Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Australia AI infrastructure market is valued at approximately USD ~ billion based on a recent historical assessment, driven by hyperscale data center expansion, enterprise AI adoption, and national digital economy initiatives. Investments in GPU-accelerated computing, high-performance storage, and advanced networking systems support AI training and inference workloads across industries. Growth of cloud-based AI services and research computing programs further accelerates deployment of specialized AI servers and supporting data center infrastructure nationwide.

Sydney and Melbourne dominate the Australia AI infrastructure market due to concentration of hyperscale data centers, enterprise headquarters, and connectivity hubs. These cities host major cloud regions, financial institutions, and technology firms requiring high-performance AI computing capacity. Canberra supports government and defense AI programs, while Brisbane and Perth are emerging digital infrastructure hubs linked to subsea connectivity and resource industry demand. Proximity to users, power availability, and fiber networks reinforces regional leadership in AI infrastructure deployment.

Market Segmentation

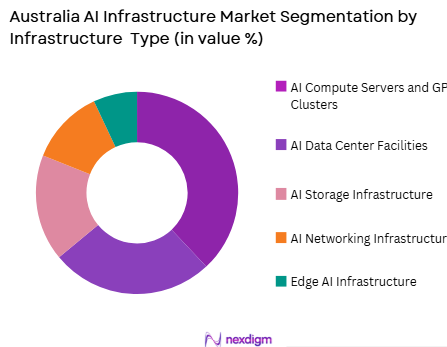

By Infrastructure Type

Australia AI Infrastructure market is segmented by product type into AI compute servers and GPU clusters, AI storage infrastructure, AI networking infrastructure, edge AI infrastructure, and AI data center facilities. Recently, AI compute servers and GPU clusters has a dominant market share due to factors such as rapid generative AI adoption, hyperscale cloud expansion, and enterprise demand for accelerated computing. Organizations deploy GPU-dense servers for model training, simulation, and analytics workloads. Hyperscale providers invest heavily in GPU clusters within Australian regions to support local AI services. Research institutions and government AI initiatives also procure high-performance compute systems. Increasing computational intensity of AI workloads sustains highest capital allocation toward GPU-based compute infrastructure compared with other AI infrastructure segments.

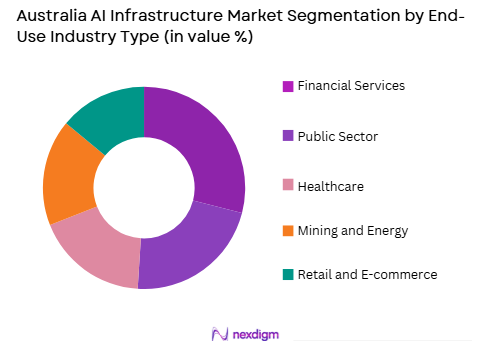

By End-Use Industry

Australia AI Infrastructure market is segmented by end-use industry into financial services, healthcare, public sector, mining and energy, and retail and e-commerce. Recently, financial services has a dominant market share due to factors such as strong adoption of AI analytics, fraud detection, and algorithmic decision systems across banks and insurers. Financial institutions deploy GPU-accelerated infrastructure for risk modeling and customer analytics. Strict data governance requirements encourage domestic AI infrastructure deployment. Large financial enterprises invest in private and hybrid AI computing environments. Integration of AI into digital banking and trading platforms increases compute demand. These factors position financial services as the leading industry consumer of AI infrastructure capacity in Australia.

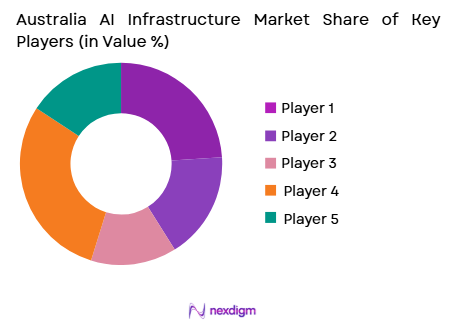

Competitive Landscape

The Australia AI infrastructure market is moderately consolidated with dominance of global hyperscale cloud providers and specialized data center operators, complemented by domestic technology service firms. Large-scale GPU cluster deployments and hyperscale facilities define competitive positioning. Partnerships between cloud platforms, hardware vendors, and colocation providers shape infrastructure expansion. Global providers lead in AI platform breadth and compute scale, while local firms leverage regional presence and regulatory alignment to serve enterprise and government AI workloads.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Australia AI Data Center Presence |

| Amazon Web Services | 2006 | Seattle, USA | ~ | ~ | ~ | ~ | ~ |

| Microsoft | 1975 | Redmond, USA | ~ | ~ | ~ | ~ | ~ |

| 1998 | Mountain View, USA | ~ | ~ | ~ | ~ | ~ | |

| NextDC | 2010 | Brisbane, Australia | ~ | ~ | ~ | ~ | ~ |

| Equinix | 1998 | Redwood City, USA | ~ | ~ | ~ | ~ |

Australia AI Infrastructure Market Analysis

Growth Drivers

Enterprise and Government Adoption of AI-Driven Digital Services and Analytics Platforms

