Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Australia agricultural equipment market reached approximately USD ~ billion based on a recent historical assessment supported by data from national agricultural machinery sales statistics and industry associations. Demand is driven by large-scale mechanized farming operations, precision agriculture adoption, and high-capacity machinery requirements in grain, livestock, and horticulture production systems. Government farm modernization incentives and ongoing replacement cycles of aging tractors and harvesters further sustain equipment purchases across commercial farms and agricultural contractors nationwide.

New South Wales, Victoria, and Western Australia dominate Australia agricultural equipment demand due to expansive grain production, large farm sizes, and high mechanization intensity across cropping regions. These states host major agricultural machinery dealerships, service infrastructure, and equipment financing networks, enabling sustained procurement. Western Australia’s broadacre wheat belt and New South Wales mixed farming systems require high-horsepower tractors and harvesters, while Victoria’s horticulture and dairy sectors drive demand for specialized equipment and precision farming technologies.

Market Segmentation

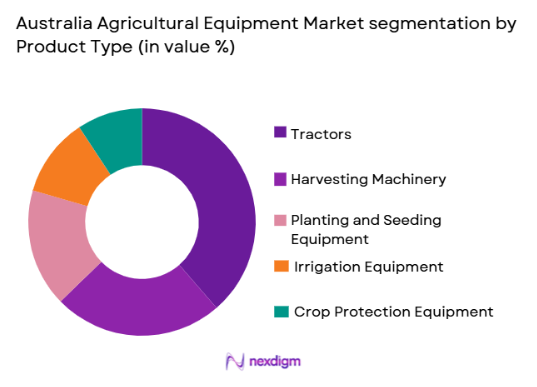

By Product Type

Australia agricultural equipment market is segmented by product type into tractors, harvesting machinery, planting and seeding equipment, irrigation equipment, and crop protection equipment. Recently, tractors has a dominant market share due to factors such as widespread applicability across farm operations, high replacement frequency, strong dealer networks, and suitability for Australia’s large-scale mechanized farming. High-horsepower tractors are essential for broadacre grain production and livestock operations, while utility tractors support horticulture and mixed farms. Their versatility in towing implements, land preparation, and transport tasks makes tractors indispensable across regions, ensuring sustained procurement demand.

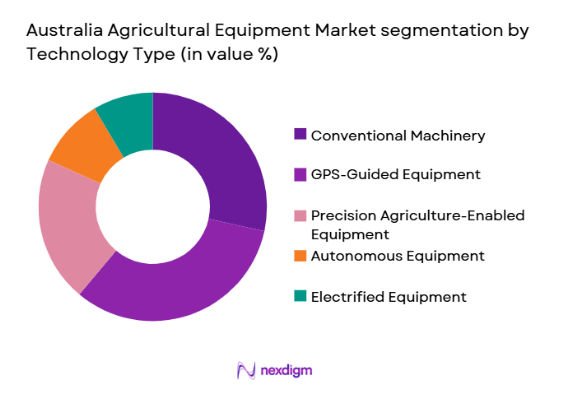

By Technology Type

Australia agricultural equipment market is segmented by technology type into conventional machinery, GPS-guided equipment, precision agriculture-enabled equipment, autonomous equipment, and electrified equipment. Recently, GPS-guided equipment has a dominant market share due to factors such as widespread adoption of satellite guidance for broadacre farming, improved input efficiency, and strong compatibility with existing machinery fleets. Australian farms operate over large land parcels requiring accurate seeding, spraying, and harvesting, making GPS systems essential for productivity and cost control, thereby driving dominance over emerging automation technologies.

