Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Australia Cloud Infrastructure Market reached approximately USD ~ billion, supported by enterprise cloud migration, hyperscale data center expansion, and sustained investment from global cloud providers including AWS, Microsoft, and Google. Strong demand for AI workloads, SaaS adoption, and digital government platforms accelerated spending on compute servers, storage infrastructure, networking systems, and data center power and cooling equipment across commercial and public sector cloud deployments nationwide.

Sydney and Melbourne dominate cloud infrastructure deployment due to concentration of hyperscale data centers, subsea cable connectivity, enterprise headquarters, and financial and technology industries requiring large-scale cloud capacity. New South Wales benefits from dense internet exchange ecosystems and global cloud regions, while Victoria hosts major colocation campuses and renewable-powered data centers. Canberra supports sovereign government cloud infrastructure and secure data hosting environments driven by federal digital transformation and cybersecurity requirements.

Market Segmentation

By Product Type

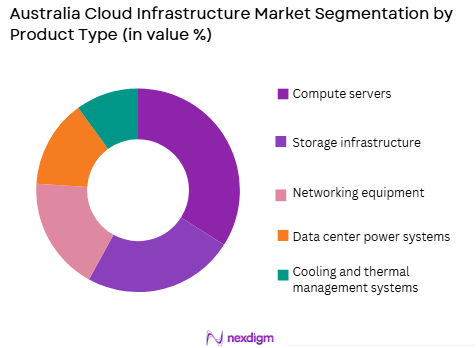

Australia Cloud Infrastructure market is segmented by product type into compute servers, storage infrastructure, networking equipment, data center power systems, and cooling and thermal management systems. Recently, compute servers has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Compute servers dominate because hyperscale cloud providers prioritize large-scale processing capacity to support AI, analytics, and enterprise cloud workloads, driving substantial investment into high-density server clusters across Australian data centers. Rapid adoption of generative AI and machine learning platforms increases demand for GPU-accelerated servers and specialized compute architectures. Enterprise cloud migration from on-premise environments further shifts infrastructure spending toward centralized compute capacity. Hyperscale providers deploy modular server farms to scale cloud regions quickly in response to demand growth. Data sovereignty regulations encourage domestic cloud capacity expansion, reinforcing compute infrastructure investment. Server hardware refresh cycles remain shorter than other infrastructure categories, sustaining recurring capital expenditure. As cloud services evolve toward compute-intensive applications, compute servers structurally retain the largest share within Australia’s cloud infrastructure market.

By Deployment Type

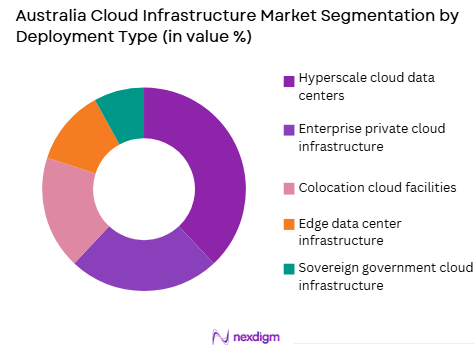

Australia Cloud Infrastructure market is segmented by deployment type into hyperscale cloud data centers, enterprise private cloud infrastructure, colocation cloud facilities, edge data center infrastructure, and sovereign government cloud infrastructure. Recently, hyperscale cloud data centers has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Hyperscale data centers dominate because global cloud providers continue expanding Australian cloud regions to support enterprise digital transformation, AI services, and SaaS platform delivery across Asia-Pacific markets. Australia’s strong connectivity, stable regulatory environment, and renewable energy availability attract hyperscale investments from major cloud operators. Large enterprises increasingly migrate workloads to hyperscale platforms rather than maintaining private infrastructure. Hyperscale facilities benefit from economies of scale in power, cooling, and networking efficiency, lowering cost per compute unit. Government cloud adoption strategies also leverage hyperscale providers for scalable infrastructure. Rapid growth of AI cloud services further concentrates investment into hyperscale campuses. These structural demand factors sustain hyperscale cloud data centers as the leading deployment segment in Australia’s cloud infrastructure market.

