Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Australia cabin interior composites Market market current size stands at around USD ~ million, supported by ~ aircraft undergoing interior retrofits and ~ new platform installations across fleets. Demand intensity reflects ~ percent utilization rates within commercial cabins and ~ percent penetration of composite panels across seating, flooring, and sidewall applications. Production volumes increased by ~ units driven by modernization cycles, while material adoption expanded across ~ platforms due to weight optimization priorities and regulatory compliance requirements.

Market activity remains concentrated across New South Wales, Victoria, and Queensland, supported by established aviation infrastructure, MRO density, and defense aviation facilities. These regions benefit from skilled composite manufacturing labor, proximity to airport hubs, and stable certification ecosystems. Western Australia shows niche demand linked to defense patrol aircraft. Policy support for aerospace manufacturing, coupled with long-term fleet sustainment programs, continues shaping regional dominance patterns.

Market Segmentation

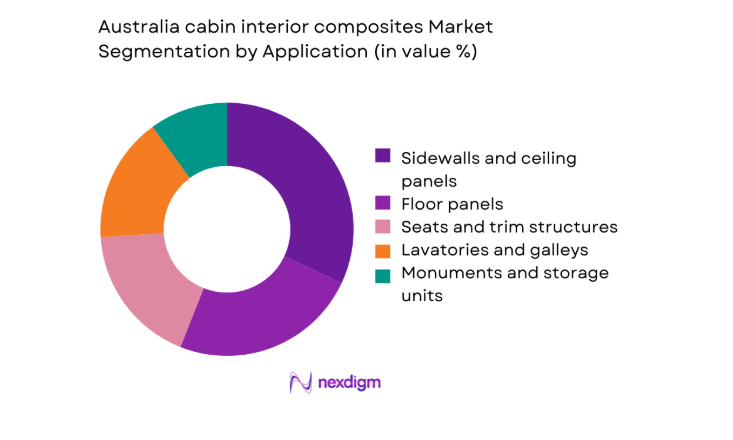

By Application

Sidewalls, ceiling panels, and floor panels dominate application demand due to recurring replacement cycles, strict fire resistance standards, and continuous airline cabin refresh strategies. Seating structures and monuments show steady adoption as airlines focus on lightweight modular interiors. Lavatories and galleys increasingly integrate advanced composites to improve durability and hygiene compliance. Retrofit programs drive higher penetration across commercial fleets, while defense and business aviation prioritize customized interior applications aligned with mission-specific requirements and long service intervals.

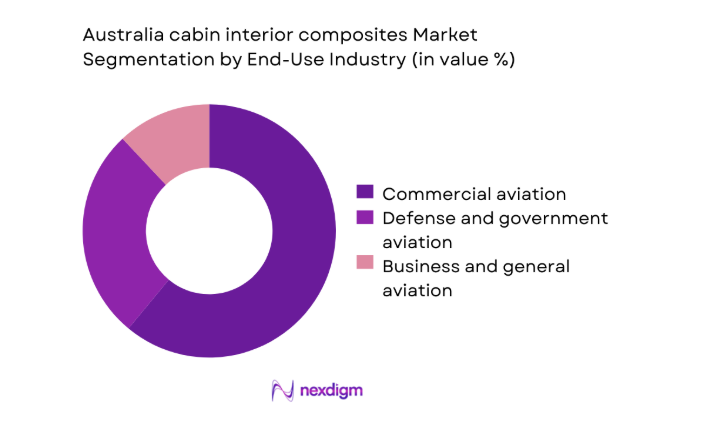

By End-Use Industry

Commercial aviation represents the dominant end-use segment driven by domestic fleet density, high passenger traffic, and frequent cabin reconfiguration cycles. Defense aviation maintains consistent demand through long-term sustainment and refurbishment programs. Business and general aviation contributes niche but high-value demand, emphasizing premium finishes and customization. End-use segmentation reflects differing certification paths, replacement frequencies, and performance requirements shaping composite material selection and system integration strategies.

