Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Australia Cold Chain Logistics market is valued at USD ~ billion based on a recent historical assessment, driven by increasing demand for temperature-sensitive goods across food, pharmaceutical, and biotechnology sectors. Expanding e-commerce and grocery delivery services are fueling investments in cold storage warehouses, refrigerated transport fleets, and automated monitoring systems. Rising consumer expectations for product quality and safety compel supply chain operators to enhance real-time tracking and temperature control mechanisms. Government regulations on food safety and healthcare logistics further reinforce the necessity for reliable cold chain solutions. Strategic partnerships between logistics providers and retailers optimize distribution networks and reduce spoilage. Investments in energy-efficient refrigeration and IoT-based monitoring systems also support operational sustainability.

Australia’s cold chain logistics landscape is concentrated in cities such as Sydney, Melbourne, and Brisbane due to dense population centers and robust transport infrastructure facilitating last-mile delivery. Major seaports such as Port of Melbourne and Port of Brisbane facilitate large volumes of refrigerated cargo including dairy, meat, and fresh produce destined for international markets. Advanced refrigerated warehouses and logistics hubs located near these ports improve export efficiency and product quality. Expanding pharmaceutical distribution networks across metropolitan healthcare clusters further increase the need for compliant cold chain transportation infrastructure.

Market Segmentation

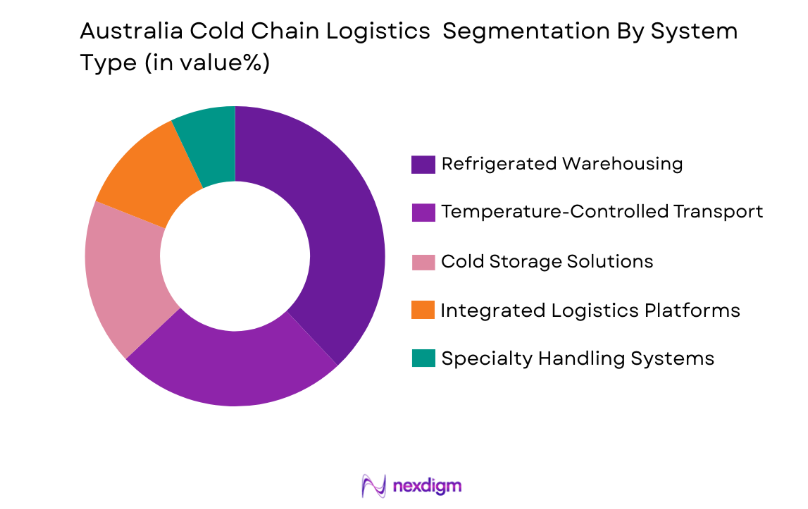

By System Type

Australia Cold Chain Logistics market is segmented by system type into refrigerated warehousing, temperature-controlled transport, cold storage solutions, integrated logistics platforms, and specialty handling systems. Recently, refrigerated warehousing has a dominant market share due to factors such as high demand from food manufacturers and pharmaceutical companies, availability of advanced infrastructure, proximity to ports and distribution centers, and increasing e-commerce fulfillment requirements. Investment in automated storage and retrieval technologies, combined with IoT-enabled monitoring and energy-efficient refrigeration systems, supports large-scale operations. Brand presence of established logistics providers and partnerships with end users facilitate reliability and scalability. Demand for high-value, perishable products reinforces warehouse-centric operations. Regulatory compliance for safety and quality further necessitates controlled storage environments. The versatility of refrigerated warehouses in serving multiple industries enhances adoption. Integration with transportation networks ensures product integrity throughout the supply chain, making refrigerated warehousing the most preferred system type.

