Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Australia Airport Kiosk market current size stands at around USD ~ million, reflecting steady demand from airport operators and airlines seeking to optimize passenger processing and reduce frontline staffing intensity. In the recent period, market value expanded from approximately USD ~ million, supported by rising automation budgets and accelerated replacement of legacy check-in systems. Deployment volumes reached nearly ~ units, while the installed base exceeded ~ systems, indicating a mature but still expanding self-service ecosystem across major aviation hubs.

Market activity is concentrated in metropolitan aviation clusters such as Sydney, Melbourne, and Brisbane, where high passenger throughput and international traffic density justify large-scale kiosk deployments. These cities benefit from advanced digital infrastructure, established airport technology vendors, and proactive policy frameworks supporting contactless travel and biometric screening. Regional dominance is also shaped by strong airline presence, integrated border management systems, and coordinated investments between airport authorities and federal agencies.

Market Segmentation

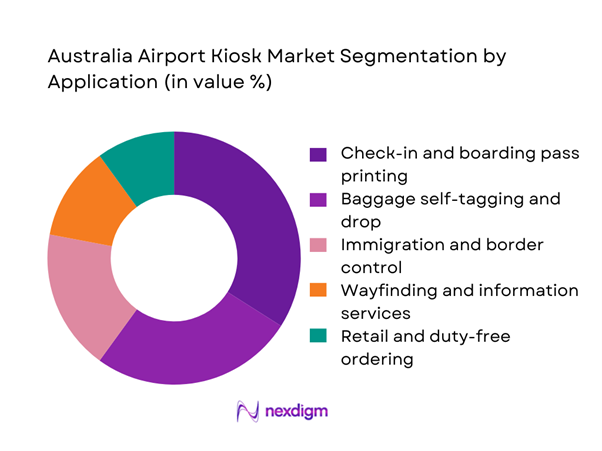

By Application

Self-service check-in and boarding solutions dominate the Australia Airport Kiosk market due to their direct impact on passenger flow optimization and airline cost reduction. Baggage self-tagging and automated drop systems follow closely, driven by labor constraints and rising baggage volumes. Immigration and border control kiosks continue to gain traction as authorities focus on reducing manual processing time. Wayfinding and information kiosks support passenger experience initiatives, while retail and duty-free ordering kiosks are emerging as a revenue-enhancement tool. The application mix reflects a shift from purely operational efficiency toward a blended model of service automation and commercial engagement.

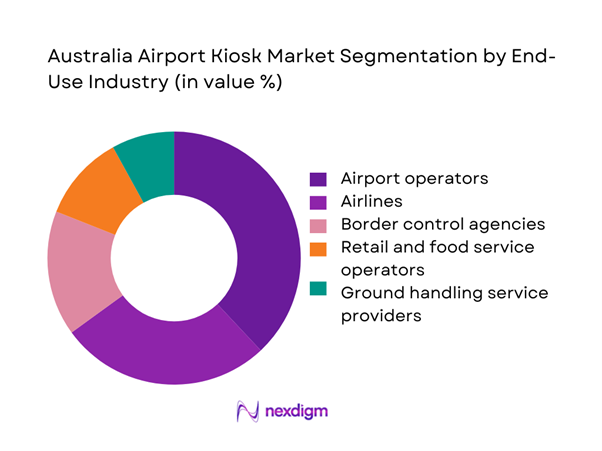

By End-Use Industry

Airport operators account for the largest share of kiosk deployments as they lead infrastructure modernization programs and coordinate multi-tenant technology rollouts. Airlines remain a key end-user group, prioritizing dedicated and hybrid kiosks to streamline passenger handling. Border control agencies increasingly invest in automated processing kiosks to manage growing international arrivals. Retail and food service operators are adopting kiosks to expand digital ordering channels, while ground handling service providers use them to improve baggage and passenger service workflows. This segmentation highlights the expanding role of kiosks beyond airline operations into a broader airport commercial and security ecosystem.

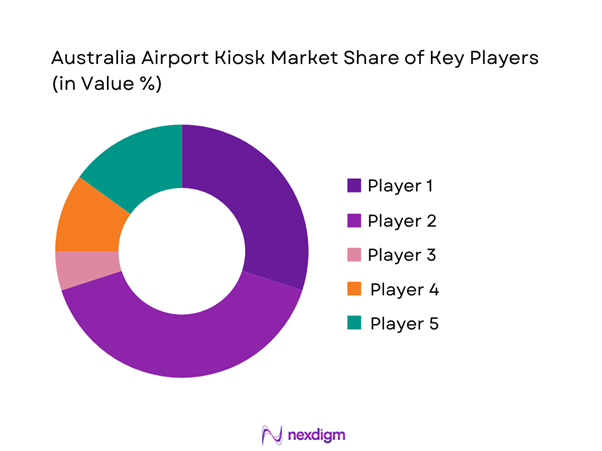

Competitive Landscape

The Australia Airport Kiosk market shows moderate concentration, with a small group of global airport technology providers and system integrators controlling a significant portion of large-scale deployments. Local system partners and hardware specialists complement this structure by supporting regional airports and specialized applications, creating a layered competitive environment.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| SITA | 1949 | Switzerland | ~ | ~ | ~ | ~ | ~ | ~ |

