Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Australian Air-to-Air Refueling System market is expected to witness substantial growth due to increasing demand for strategic air mobility and air defense capabilities. In 2023, the Australian Department of Defence allocated significant funding toward enhancing air-to-air refueling capabilities, especially as part of the broader defense modernization initiatives. This market size is primarily driven by the strategic requirement for long-range fighter aircraft operations and greater interoperability with allied forces in the Indo-Pacific region. The Australian Air Force (RAAF) has strategically expanded its fleet of refueling aircraft, such as the KC-30A MRTT, which significantly contributes to the market size. The growing need for advanced systems and the shift toward integrating more autonomous refueling systems further accelerates the market’s expansion.

Australia stands as the dominant player in the regional Air-to-Air Refueling System market. The country’s strategic location in the Indo-Pacific region and its defense partnerships with allies such as the United States and Japan reinforce the demand for advanced refueling systems. The capital cities, particularly Canberra (for policy-making) and major bases like RAAF Base Amberley, are central to the deployment and procurement of these systems. Australia’s defense modernization programs and increasing involvement in regional security partnerships, combined with its global defense alliances, ensure its strong position in the market. This dominance is also attributed to Australia’s significant investments in indigenous technological advancements and the integration of next-generation refueling systems in its military fleet.

Market Segmentation

By System Type

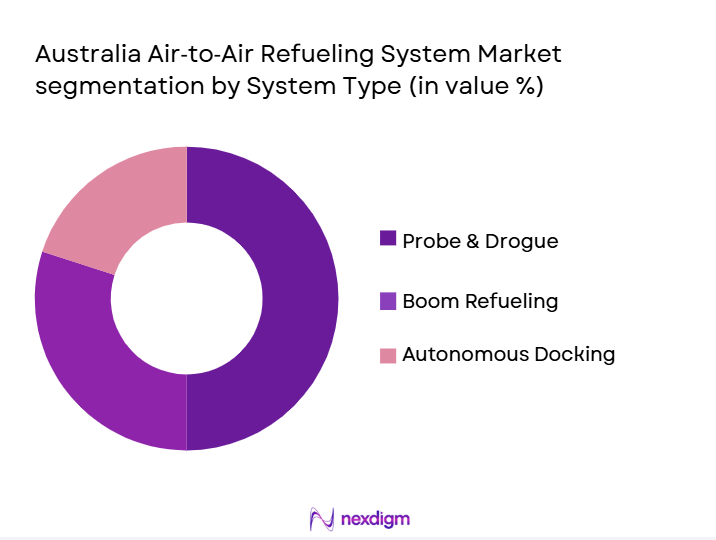

The Australian Air-to-Air Refueling System market is segmented into probe & drogue, boom refueling, and autonomous docking systems. Among these, the boom refueling system currently dominates the market. This dominance is largely due to the RAAF’s integration of the Boeing KC-30A MRTT, which employs the boom refueling technology. This system is preferred for its ability to refuel larger aircraft such as the F/A-18F Super Hornet and the E-7A Wedgetail. The boom system provides faster refueling speeds and is highly efficient for military-grade operational needs. Additionally, the ongoing development of autonomous refueling technologies, while promising, has not yet surpassed the operational reliability and widespread acceptance of the boom refueling technology.

