commercial airlines have a dominant market share due to aggressive fleet expansion, mandatory simulator hours for pilot certification, and the need to maintain operational safety standards. Airlines increasingly internalize training capabilities to reduce long-term costs and ensure scheduling flexibility. Growing passenger volumes and route density further require continuous pilot onboarding, positioning airline operators as the largest purchasers of advanced simulation technologies across regional aviation ecosystems.

Competitive Landscape

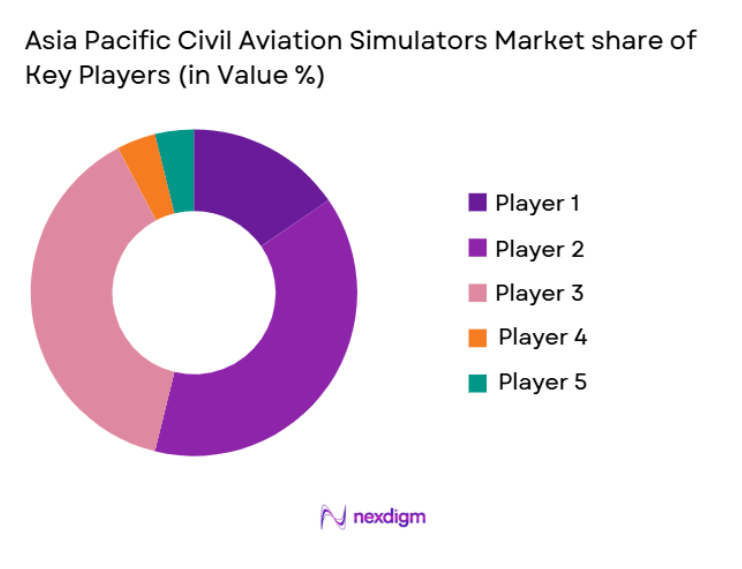

The Asia Pacific Civil Aviation Simulators market exhibits moderate consolidation, with established global simulator manufacturers maintaining technological leadership through long-term airline partnerships and integrated training solutions. Competitive intensity is shaped by innovation in immersive simulation, lifecycle support services, and regulatory certification capabilities. Major participants leverage strategic expansions, joint ventures, and localized training centers to strengthen regional presence, while smaller providers focus on niche training requirements and cost-efficient simulator platforms to remain competitive.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Certification Capability |

| CAE Inc. | 1947 | Canada | ~ | ~ | ~ | ~ | ~ |

| L3Harris Technologies | 2019 | United States | ~ | ~ | ~ | ~ | ~ |

| Thales Group | 1893 | France | ~ | ~ | ~ | ~ | ~ |

| FlightSafety International | 1951 | United States | ~ | ~ | ~ | ~ | ~ |

| TRU Simulation + Training | 2014 | United States | ~ | ~ | ~ | ~ | ~ |

Asia Pacific Civil Aviation Simulators Market Analysis

Growth Drivers

Accelerating Pilot Shortage and Fleet Expansion

Commercial aviation across Asia Pacific is undergoing structural expansion driven by rising passenger traffic, expanding middle-class travel demand, and increased airline route density, all of which require a steady influx of trained pilots. Industry forecasts indicate that fleet sizes are growing rapidly, compelling airlines to scale training capacity without compromising operational safety. Simulator-based instruction enables pilots to practice complex flight conditions while avoiding real-world risk exposure, making it a preferred training approach. Airlines are prioritizing investments in high-fidelity simulators to meet regulatory mandates that require structured simulator hours for certification and recurrent assessments. Training through simulators also reduces fuel consumption and aircraft wear, improving cost efficiency for carriers operating on tight margins. Additionally, the ability to simulate emergency procedures enhances crew preparedness, reinforcing regulatory compliance. Regional aviation authorities increasingly emphasize standardized training frameworks, further strengthening simulator adoption. As low-cost carriers expand aggressively, training throughput requirements continue to rise. The convergence of workforce demand, safety priorities, and operational economics ensures sustained procurement of advanced simulation platforms throughout the region.

Technological Advancements Enhancing Training Effectiveness

Rapid innovation in simulation technology is transforming pilot instruction by delivering immersive environments that closely replicate real flight dynamics. Virtual reality and artificial intelligence tools now enable adaptive training scenarios tailored to individual pilot performance, improving retention and skill development. Advanced visual projection systems provide near-realistic weather conditions and terrain mapping, allowing trainees to experience diverse operational contexts within controlled settings. Data analytics embedded within simulators support performance monitoring, enabling instructors to refine training modules and address competency gaps. Electric motion platforms further enhance realism while reducing maintenance complexity compared with traditional hydraulic systems. Integration with digital twin architectures allows airlines to align simulator data with aircraft behavior, strengthening predictive training models. These improvements shorten learning cycles and enhance operational readiness, which is particularly valuable as airlines accelerate recruitment. Training providers leverage these capabilities to differentiate service offerings and attract international carriers. As technology continues to lower lifecycle costs while improving fidelity, adoption across both established and emerging aviation markets is expected to intensify.

