Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Australia Courier, Express, and Parcel market recorded a total market value of USD ~ billion, supported primarily by expanding digital commerce ecosystems, strong parcel delivery demand, and growing investments in automated logistics networks. Rapid online retail transactions, increased last-mile delivery requirements, and expanding cross-border e-commerce shipments continue strengthening parcel transportation volumes. Logistics companies increasingly deploy automated sorting hubs, route optimization software, and parcel locker infrastructure to improve delivery speed and operational efficiency across national supply chain networks.

Sydney, Melbourne, Brisbane, and Perth dominate the Australia Courier, Express, and Parcel market due to their dense population clusters, strong retail consumption patterns, and highly developed logistics infrastructure networks. These metropolitan regions host major distribution hubs, automated fulfillment warehouses, and international cargo gateways connecting domestic supply chains with global trade routes. Strong e-commerce participation among urban consumers, advanced transportation connectivity, and concentration of retail and manufacturing businesses significantly strengthen parcel delivery volumes across these cities.

Market Segmentation

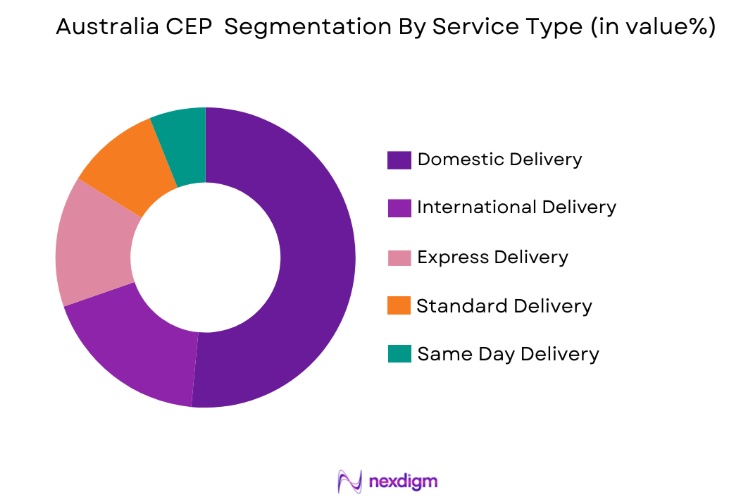

By Service Type

Australia Courier, Express, and Parcel market is segmented by service type into domestic delivery, international delivery, express delivery, standard delivery, and same-day delivery. Recently, domestic delivery has a dominant market share due to factors such as strong online retail activity, dense urban distribution networks, and increasing demand for rapid last mile fulfillment services. Australian e-commerce platforms process large volumes of domestic orders daily, requiring extensive courier networks connecting metropolitan warehouses with residential consumers. Major logistics companies maintain extensive ground transportation fleets and automated sorting facilities designed specifically for domestic parcel distribution across short and medium distances. Domestic shipments also benefit from lower operational complexity compared to international deliveries, allowing courier companies to offer cost-efficient pricing and faster delivery times. Retailers increasingly partner with national logistics providers to manage inventory distribution within the country, strengthening domestic shipment demand. Additionally, rapid expansion of same-day and next-day delivery expectations further supports domestic parcel movement across urban regions. Continuous investment in automated sorting hubs, parcel locker networks, and digital tracking technologies also improves domestic logistics efficiency, reinforcing the dominance of domestic delivery services across the national CEP ecosystem.