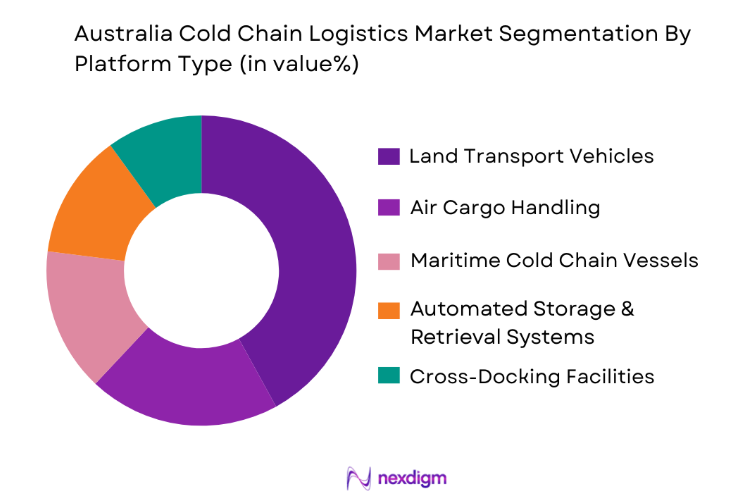

By Platform Type

Australia Cold Chain Logistics market is segmented by platform type into land transport vehicles, air cargo handling, maritime cold chain vessels, automated storage and retrieval systems, and cross-docking facilities. Recently, land transport vehicles have a dominant market share due to factors such as extensive road networks connecting urban centers, adaptability to last-mile delivery, high frequency of shipments for perishable goods, integration with e-commerce logistics, and cost-efficiency relative to air or maritime alternatives. Urban distribution hubs are designed to accommodate temperature-controlled trucks for rapid dispatch. The presence of advanced refrigeration units and GPS-enabled tracking systems enhances reliability. Demand from food and pharmaceutical sectors requiring timely delivery supports vehicle-based platforms. Government regulations on vehicle standards and cold storage compliance ensure adherence to safety norms. Investment in hybrid and electric fleets is rising to reduce emissions and operational costs. Flexibility in route planning allows coverage of regional agricultural zones and metropolitan retail networks.

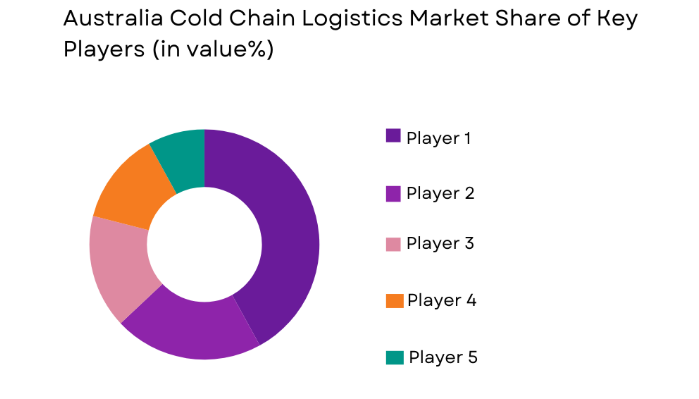

Competitive Landscape

The Australia Cold Chain Logistics market exhibits a moderately consolidated competitive landscape with a few dominant players leveraging advanced technologies, large-scale infrastructure, and extensive distribution networks. Key operators focus on expanding service portfolios through acquisitions, strategic partnerships, and geographic expansion. Innovation in IoT-based monitoring, energy-efficient refrigeration, and automated warehouse solutions differentiates market leaders. Operational excellence, regulatory compliance, and strong client relationships provide competitive advantages. Companies are also investing in green logistics initiatives to align with environmental regulations. The influence of major players shapes market pricing, service standards, and adoption of emerging technologies, encouraging smaller firms to specialize or form alliances.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Cold Storage Capacity (units) |

| Toll Group | 1888 | Melbourne, Australia | ~ | ~ | ~ | ~ | ~ |

| Linfox | 1956 | Melbourne, Australia | ~~ | ~ | ~ | ~ | ~ |

| Mainfreight | 1978 | Auckland, New Zealand | ~ | ~ | ~ | ~ | ~ |

| DHL Supply Chain | 1969 | Bonn, Germany | ~ | ~ | ~ | ~ | ~ |

| Kuehne + Nagel | 1890 | Schindellegi, Switzerland | ~ | ~ | ~ | ~ | ~ |

Australia Cold Chain Logistics Market Analysis

Growth Drivers

Expansion of E-Commerce and Online Grocery Channels

The expansion of e-commerce and online grocery channels: the growing prevalence of online food, grocery, and pharmaceutical ordering platforms in Australia has significantly increased the demand for efficient cold chain logistics solutions. Consumers expect rapid delivery of perishable and temperature-sensitive goods, compelling logistics operators to enhance refrigerated transport, automated warehousing, and last-mile fulfillment capabilities. The surge in digital retail adoption drives investment in urban micro-distribution hubs equipped with advanced refrigeration and IoT monitoring systems to maintain product integrity. Strategic partnerships between logistics providers and online retailers improve distribution efficiency and reduce spoilage rates. Increased volume of small parcel shipments necessitates flexible transport fleets capable of handling temperature-controlled goods. Government initiatives supporting digital commerce infrastructure and food safety standards also reinforce the need for robust cold chain networks. Rising competition among e-commerce platforms encourages adoption of technology-driven logistics solutions. Investment in scalable cold storage facilities ensures rapid response to fluctuating demand, mitigating risks of stockouts or spoilage. Expansion of online marketplaces enhances nationwide coverage, integrating rural and regional supply chains into urban logistics networks, further strengthening demand for sophisticated cold chain systems.