Australia’s enterprises and public sector organizations are rapidly deploying artificial intelligence across digital services, operational analytics, cybersecurity, and automation initiatives, creating sustained demand for specialized AI infrastructure nationwide. Financial institutions apply AI models for fraud detection, credit risk, and customer analytics, requiring GPU-accelerated compute clusters and secure data environments. Government agencies deploy AI for defense analytics, public services optimization, and smart city systems, increasing domestic compute infrastructure investment. Healthcare providers use AI for imaging diagnostics and genomics analysis, expanding high-performance computing requirements. Mining and energy firms adopt AI for exploration modeling and predictive maintenance, driving regional AI infrastructure deployment. Strict data governance and sovereignty requirements encourage local hosting of AI workloads. Enterprises increasingly shift from experimentation to production AI, expanding infrastructure scale. Integration of AI into enterprise software platforms increases compute and storage intensity. Cloud providers expand GPU capacity in Australian regions to meet enterprise demand. These adoption dynamics collectively sustain strong growth of AI infrastructure across sectors and geographies.

Hyperscale Cloud Expansion and Generative AI Workload Growth Across Industries

Rapid expansion of hyperscale cloud regions and proliferation of generative AI applications in Australia are driving significant deployment of AI servers, GPU clusters, and supporting data center infrastructure. Cloud providers invest in new availability zones equipped with high-density GPU compute and advanced networking to support AI services. Enterprises adopt generative AI for content creation, automation, and decision support, increasing demand for large-scale training and inference capacity. AI-driven software platforms, digital media, and gaming services generate intensive compute workloads requiring scalable cloud infrastructure. Data localization regulations favor domestic hosting of AI models and datasets. Growth of AI startups and research programs expands GPU demand. Edge AI integration in telecom and industrial systems increases distributed infrastructure nodes. High-performance storage and networking upgrades accompany GPU cluster expansion. Continuous growth in AI service consumption across industries sustains hyperscale infrastructure investment. These factors reinforce long-term expansion of AI infrastructure capacity in Australia.

Market Challenges

Power Availability, Energy Costs, and Sustainability Constraints in AI Data Centers

Expansion of AI infrastructure in Australia faces constraints related to high electricity consumption, energy costs, and sustainability requirements associated with GPU-intensive data centers. AI training clusters consume substantial power, increasing operational expenses and environmental impact concerns. Availability of grid capacity near major urban demand centers limits new facility deployment. Renewable energy integration is necessary to meet sustainability targets but requires infrastructure investment. Cooling requirements for high-density GPU racks increase water and energy usage. Data center operators must balance expansion with carbon reduction commitments. Energy price volatility affects infrastructure economics. Remote regions suitable for renewable power may lack connectivity and workforce access. Regulatory frameworks governing energy efficiency influence facility design. These constraints complicate rapid scaling of AI data center capacity across Australia.

Talent Shortages and Limited Domestic Semiconductor Supply Chain

Australia’s AI infrastructure ecosystem faces challenges related to limited domestic semiconductor manufacturing and shortages of specialized engineering talent required for AI hardware deployment and operation. Dependence on imported GPUs and servers exposes infrastructure projects to global supply constraints and pricing volatility. Lack of local chip fabrication reduces technology sovereignty and supply flexibility. Skilled workforce shortages in data center engineering, AI hardware optimization, and high-performance computing operations limit deployment capacity. Competition for talent from global technology firms increases costs. Training and education pipelines are still developing. Infrastructure operators rely on international vendors for advanced hardware support. These structural limitations slow domestic AI infrastructure scaling. Building local expertise and supply capability remains a long-term challenge.

Opportunities

Renewable-Powered AI Data Centers and Green Infrastructure Leadership

Australia has significant opportunity to develop renewable-powered AI data centers leveraging abundant solar and wind resources to create sustainable AI infrastructure leadership globally. Co-location of data centers with renewable generation can reduce energy costs and carbon footprint. Green AI infrastructure aligns with national sustainability and climate goals. Hyperscale providers increasingly prioritize renewable energy sourcing for facilities. Regional renewable hubs offer land and power availability for large AI campuses. Export of green cloud services and AI compute capacity can attract international customers. Government incentives for clean energy infrastructure support development. Integration of energy storage and smart grids enhances reliability. Sustainable AI infrastructure differentiates Australia in global cloud markets. This opportunity enables expansion of AI capacity while meeting environmental commitments.

Regional AI Infrastructure Hubs Supporting Asia-Pacific Digital Economy

Australia can position itself as a regional AI infrastructure hub serving Asia-Pacific markets through advanced connectivity, stable regulatory environment, and proximity to emerging digital economies. Subsea cable connectivity links Australia with Asia and North America, enabling cross-border data flows. Hyperscale providers can deploy regional AI compute zones in Australia serving international workloads. Strong data governance and political stability attract multinational enterprises. Growth of AI services in Asia-Pacific increases demand for regional infrastructure. Export of AI cloud services expands digital economy revenues. Partnerships with global technology firms support hub development. Regional positioning diversifies infrastructure utilization beyond domestic demand. This opportunity strengthens Australia’s role in global AI infrastructure networks.