Competitive Landscape

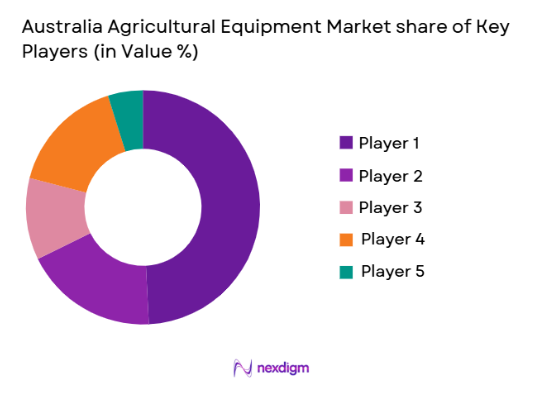

Australia agricultural equipment market is moderately consolidated, with global manufacturers and regional distributors dominating machinery supply through extensive dealer networks and service capabilities. Major multinational firms such as John Deere, CNH Industrial, and AGCO maintain strong market presence through localized manufacturing partnerships, financing programs, and precision agriculture technology integration. Competitive advantage is shaped by aftersales support coverage, equipment reliability in harsh farming environments, and advanced guidance and automation solutions tailored for broadacre operations.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Distribution Network Strength |

| John Deere | 1837 | USA | ~ | ~ | ~ | ~ | ~ |

| CNH Industrial | 2013 | UK | ~ | ~ | ~ | ~ | ~ |

| AGCO Corporation | 1990 | USA | ~ | ~ | ~ | ~ | ~ |

| Kubota | 1890 | Japan | ~ | ~ | ~ | ~ | ~ |

| Claas | 1913 | Germany | ~ | ~ | ~ | ~ | ~ |

Australia Agricultural Equipment Market Analysis

Growth Drivers

Large-Scale Mechanized Farming Expansion:

Australia’s agricultural production relies heavily on extensive landholdings and low labor density, encouraging investment in high-capacity agricultural equipment capable of covering vast areas efficiently. Grain farms in Western Australia and New South Wales often exceed thousands of hectares, necessitating high-horsepower tractors, wide-span seeders, and advanced combine harvesters to maintain operational efficiency. Mechanization reduces dependence on seasonal labor and supports timely planting and harvesting cycles critical for yield optimization. Farmers increasingly adopt multi-functional machinery capable of performing several operations, improving capital utilization. Broadacre farming also requires robust equipment engineered for harsh climatic conditions and sandy or heavy soils, reinforcing demand for premium machinery. Government modernization incentives and financing schemes support capital investment in mechanization upgrades. Replacement demand for aging machinery fleets further drives purchases as farms seek higher productivity and reliability. Increasing global food demand and export-oriented grain production reinforce the need for scalable mechanized agriculture systems. Consequently, large-scale mechanization remains a fundamental driver sustaining equipment demand across Australian agriculture.

Precision Agriculture and Digital Farming Adoption:

Australian agriculture increasingly integrates digital technologies to improve productivity, resource efficiency, and environmental sustainability, driving demand for precision agriculture-enabled equipment. GPS guidance, variable-rate application, and telematics systems enable farmers to optimize seed placement, fertilizer use, and chemical spraying across heterogeneous fields. Precision technologies reduce input costs and environmental impact, aligning with regulatory and sustainability objectives. Data-driven farm management platforms integrate machinery operations with soil, yield, and weather analytics, enhancing decision-making. Large farm sizes amplify the economic benefits of precision agriculture, accelerating adoption rates. Equipment manufacturers embed sensors, automation modules, and connectivity features into tractors and implements, creating value-added offerings. Contractors providing precision farming services also stimulate equipment demand. Government support for sustainable farming practices encourages technology integration in machinery purchases. Over time, digital farming adoption transforms agricultural equipment from purely mechanical assets into intelligent productivity systems, sustaining strong market growth.

Market Challenges

High Capital Cost of Advanced Agricultural Machinery:

Modern agricultural equipment incorporating precision technology, automation, and high horsepower capabilities involves substantial upfront investment, creating affordability constraints for many Australian farms. Even large commercial operations face financial risk when commodity prices fluctuate or seasonal yields decline due to drought. Financing availability varies across regions, particularly in remote farming areas with limited lender presence. Smaller family farms struggle to justify investment in high-end machinery, leading to delayed replacement cycles and reliance on older equipment. Maintenance and repair costs of technologically complex machinery further increase ownership expenses. Imported machinery also faces currency fluctuations and shipping costs, affecting purchase decisions. Contractors must achieve high utilization rates to recover investment, increasing operational risk. Insurance and depreciation costs add financial pressure over equipment lifecycles. Consequently, high capital intensity remains a persistent barrier limiting widespread adoption of advanced agricultural machinery.