Competitive Landscape

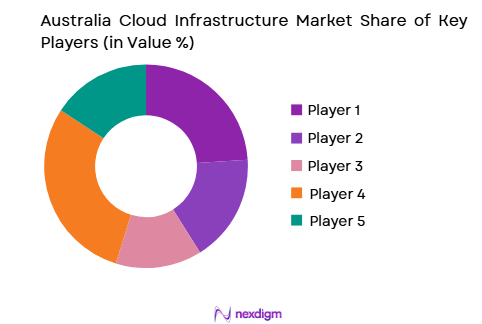

The Australia Cloud Infrastructure Market is highly concentrated around global hyperscale cloud providers and multinational data center infrastructure vendors that dominate compute, storage, and networking deployments across Australian cloud regions. Domestic colocation operators and engineering firms support hyperscale facility construction and infrastructure integration. Competition centers on scale of cloud regions, AI compute capacity, renewable-powered data centers, and compliance with data sovereignty and security standards required by enterprise and government customers.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Cloud Infrastructure Role |

| Amazon Web Services | 2006 | USA | ~ | ~ | ~ | ~ | ~ |

| Microsoft | 1975 | USA | ~ | ~ | ~ | ~ | ~ |

| 1998 | USA | ~ | ~ | ~ | ~ | ~ | |

| Equinix | 1998 | USA | ~ | ~ | ~ | ~ | ~ |

| NextDC | 2010 | Australia | ~ | ~ | ~ | ~ | ~ |

Australia Cloud Infrastructure Market Analysis

Growth Drivers

Hyperscale Cloud Region Expansion and AI Workload Demand

Australia’s cloud infrastructure growth is primarily driven by continuous expansion of hyperscale cloud regions and rapidly increasing demand for AI and machine learning workloads across enterprises and digital platforms. Global cloud providers are investing heavily in Australian data center campuses to deliver scalable compute, storage, and AI processing capacity within national borders to meet data sovereignty requirements. Generative AI adoption across industries significantly increases demand for GPU clusters, high-performance compute servers, and high-speed networking infrastructure, structurally elevating infrastructure investment intensity. Enterprises migrating mission-critical applications, analytics platforms, and SaaS environments to cloud further accelerate hyperscale infrastructure deployment. Hyperscale providers scale server farms, storage arrays, and interconnection networks in modular architectures to rapidly expand capacity in response to demand growth. Australia’s geographic position as a digital gateway to Asia-Pacific also supports regional cloud capacity investments serving multinational enterprises. Renewable energy integration into hyperscale facilities further enables large-scale data center expansion aligned with sustainability mandates. Government cloud adoption strategies leverage hyperscale platforms for digital services and secure data hosting, reinforcing infrastructure investment momentum. The convergence of AI compute demand, enterprise cloud migration, and hyperscale region expansion structurally drives sustained growth in Australia’s cloud infrastructure market.

Enterprise Digital Transformation and Cloud Migration Acceleration

Widespread enterprise digital transformation across finance, retail, healthcare, government, and telecommunications sectors is accelerating migration from on-premise IT infrastructure to cloud environments, driving sustained investment in Australia’s cloud infrastructure. Organizations increasingly adopt cloud-native architectures, microservices platforms, and SaaS ecosystems requiring scalable compute, storage, and networking capacity within domestic cloud regions. Legacy data center consolidation initiatives shift capital expenditure toward centralized cloud infrastructure operated by hyperscale and colocation providers. Hybrid and multi-cloud strategies expand entsage for cooling systems also presents environmental considerations in certain regions. These energy and sustainability factors create constraints on the pace and location of cloud infrastructure expansion despite strong demand growth.

Data Sovereignty, Security, and Regulatory Compliance Complexity

Cloud infrastructurenerprise demand for interconnection infrastructure and distributed cloud capacity across Australian metropolitan regions. Regulatory compliance and data residency requirements further incentivize domestic cloud infrastructure deployment to host sensitive workloads locally. AI-driven analytics, digital customer platforms, and remote workforce technologies increase enterprise reliance on cloud compute resources. Telecommunications 5G rollout and edge computing adoption also expand cloud infrastructure footprints supporting low-latency services. Government digital service modernization programs mirror enterprise cloud migration patterns. These combined digital transformation forces create structurally sustained demand for cloud infrastructure expansion across Australia’s economy.

