Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Australia airport moving walkways market current size stands at around USD ~ million, supported by steady capital allocation across major terminal upgrade programs and system replacement cycles. Recent demand has translated into annual deployment of ~ systems, reflecting a gradual shift toward automated passenger mobility solutions. Average contract values remain near USD ~ million per project, driven by customization needs, safety compliance requirements, and integration with existing terminal infrastructure. Ongoing modernization has resulted in an installed base exceeding ~ systems nationwide, underlining the sector’s operational importance.

Market activity is concentrated in metropolitan aviation hubs where passenger throughput, inter-terminal transfers, and long walking corridors are most prevalent. Sydney, Melbourne, and Brisbane dominate adoption due to sustained airport redevelopment pipelines, higher international traffic density, and early uptake of smart terminal concepts. These regions benefit from mature supplier ecosystems, established maintenance networks, and supportive infrastructure policy frameworks. Secondary airports are gradually increasing adoption as regional connectivity improves and state-led infrastructure programs prioritize accessibility, safety, and passenger comfort.

Market Segmentation

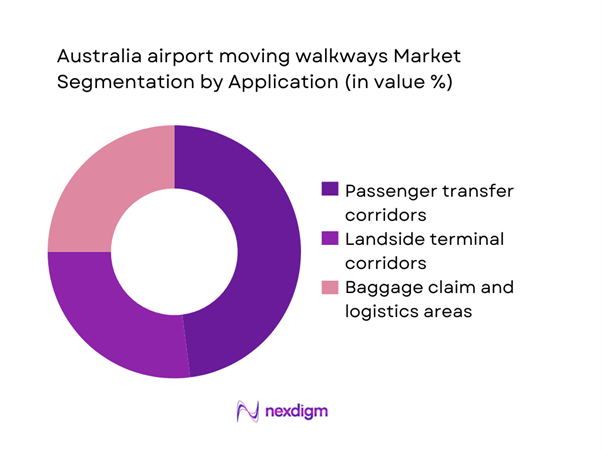

By Application

Passenger transfer corridors dominate adoption as airports focus on reducing walking time between terminals, gates, and baggage areas while improving traveler comfort. High daily footfall and peak-hour congestion make these zones the most critical for moving walkway deployment. Landside corridors also show consistent demand, particularly in terminals integrating rail links and parking facilities. Baggage claim and logistics areas remain a smaller but growing segment as airports modernize backend operations for smoother passenger flow. Overall, application-driven demand is shaped by terminal layout complexity, average passenger dwell time, and the strategic push to enhance end-to-end travel experience.

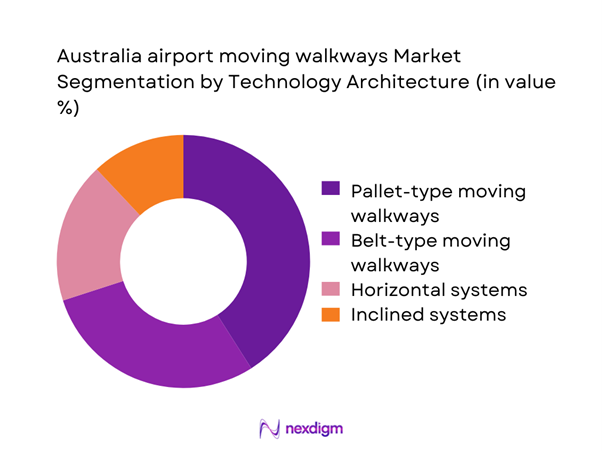

By Technology Architecture

Pallet-type moving walkways lead the market due to their durability, higher load capacity, and suitability for high-traffic environments such as international terminals. Belt-type systems follow, favored for their quieter operation and flexibility in medium-traffic zones. Inclined walkways are gaining relevance as multi-level terminal designs become more common, reducing reliance on elevators and escalators for short vertical transitions. Horizontal systems continue to account for steady installations in long, flat corridors. Technology selection is influenced by maintenance cost profiles, energy efficiency goals, and the need for seamless integration with terminal aesthetics and safety systems.

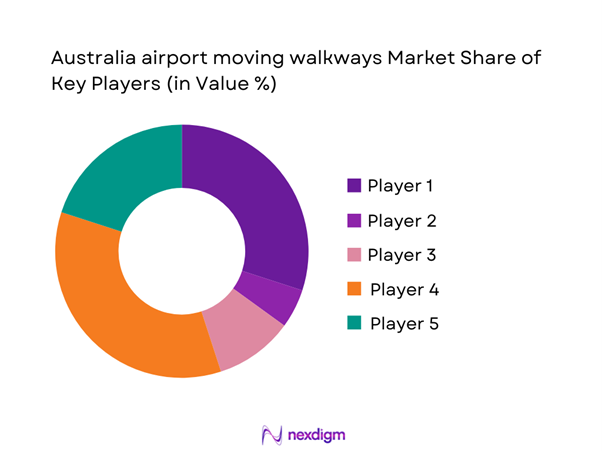

Competitive Landscape

The market is moderately concentrated, with a small group of global elevator and mobility solution providers controlling most large-scale airport contracts. Long-standing relationships with airport authorities, proven safety records, and nationwide service networks create high entry barriers for smaller players. Competitive differentiation is driven less by price and more by lifecycle support, system reliability, and the ability to deliver complex installations within tight construction timelines.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| KONE Corporation | 1910 | Finland | ~ | ~ | ~ | ~ | ~ | ~ |

| Schindler Group | 1874 | Switzerland | ~ | ~ | ~ | ~ | ~ | ~ |

| Otis Worldwide Corporation | 1853 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Mitsubishi Electric Corporation | 1921 | Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| TK Elevator | 2020 | Germany | ~ | ~ | ~ | ~ | ~ | ~ |

