Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Australian air traffic management market is valued at approximately USD ~ billion. The growth is driven by the rising number of air traffic movements, infrastructure modernization, and the integration of automation and digital technologies. The sector is propelled by the need for more efficient airspace management systems, given the increasing demands for air travel and the growing complexity of the airspace system. In 2025, the market is expected to continue its upward trajectory, as the Australian government invests in next-generation ATM technologies and regulatory frameworks to streamline operations, improve safety, and handle the expanding volume of domestic and international air traffic.

Australia’s air traffic management market is primarily dominated by key metropolitan areas with high traffic volumes such as Sydney, Melbourne, and Brisbane. Sydney, being the largest city and a major hub for international flights, sees the highest air traffic demand. Melbourne and Brisbane also contribute significantly due to their role in domestic and international routes. These cities dominate due to their infrastructure development, strong economic activity, and strategic positioning as gateways to the Asia-Pacific region. Their airports serve as key operational hubs for both commercial aviation and growing unmanned aerial systems (UAS) management.

Market Segmentation

By Technology & System Type

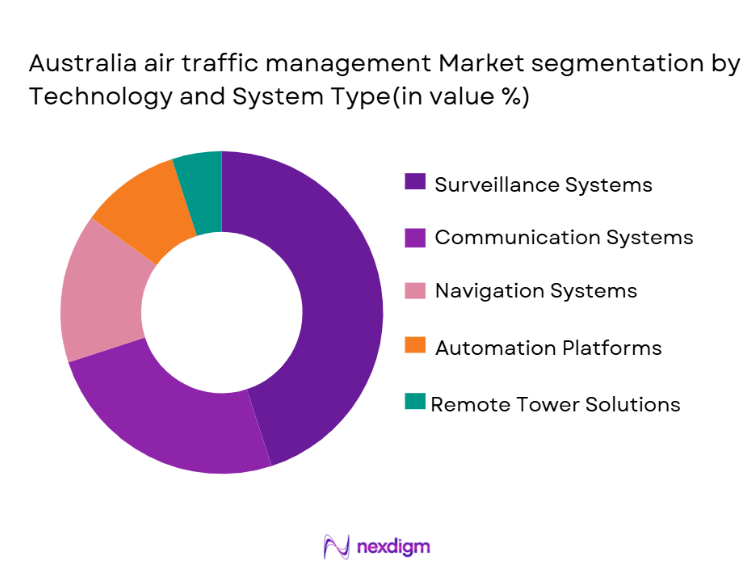

Australia’s air traffic management market is segmented by technology and system type, which includes surveillance systems, communication systems, navigation systems, automation & decision support platforms, and remote tower solutions. Among these, surveillance systems, particularly radar and ADS-B technologies, dominate the market due to their critical role in ensuring airspace safety and real-time tracking of aircraft. As Australia’s air traffic volumes grow, there is an increasing reliance on advanced radar and satellite-based systems to manage high-density airspace. Moreover, ADS-B (Automatic Dependent Surveillance–Broadcast) is becoming increasingly integrated into the national air traffic management system as it offers more accurate and real-time data for aircraft position tracking, essential for enhancing safety and operational efficiency.

By Service Offering

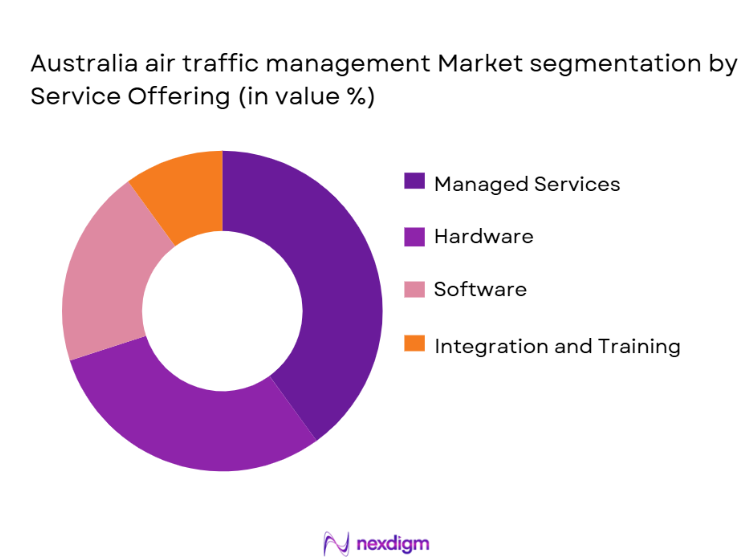

Australia’s air traffic management market is segmented by service offering into hardware, software, managed services, and integration & training services. Among these, managed services hold a significant market share, as air traffic control operators increasingly seek outsourced solutions to manage air traffic flow more efficiently. These managed services, provided by Airservices Australia and other service providers, cover ATC tower operations, radar maintenance, and real-time support for airlines. The demand for integrated services, including automation and optimization, has further contributed to the dominance of this segment. Additionally, the integration of remote towers into the market is a key growth driver in this segment.