Market Challenges

High Energy Consumption and Data Center Sustainability Constraints

Cloud infrastructure expansion in Australia faces significant challenges from high energy consumption requirements and sustainability constraints associated with large-scale data center operations. Hyperscale cloud facilities require substantial electrical capacity for compute clusters, cooling systems, and networking infrastructure, placing pressure on regional power grids and energy supply planning. Renewable energy procurement and grid connection approvals can delay data center development timelines and increase infrastructure costs. Australia’s energy price volatility and transmission constraints affect long-term operating economics for hyperscale providers and colocation operators. Cooling infrastructure in certain climate regions requires advanced thermal management systems increasing capital intensity. Community concerns regarding energy usage and environmental impact can influence planning approvals for new data center campuses.

Sustainability reporting and carbon reduction commitments impose additional investment into energy-efficient infrastructure and renewable sourcing agreements

Water u providers in Australia must navigate complex data sovereignty, cybersecurity, and regulatory compliance requirements that increase infrastructure design and operational complexity. Government and regulated industries require cloud environments compliant with national security, privacy, and critical infrastructure protection standards, necessitating secure data center architectures and localized infrastructure deployment. Sovereign cloud requirements mandate physical data residency and restricted operational control within national jurisdictions, influencing infrastructure investment patterns. Compliance with financial, healthcare, and government data regulations requires dedicated secure zones within cloud facilities and certified infrastructure controls. Security certification processes and regulatory audits increase deployment timelines and operational costs for cloud providers. Cross-border data transfer restrictions influence interconnection architecture and network design. Multi-tenant cloud environments must incorporate advanced segmentation and encryption infrastructure to meet compliance mandates. Evolving cybersecurity regulations and critical infrastructure protections continue raising infrastructure requirements. These regulatory and security complexities create structural challenges in scaling cloud infrastructure efficiently across Australia.

Opportunities

AI-Optimized Data Center and GPU Cloud Infrastructure Development

Rapid growth of artificial intelligence applications across industries creates substantial opportunities for developing AI-optimized cloud infrastructure and specialized GPU data centers in Australia. AI training and inference workloads require high-density compute clusters, advanced cooling architectures, and ultra-fast interconnect networks beyond conventional cloud infrastructure design. Hyperscale and specialized cloud providers can invest in AI-focused data center campuses optimized for GPU and accelerator deployment to support regional AI demand. Australia’s research institutions and AI startups also require scalable domestic AI cloud infrastructure for model development and deployment. Government AI strategies and industry adoption programs further stimulate demand for local AI compute capacity. AI infrastructure development also aligns with Australia’s renewable energy resources enabling sustainable high-density compute facilities. Regional AI cloud capacity can serve Asia-Pacific markets with low-latency AI services. Specialized AI cloud infrastructure offers higher value-added services compared to general-purpose cloud capacity. This emerging AI infrastructure segment presents a major growth opportunity within Australia’s cloud infrastructure market.

Edge Cloud and Distributed Infrastructure for 5G and Digital Services

Expansion of 5G networks, IoT applications, and low-latency digital services presents opportunities for distributed edge cloud infrastructure deployment across Australia. Telecommunications operators and cloud providers are establishing edge data centers closer to population centers to support latency-sensitive applications such as autonomous systems, smart cities, and real-time analytics. Edge cloud infrastructure complements hyperscale regions by enabling localized compute and storage capacity. Growth of connected devices and industrial IoT platforms increases demand for distributed processing infrastructure nationwide. Government smart infrastructure and digital economy initiatives further support edge deployment. Edge data centers also enhance resilience and redundancy for national cloud services. Regional economic development programs encourage digital infrastructure investment beyond major metropolitan hubs. Integration of edge and hyperscale architectures creates new infrastructure investment pathways. Distributed cloud ecosystems therefore offer significant expansion potential within Australia’s evolving cloud infrastructure landscape.

Future Outlook

Australia’s cloud infrastructure market is expected to grow strongly over the next five years driven by hyperscale region expansion, AI compute demand, and enterprise cloud migration. AI-optimized data centers, edge cloud deployment, and sovereign government cloud platforms will shape infrastructure investment trends. Renewable-powered hyperscale facilities and sustainability-compliant data centers will expand capacity nationwide. Regulatory support for digital economy growth and secure cloud adoption will further sustain infrastructure demand.