Increasing Demand for Pharmaceutical Cold Storage

The increasing demand for pharmaceutical cold storage: Australia’s pharmaceutical sector growth, including biotechnology and vaccine production, has intensified the need for reliable cold chain logistics capable of maintaining precise temperature conditions. Regulatory requirements for drug storage, handling, and transport necessitate advanced refrigerated warehouses, monitoring systems, and temperature-controlled vehicles. Rising imports of biologics and vaccines require specialized logistics networks with robust tracking and compliance protocols. Investments in automated storage and retrieval technologies improve efficiency and reduce human error, ensuring consistent quality of temperature-sensitive pharmaceuticals. Strategic alliances between logistics providers and healthcare organizations enable streamlined distribution from manufacturing facilities to hospitals and pharmacies. Advanced IoT-enabled monitoring systems allow real-time tracking of temperature, humidity, and transit conditions, preventing product degradation. The growing emphasis on vaccination programs and personalized medicine increases shipment volumes, creating steady demand for cold chain capacity expansion. Technological integration with inventory management and regulatory compliance platforms enhances transparency and accountability throughout the supply chain. Continued R&D in pharmaceuticals coupled with e-health initiatives drives further adoption of cold chain logistics solutions across metropolitan and regional areas. Investment in specialized cold storage infrastructure provides competitive differentiation, attracting high-value pharmaceutical clients and ensuring long-term market growth.

Market Challenges

High Operational and Energy Costs

managing temperature-sensitive logistics infrastructure in Australia entails significant operational expenses, including electricity for refrigeration, maintenance of vehicles and warehouses, and workforce management. Fluctuations in energy prices directly impact operational budgets, necessitating investment in energy-efficient technologies such as solar-powered refrigeration and smart HVAC systems. Maintenance of specialized vehicles with temperature control capabilities increases operational complexity and cost. Skilled labor is required to operate sophisticated automated systems, adding to human resource expenses. Regulatory compliance for safety and product integrity requires frequent audits, inspections, and certification, further increasing costs. Evolving standards in cold chain operations necessitate ongoing training programs and technology upgrades. Balancing service reliability with cost containment is challenging for smaller operators, potentially limiting expansion. Supply chain disruptions, such as fuel price volatility or equipment failure, amplify cost pressures. Investment in sustainable energy solutions mitigates long-term expenses, but upfront capital requirements can restrict adoption. Overall, high operational and energy costs remain a persistent barrier to profitability and market efficiency.

Regulatory Compliance and Cross-Border Restrictions

navigating Australia’s stringent regulatory landscape for cold chain logistics poses significant challenges for operators handling perishable and pharmaceutical goods. Adherence to food safety standards, pharmaceutical storage protocols, and transport regulations requires meticulous documentation, monitoring, and frequent audits. Cross-border shipments face additional compliance obligations, including customs clearance, import/export licenses, and temperature verification reports. Non-compliance can result in penalties, shipment delays, or product loss, impacting service reliability and client trust. Integrating regulatory requirements into operational workflows increases administrative burden. Continuous updates to regulatory frameworks necessitate staff training and system upgrades. International trade agreements and quarantine requirements further complicate distribution networks. Investment in compliance management systems and technology-enabled monitoring platforms helps mitigate risks, but increases operational complexity. Logistics providers must maintain consistent quality across multi-jurisdictional operations, balancing efficiency with adherence to laws. Regulatory compliance and cross-border restrictions remain a significant market challenge, affecting scalability and profitability.

Opportunities

Integration of IoT and Smart Temperature Monitoring

implementing IoT-based solutions in Australia’s cold chain logistics offers significant opportunities to enhance operational efficiency, product integrity, and real-time monitoring. Smart sensors and connected devices provide continuous tracking of temperature, humidity, and location across warehouses and transport fleets. Integration with cloud platforms enables centralized visibility, predictive maintenance, and automated alerts in case of deviations. Retailers, pharmaceutical companies, and e-commerce platforms increasingly demand transparency and traceability, driving adoption of IoT-enabled solutions. Data analytics from connected devices allow optimization of routes, storage conditions, and inventory management. Energy consumption can be monitored and adjusted dynamically, reducing operational costs and carbon footprint. Integration of blockchain with IoT ensures secure documentation and compliance verification, enhancing trust with stakeholders. Partnerships between technology providers and logistics operators facilitate deployment of scalable solutions across metropolitan and regional areas. Customizable dashboards and mobile access improve decision-making speed and responsiveness. Adoption of smart temperature monitoring strengthens Australia’s cold chain resilience against spoilage, regulatory violations, and operational inefficiencies, creating a strong competitive advantage for early adopters.