Competitive Landscape

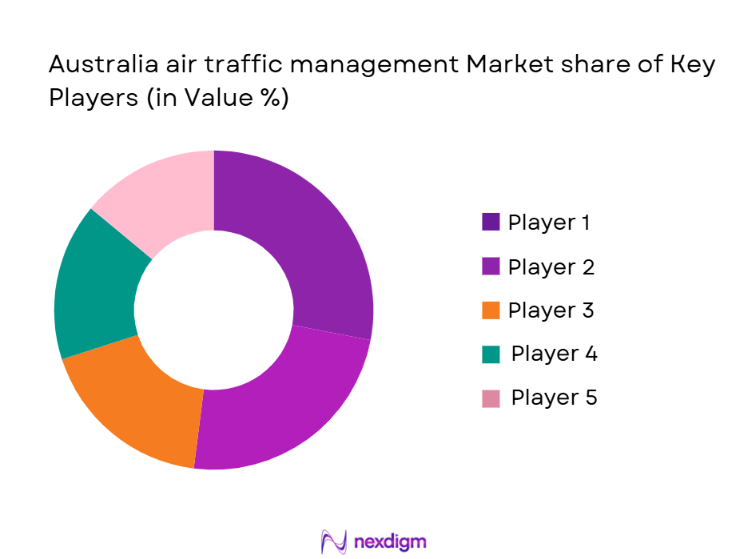

The Australian air traffic management market is competitive, with a few key players dominating the space. The market is primarily led by Airservices Australia, a government-owned entity responsible for providing safe and efficient air traffic control services. Global companies like Thales Group, Frequentis, and Saab are also major players in the market, supplying advanced radar systems, automation platforms, and communication technologies. The competition is intensified by the need for constant innovation in digital air traffic management and remote tower systems.

| Company Name | Establishment Year | Headquarters | Key Product/Technology | Operational Scope | Market Focus | Regulatory Compliance |

| Airservices Australia | 1995 | Canberra | ~ | ~ | ~ | ~ |

| Thales Group | 2000 | Sydney | ~ | ~ | ~ | ~ |

| Frequentis | 1998 | Melbourne | ~ | ~ | ~ | ~ |

| Saab | 1994 | Sydney | ~ | ~ | ~ | ~ |

| Indra Sistemas | 2001 | Melbourne | ~ | ~ | ~ | ~ |

Australia Air Traffic Management Market Analysis

Growth Drivers

Technological Advancements in ATM Systems

The integration of advanced technologies such as satellite-based navigation, automated air traffic control systems, and remote tower capabilities is propelling the growth of the air traffic management market. These innovations enhance operational efficiency, reduce congestion, and improve airspace safety, leading to increased demand for modernized ATM solutions.

Rising Air Traffic Demand

As global air travel continues to increase, driven by the recovery from the COVID-19 pandemic and growing air mobility, the demand for more sophisticated air traffic management solutions grows. This includes both commercial aviation and the emerging drone market, creating a significant need for better traffic control infrastructure and advanced systems.

Market Challenges

Cybersecurity Threats

With the increasing reliance on digital systems for air traffic management, there is a growing risk of cyberattacks on critical infrastructure. Protecting sensitive air traffic control systems and ensuring data integrity is an ongoing challenge for the market, as any breach can lead to major disruptions.

High Capital Investment and Infrastructure Upgrades

The cost of upgrading existing infrastructure to incorporate modern ATM technologies such as automation and satellite-based systems is a significant challenge. The high capital expenditure required for such investments may be a barrier for some regions or smaller airports, limiting overall market adoption.

Opportunities

Remote Tower Solutions

The rise of remote tower technology, which allows air traffic controllers to manage airports from centralized locations rather than being on-site, offers a major growth opportunity. This technology reduces costs, enhances operational efficiency, and allows airports with lower traffic volumes to benefit from advanced air traffic management systems.

Expansion of Unmanned Aircraft Systems

The increasing use of drones and unmanned aerial vehicles (UAVs) presents new opportunities for the air traffic management market. Developing systems to manage UAS operations in both controlled and uncontrolled airspace can significantly expand the role of air traffic management in overseeing airspace operations and contribute to the growth of the market.

Future Outlook

Over the next five years, the Australian air traffic management market is expected to show steady growth, driven by technological advancements and increasing air traffic demands. The adoption of automation systems, remote towers, and satellite-based communication solutions will be pivotal in modernizing the air traffic management infrastructure. Additionally, government investments in infrastructure to support high-traffic volume, coupled with international collaborations, will boost the growth of this market.