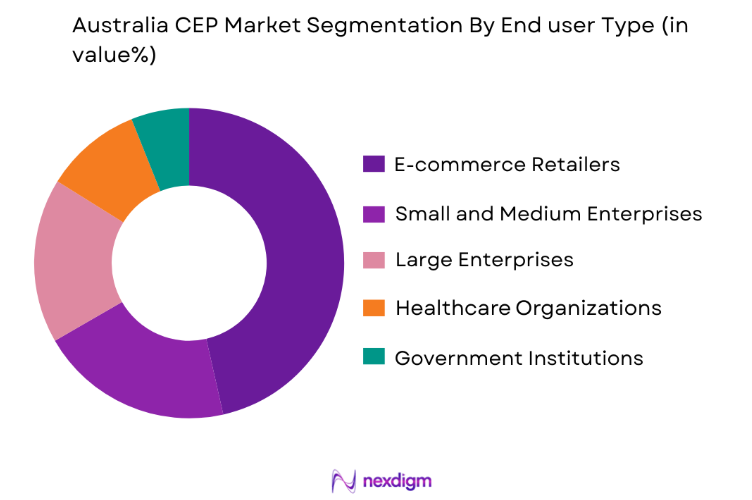

By End User

Australia Courier, Express, and Parcel market is segmented by end user into e-commerce retailers, small and medium enterprises, large enterprises, healthcare organizations, and government institutions. Recently, e-commerce retailers have a dominant market share due to strong digital retail adoption, growing consumer preference for online shopping platforms, and rising parcel shipment volumes across metropolitan areas. Online marketplaces process millions of product orders that require reliable delivery networks capable of handling large daily shipment volumes. Retail companies increasingly outsource logistics operations to third-party courier providers capable of managing order fulfillment, inventory distribution, and last-mile delivery services. The continued growth of mobile commerce platforms and digital payment ecosystems further accelerates online retail transactions across Australian consumers. Logistics providers also invest heavily in automated distribution facilities and smart routing technologies to support the operational requirements of high-volume online retailers. Increasing cross-border e-commerce activity also generates additional parcel shipments connecting domestic retailers with international markets. As digital retail ecosystems continue expanding across multiple consumer product categories, courier and parcel delivery services remain essential infrastructure supporting online commerce supply chains.

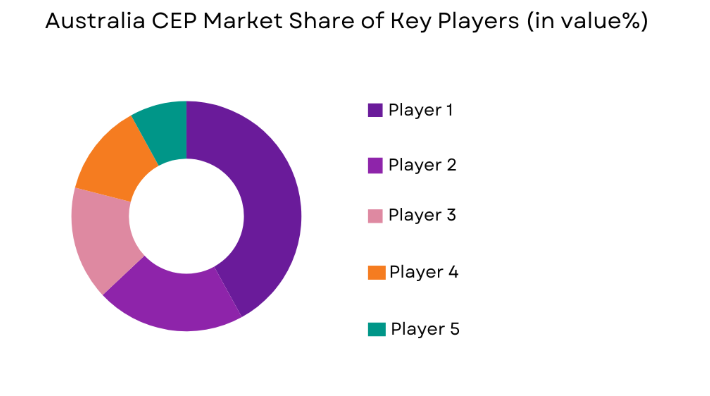

Competitive Landscape

The Australia Courier, Express, and Parcel market is moderately consolidated, with a combination of national postal operators, global logistics corporations, and regional courier companies competing across parcel delivery networks. Major companies focus heavily on expanding automated distribution centers, advanced route optimization technologies, and integrated logistics platforms to strengthen operational efficiency. Strategic partnerships with online retail platforms and cross-border logistics providers further enhance competitive positioning. Market competition is driven by service reliability, delivery speed, technological innovation, and nationwide logistics infrastructure capabilities.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Parcel Network Coverage |