Service and Maintenance Constraints in Remote Farming Regions:

Australia’s agricultural activity occurs across vast rural regions where access to technical service infrastructure is limited, posing operational challenges for machinery owners. Equipment downtime during critical planting or harvesting windows can significantly affect farm productivity and revenue. Dealer networks and spare parts logistics are concentrated near major agricultural hubs, leaving remote farms dependent on long-distance support. Skilled technicians trained in advanced precision agriculture systems are scarce in rural areas, complicating maintenance of modern machinery. Transportation costs for equipment servicing are high due to geographic isolation. Harsh operating environments accelerate wear and tear, increasing maintenance frequency. Farmers often retain older machinery for reliability and ease of repair, slowing adoption of newer technologies. Limited digital connectivity in some regions restricts remote diagnostics and telematics support capabilities. Overall, service infrastructure constraints hinder optimal utilization and modernization of agricultural equipment fleets.

Opportunities

Autonomous and Robotics-Enabled Farm Equipment Development:

Australia’s large farms and labor shortages create strong conditions for adoption of autonomous agricultural machinery capable of operating continuously with minimal human intervention. Autonomous tractors, robotic harvesters, and automated spraying systems can significantly improve productivity and reduce labor dependence. Remote operation technologies enable centralized fleet management across dispersed fields, enhancing operational efficiency. Australian research institutions and agritech firms are actively developing robotics suited to broadacre cropping and horticulture applications. Integration of artificial intelligence with machinery navigation and sensing systems supports precise field operations. Autonomous equipment also enables night-time farming and extended working hours. Contractors offering autonomous services could accelerate market adoption. Regulatory frameworks supporting safe deployment of agricultural robotics are evolving, facilitating commercialization. Over time, robotics-enabled equipment presents a transformative opportunity to reshape agricultural mechanization in Australia.

Sustainable and Low-Emission Agricultural Machinery Adoption:

Environmental sustainability goals and emissions regulations are driving innovation in agricultural machinery powertrains and materials, creating opportunities for electrified and low-emission equipment. Electric and hybrid tractors reduce fuel consumption and greenhouse gas emissions, aligning with climate policies and carbon reduction targets. Lightweight materials and energy-efficient hydraulics improve equipment efficiency and reduce soil compaction. Renewable energy integration on farms enables charging of electric machinery, supporting sustainable operations. Manufacturers developing low-emission machinery gain competitive advantage in environmentally conscious markets. Government incentives promoting sustainable agriculture encourage adoption of green equipment technologies. Export-oriented producers seek sustainability certification, requiring low-emission farming practices supported by advanced machinery. Electrification is particularly suited to horticulture, viticulture, and controlled-environment agriculture. As sustainability becomes integral to agricultural production, demand for environmentally optimized machinery is expected to expand significantly.

Future Outlook

Australia agricultural equipment market is expected to expand steadily over the next five years supported by continued mechanization, digital farming integration, and sustainability-driven innovation. Autonomous machinery, electrified powertrains, and precision agriculture platforms will reshape equipment capabilities and productivity. Government support for modern farming practices and emissions reduction will encourage technology adoption. Demand from large-scale grain and livestock operations alongside horticulture modernization will sustain equipment procurement and replacement cycles nationwide.

