Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Australia 3PL market is valued at USD ~ billion based on a recent historical assessment, driven by increasing e-commerce penetration, growing demand for supply chain efficiency, and rising adoption of automation technologies in warehousing and transportation. Expansion of omnichannel retail strategies has further propelled demand, encouraging third-party providers to offer integrated logistics solutions. Investment in digital freight management systems, inventory optimization platforms, and real-time tracking capabilities has enhanced operational efficiency. Rising consumer expectations for faster deliveries and cost-effective logistics solutions continue to incentivize providers to scale operations. Strategic partnerships between retailers, manufacturers, and 3PL firms support seamless distribution networks. Government incentives for infrastructure development and modernization of freight corridors have strengthened market dynamics. Increasing international trade and import-export activities contribute additional momentum to the market. The overall market landscape benefits from technological innovations, workforce upskilling, and growing regional distribution hubs. Logistics service providers are increasingly investing in temperature-controlled and specialized storage facilities to capture niche demand. Consumer preference for timely, reliable deliveries drives continuous expansion and modernization.

Market Segmentation

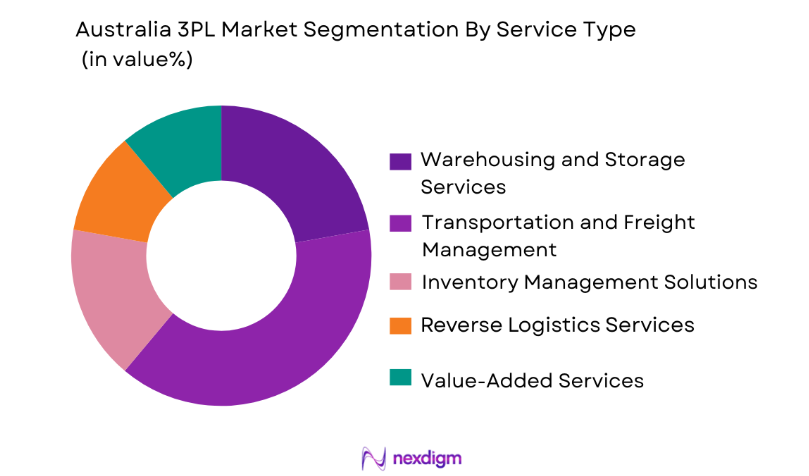

By Service Type

Australia 3PL market is segmented by service type into warehousing and storage services, transportation and freight management, inventory management solutions, reverse logistics services, and value-added services. Recently, transportation and freight management has a dominant market share due to factors such as increasing demand for rapid and cost-efficient distribution, technological integration in route optimization and tracking, strategic partnerships with e-commerce platforms, and expanding cross-border logistics operations. The segment benefits from investments in automated fleet management systems and intermodal transportation solutions. High consumer expectations for timely delivery reinforce the need for efficient transport services. The sector leverages data analytics for predictive demand planning. Growing adoption of environmentally sustainable vehicles and compliance with regulatory standards further supports expansion. Industry consolidation and strategic acquisitions enhance network coverage. Partnerships with technology providers enable integration of IoT and AI systems for operational efficiency. Seasonal demand fluctuations in retail and agriculture are addressed through scalable transportation services. Third-party providers offer flexible contract options. Investment in infrastructure modernization facilitates faster turnaround times. Transportation hubs near major ports and airports optimize freight handling. Advanced telematics and route planning software improve productivity. Integration with warehouse operations enhances supply chain visibility. Technology-enabled tracking improves customer satisfaction. The sector’s strategic role in connecting manufacturers, retailers, and consumers positions it as a market leader.