Australia airport moving walkways Market Analysis

Growth Drivers

Rising airport passenger traffic and terminal expansion projects

Sustained growth in air travel has pushed annual passenger throughput beyond ~ travelers across major Australian hubs, creating pressure on existing terminal layouts and pedestrian circulation capacity. In response, airport authorities have committed more than USD ~ million in combined terminal redevelopment and airside expansion programs, directly increasing demand for moving walkway installations. New concourse developments typically require ~ systems per project to manage longer walking distances and improve transfer efficiency. This infrastructure-driven expansion has translated into consistent procurement pipelines for suppliers, with multi-year contracts covering installation, maintenance, and system upgrades to support rising operational volumes.

Increased focus on passenger experience and reduced transit time

Airports are increasingly measured by dwell time efficiency and traveler comfort metrics, leading to wider adoption of automated mobility solutions. Surveys of terminal operators indicate average acceptable walking distances have reduced to ~ meters, prompting redesigns that integrate moving walkways across long corridors. Investments of USD ~ million annually are now directed toward passenger experience enhancements, including barrier-free access and smoother baggage-to-gate transitions. These initiatives have resulted in deployment of ~ additional systems across premium terminals, reinforcing the role of moving walkways as a core component of customer satisfaction strategies and competitive airport positioning.

Challenges

High upfront capital expenditure for new installations

Installing a single moving walkway system typically requires project budgets approaching USD ~ million when civil works, electrical integration, and safety certification are included. For multi-terminal airports, cumulative costs can exceed USD ~ million per modernization phase, placing pressure on capital allocation frameworks. Smaller regional airports often face constraints, limiting adoption to only ~ systems despite operational need. These financial barriers extend procurement cycles and increase reliance on phased installations, slowing overall market penetration and creating uneven demand patterns across the national airport network.

Complex retrofitting in constrained terminal layouts

A significant portion of Australia’s airport infrastructure was designed decades ago, leaving limited structural flexibility for large-scale mobility upgrades. Retrofitting projects often involve reconfiguration of corridors measuring less than ~ meters in width, adding complexity to system design and installation. Engineering assessments and compliance procedures can extend project timelines by ~ months, increasing indirect costs and operational disruption. These constraints reduce the feasibility of standard solutions, requiring customized systems that elevate expenditure and prolong deployment schedules, ultimately dampening short-term installation volumes.

Opportunities

Development of energy-efficient and low-noise walkway systems

Airports are under increasing pressure to reduce operational energy consumption, with sustainability targets driving demand for next-generation mobility solutions. New models capable of lowering power usage by ~ kilowatt-hours annually per system present a compelling value proposition. Noise reduction technologies that cut operational sound levels by ~ decibels also enhance passenger comfort in enclosed terminal spaces. As airports allocate USD ~ million toward green infrastructure initiatives, suppliers offering energy-optimized and acoustically advanced walkways stand to capture a growing share of upgrade and replacement contracts.

Expansion of regional airports under government infrastructure programs

State and federal aviation infrastructure initiatives have earmarked USD ~ million for regional airport upgrades aimed at improving connectivity and accessibility. These projects are expected to introduce ~ new terminals and expanded concourses over the next planning cycle, each requiring integrated passenger mobility solutions. Regional deployments typically involve ~ systems per site, creating a new demand layer beyond major metropolitan hubs. This policy-driven expansion opens opportunities for suppliers to establish long-term service footprints in emerging aviation centers and diversify revenue away from saturated metro markets.

Future Outlook

The Australia airport moving walkways market is set to evolve alongside broader smart airport initiatives, with greater emphasis on automation, sustainability, and passenger-centric design. As terminal footprints expand and regional aviation gains policy support, demand will increasingly balance between large metropolitan hubs and emerging secondary airports. Technology upgrades, energy efficiency mandates, and digital integration will shape procurement priorities, positioning moving walkways as a strategic asset in future-ready airport infrastructure.

Major Players

- KONE Corporation

- Schindler Group

- Otis Worldwide Corporation

- Mitsubishi Electric Corporation

- TK Elevator

- Hitachi Ltd.

- Hyundai Elevator

- Fujitec Co., Ltd.

- Toshiba Elevator and Building Systems

- Orona Group

- Stannah Lifts Holdings

- KLEEMANN Hellas

- SJEC Corporation

- Canny Elevator Co., Ltd.