By Platform Type

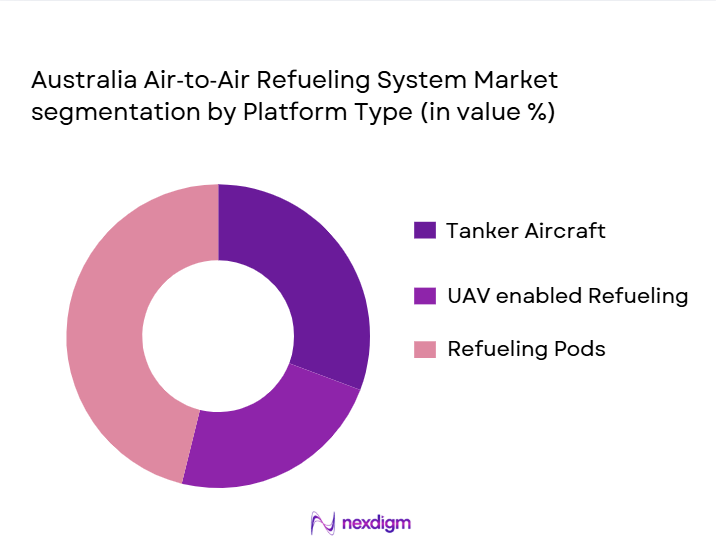

The platform type segmentation includes tanker aircraft, UAV-enabled refueling systems, and refueling pods. Tanker aircraft remain the dominant platform, particularly the Boeing KC-30A MRTT. These aircraft are capable of refueling a wide variety of military jets, transport aircraft, and even allied forces’ planes. Their versatility, combined with the RAAF’s investment in this platform, ensures that tanker aircraft hold a significant market share. UAV-enabled refueling systems, although growing, are still in early adoption phases due to technological and regulatory challenges, which limits their dominance in the market.

Competitive Landscape

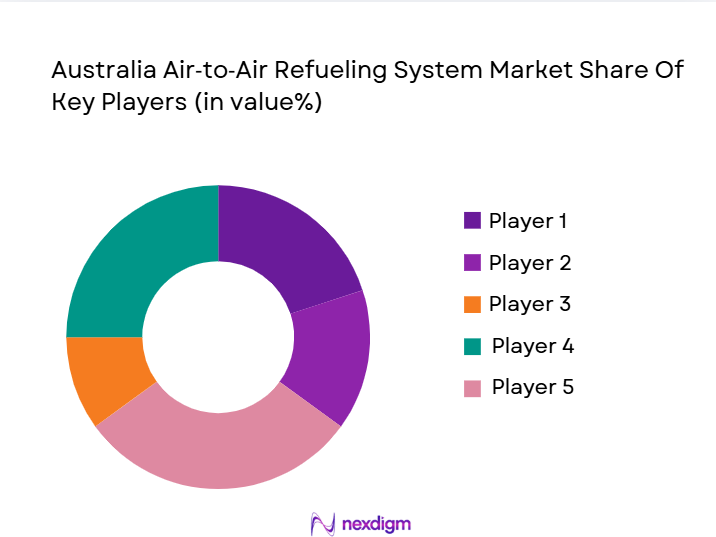

The Australian Air-to-Air Refueling System market is dominated by a few major players, including global giants like Boeing and Airbus. These companies hold a significant share due to their well-established presence and continued technological innovations in the refueling sector. Boeing, in particular, leads with the KC-30A MRTT, which is the primary refueling platform for the Australian Defence Force (ADF). Other players like Cobham and Safran also contribute through their probe & drogue and refueling component technologies. The competitive dynamics are shaped by the need for high interoperability between systems, particularly given Australia’s global defense alliances and participation in multinational exercises and operations.

| Player | Establishment Year | Headquarters | Technology Offering | Market Focus | Global Defense Alliances | Product Focus |

| Boeing | 1916 | Chicago, USA | ~ | ~ | ~ | ~ |

| Airbus Defence & Space | 2000 | Toulouse, France | ~ | ~ | ~ | ~ |

| Cobham | 1934 | Dorset, UK | ~ | ~ | ~ | ~ |

| Safran | 2005 | Paris, France | ~ | ~ | ~ | ~ |

| Lockheed Martin | 1912 | Bethesda, USA | ~ | ~ | ~ | ~ |

Australia Air‑to‑Air Refueling System Market Analysis

Growth Drivers

Extended Range Requirement

In 2024, Australia’s defense forces face an increasing demand for long-range operational capabilities to enhance military presence in the Indo-Pacific region. The Australian government’s defense white paper highlights a need for modernized and capable refueling systems to support fighter jets, surveillance aircraft, and strategic bombers in extended-range missions. The Royal Australian Air Force (RAAF) is particularly focused on extending operational reach, with the KC-30A Multi-Role Tanker Transport (MRTT) aircraft integrated into RAAF’s fleet, which enhances the combat range of Australian fighter jets like the F/A-18 Hornet. According to the Australian Department of Defence’s 2023 budget estimates, funding of over AUD ~ billion is allocated towards upgrading capabilities like aerial refueling systems to ensure Australia maintains strategic air power across its vast operational geography.