| Australia Post | 1809 | Melbourne, Australia | ~ | ~ | ~ | ~ | ~ |

| DHL Group | 1969 | Bonn, Germany | ~ | ~ | ~ | ~ | ~ |

| FedEx Corporation | 1971 | Memphis, USA | ~ | ~ | ~ | ~ | ~ |

| UPS | 1907 | Atlanta, USA | ~ | ~ | ~ | ~ | ~ |

| Toll Group | 1888 | Melbourne, Australia | ~ | ~ | ~ | ~ | ~ |

Australia CEP Market Analysis

Growth Drivers

Expansion of E Commerce Retail and Digital Marketplace Logistics Networks

Rapid expansion of digital retail platforms across Australia significantly strengthens demand for courier, express, and parcel delivery services responsible for transporting goods from distribution centers to end consumers across metropolitan and regional areas. Online retail platforms generate extremely high daily order volumes for consumer electronics, apparel, groceries, household goods, and lifestyle products that require reliable logistics infrastructure capable of processing large parcel volumes efficiently. Logistics companies therefore invest heavily in automated parcel sorting hubs, intelligent warehouse management systems, and advanced route optimization software designed to improve operational efficiency across national distribution networks. Retailers increasingly partner with third-party logistics providers to manage inventory distribution and last-mile delivery operations without building their own transportation infrastructure. Mobile commerce applications and digital payment platforms also simplify purchasing behavior among consumers, encouraging frequent online shopping transactions that generate consistent parcel delivery demand. The rapid growth of marketplace platforms connecting domestic sellers with nationwide consumers further strengthens shipping volumes handled by courier providers. Logistics operators continuously expand urban distribution centers and regional delivery fleets to shorten shipping distances and accelerate fulfillment timelines across metropolitan markets. Growing cross-border e-commerce trade between Australia and international retail marketplaces further increases parcel shipments requiring integrated customs processing and international logistics coordination. As digital retail ecosystems continue expanding across multiple product categories, courier and parcel delivery services remain essential infrastructure supporting national e-commerce supply chains and consumer purchasing behavior.

Investment in Automated Logistics Infrastructure and Smart Parcel Delivery Systems

Increasing investment in advanced logistics technologies and automated distribution infrastructure significantly strengthens operational capabilities across the Australia Courier, Express, and Parcel market. Logistics providers continuously deploy automated parcel sorting systems, robotic handling technologies, and digital warehouse management platforms capable of processing high parcel volumes with minimal manual intervention. Automated distribution centers improve sorting accuracy, reduce processing time, and increase throughput capacity across national logistics networks. Courier companies also expand smart parcel locker networks across urban residential areas, allowing consumers to collect shipments conveniently without requiring home delivery scheduling. Advanced route optimization software and predictive analytics platforms enable logistics companies to reduce transportation costs while improving delivery speed and fleet productivity. Investment in electric delivery vehicles and sustainable logistics technologies further improves operational efficiency while supporting environmental sustainability objectives. Major courier operators also integrate real-time tracking platforms and digital customer communication systems to enhance shipment visibility and delivery reliability. Continuous expansion of last-mile delivery infrastructure across metropolitan and regional areas further improves network coverage and service quality. As logistics companies modernize operational infrastructure and adopt advanced technology solutions, the overall efficiency and scalability of the national CEP ecosystem continues strengthening, supporting long-term growth across Australia’s logistics sector.

Market Challenges

High Operational Costs and Logistics Complexity Across Remote Geographic Regions

High operational costs associated with transporting parcels across Australia’s geographically vast landscape represent a major challenge affecting courier, express, and parcel logistics providers operating nationwide. Australia’s dispersed population distribution and long transportation distances between major cities and regional communities significantly increase fuel consumption, labor expenses, and fleet maintenance costs for logistics operators. Delivering parcels to remote towns, rural communities, and isolated regions requires additional transportation coordination and extended travel distances, which increases operational expenditure compared with dense metropolitan delivery networks. Logistics companies often maintain additional distribution hubs and regional depots to ensure nationwide coverage, which further increases infrastructure investment requirements. Fluctuating fuel prices and transportation costs also influence operational profitability across courier networks. Additionally, limited transportation infrastructure in certain regional areas can delay shipments and complicate delivery scheduling. Courier providers must continuously balance delivery speed expectations with operational cost efficiency when serving remote geographic regions. Seasonal weather disruptions and transportation delays can also impact parcel distribution schedules across long-distance logistics corridors. As parcel shipment volumes increase due to digital retail expansion, managing operational costs across large geographic distances remains a persistent challenge influencing profitability and service pricing across the national courier logistics ecosystem.