| Amadeus IT Group | 1987 | Spain | ~ | ~ | ~ | ~ | ~ | ~ |

| Thales Group | 1893 | France | ~ | ~ | ~ | ~ | ~ | ~ |

| Collins Aerospace | 2018 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Fujitsu Limited | 1935 | Japan | ~ | ~ | ~ | ~ | ~ | ~ |

Australia Airport Kiosk Market Analysis

Growth Drivers

Rising passenger volumes across major Australian airports

Sustained growth in domestic and international travel has increased passenger throughput at key Australian aviation hubs, intensifying pressure on terminal processing capacity. Over the recent period, annual passenger handling expanded to nearly ~ million travelers, driving demand for self-service infrastructure to manage peak-hour congestion. Airports responded by deploying over ~ units of new kiosks, lifting the active installed base beyond ~ systems. This expansion supported processing efficiency gains and reduced average queue times. Airlines also aligned with this trend by reallocating operational budgets toward automation, with technology upgrades accounting for close to USD ~ million in cumulative spending during the period.

Push for end-to-end contactless and self-service journeys

The shift toward contactless travel experiences accelerated investment in kiosk-based solutions that minimize physical interactions. Recent deployments added approximately ~ systems focused on touchless check-in, biometric identity verification, and mobile-integrated boarding. Capital allocation for contactless infrastructure reached nearly USD ~ million, reflecting strategic prioritization by both airport authorities and carriers. Passenger adoption followed a similar trajectory, with self-service usage volumes exceeding ~ million transactions annually. This behavioral shift reinforced long-term demand for advanced kiosk platforms, positioning self-service technology as a core element of modern airport operations rather than a supplementary feature.

Challenges

High upfront capital and integration costs

Airport kiosk deployments require substantial initial outlays, covering hardware acquisition, software licensing, and systems integration with airline and border control platforms. Recent projects recorded average implementation expenditures of USD ~ million per terminal, limiting adoption among smaller and regional airports. Integration complexity further increased costs, with customization efforts exceeding ~ development hours per deployment cycle. These financial and technical barriers slowed replacement of legacy systems, leaving an estimated ~ systems operating beyond optimal lifecycle thresholds. Budget constraints therefore continue to shape the pace and scale of market expansion despite strong operational demand.

Complex compliance with aviation security and privacy standards

Regulatory compliance presents a persistent challenge, particularly for kiosks handling passenger identity and travel data. Recent regulatory updates required system upgrades across ~ installations to meet enhanced data protection and cybersecurity benchmarks. Compliance investments reached approximately USD ~ million, covering encryption, access controls, and audit mechanisms. For operators managing multi-airport networks, harmonizing standards added further complexity, often extending deployment timelines by ~ months per project. These regulatory pressures, while essential for security, raise both cost and implementation risk, influencing procurement decisions across the market.

Opportunities

Deployment of biometric-enabled kiosks for seamless travel

Biometric technology offers a major growth avenue as airports seek to streamline identity verification and boarding processes. Recent pilots introduced facial recognition kiosks across ~ terminals, processing more than ~ million passengers annually through automated lanes. Investment in biometric infrastructure surpassed USD ~ million, signaling strong institutional commitment. Performance metrics indicate significant reductions in manual checks, freeing up staff for higher-value roles. As regulatory frameworks mature and passenger acceptance increases, biometric-enabled kiosks are positioned to become a standard feature across Australian international gateways.

Growth in self-service baggage handling solutions

Rising baggage volumes and labor constraints are driving adoption of self-service tagging and automated drop kiosks. Recent installations added over ~ units dedicated to baggage processing, lifting system coverage across major terminals. Airlines allocated close to USD ~ million toward these solutions, targeting faster turnaround times and reduced mishandling rates. Operational data shows throughput improvements of nearly ~ bags processed per day at peak sites. This momentum creates a scalable opportunity for kiosk providers to integrate baggage solutions with broader passenger service platforms.

Future Outlook

The Australia Airport Kiosk market is set to advance steadily through the next decade as automation becomes integral to airport infrastructure planning. Continued emphasis on digital border control, passenger experience enhancement, and operational resilience will sustain investment momentum. The market is expected to benefit from deeper integration of kiosks with mobile platforms and biometric systems, reinforcing the transition toward fully self-service airport environments.