Major Players

- Airservices Australia

- Thales Group

- Frequentis

- Saab

- Indra Sistemas

- Honeywell

- Raytheon Technologies

- L3Harris Technologies

- Collins Aerospace

- BAE Systems

- Leonardo

- Northrop Grumman

- Adacel Technologies

- CAE Inc.

- Raytheon Anschütz

Key Target Audience

- Airlines and Aviation Operators

- Air Traffic Control Providers

- Government and Regulatory Bodies

- Aerospace and Defense Contractors

- Investments and Venture Capitalist Firms

- Aircraft Manufacturers

- Airport Operators

- Airport Infrastructure Investors

Research Methodology

Step 1: Identification of Key Variables

This phase involves identifying and defining the key variables influencing the Australian air traffic management market, such as air traffic growth, infrastructure expansion, regulatory impacts, and technological innovations. Research tools include secondary data analysis, market reports, and expert consultations.

Step 2: Market Analysis and Construction

This phase focuses on assessing historical data to understand air traffic trends, service quality, and system penetration. The revenue generated from different technology types, such as radar systems and remote towers, will be analyzed.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts, including air traffic controllers, software providers, and regulatory bodies, will be consulted through interviews and surveys. Their insights will validate the hypotheses related to market growth, technological adoption, and regulatory compliance.

Step 4: Research Synthesis and Final Output

The final phase synthesizes findings into a cohesive report, incorporating input from market stakeholders and verified data. This ensures an accurate representation of the market size, trends, and growth drivers.

- Executive Summary

- Research Methodology (Market Definitions and Scope, Abbreviations and Technical Glossary, Data Sources and Triangulation, Primary & Secondary Research Protocol, TopDown and BottomUp Market Sizing Methodology, Market Assumptions and Key Indicators, Limitations and Confidence Levels)

- Market Definition and Service Scope

- Historical Context of Airspace Management in Australia

- Evolution of CNS/ATM & Remote Tower Technology

- Australia Airspace Class & Air Route Structures

- Air Traffic Flow & Capacity Management

- Key National Stakeholders and Regulatory Bodies

- Value Chain and Service Delivery Framework

- Growth Drivers

Air Travel Demand & Operational Scaling

Surveillance Mandates

Digital ATC Modernization Initiatives

Integration of Uncrewed Aircraft Systems (UTM) - Market Challenges

Controller Workforce Shortage & Fatigue Risk Management

Cybersecurity Threat Landscape

Regulatory Compliance & Safety Certification - Opportunities

Remote Tower and Digital ATM Growth

AI/Automation for Conflict Resolution & Efficiency

Drone Corridor & Urban Air Mobility Services - Market Trends

Shift to Satellitebased Navigation (GNSS)

Crossdomain ATM/CNS integration

Investment in Resilience & Redundancy - Regulatory & Policy Landscape

Civil Aviation Safety Authority (CASA) Frameworks

Airservices Australia Strategic Plans

International Civil Aviation Organization (ICAO) Standards

- Total Market Revenue 2020-2025

- Segmented Revenue 2020-2025

- Market Volume Radars/Remote Towers/Shorebased Systems 2020-2025

- Average Contract Values and Pricing Benchmarks 2020-2025

- By Technology & System Type (In Value%)

Surveillance Systems

Communication Systems

Navigation Systems

Automation & Decision Support Platforms

Remote/Virtual Tower Solutions - By Service Offering (In Value%)

Hardware

Software Solutions

Managed Services

Integration & Training Services - By Operation Phase (In Value%)

EnRoute

Approach/Departure

Aerodrome

UTM - By EndUser (In Value%)

Commercial Aviation

Regional & General Aviation

Defence & Government ATC Operations

Drone & Urban Mobility Traffic Management - By Region/State (In Value%)

New South Wales

Victoria

Queensland

Western Australia

Other States & Territories

- Market Share and Competitive Positioning

- Cross Comparison Parameters (Company Overview & Ownership Structure, Australia Contract Footprint, Product/Technology Breadth, Installed Base, Integration & Interoperability Capabilities, Regulatory Compliance & Safety Certifications, R&D & Innovation Investments, Strategic Partnerships & Alliances)

- Key Competitors

Airservices Australia

Thales Group

Frequentis Australasia

Saab AB

Indra Sistemas

Honeywell International

Collins Aerospace (UTC)

L3Harris Technologies

Raytheon Technologies

BAE Systems

Leonardo S.p.A

Northrop Grumman

Adacel Technologies

CAE Inc. (ATC Training)

Raytheon Anschütz

- Operational Data & Airspace Utilization Trends

- ATC System Architecture & Integration Points

- Supply Chain for Hardware, Software, Services

- Channel Partners & System Integrators

- Maintenance, Training, Support Services

- Market Revenue Forecast by Segment 2026-2035

- Market Volume & Adoption Trends 2026-2035

- Technology Penetration Scenarios 2026-2035

- Impact of UTM & Urban Air Mobility 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now