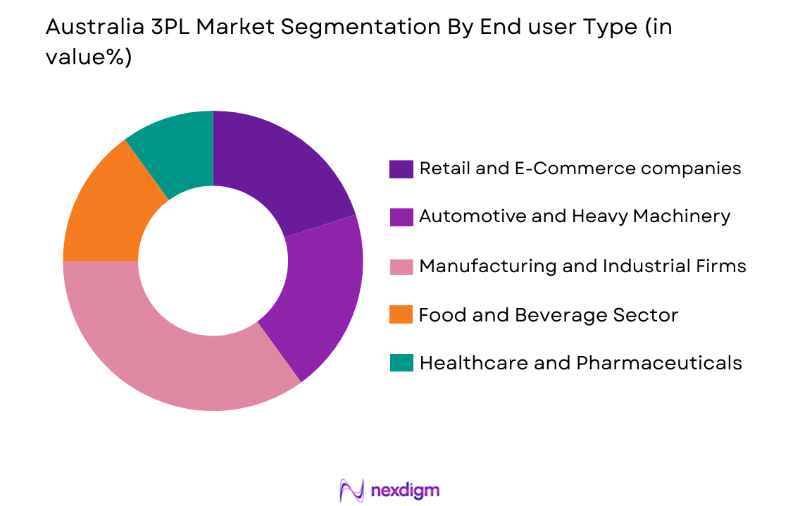

By End-User Segment

Australia 3PL market is segmented by end-user into retail and e-commerce companies, manufacturing and industrial firms, food and beverage sector, healthcare and pharmaceuticals, and automotive and heavy machinery. Recently, retail and e-commerce companies have a dominant market share due to factors such as rapid growth of online shopping, demand for faster delivery and same-day fulfillment, significant partnerships with logistics providers, integration of automated order processing systems, and need for flexible supply chain solutions. Investments in cold chain logistics for perishable goods, advanced inventory management, and last-mile distribution networks strengthen market dominance. Strategic collaborations between e-commerce platforms and third-party logistics providers ensure consistent service levels. Adoption of technology-enabled tracking systems improves operational efficiency. Regulatory compliance in packaging and transportation standards enhances reliability. Seasonal peaks in consumer demand require scalable logistics solutions. Data analytics facilitate predictive fulfillment planning. Expansion of regional distribution centers supports broader market coverage. Operational optimization reduces delivery costs and enhances customer satisfaction. Integration of warehouse and transportation services enables end-to-end supply chain management. Advanced robotics and AI streamline sorting and picking processes. Real-time performance monitoring improves efficiency and responsiveness. E-commerce growth drives high-frequency shipments, reinforcing the segment’s leading position.

Competitive Landscape

The Australia 3PL market is characterized by moderate consolidation with a few dominant players exerting significant influence over pricing, service innovation, and network expansion. Major global and regional logistics providers actively invest in technology integration, automation, and strategic partnerships. Mergers and acquisitions have enhanced operational capacity and geographic coverage. Companies focus on offering end-to-end solutions, including warehousing, transportation, and value-added services. Competitive differentiation is achieved through technological innovation, sustainability initiatives, and customer-centric supply chain models. The presence of multinational e-commerce and manufacturing clients drives the demand for advanced logistics capabilities. Providers are increasingly leveraging AI, IoT, and real-time data analytics to optimize operations. Strategic investments in cold chain, temperature-controlled storage, and urban micro-fulfillment centers strengthen competitive advantage. Focus on compliance, safety, and regulatory adherence ensures reliability. The competitive landscape continues to evolve with digital transformation and service diversification. Collaboration with technology firms enhances automation and operational efficiency. Continuous service innovation maintains market relevance. Network optimization and route planning are increasingly automated. Talent acquisition and workforce training further enhance operational performance. Brand recognition and reputation play a key role in client acquisition and retention.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (Approx.) | Fleet Size / Coverage |