- IFE Elevators

Key Target Audience

- Airport authorities and airport operating corporations

- State and federal government transport infrastructure agencies

- Civil aviation safety regulators and standards bodies

- Engineering, procurement, and construction firms in aviation projects

- Facility management and airport services providers

- Urban mobility and smart infrastructure solution integrators

- Investments and venture capital firms focused on infrastructure technology

- Government and regulatory bodies such as the Department of Infrastructure and Civil Aviation Safety Authority

Research Methodology

Step 1: Identification of Key Variables

Key demand indicators, infrastructure development pipelines, and passenger mobility requirements were mapped across major and regional airports. Operational constraints, safety compliance needs, and lifecycle cost factors were defined as primary evaluation metrics. Stakeholder roles across procurement, installation, and maintenance were outlined to structure the analytical framework.

Step 2: Market Analysis and Construction

Historical deployment patterns and current project pipelines were assessed to build baseline demand scenarios. Segment-level adoption drivers were analyzed across application and technology categories. Supply-side capabilities were reviewed to understand capacity alignment with projected infrastructure needs.

Step 3: Hypothesis Validation and Expert Consultation

Industry practitioners from airport operations and mobility system integration were consulted to validate assumptions. Feedback loops refined demand forecasts and technology adoption timelines. Operational feasibility and policy alignment were tested against real-world deployment conditions.

Step 4: Research Synthesis and Final Output

All qualitative and quantitative insights were consolidated into a unified analytical model. Scenario outcomes were stress-tested to ensure robustness under different infrastructure investment pathways. Findings were structured into actionable insights for strategic and operational decision-making.

- Executive Summary

- Research Methodology (Market definitions and scope boundaries, moving walkway system taxonomy across horizontal and inclined designs, market sizing logic by airport expansion and retrofit demand, revenue attribution across equipment installation and maintenance services, primary interview program with airports system integrators and MRO providers, data triangulation validation assumptions and limitations)

- Definition and scope

- Market evolution in Australian aviation infrastructure

- Passenger flow and baggage handling usage pathways

- Airport mobility ecosystem structure

- Supply chain and installation channel structure

- Regulatory and safety standards environment

- Growth Drivers

Rising airport passenger traffic and terminal expansion projects

Increased focus on passenger experience and reduced transit time

Aging infrastructure driving replacement and modernization demand

Growth of hub-and-spoke airport models increasing walking distances

Higher safety and accessibility compliance requirements

Integration of smart mobility solutions in airport design - Challenges

High upfront capital expenditure for new installations

Complex retrofitting in constrained terminal layouts

Long procurement and tender approval cycles

Dependence on global OEM supply chains and lead times

Maintenance downtime affecting airport operations

Regulatory compliance costs and certification timelines - Opportunities

Development of energy-efficient and low-noise walkway systems

Expansion of regional airports under government infrastructure programs

Adoption of predictive maintenance and remote monitoring solutions

Public-private partnerships for terminal modernization

Customization for high-capacity and peak-hour traffic handling

Integration with smart airport and digital twin platforms - Trends

Shift toward inclined and high-speed walkways in large terminals

Growing use of condition-based maintenance technologies

Preference for modular designs to reduce installation time

Emphasis on sustainability and reduced power consumption

Increased demand for aesthetically integrated systems

Standardization of safety features across airport networks - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2020–2025

- By Volume, 2020–2025

- By Installed Base, 2020–2025

- By Average Selling Price, 2020–2025

- By Fleet Type (in Value %)

New installations

Replacement and modernization systems - By Application (in Value %)

Landside terminal corridors

Airside passenger transfer zones

Baggage claim and logistics areas - By Technology Architecture (in Value %)

Pallet-type moving walkways

Belt-type moving walkways

Horizontal walkways

Inclined walkways - By End-Use Industry (in Value %)

International airports

Domestic airports

Regional and secondary airports - By Connectivity Type (in Value %)

Standalone systems

Networked and IoT-enabled systems - By Region (in Value %)

New South Wales

Victoria

Queensland

Western Australia

South Australia

Rest of Australia

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (installation footprint, energy efficiency, load capacity, speed range, incline capability, safety certifications, maintenance intervals, lifecycle cost)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarketing

- Detailed Profiles of Major Companies

Otis Worldwide Corporation

KONE Corporation

Schindler Group

TK Elevator

Mitsubishi Electric Corporation

Hitachi Ltd.

Hyundai Elevator

Fujitec Co., Ltd.

Toshiba Elevator and Building Systems

Orona Group

Stannah Lifts Holdings

Canny Elevator Co., Ltd.

SJEC Corporation

KLEEMANN Hellas

IFE Elevators

- Demand and utilization drivers across airport types

- Procurement and tender dynamics in public infrastructure projects

- Buying criteria and vendor selection frameworks

- Budget allocation and financing preferences of airport authorities

- Implementation barriers and operational risk factors

- Post-purchase service and lifecycle support expectations

- By Value, 2026–2035

- By Volume, 2026–2035

- By Installed Base, 2026–2035

- By Average Selling Price, 2026–2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now