Force Projection Needs

The Australian government is committed to improving force projection capabilities in the Indo-Pacific, particularly in light of rising regional tensions. As of 2024, Australia’s defense spending is projected to increase by AUD ~ billion over the next five years to support the strategic capability of the Australian Defence Force (ADF). This increase is aimed at modernizing Australia’s air refueling assets to enable more flexible and scalable force deployment capabilities. The ongoing participation in international missions, including in the South China Sea and Middle East, underscores the need for air-to-air refueling systems to maintain extended operational capacity for Australian air assets deployed globally. Australia’s focus on maintaining a credible deterrent force within its defense strategies reinforces the increased emphasis on air mobility systems.

Market Challenges

Interoperability Standards

Australia’s need for interoperability within the Indo-Pacific region has driven the demand for air-to-air refueling systems capable of working seamlessly with allied forces. In 2024, interoperability remains a significant challenge as countries like the US, Japan, and South Korea deploy different refueling systems with varied protocols and interfaces. For instance, Australia’s KC-30A MRTT aircraft must be compatible with U.S. aircraft such as the F-35 and P-8 Poseidon. In 2024, the Australian government continues to prioritize interoperability standards, collaborating on joint training and standardization efforts under programs such as the Pacific Defence Cooperation Agreement. The ability to work in unison with international partners in joint operations highlights the complexity of ensuring systems meet both national and allied requirements. This emphasis on joint-force integration results in additional challenges surrounding system upgrades and training to meet cross-border standards.

Certification & Training Costs

In 2024, one of the major obstacles to the widespread adoption of advanced refueling systems is the high cost of certification and training for both pilots and ground crews. Air-to-air refueling systems, such as the KC-30A MRTT, require specialized training programs to ensure operational effectiveness. The Australian Department of Defence’s Annual Report states that training and certification for aerial refueling can cost upwards of AUD million annually, covering not only personnel training but also system-specific certifications required by both local and international aviation authorities. With the shift towards incorporating autonomous refueling systems, these costs are expected to rise due to the need for further crew training and system adaptation. Additionally, Australia’s defense budget is focusing on long-term training sustainability, with a projected increase in expenditures on aviation-related training infrastructure in the coming years.

Opportunities

Indo‑Pacific Defense Partnerships on Refueling Interoperability

The Indo-Pacific region continues to be a focal point for Australia’s defense strategy, and the emphasis on interoperability with regional partners offers significant opportunities in the air-to-air refueling market. As of 2024, Australia is deepening its defense cooperation with key Indo-Pacific countries, including the United States, Japan, and India, focusing on enhancing refueling capabilities for joint military operations. In 2024, Australia’s participation in multinational defense exercises such as Talisman Sabre 2024 will require seamless integration of refueling technologies with partner nations. The Australian government has committed to increasing defense ties with India under the India-Australia defense cooperation framework, which includes collaborative air mobility training, refueling integration, and joint operational missions. With these partnerships, Australia is positioning itself as a key player in the region’s defense infrastructure, opening avenues for strategic contracts and technology sharing within the air-to-air refueling space.

Department of Defense

By leveraging current defense investments, technological advancements, and strategic partnerships, the Australian Air-to-Air Refueling System market is set for continued growth and technological evolution, especially as interoperability and autonomous refueling systems are integrated into Australia’s defense infrastructure. The ongoing focus on these areas strengthens Australia’s position as a key player in the Indo-Pacific’s defense sector.

Future Outlook

Over the next decade, the Australian Air-to-Air Refueling System market is expected to experience steady growth, driven by continuous advancements in refueling technologies and strategic government spending. Australia is committed to modernizing its defense infrastructure, particularly to enhance its interoperability with key allies in the Indo-Pacific region. With increasing demand for long-range fighter operations and the introduction of new refueling platforms, the market is poised for innovation in autonomous refueling systems. Technological developments in UAV-enabled refueling and the increasing need for air combat readiness will propel the market forward.

Major Players

- Boeing

- Airbus Defence & Space

- Cobham

- Safran

- Lockheed Martin

- General Electric

- Northrop Grumman

- Raytheon Technologies

- Israel Aerospace Industries (IAI)

- Parker Hannifin

- Thales Group

- Leonardo S.p.A.