| Toll Group | 1888 | Melbourne, Australia | ~ | ~ | ~ | ~ | ~ |

| Linfox | 1956 | Melbourne, Australia | ~ | ~ | ~ | ~ | ~ |

| DB Schenker Australia | 1872 | Sydney, Australia | ~ | ~ | ~ | ~ | ~ |

| DHL Supply Chain Australia | 1969 | Sydney, Australia | ~ | ~ | ~ | ~ | ~ |

| Kuehne + Nagel Australia | 1890 | Sydney, Australia | ~ | ~ | ~ | ~ | ~ |

Australia 3PL Market Analysis

Growth Drivers

E-Commerce Expansion and Omnichannel Integration

The Australia 3PL market growth is significantly driven by e-commerce expansion and omnichannel integration: rapidly increasing online retail sales, consumer preference for home delivery, and the demand for faster fulfillment have created substantial growth opportunities for third-party logistics providers. Retailers and e-commerce companies require flexible, scalable solutions to manage fluctuating order volumes efficiently, resulting in higher demand for outsourced transportation, warehousing, and value-added services. Investments in digital platforms, AI-driven order management, and automated warehouse solutions facilitate seamless integration between online and offline sales channels. Advanced last-mile delivery solutions, including urban micro-fulfillment centers, enhance speed and reliability while minimizing operational costs. Strategic collaborations between logistics providers and e-commerce platforms strengthen network reach and service capabilities. The increasing adoption of mobile commerce has intensified demand for real-time shipment tracking, predictive inventory management, and customer-centric fulfillment services. Companies are leveraging data analytics to optimize routing, reduce transit times, and improve operational efficiency. Regulatory support for infrastructure development and trade facilitation further reinforces market expansion. Sustainable and green logistics initiatives, including electric vehicle deployment and energy-efficient warehouses, add value while meeting consumer expectations. The combination of technology adoption, network expansion, and demand-driven service enhancement positions the Australia 3PL market for robust growth. Urban population density, regional connectivity, and strategic distribution hubs contribute to operational efficiency, supporting continuous expansion of logistics networks. Consumer demand for faster and reliable delivery options motivates providers to implement advanced transportation management systems. Cross-border e-commerce and import-export activities necessitate integrated supply chain solutions that bridge manufacturers, retailers, and end customers. The growth trajectory is underpinned by technological innovations, operational flexibility, and strategic partnerships across the logistics ecosystem, ensuring long-term scalability and competitive advantage.

Automation and Digitalization in Logistics Operations

technological adoption in warehouse management, transportation, and inventory systems has emerged as a primary driver of the Australia 3PL market. Companies increasingly implement robotics, AI, and IoT-enabled solutions to streamline picking, packing, sorting, and route optimization processes, reducing manual intervention and operational errors. Digital freight management platforms facilitate real-time tracking, predictive maintenance, and efficient fleet utilization. Adoption of warehouse automation solutions, including conveyor systems, automated storage, and retrieval systems, enhances throughput capacity while lowering costs. E-commerce growth intensifies demand for rapid fulfillment and accurate order processing, reinforcing investment in digital tools. Integration of supply chain visibility platforms enables enhanced collaboration among retailers, manufacturers, and logistics providers. Predictive analytics allows proactive inventory replenishment, improving service levels and reducing stockouts. Regulatory requirements for safety, security, and environmental compliance are better managed through digital monitoring systems. Cloud-based solutions provide scalable infrastructure for operational flexibility and remote monitoring. Data-driven insights improve route planning, resource allocation, and decision-making. Technology-enabled last-mile delivery solutions support urban and regional distribution efficiency. Cross-docking and real-time order management further optimize transportation networks. Sustainable operations are enhanced via energy-efficient automated systems. Companies leverage AI algorithms for demand forecasting and workflow optimization. The synergy of automation, AI, and IoT strengthens operational efficiency, reduces costs, and enhances competitiveness. Digitalization facilitates customer-centric services, transparency, and scalability, creating a resilient and adaptive 3PL ecosystem in Australia.

Market Challenges

Skilled Workforce Shortage in Logistics Operations

the Australia 3PL market faces challenges due to limited availability of trained personnel capable of managing complex supply chain systems and technologically advanced warehouse operations. The growing adoption of automated solutions, AI-driven systems, and digital freight management platforms necessitates specialized skills in robotics, IT, and process optimization. Recruitment and retention of qualified staff are critical for maintaining operational efficiency and ensuring compliance with safety and regulatory standards. Companies invest in workforce training programs, but demand often outpaces supply. Seasonal and peak demand fluctuations require flexible workforce management, adding complexity. High turnover rates and competition for skilled labor increase operational costs. Remote monitoring and digital supervision partially mitigate staffing gaps, but on-site expertise remains essential. Collaboration with vocational training institutions and targeted hiring strategies attempt to bridge skill gaps. Integration of AI and machine learning systems helps reduce dependency on manual intervention. Logistics providers are challenged to balance technology adoption with effective workforce utilization. Specialized skills are needed for cold chain logistics, hazardous goods handling, and multi-modal transportation management. Employee safety and regulatory compliance require continuous monitoring and expertise. Workforce shortages may slow expansion of new distribution centers and service offerings. Operational performance is directly affected by availability and competency of trained staff. Providers must invest in continuous professional development to maintain competitive advantage and service quality.