Development of Automated and Modular Cold Chain Facilities

investing in automated, modular storage and distribution infrastructure represents a significant opportunity to meet Australia’s growing demand for flexible, scalable, and efficient cold chain logistics. Modular facilities can be deployed rapidly in urban centers or regional zones, adapting to varying demand levels while minimizing construction timelines and costs. Automation technologies, including robotic picking, automated conveyors, and temperature-controlled storage systems, enhance operational efficiency, reduce human error, and maintain product quality. Integration with advanced warehouse management software allows seamless coordination with transport fleets and e-commerce fulfillment operations. Modular design facilitates energy efficiency, adaptability to changing regulations, and scalability for seasonal peaks. Partnerships with technology providers enable continuous upgrading of automation capabilities. Growing demand from pharmaceutical and food sectors necessitates high-capacity, reliable infrastructure. Real-time monitoring and predictive maintenance systems reduce downtime and operational risk. Modular facilities also support multi-client operations, enabling service diversification and revenue expansion. Overall, the development of automated and modular cold chain facilities positions operators to capture emerging market demand efficiently, strengthening competitive positioning and long-term growth prospects.

Future Outlook

Australia’s Cold Chain Logistics market is expected to experience steady growth over the next five years, driven by expansion in e-commerce, pharmaceutical logistics, and food distribution networks. Technological developments such as IoT-enabled monitoring, automation, and energy-efficient refrigeration will enhance operational efficiency and product integrity. Supportive government regulations and investment incentives encourage infrastructure development. Demand-side factors, including urbanization, increasing consumer expectations, and export-oriented perishable goods, will sustain market expansion. Strategic partnerships and facility modernization are anticipated to improve nationwide distribution coverage and responsiveness.

Major Players

- Toll Group

- Linfox

- Mainfreight

- DHL Supply Chain

- Kuehne + Nagel

- DB Schenker

- Ceva Logistics

- Agility Logistics

- Frosty Cold Chain Solutions

- Cold Logic

- VersaColdLogistics Services

- Lineage Logistics

- Scanlog

- ColdXpress

- Freightways

Key Target Audience

- Food and beverage manufacturers

- Pharmaceutical and biotechnology companies

- Retail and supermarket chains

- E-commerce grocery platforms

- Healthcare and hospital networks

- Logistics infrastructure developers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Identification of demand drivers, product types, platform preferences, and end-user requirements relevant to cold chain logistics, along with regulatory and technological factors.

Step 2: Market Analysis and Construction

Compilation and evaluation of secondary data from credible sources, construction of market frameworks, segmentation, and preliminary analysis of system types, platforms, and end users.

Step 3: Hypothesis Validation and Expert Consultation

Engagement with industry experts, supply chain managers, and regulatory officials to validate assumptions, refine data, and ensure accuracy of market insights and projections.

Step 4: Research Synthesis and Final Output

Integration of validated data into final market report, including detailed segmentation, competitive analysis, market dynamics, and future outlook with cross-checked statistical and qualitative insights.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of E-commerce and Online Grocery Channels

Increasing Demand for Pharmaceutical Cold Storage

Government Initiatives Supporting Food Safety and Healthcare Logistics - Market Challenges

High Operational and Energy Costs

Skilled Workforce Shortages

Regulatory Compliance and Cross-Border Restrictions - Market Opportunities

Integration of IoT and Smart Temperature Monitoring

Development of Automated and Modular Cold Chain Facilities

Collaborations with E-commerce and Retail Networks - Trends

Adoption of Green and Energy-Efficient Cold Storage

Digitalization of Supply Chain and Real-Time Tracking

Growth of Regional and Localized Distribution Hubs - Government Regulations

- SWOT Analysis of Key Competitors

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Refrigerated Warehousing

Temperature-Controlled Transport

Cold Storage Solutions

Integrated Logistics Platforms

Specialty Handling Systems - By Platform Type (In Value%)

Land Transport Vehicles

Air Cargo Handling

Maritime Cold Chain Vessels

Automated Storage & Retrieval Systems

Cross-Docking Facilities - By Fitment Type (In Value%)

On-Premise Cold Storage

Third-Party Logistics Services

Modular Cold Rooms

Automated Fulfillment Centers

Hybrid Cold Chain Systems - By EndUser Segment (In Value%)

Food and Beverage Manufacturers

Pharmaceutical and Biotech Companies

Retail and Supermarket Chains

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Fitment Type, EndUser Segment, Procurement Channel)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

Toll Group

Linfox

Mainfreight

DHL Supply Chain

Kuehne + Nagel

DB Schenker

Ceva Logistics

Agility Logistics

Frosty Cold Chain Solutions

Cold Logic

VersaCold Logistics Services

Lineage Logistics

Scanlog

ColdXpress

Freightways

- Food Manufacturers Increasing Reliance on Temperature-Controlled Distribution

- Healthcare Providers Expanding Cold Storage Capabilities

- Retail Chains Integrating Logistics and Inventory Management

- E-commerce Platforms Investing in Dedicated Cold Chain Networks

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now