Market Challenges

High Capital Investment and Lifecycle Costs

Civil aviation simulators require substantial upfront investment, with advanced full flight systems costing upward of USD 10 million per unit, creating financial barriers for smaller training providers. Beyond procurement, operators must account for facility construction, motion platform maintenance, and periodic software upgrades to remain compliant with evolving certification standards. Financing these assets can strain cash flows, particularly in developing aviation markets where access to long-term capital is limited. Airlines may delay purchases during economic uncertainty, opting instead for leased training capacity, which constrains manufacturer order volumes. Depreciation cycles also necessitate replacement planning as technology becomes obsolete. Furthermore, specialized technicians are required for calibration and repairs, increasing operational expenditure. Training centers must maintain high utilization rates to justify investments, yet fluctuating pilot demand can affect scheduling efficiency. Regulatory recertification processes introduce additional costs and downtime. These financial pressures collectively slow market entry for new participants and reinforce reliance on established providers with stronger balance sheets.

Regulatory Complexity and Certification Requirements

Simulator deployment must comply with stringent aviation authority standards that govern fidelity, motion response, and software validation before devices can be used for certified training. Achieving approval involves rigorous testing protocols that extend project timelines and elevate compliance costs. Differences in regulatory frameworks across Asia Pacific countries further complicate cross-border training operations, requiring providers to customize systems for local approval. Any delay in certification can postpone revenue generation, creating planning uncertainty for investors. Continuous updates to match evolving aircraft models demand additional validation cycles. Operators must also ensure instructor qualifications and procedural alignment with regulatory expectations, adding administrative overhead. Failure to meet standards risks operational suspension, emphasizing the importance of meticulous compliance management. Smaller firms often lack the regulatory expertise needed to navigate these processes efficiently. Consequently, certification complexity acts as a structural barrier that consolidates market power among experienced manufacturers with established regulatory relationships.

Opportunities

Expansion of Regional Pilot Training Hubs

Asia Pacific is emerging as a global center for aviation workforce development, with governments and private operators investing in large-scale training campuses to address pilot shortages. Strategic geographic positioning allows these hubs to serve multiple airlines across neighboring markets, improving asset utilization for simulator operators. Partnerships between airlines and training providers are becoming more common, enabling shared infrastructure and reducing capital burdens. Modern campuses increasingly integrate accommodation, digital classrooms, and multi-aircraft simulators, creating comprehensive training ecosystems. This approach attracts international cadets seeking cost-efficient certification pathways. Governments support such initiatives to strengthen domestic aviation capabilities and reduce reliance on overseas training. Rising aircraft deliveries reinforce the need for localized instruction capacity. Simulator manufacturers benefit from bulk procurement agreements tied to hub development projects. As air traffic continues to rise, regional training centers are expected to evolve into long-term anchors for simulator demand and technological deployment.

Adoption of Mixed Reality and Data-Driven Training Models

Mixed reality platforms combining augmented and virtual environments are redefining how pilots interact with simulated cockpits by enabling immersive yet flexible instruction modules. These systems allow trainees to rehearse complex procedures repeatedly without the logistical constraints of traditional simulators. Data-driven analytics capture behavioral insights that help instructors tailor programs to individual learning curves, improving training efficiency. Airlines increasingly view such technologies as strategic tools to accelerate readiness while controlling operational costs. Cloud connectivity supports remote scenario updates, ensuring training relevance as aircraft software evolves. Lower hardware footprints make mixed reality attractive for secondary training facilities and emerging aviation markets. Vendors are actively investing in software ecosystems that complement high-fidelity simulators, expanding revenue streams beyond hardware sales. As digital transformation reshapes aviation training philosophies, mixed reality solutions are positioned to unlock scalable growth opportunities across the regional simulator landscape.

Future Outlook

The Asia Pacific Civil Aviation Simulators market is expected to advance steadily as airlines expand fleets and training demand intensifies across emerging aviation economies. Technological integration including AI-enabled analytics and immersive simulation is likely to improve training precision while lowering lifecycle costs. Regulatory frameworks emphasizing safety and standardized pilot certification will continue to support simulator adoption. Growing training hubs and cross-border partnerships are anticipated to strengthen infrastructure, sustaining long-term procurement momentum.