Major Players

- SITA

- Amadeus IT Group

- Thales Group

- Collins Aerospace

- Fujitsu Limited

- NCR Voyix

- Diebold Nixdorf

- IER

- Embross

- Materna IPS

- KIOSK Information Systems

- Olea Kiosks

- Zivelo

- Advantech

- Samsung Electronics

Key Target Audience

- Airport operators and airport authority boards

- Domestic and international airlines

- Border control and immigration agencies

- Aviation security and compliance bodies

- Airport retail and duty-free operators

- Ground handling and baggage service providers

- Investments and venture capital firms

- Government and regulatory bodies such as the Department of Infrastructure,

- Transport, Regional Development, Communications and the Arts

Research Methodology

Step 1: Identification of Key Variables

Key demand drivers, regulatory factors, technology adoption patterns, and investment flows were mapped to define the core structure of the Australia Airport Kiosk market. Data points were aligned to passenger processing, automation intensity, and infrastructure modernization indicators.

Step 2: Market Analysis and Construction

Historical performance trends were analyzed to establish baseline market behavior. Supply-side dynamics, deployment cycles, and procurement models were assessed to construct a coherent market framework.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings were tested through structured discussions with industry stakeholders across airport operations, aviation technology, and regulatory compliance. Feedback was used to refine assumptions and validate market direction.

Step 4: Research Synthesis and Final Output

All quantitative and qualitative insights were consolidated into a unified market narrative. Final outputs were reviewed for internal consistency, analytical rigor, and strategic relevance to decision-makers.

- Executive Summary

- Research Methodology (Market definitions and scope boundaries, airport kiosk taxonomy across self check in bag drop and wayfinding units, market sizing logic by airport passenger traffic and kiosk deployment density, revenue attribution across hardware software and service contracts, primary interview program with airport operators system integrators and kiosk vendors, data triangulation validation assumptions and limitations)

- Definition and scope

- Market evolution

- Passenger journey and self-service usage pathways

- Airport technology ecosystem structure

- Supply chain and channel structure

- Regulatory and security environment

- Growth Drivers

Rising passenger volumes across major Australian airports

Push for end-to-end contactless and self-service journeys

Airport capacity constraints driving automation investments

Government focus on border efficiency and biosecurity screening

Airline cost optimization through reduced counter staffing

Expansion of airport retail digitalization - Challenges

High upfront capital and integration costs

Complex compliance with aviation security and privacy standards

System interoperability issues with legacy airport IT

Cybersecurity risks in connected kiosks

Operational disruptions during technology upgrades

Uneven adoption across regional and smaller airports - Opportunities

Deployment of biometric-enabled kiosks for seamless travel

Growth in self-service baggage handling solutions

Private 5G networks enabling real-time kiosk management

AI-driven personalization for airport retail kiosks

Retrofit and modernization of aging kiosk fleets

Expansion into regional airport infrastructure upgrades - Trends

Shift toward cloud-managed kiosk platforms

Integration of facial recognition and e-gates

Rising demand for multilingual and accessibility-compliant interfaces

Convergence of kiosks with mobile passenger apps

Increased use of modular and portable kiosk designs

Data-driven optimization of passenger flow - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2020–2025

- By Volume, 2020–2025

- By Installed Base, 2020–2025

- By Average Selling Price, 2020–2025

- By Fleet Type (in Value %)

Common-use kiosks

Dedicated airline kiosks

Hybrid shared-service kiosks

Premium and fast-track kiosks - By Application (in Value %)

Check-in and boarding pass printing

Baggage self-tagging and drop

Immigration and border control

Wayfinding and information services

Retail and duty-free ordering - By Technology Architecture (in Value %)

Standalone kiosks

Networked kiosks

Cloud-managed kiosks

Edge-enabled kiosks - By End-Use Industry (in Value %)

Airport operators

Airlines

Border control agencies

Retail and food service operators

Ground handling service providers - By Connectivity Type (in Value %)

Wired LAN

Wi-Fi enabled

Cellular and private 5G

Hybrid connectivity - By Region (in Value %)

New South Wales

Victoria

Queensland

Western Australia

South Australia

Other states and territories

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (installed base at Australian airports, system uptime performance, biometric integration capability, cybersecurity certifications, compliance with aviation standards, local service network strength, total cost of ownership, scalability and modularity)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

SITA

Amadeus IT Group

Thales Group

Collins Aerospace

Fujitsu Limited

NCR Voyix

Diebold Nixdorf

IER (an Ingenico Group company)

Embross

Materna IPS

KIOSK Information Systems

Olea Kiosks

Zivelo

Advantech

Samsung Electronics

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

By Value, 2026–2035

By Volume, 2026–2035

By Installed Base, 2026–2035

By Average Selling Price, 2026–2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now