Major Players

- John Deere Australia

- CNH Industrial Australia

- AGCO Corporation Australia

- Kubota Australia

- Claas Harvest Centre Australia

- JCB Agriculture Australia

- Kuhn Australia

- Lemken Australia

- Hardi Australia

- Kverneland Group Australia

- Horsch Australia

- Trimble Agriculture Australia

- Topcon Agriculture Australia

- Croplands Equipment

- Auscott Precision Farming

Key Target Audience

- Agricultural machinery manufacturers

- Farm equipment distributors and dealers

- Precision agriculture technology providers

- Agricultural contractors and service providers

- Commercial farming enterprises

- Investments and venture capitalist firms

- Government and regulatory bodies

- Agricultural equipment financing institutions

Research Methodology

Step 1: Identification of Key Variables

Primary variables including machinery categories, technology adoption levels, farm size distribution, and mechanization intensity were identified. Regional agricultural production patterns and equipment utilization factors were mapped to establish market structure and demand drivers across Australia.

Step 2: Market Analysis and Construction

Market sizing integrated agricultural machinery sales data, farm mechanization statistics, and manufacturer revenue segmentation. Demand patterns were modeled across product and technology segments using equipment deployment density and replacement cycle analysis.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including machinery distributors, agritech specialists, and large-scale farmers validated assumptions regarding technology adoption, purchasing behavior, and equipment utilization trends across major agricultural regions.

Step 4: Research Synthesis and Final Output

Validated datasets and qualitative insights were synthesized into market segmentation, competitive landscape, and growth projections. Analytical frameworks ensured consistency between mechanization trends, technology evolution, and regional agricultural dynamics.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of large-scale mechanized farming operations

Adoption of precision agriculture and smart farming technologies

Labor shortages driving automation and mechanization - Market Challenges

High capital cost of advanced agricultural machinery

Volatility in agricultural commodity prices affecting investment

Maintenance and service constraints in remote farming regions - Market Opportunities

Growth in autonomous and robotics-enabled farm equipment

Integration of digital farm management platforms with machinery

Demand for sustainable and low-emission agricultural equipment - Trends

Shift toward data-driven precision farming ecosystems

Rising use of autonomous tractors and robotic harvesters

Electrification of small and mid-size farm machinery

Integration of telematics and remote diagnostics

Growth of equipment-as-a-service business models - Government Regulations & Defense Policy

Farm mechanization subsidy and rebate programs

Emissions and environmental compliance standards for machinery

Workplace safety and operator certification regulations - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Tractors

Harvesting Machinery

Planting and Seeding Equipment

Irrigation Systems

Crop Protection Equipment - By Platform Type (In Value%)

Wheeled Equipment Platforms

Tracked Equipment Platforms

Self-Propelled Systems

Mounted and Trailed Implements

Autonomous Equipment Platforms - By Fitment Type (In Value%)

OEM Integrated Equipment

Aftermarket Attachments

Retrofit Automation Kits

Modular Implement Systems

Precision Upgrade Packages - By EndUser Segment (In Value%)

Broadacre Crop Farms

Horticulture and Viticulture Farms

Livestock and Dairy Farms

Agricultural Contractors

Government and Research Farms - By Procurement Channel (In Value%)

Direct Manufacturer Sales

Dealer and Distributor Networks

Cooperative Purchasing Programs

Government Subsidy Schemes

Online Equipment Marketplaces - By Material / Technology (in Value %)

Precision Agriculture Technologies

GPS and Guidance Systems

Electrified and Hybrid Powertrains

Advanced Hydraulic Systems

Lightweight Composite Structures

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Product Portfolio Breadth, Technology Integration Level, Local Manufacturing Presence, Dealer Network Strength, Precision Farming Capability, AfterSales Service Coverage, Pricing Tier Positioning, Customization Capability, Sustainability Features, Automation Readiness)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

John Deere Australia

CNH Industrial Australia

AGCO Corporation Australia

Kubota Australia

Claas Harvest Centre Australia

JCB Agriculture Australia

Kuhn Australia

Lemken Australia

Hardi Australia

Kverneland Group Australia

Horsch Australia

Trimble Agriculture Australia

Topcon Agriculture Australia

Croplands Equipment

Auscott Precision Farming

- Broadacre farms prioritizing high-capacity and automated machinery

- Horticulture farms adopting precision and specialty equipment

- Contractors investing in multi-functional and high-utilization fleets

- Research farms piloting advanced and sustainable technologies

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now