Labor Shortages and Workforce Management Constraints in Logistics Operations

Workforce shortages and labor management challenges represent another major constraint affecting operational efficiency across the Australia Courier, Express, and Parcel logistics sector. The logistics industry requires a large workforce including drivers, warehouse personnel, parcel handlers, and logistics coordinators responsible for processing and delivering high parcel volumes daily. Increasing demand for parcel delivery services places additional pressure on logistics companies to recruit and retain skilled employees capable of operating automated logistics facilities and transportation fleets. Competition for skilled labor across transportation and warehousing industries also contributes to workforce shortages. Logistics companies must therefore offer competitive compensation packages and improved working conditions to attract qualified employees. High employee turnover rates within the delivery sector can also disrupt operational consistency and increase recruitment and training expenses for logistics providers. Additionally, managing delivery workforce scheduling across fluctuating parcel volumes during peak retail seasons creates additional operational complexity. Rapid growth of e-commerce shipments requires logistics companies to continuously expand workforce capacity across distribution centers and transportation fleets. Automation technologies help mitigate certain labor shortages, but skilled technicians and logistics specialists remain necessary to manage complex supply chain systems. Ensuring stable workforce availability therefore remains a critical operational challenge influencing service reliability and logistics network productivity across the Australian CEP market.

Opportunities

Expansion of Smart Parcel Locker Networks and Contactless Delivery Infrastructure

Rapid expansion of smart parcel locker networks and contactless delivery solutions represents a significant opportunity for courier, express, and parcel logistics providers across Australia. Urban population density and increasing online retail activity generate high parcel volumes requiring convenient delivery options for consumers living in apartment complexes and densely populated residential areas. Parcel locker systems allow customers to collect deliveries securely from automated storage units located in residential buildings, shopping centers, and transportation hubs. These systems reduce delivery failure rates associated with unattended home deliveries and significantly improve logistics efficiency by consolidating multiple parcel drop-offs into centralized locations. Logistics companies increasingly deploy intelligent locker systems integrated with digital tracking platforms that notify customers when shipments are available for collection. Contactless delivery technologies also improve convenience and safety for both delivery personnel and consumers. Retailers and logistics providers collaborate to expand parcel locker installations across metropolitan regions, further strengthening last-mile delivery infrastructure. Automated locker networks also enable courier companies to handle higher parcel volumes without proportionally increasing delivery workforce requirements. As urban housing density continues increasing across major Australian cities, parcel locker solutions represent a scalable logistics infrastructure capable of supporting future parcel delivery demand while improving operational efficiency across last-mile distribution networks.

Growth of Cross Border E Commerce Logistics and International Parcel Transportation

Expanding cross-border e-commerce activity presents substantial growth opportunities for the Australia Courier, Express, and Parcel market as international retail transactions continue increasing across global online marketplaces. Australian consumers frequently purchase products from international retailers located in Asia, North America, and Europe, generating a growing volume of inbound international parcel shipments. At the same time, Australian businesses increasingly sell goods through global online platforms, requiring efficient outbound logistics services capable of transporting products to overseas markets. Courier and logistics providers therefore expand international freight forwarding networks, customs clearance services, and air cargo transportation capabilities to support cross-border parcel movement. Advanced digital documentation platforms simplify customs processing and regulatory compliance procedures for international shipments. Logistics providers also collaborate with international courier networks to create integrated delivery systems capable of handling global parcel transportation efficiently. Improvements in international air cargo connectivity and logistics infrastructure further strengthen cross-border parcel distribution capabilities. As global e-commerce ecosystems continue expanding and consumers increasingly purchase goods from international sellers, cross-border logistics services represent a major revenue growth opportunity for courier and parcel delivery providers operating within the Australian logistics ecosystem.

Future Outlook

The Australia Courier, Express, and Parcel market is expected to experience steady expansion driven by increasing digital retail adoption, logistics automation, and strong consumer demand for fast parcel delivery services. Investments in automated sorting facilities, smart delivery technologies, and sustainable transportation systems are likely to strengthen operational efficiency across logistics networks. Government infrastructure development and urban logistics modernization programs may further support distribution capabilities. Rising cross-border trade and e-commerce logistics integration will continue shaping the competitive landscape of the national CEP ecosystem.