- Qantas Defence Services

- BAE Systems

- Rolls-Royce

Key Target Audience

- Government agencies Department of Defence, Australia

- Military procurement officers Royal Australian Air Force

- Aircraft manufacturers and suppliers

- Investments and venture capital firms

- Aerospace and defense contractors

- Strategic defense planning committees

- Global aerospace partnerships e.g., NATO

- Regulatory bodies Australian Civil Aviation Safety Authority

Research Methodology

Step 1: Identification of Key Variables

The first phase involves constructing a detailed ecosystem map of stakeholders in the Australian Air-to-Air Refueling System market. This step is supported by secondary data from credible defense publications and industry reports. The main objective is to identify the key players, technologies, and regulatory factors driving market dynamics, including government spending, defense procurement schedules, and military alliances.

Step 2: Market Analysis and Construction

In this phase, historical data on military air refueling fleets and defense budget allocations are compiled and analyzed. This helps to assess the market’s penetration in the air defense sector, evaluate the growth potential of refueling systems, and understand the operational hours and frequency of refueling missions. The analysis also includes the identification of key technological innovations in refueling systems.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses about market trends and technology adoption are tested through consultations with defense industry experts, including procurement officers, aerospace engineers, and regulatory bodies. Expert opinions are gathered through telephone interviews, providing valuable insights that help refine the data and validate assumptions.

Step 4: Research Synthesis and Final Output

In the final stage, insights from defense manufacturers, component suppliers, and system integrators are synthesized to provide a comprehensive report. This phase also includes a detailed validation process to cross-check the data with actual procurement schedules, operational requirements, and future technology developments, ensuring the report’s accuracy and market relevance.

- Executive Summary

- Research Methodology (Market definitions and assumptions Defense procurement, research approach Primary research approach, Limitations and future conclusions)

- Definition and scope

- Market genesis

- Market Attractiveness Framework (fuel transfer capability, force multiplier effect)

- Supply chain and value chain analysis Policy framework and defense strategy alignment

- Growth drivers

extended range requirement

force projection needs

- Market challenges

interoperability standards

certification & training costs

- Trends

autonomous refueling development

digital refueling operator systems

- Opportunities

Indo‑Pacific defense partnerships on refueling interoperability

Regulatory & compliance landscape (defense export control, interoperability protocols) - SWOT analysis (Australian specific strengths, weaknesses, strategic ties)

- Porter’s Five Forces (supplier power, defense contractor competition, substitute systems)

- By value, 2020‑2025

- By fleet operational hours, 2020‑2025

- By capability units, 2020‑2025

- By average unit cost, 2020‑2025

- By System Type (In Value %)

probe & drogue

boom refueling

autonomous docking systems

- By Platform Type (In Value %)

tanker transport

UAV‑enabled refueling extensions

pods

- By End Use (In Value %)

RAAF strategic air mobility

coalition interoperability missions

OEM modernization

- By Procurement Route (In Value %)

new defense acquisition vs upgrade/retrofit

- By Geographic Deployment (In Value %)

domestic bases

Indo‑Pacific operations

- By Operation Mode (In Value %)

tanker‑to‑fighter

tanker‑to‑transport

coalition interoperability missions

- Market share of major players

- Cross comparison parameters (Company market positioning, Technology readiness level, Refueling throughput rate, Interoperability certification, Systems reliability metrics, Aftermarket support presence, Local maintenance partnerships, Defence contract backlog)

- SWOT analysis of key players

- Pricing analysis of major players

- Detailed profiles of major players

- Major players to be profiled

Airbus Defence & Space

The Boeing Company

Cobham plc

Eaton Corporation

GE Aviation

Lockheed Martin Systems integration

Safran SA Refueling component tech

Parker Hannifin Corporation

Israel Aerospace Industries Ltd. AAR technologies

BAE Systems plc

Northrop Grumman Simulation & training systems

Qantas Defence Services Maintenance partner ecosystem

Leonardo S.p.A Aerial support systems

Thales Group Refueling avionics interface

- Operational readiness requirements

- Budget allocations & defense budget cycles

- Platform compatibility demands F‑35A, E‑7A Wedgetail etc.

- Interoperability capability needs

- Maintenance & lifecycle costs impacts

- Training and skill readiness

- By value, 2026‑2035

- By operational capability units, 2026‑2035

- By average performance cost evolution, 2026‑2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now