Infrastructure Limitations and Urban Congestion

the Australia 3PL market growth is impeded by constraints in transport infrastructure, road congestion, and limited warehousing space in major metropolitan areas. Dense urban environments create bottlenecks for freight movement, resulting in increased transit times, higher fuel consumption, and logistical inefficiencies. Expansion of distribution centers is challenged by land availability, zoning restrictions, and high real estate costs. Intermodal connectivity between ports, airports, and regional distribution hubs is often suboptimal, complicating timely deliveries. Regulatory compliance for heavy vehicle operations and traffic restrictions further restrict logistics operations. Investments in intelligent transport systems, route optimization software, and last-mile micro-distribution hubs partially mitigate these issues. Public-private partnerships support development of freight corridors and urban logistics solutions. Peak traffic periods affect fleet utilization and scheduling, necessitating adaptive planning. Infrastructure constraints may limit scalability of e-commerce and rapid delivery services. High demand in dense cities increases pressure on existing facilities and logistics networks. Adoption of sustainable delivery modes, including electric vehicles and cargo bikes, is constrained by infrastructure limitations. Integration of technology and data analytics improves operational planning but cannot fully overcome physical bottlenecks. Limited intermodal transfer points and port congestion impact supply chain efficiency. Urban congestion directly affects service quality, operational costs, and competitive positioning. Companies must invest in innovative distribution strategies, flexible routing, and micro-fulfillment centers to address infrastructure limitations while maintaining service reliability and customer satisfaction.

Opportunities

Cold Chain Logistics Expansion for Perishable Goods

Australia 3PL providers have a significant opportunity to expand temperature-controlled and specialized logistics services for perishable food, pharmaceuticals, and healthcare products. Rising consumer demand for fresh and frozen food delivery, coupled with stringent regulatory requirements, drives investments in refrigerated storage, transport vehicles, and monitoring technologies. Advanced cold chain solutions ensure product quality, safety, and compliance during storage and transit. Integration of IoT sensors, real-time temperature monitoring, and data analytics improves traceability and operational efficiency. Strategic partnerships with e-commerce, grocery, and pharmaceutical companies enable market penetration and service differentiation. Investment in regional cold storage hubs enhances distribution capabilities. Automation in refrigerated warehouses accelerates order fulfillment and reduces spoilage risks. Sustainable cold chain solutions, including energy-efficient refrigeration and solar-powered facilities, contribute to cost savings and environmental compliance. Logistics providers can leverage demand for home delivery of perishable goods to capture additional revenue streams. Consumer preference for high-quality, fresh products reinforces service adoption. Regulatory incentives for compliance and quality monitoring encourage expansion. Collaboration with technology firms enhances predictive maintenance and monitoring systems. Cold chain integration supports multi-temperature shipments and complex inventory management. Service differentiation through specialized handling increases client retention. Market growth is strengthened by rising healthcare, pharmaceutical, and online grocery sectors. Expansion of cold chain logistics underpins competitive advantage and market diversification.

Technology-Driven Supply Chain Visibility Solutions

the Australia 3PL market benefits from opportunities presented by implementing advanced digital platforms, real-time tracking systems, and AI-enabled analytics to enhance end-to-end supply chain transparency. Companies increasingly demand real-time monitoring of shipments, inventory levels, and order fulfillment to optimize operations and reduce costs. Integration of cloud-based TMS and WMS systems allows seamless coordination between warehouses, transportation networks, and end customers. Predictive analytics facilitates proactive decision-making, demand forecasting, and exception management. IoT sensors, RFID tags, and GPS tracking improve accuracy, traceability, and accountability across logistics networks. Collaboration with technology partners enhances platform capabilities and system integration. E-commerce growth necessitates robust visibility solutions to ensure timely delivery and customer satisfaction. Data-driven insights enable route optimization, resource allocation, and inventory planning. Regulatory requirements for product tracking and reporting reinforce adoption. Supply chain visibility solutions improve transparency for temperature-sensitive and high-value goods. Mobile applications and customer portals enhance real-time updates for clients and end-users. Integration of AI and machine learning automates exception handling and performance monitoring. Digital platforms enable predictive maintenance and operational efficiency. Strategic adoption of technology-driven visibility solutions strengthens competitive differentiation. Market expansion is supported by growing demand for transparent, reliable, and accountable logistics services. End-to-end visibility enhances operational agility, cost efficiency, and service quality, reinforcing long-term growth prospects.