Major Players

- Australia Post

- DHL Group

- FedEx Corporation

- UPS

- Toll Group

- Aramex Australia

- CouriersPlease

- StarTrack

- TNT Express Australia

- Border Express

- Allied Express

- Fastway Couriers

- Direct Freight Express

- Zoom2u

- Singapore Post Logistics

Key Target Audience

- E-commerce Retail Companies

- Logistics and Supply Chain Operators

- Transportation Infrastructure Developers

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies

- International Trade Organizations

- Retail Distribution Companies

- Technology Providers for Logistics Automation

Research Methodology

Step 1: Identification of Key Variables

The research process begins by identifying critical variables affecting the Australia Courier, Express, and Parcel market. These include logistics infrastructure development, parcel delivery demand, technological adoption in distribution centers, and e-commerce transaction volumes. Relevant macroeconomic indicators and supply chain performance metrics are also evaluated to understand demand drivers and operational trends.

Step 2: Market Analysis and Construction

Extensive secondary research is conducted using industry databases, logistics reports, company financial disclosures, and government transportation statistics. Market segmentation models are constructed to analyze service types, end users, and logistics infrastructure distribution across Australia’s major regions and metropolitan logistics hubs.

Step 3: Hypothesis Validation and Expert Consultation

Initial analytical findings are validated through consultation with logistics industry professionals, transportation analysts, and supply chain management specialists. Their insights help refine market assumptions, verify operational trends, and strengthen analytical accuracy regarding courier logistics infrastructure and parcel delivery demand.

Step 4: Research Synthesis and Final Output

All validated data sources, industry insights, and analytical findings are synthesized into a comprehensive market framework. Quantitative and qualitative information is integrated to produce a structured analysis of market dynamics, segmentation trends, competitive landscape, and future outlook for the Australia CEP logistics sector.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rapid Expansion of E Commerce Retail Distribution

Rising Demand for Same Day and Next Day Parcel Delivery

Growth of Cross Border Online Retail Trade - Market Challenges

High Last Mile Delivery Costs in Remote Regions

Operational Complexity in Urban Congestion Zones

Labor Shortages in Logistics and Transportation - Market Opportunities

Expansion of Automated Parcel Sorting Infrastructure

Growth of Smart Parcel Locker Networks

Integration of Advanced Route Optimization Technologies - Trends

Adoption of Automated Parcel Sorting and Robotics

Growth of Sustainable Electric Delivery Fleets

Expansion of Digital Shipment Tracking Platforms - Government Regulations

- SWOT Analysis of Key Competitors

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Domestic Parcel Delivery Services

International Express Shipping

Same Day Delivery Services

Next Day Delivery Services

Economy Parcel Delivery Services - By Platform Type (In Value%)

Road Transportation Networks

Air Express Cargo Networks

Rail Integrated Parcel Networks

Multimodal Logistics Platforms

Digital Parcel Management Platforms - By Fitment Type (In Value%)

Automated Parcel Sorting Systems

Manual Handling Logistics Operations

Hybrid Sorting Facilities

Smart Locker Delivery Systems

Micro Fulfillment Distribution Centers - By EndUser Segment (In Value%)

E Commerce Retailers

Small and Medium Enterprises

Large Enterprises and Corporations

- Market Share Analysis

- CrossComparison Parameters (Service Coverage Network, Delivery Speed, Pricing Structure, Technology Integration, Parcel Handling Capacity)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

Australia Post

DHL Express Australia

FedEx Australia

UPS Australia

Toll Group

Aramex Australia

CouriersPlease

Sendle

TNT Australia

StarTrack

Border Express

Allied Express

Fastway Couriers Australia

Direct Freight Express

Zoom2u

- E Commerce Retailers Driving High Parcel Shipment Volumes

- SMEs Increasing Adoption of Outsourced Parcel Logistics

- Healthcare Sector Expanding Temperature Controlled Parcel Distribution

- Government Agencies Supporting National Postal Infrastructure Modernization

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now