Major Players

- Amazon Web Services

- Microsoft

- Equinix

- NextDC

- Oracle

- IBM

- Alibaba Cloud

- Huawei Cloud

- Digital Realty

- Vantage Data Centers

- Macquarie Data Centres

- Fujitsu

- HPE

- Dell Technologies

Key Target Audience

- Cloud service providers

- Data center operators

- Telecommunications companies

- Enterprises and large IT users

- Investments and venture capitalist firms

- Government and regulatory bodies

- AI and software platform companies

- Financial institutions

Research Methodology

Step 1: Identification of Key Variables

Cloud infrastructure investment categories including compute, storage, networking, power, cooling, and deployment models were identified through cloud provider financial disclosures, data center investment databases, and digital infrastructure policy frameworks. Demand drivers across hyperscale, enterprise, and government cloud segments were mapped to infrastructure spending components.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed using data center capacity additions, cloud provider capital expenditure, and server deployment estimates across Australia. Infrastructure component spending ratios and facility deployment patterns were synthesized to derive segment shares and market structure.

Step 3: Hypothesis Validation and Expert Consultation

Market assumptions regarding hyperscale dominance, compute infrastructure share, and deployment patterns were validated through cloud infrastructure engineers, data center operators, and digital infrastructure analysts. Cross-verification ensured alignment with actual Australian cloud deployment trends.

Step 4: Research Synthesis and Final Output

Validated quantitative and qualitative inputs were integrated into a structured cloud infrastructure market model covering segmentation, drivers, challenges, and opportunities. Competitive landscape and outlook were derived from hyperscale investment trajectories and enterprise cloud adoption patterns.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising hyperscale cloud region investments across Australia

Enterprise migration to cloud-native and AI workloads

Government sovereign cloud and data localization initiatives - Market Challenges

High energy and land costs for large data centers

Grid capacity and renewable power availability constraints

Data sovereignty and compliance complexity - Market Opportunities

Expansion of regional edge and metro data centers

Development of renewable-powered hyperscale campuses

Public sector sovereign cloud infrastructure programs - Trends

Shift toward high-density AI-optimized data centers

Adoption of liquid cooling and advanced thermal systems

Growth of multi-cloud and hybrid infrastructure architectures - Government regulations

Critical infrastructure and data security regulations

National data sovereignty and privacy compliance frameworks

Energy efficiency and carbon reporting standards - SWOT analysis

- Porters Five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Compute server infrastructure

Storage infrastructure systems

Network and switching infrastructure

Data center power systems

Cooling and thermal management systems - By Platform Type (In Value%)

Hyperscale cloud data centers

Enterprise private cloud infrastructure

Edge data center infrastructure

Colocation cloud facilities

Sovereign government cloud platforms - By Fitment Type (In Value%)

Greenfield data center builds

Brownfield data center expansions

Modular prefabricated deployments

On-premise enterprise installations

Hybrid multi-site integrations - By EndUser Segment (In Value%)

Cloud service providers

Large enterprises

Government and public sector agencies

Telecommunications operators

Financial and digital service firms - By Procurement Channel (In Value%)

Direct OEM procurement

Systems integrator contracts

Colocation provider sourcing

EPC turnkey contractors

Government digital infrastructure tenders

- Market Share Analysis

- Cross Comparison Parameters (Data Center Scale, Power Density Capability, Cooling Technology, Network Connectivity, Sovereign Compliance, Energy Efficiency, Latency Performance, Automation Level)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Amazon Web Services

Microsoft Azure

Google Cloud

Oracle Cloud

IBM Cloud

Equinix

Digital Realty

NEXTDC

AirTrunk

Keppel Data Centres

NTT Global Data Centers

Schneider Electric

Vertiv

Huawei Cloud

Alibaba Cloud

- Hyperscale providers expanding sovereign and AI regions

- Enterprises accelerating hybrid cloud modernization

- Government agencies adopting secure sovereign platforms

- Telecom operators deploying edge cloud infrastructure

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now