Major Players

- CAE Inc.

- L3Harris Technologies

- Thales Group

- FlightSafety International

- TRU Simulation + Training

- Indra Sistemas

- Frasca International

- Boeing Training & Flight Services

- Collins Aerospace

- Alpha Aviation Group

- ALSIM

- Precision Flight Controls

- SIM International

- Reiser Simulation and Training

- Avion Group

Key Target Audience

- Commercial airline operators

- Aircraft leasing companies

- Flight training organizations

- Simulator manufacturing companies

- Aviation technology providers

- Defense aviation transition units

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Core variables including simulator demand, pilot training requirements, fleet expansion, and regulatory mandates were mapped. Secondary industry databases and aviation authority publications were reviewed to establish baseline indicators influencing regional simulator procurement patterns.

Step 2: Market Analysis and Construction

Quantitative modeling combined regional aviation activity with simulator deployment metrics to construct market sizing. Historical revenue data and installation trends were synthesized to derive realistic structural assumptions supporting market interpretation.

Step 3: Hypothesis Validation and Expert Consultation

Industry viewpoints from training providers, aviation specialists, and technology stakeholders were evaluated to validate assumptions. Cross-verification ensured alignment between operational realities, procurement cycles, and emerging training technologies.

Step 4: Research Synthesis and Final Output

All validated insights were consolidated into a structured framework emphasizing growth dynamics, competitive positioning, and demand catalysts. Analytical outputs were refined to ensure consistency, reliability, and decision-ready interpretation.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rapid commercial fleet expansion across emerging Asia Pacific economies

Rising pilot training requirements driven by regional air traffic growth

Increasing regulatory mandates for recurrent simulator based training

Expansion of low cost carriers requiring scalable training infrastructure

Technological advancements improving simulator realism and efficiency - Market Challenges

High capital investment required for advanced full flight simulators

Limited availability of certified training instructors in developing markets

Complex regulatory approvals for simulator certification

Operational downtime linked to simulator maintenance cycles

Integration challenges with next generation aircraft platforms - Market Opportunities

Growing demand for cross border pilot training hubs

Adoption of mixed reality technologies for cost efficient training

Partnership models between airlines and simulator providers - Trends

Shift toward AI enabled predictive training analytics

Increasing deployment of ultra high definition immersive visuals

Growth of simulator leasing as a service models

Expansion of multi aircraft type training centers

Rising preference for energy efficient electric motion systems - Government Regulations & Defense Policy

Civil aviation authorities mandating simulator hours for type ratings

Regional safety oversight programs harmonizing training standards

Government incentives supporting aviation training infrastructure - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Full Flight Simulators

Flight Training Devices

Fixed Base Simulators

Virtual Reality Based Simulators

Augmented Reality Assisted Training Systems - By Platform Type (In Value%)

Commercial Narrow Body Aircraft Simulators

Commercial Wide Body Aircraft Simulators

Regional Jet Simulators

Business Jet Simulators

Helicopter Training Simulators - By Fitment Type (In Value%)

OEM Installed Training Systems

Retrofit Simulator Platforms

Standalone Training Centers

Mobile Simulator Units

Cloud Connected Simulation Environments - By EndUser Segment (In Value%)

Commercial Airline Operators

Independent Flight Training Organizations

Aircraft Leasing Companies

Cargo Airline Operators

Government Supported Aviation Academies - By Procurement Channel (In Value%)

Direct Manufacturer Procurement

Long Term Leasing Contracts

Training Service Outsourcing Agreements

Public Aviation Tenders

Strategic Airline Partnerships - By Material / Technology (in Value %)

Electric Motion Actuation Systems

Hydraulic Motion Platforms

AI Driven Scenario Generation

High Fidelity Visual Projection Systems

Digital Twin Enabled Simulation

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Simulator Fidelity Level, Motion Technology, Visual Resolution Capability, Aircraft Type Coverage, Training Throughput Capacity, Certification Standards Compliance, Lifecycle Support Services, Integration Capability, Delivery Timelines, Pricing Flexibility)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

CAE Inc.

L3Harris Technologies

TRU Simulation + Training

Thales Group

Indra Sistemas

FlightSafety International

Frasca International

Reiser Simulation and Training

ALSIM

SIM International

Pacific Simulators

Fidelity Flight Simulation

Avion Group

Axis Flight Training Systems

Aeromaoz Simulation

- Airlines prioritizing simulator ownership to reduce long term training costs

- Flight schools expanding capacity to address regional pilot shortages

- Leasing firms incorporating simulator access within fleet agreements

- Government academies strengthening domestic pilot training pipelines

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now