Competitive Landscape

The competitive landscape reflects a mix of global aerospace interior specialists and advanced composite material suppliers supporting Australian OEM and MRO requirements.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Safran Cabin | 1946 | France | ~ | ~ | ~ | ~ | ~ | ~ |

| Collins Aerospace | 2018 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Diehl Aviation | 2006 | Germany | ~ | ~ | ~ | ~ | ~ | ~ |

| FACC | 1989 | Austria | ~ | ~ | ~ | ~ | ~ | ~ |

| GKN Aerospace | 1759 | United Kingdom | ~ | ~ | ~ | ~ | ~ | ~ |

Australia cabin interior composites Market Analysis

Growth Drivers

Rising domestic and regional aircraft fleet modernization

Fleet modernization activities expanded with ~ aircraft undergoing refurbishment, driving consistent demand for advanced interior composite components. Airlines prioritized lighter cabin structures to improve operational efficiency and extend aircraft service life. Composite interiors enabled modular upgrades without extensive structural rework. Regulatory compliance requirements accelerated replacement of legacy materials. MRO facilities increased throughput capacity to support retrofit volumes. Defense fleets adopted modernization programs emphasizing durability and lifecycle performance. Business aviation operators pursued cabin refresh cycles aligned with competitive differentiation. Domestic travel recovery strengthened utilization rates across narrow body fleets. Modernization timelines shortened due to standardized composite architectures. These factors collectively reinforced sustained demand momentum.

Increasing use of lightweight materials to reduce fuel burn

Lightweight material adoption increased as operators targeted incremental fuel efficiency improvements across high-frequency routes. Composite interiors contributed measurable weight reductions per aircraft configuration. Airlines evaluated material substitutions to support emissions reduction strategies. Cabin weight optimization complemented aerodynamic and engine efficiency programs. Composite sandwich panels replaced heavier metallic assemblies. Material performance improvements enhanced fire resistance and durability simultaneously. Engineering teams standardized lightweight designs across fleet families. Defense operators valued payload flexibility benefits. Business jets leveraged lightweight cabins for extended range profiles. Fuel efficiency imperatives sustained material transition momentum.

Challenges

High certification and qualification costs for new composite materials

Certification processes require extensive testing, increasing development timelines for new composite formulations. Compliance with fire, smoke, and toxicity standards adds procedural complexity. Smaller suppliers face resource constraints navigating approval pathways. Aircraft platform-specific certifications limit material reuse flexibility. Qualification costs influence conservative adoption behaviors among operators. Documentation requirements extend program schedules. Regulatory harmonization challenges persist across civil and defense segments. Testing infrastructure availability remains limited domestically. These factors elevate entry barriers for innovative materials. Cost pressures influence supplier prioritization decisions.

Dependence on imported prepregs fibers and resins

The supply chain relies heavily on imported composite raw materials. Lead times remain sensitive to global logistics disruptions. Currency volatility affects procurement planning stability. Limited domestic resin production constrains localization efforts. Inventory buffering increases working capital exposure. Defense programs face security-of-supply considerations. Qualification of alternate suppliers requires lengthy validation cycles. Transportation constraints impact temperature-sensitive materials. Supply concentration elevates operational risk profiles. These dependencies restrict rapid scaling capabilities.

Opportunities

Defense aircraft interior refurbishment programs

Defense fleets require periodic interior upgrades aligned with mission requirements and compliance standards. Long service lives create recurring refurbishment demand cycles. Composite interiors enhance durability under demanding operational conditions. Government sustainment budgets support multi-year programs. Local MRO participation strengthens domestic value capture. Customization requirements favor specialized composite solutions. Security-driven sourcing preferences encourage supplier partnerships. Platform standardization simplifies material integration. Interior upgrades improve crew ergonomics and safety. These programs provide stable demand visibility.

Adoption of thermoplastic composites for faster processing

Thermoplastic composites offer reduced cycle times and improved recyclability. Faster processing supports higher throughput in MRO environments. Weldable characteristics simplify assembly and repairs. Impact resistance benefits high-traffic cabin areas. Material consistency improves quality control outcomes. Automation compatibility enhances manufacturing scalability. Regulatory familiarity continues improving with broader adoption. Weight savings align with efficiency targets. Lifecycle cost advantages attract operator interest. These attributes support accelerated adoption pathways.

Future Outlook

The Australia cabin interior composites Market is expected to evolve steadily through 2035 as fleet modernization and defense sustainment programs continue. Material innovation, localized manufacturing initiatives, and thermoplastic adoption will shape competitive dynamics. Regulatory alignment and supply chain resilience will remain strategic priorities.