Future Outlook

The Australia 3PL market is expected to continue robust growth over the next five years, driven by e-commerce expansion, technological advancements, and increasing demand for integrated logistics solutions. Investments in automation, AI, and real-time supply chain visibility will enhance operational efficiency. Regulatory support and infrastructure development will facilitate smoother freight movements and urban delivery. Demand-side factors, including consumer expectations for rapid and reliable delivery, will further incentivize expansion. Adoption of sustainable logistics practices and cold chain services will contribute to market diversification and long-term competitiveness.

Major Players

- Toll Group

- Linfox

- DB Schenker Australia

- DHL Supply Chain Australia

- Kuehne + Nagel Australia

- Ceva Logistics Australia

- Mainfreight Australia

- SDV Logistics

- P&O Trans Australia

- UPS Supply Chain Solutions Australia

- FedEx Logistics Australia

- Bolloré Logistics Australia

- CMA CGM Logistics Australia

- Agility Logistics Australia

- Rhenus Logistics Australia

Key Target Audience

- Retail and e-commerce companies

- Manufacturing and industrial firms

- Food and beverage companies

- Healthcare and pharmaceutical firms

- Automotive and heavy machinery companies

- Investments and venture capitalist firms

- Government and regulatory bodies

- Cold chain service providers

Research Methodology

Step 1: Identification of Key Variables

The study begins by identifying key variables including market size, growth drivers, challenges, segmentation criteria, and competitive dynamics. Data sources and metrics are defined to ensure comprehensive analysis.

Step 2: Market Analysis and Construction

Secondary and primary research is conducted to collect data on market trends, service types, end-user demand, and technological adoption. Quantitative models are applied to structure the market framework.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings are validated through expert consultations with industry professionals, logistics managers, and technology providers to ensure accuracy and relevance of insights.

Step 4: Research Synthesis and Final Output

Data is synthesized into a coherent report incorporating market size, segmentation, competitive landscape, and growth analysis, with visualizations and verified statistics for credibility.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of E-Commerce and Omnichannel Retail Operations

Investment in Digital Supply Chain Technologies

Rising Demand for Cost-Effective and Flexible Logistics Solutions - Market Challenges

High Capital Investment in Automation and Infrastructure

Regulatory Compliance and Trade Policy Complexity

Shortage of Skilled Logistics Workforce - Market Opportunities

Integration of AI and Robotics in Warehousing

Partnerships with Technology Providers for Smart Logistics

Growth in Cold Chain and Temperature-Sensitive Logistics - Trends

Adoption of Autonomous Vehicles in Logistics Operations

Increased Focus on Sustainability and Green Logistics

Expansion of Regional Distribution Hubs - Government Regulations

- SWOT Analysis of Key Competitors

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Warehousing and Storage Services

Transportation and Freight Management

Inventory Management Solutions

Reverse Logistics Services

Value-Added Services - By Platform Type (In Value%)

Cloud-Based Logistics Platforms

On-Premise TMS Systems

Hybrid Supply Chain Platforms

Integrated Freight Platforms

Automated Warehouse Management Systems - By Fitment Type (In Value%)

Standard 3PL Solutions

Customized Logistics Services

Contract Logistics Agreements

Dedicated Distribution Networks

Integrated Fulfillment Solutions - By EndUser Segment (In Value%)

Retail and E-Commerce Companies

Manufacturing and Industrial Firms

Food and Beverage Sector

Healthcare and Pharmaceuticals

- Market Share Analysis

- CrossComparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

Toll Group

Linfox

DB Schenker Australia

Kuehne + Nagel Australia

DHL Supply Chain Australia

Ceva Logistics Australia

Mainfreight Australia

SDV Logistics

P&O Trans Australia

UPS Supply Chain Solutions Australia

FedEx Logistics Australia

Bolloré Logistics Australia

CMA CGM Logistics Australia

Agility Logistics Australia

Rhenus Logistics Australia

- Retailers Expanding Outsourced Logistics Services

- Manufacturers Seeking Just-In-Time Inventory Management

- Pharmaceutical Companies Relying on Temperature-Controlled Solutions

- E-Commerce Platforms Driving Demand for Rapid Fulfillment

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now