Future Outlook

Australia AI infrastructure market is expected to expand steadily as enterprise AI adoption, hyperscale cloud investment, and generative AI workloads accelerate demand for GPU-enabled computing and data center capacity. Renewable energy integration will support sustainable infrastructure scaling. Government AI strategies and digital economy programs will encourage domestic deployment. Regional connectivity and cloud hub positioning will further expand AI infrastructure investment across the country.

Major Players

- Amazon Web Services

- Microsoft

- NextDC

- Equinix

- Digital Realty

- Macquarie Data Centres

- AirTrunk

- Oracle

- IBM

- Nvidia

- Dell Technologies

- Hewlett Packard Enterprise

- Cisco Systems

- Lenovo

Key Target Audience

- Hyperscale cloud providers

- Data center operators

- Telecommunications operators

- Enterprise IT service providers

- Financial institutions

- Investments and venture capitalist firms

- Government and regulatory bodies

- AI software platform companies

Research Methodology

Step 1: Identification of Key Variables

Key variables include AI infrastructure spending, GPU deployment capacity, hyperscale data center construction, enterprise AI adoption rates, and industry demand patterns. Variables are mapped across infrastructure segments and regional hubs to define market structure.

Step 2: Market Analysis and Construction

Supply-side analysis evaluates cloud provider expansion, GPU hardware deployment, and data center investments, while demand-side analysis examines enterprise and public sector AI adoption. Data triangulation constructs market size and segmentation estimates.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts from cloud providers, data center operators, and AI technology firms validate assumptions on infrastructure growth, technology adoption, and regulatory impact. Feedback refines segmentation shares and competitive positioning.

Step 4: Research Synthesis and Final Output

Validated quantitative datasets and qualitative insights are synthesized into infrastructure forecasts, competitive analysis, and strategic outlook. Consistency checks ensure alignment across market size, segmentation, and trend narratives.

Executive Summary

Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Strong investment in AI and digital infrastructure across industries

Expansion of hyperscale cloud and AI data centers

AI adoption in mining, energy, and healthcare sectors - Market Challenges

High energy consumption and cooling requirements

Dependence on imported AI accelerators and hardware

Geographic dispersion increasing infrastructure cost - Market Opportunities

Sovereign AI infrastructure and national HPC systems

AI deployment in resource and industrial sectors

Edge AI for remote and autonomous operations - Trends

Adoption of liquid-cooled high-density AI clusters

Integration of AI accelerators in telecom and edge

Convergence of AI and cloud infrastructure ecosystems - Government regulations

National AI and digital economy strategies

Data sovereignty and critical infrastructure policies

High-performance computing and research funding - SWOT analysis

- Porters five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

AI Training Supercomputing Clusters

GPU and Accelerator Servers

AI Storage and Data Infrastructure

AI Networking and Interconnect Systems

Edge AI Infrastructure Platforms - By Platform Type (In Value%)

Hyperscale AI Data Centers

Enterprise AI Platforms

Telecom AI Cloud Infrastructure

Research and Academic HPC

Autonomous Systems Compute Platforms - By Fitment Type (In Value%)

New AI Data Center Deployment

AI Cluster Expansion

Accelerator Retrofit Integration

Modular AI Infrastructure Blocks

Edge AI Deployment Units - By End User Segment (In Value%)

Cloud and Internet Platforms

Telecommunications Operators

Mining and Energy Companies

Healthcare and Life Sciences Organizations

Government and Research Institutes - By Procurement Channel (In Value%)

Direct OEM and Accelerator Vendors

Cloud Provider Procurement

System Integrator Deployment

Telecom Infrastructure Contracts

Government AI Programs

- Market Share Analysis

- Cross Comparison Parameters (AI Compute Density, Accelerator Performance per Watt, Training Throughput Capability, Inference Latency Optimization, Memory Bandwidth and Capacity, Interconnect Bandwidth and Topology, Cluster Scalability Architecture, Cooling and Thermal Management, Power Consumption per Rack, AI Software Stack Compatibility, Deployment Flexibility, Sovereign AI Compliance Readiness)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

NextDC

AirTrunk

Macquarie Data Centres

Equinix Australia

Amazon Web Services Australia

Microsoft Azure Australia

Google Cloud Australia

NVIDIA Australia

Hewlett Packard Enterprise Australia

Dell Technologies Australia

Lenovo Australia

Cisco Systems Australia

Fujitsu Australia

DXC Technology Australia

Telstra

- Cloud providers expanding AI compute capacity

- Telecom operators deploying AI network infrastructure

- Mining and energy firms adopting AI compute systems

- Government and academia investing in national HPC

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now