Major Players

- Safran Cabin

- Collins Aerospace

- Diehl Aviation

- FACC

- GKN Aerospace

- Triumph Group

- AIM Altitude

- Jamco

- Aviointeriors

- Airbus Atlantic

- Daher

- Toray Advanced Composites

- Hexcel

- Solvay

- Teijin Carbon

Key Target Audience

- Commercial airline fleet operators

- Aircraft OEM interior integration teams

- Defense procurement agencies including Department of Defence Australia

- MRO service providers

- Composite material suppliers

- Cabin interior system integrators

- Investments and venture capital firms

- Civil Aviation Safety Authority and defense certification bodies

Research Methodology

Step 1 Identification of Key Variables

Key variables included interior component categories, composite material types, fleet classes, and certification requirements influencing demand formation.

Step 2 Market Analysis and Construction

Market structure was constructed through platform-level analysis, retrofit cycles, and material penetration assessment across applications.

Step 3 Hypothesis Validation and Expert Consultation

Assumptions were validated through structured consultations with engineers, MRO managers, and regulatory specialists within the aviation ecosystem.

Step 4 Research Synthesis and Final Output

Findings were synthesized through triangulation and consistency checks to deliver coherent, decision-oriented market insights.

- Executive Summary

- Research Methodology (Market Definitions and scope for Australian aircraft cabin interior composites, OEM and MRO segmentation taxonomy across interior components and materials, bottom-up aircraft build rate and retrofit-based market sizing, value attribution by composite type and interior system integration, primary validation with aircraft OEMs tier suppliers and Australian MRO operators, triangulation using fleet data certification filings and trade flows, assumptions related to program delays material substitution and localization)

- Definition and Scope

- Market evolution

- Usage and replacement cycles in aircraft cabins

- Aerospace interior ecosystem structure

- Supply chain and distribution channels

- Regulatory and certification environment

- Growth Drivers

Rising domestic and regional aircraft fleet modernization

Increasing use of lightweight materials to reduce fuel burn

Growth in aircraft interior retrofits and cabin upgrades

Stringent fire smoke and toxicity requirements favoring advanced composites

Expansion of Australian MRO capabilities and defense aviation programs - Challenges

High certification and qualification costs for new composite materials

Dependence on imported prepregs fibers and resins

Limited local scale of aircraft OEM production

Supply chain disruptions and long lead times

Volatility in commercial aviation demand cycles - Opportunities

Defense aircraft interior refurbishment programs

Adoption of thermoplastic composites for faster processing

Localization of interior component manufacturing

Growth in business jet and special mission aircraft demand

Sustainability-driven demand for recyclable composite materials - Trends

Shift toward lighter sandwich panel constructions

Integration of fire-resistant and low-smoke composite technologies

Increased modularization of cabin interior components

Digital design and simulation in interior composite engineering

Collaboration between material suppliers and tier-one integrators - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2020–2025

- By Volume, 2020–2025

- By Installed Base, 2020–2025

- By Average Selling Price, 2020–2025

- By Fleet Type (in Value %)

Commercial narrow body aircraft

Commercial wide body aircraft

Regional and turboprop aircraft

Business jets

Military transport and patrol aircraft - By Application (in Value %)

Sidewalls and ceiling panels

Floor panels

Stowage bins and galleys

Lavatories and monuments

Seat structures and trim components - By Technology Architecture (in Value %)

Thermoset composites

Thermoplastic composites

Sandwich structures with honeycomb cores

Advanced fire-resistant composite laminates - By End-Use Industry (in Value %)

Commercial aviation

Business and general aviation

Defense and government aviation - By Connectivity Type (in Value %)

Non-connected structural interior components

Sensor-integrated interior panels

Smart cabin-ready composite structures - By Region (in Value %)

New South Wales

Victoria

Queensland

Western Australia

Rest of Australia

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (product portfolio depth, composite material capability, certification and compliance strength, manufacturing footprint, cost competitiveness, OEM partnerships, MRO engagement, innovation and R&D focus)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Safran Cabin

Collins Aerospace

Diehl Aviation

FACC

GKN Aerospace

Triumph Group

AIM Altitude

Jamco

Aviointeriors

Airbus Atlantic

Daher

Toray Advanced Composites

Hexcel

Solvay

Teijin Carbon

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase support and lifecycle service expectations

- By Value, 2026–2035

- By Volume, 2026–2035

- By Installed Base, 2026–2035

- By Average Selling Price, 2026–2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now