Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Australia diagnostic labs market has reached an estimated value of USD ~ billion based on a recent historical assessment compiled from sources such as IBISWorld and the Australian Institute of Health and Welfare. Demand is driven by expanding pathology testing volumes, increased diagnostic screening, and rising incidence of chronic diseases requiring laboratory monitoring. Growth is also supported by government-funded healthcare programs, strong adoption of automated laboratory technologies, and increasing diagnostic referrals from hospitals, specialist clinics, and primary healthcare providers nationwide.

Major demand concentration is observed across metropolitan healthcare hubs including Sydney, Melbourne, Brisbane, and Perth due to the presence of advanced hospital infrastructure and centralized pathology networks. These cities host large diagnostic laboratories integrated with hospital systems and national pathology chains. Strong public healthcare spending, established referral networks, and access to high-end laboratory automation technologies reinforce their leadership. Regional diagnostic demand is also expanding as telehealth expansion and sample logistics networks improve access to laboratory services across remote communities.

Market Segmentation

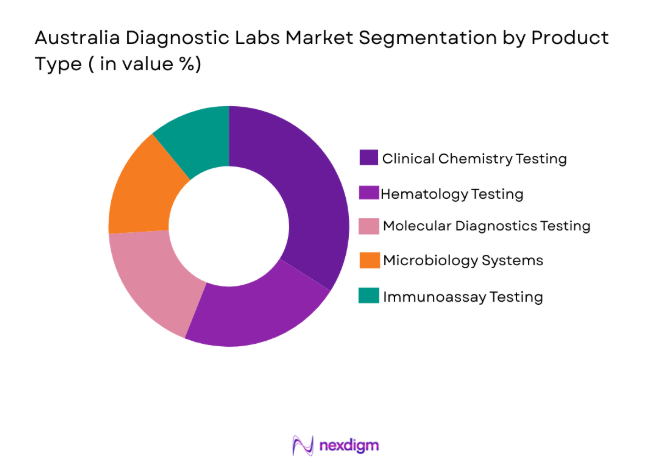

By Product Type

Australia Diagnostic Labs market is segmented by product type into clinical chemistry testing, hematology testing, molecular diagnostics testing, microbiology testing, and immunology testing. Recently, clinical chemistry testing has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, and consumer preference. Routine biochemical testing forms the backbone of diagnostic screening in hospitals and outpatient settings. The widespread requirement for metabolic panels, kidney function tests, and liver function diagnostics sustains high test volumes. Additionally, automated analyzers installed across centralized pathology laboratories enable high throughput processing. Integration with electronic medical records further improves clinical adoption and test utilization across the healthcare ecosystem.

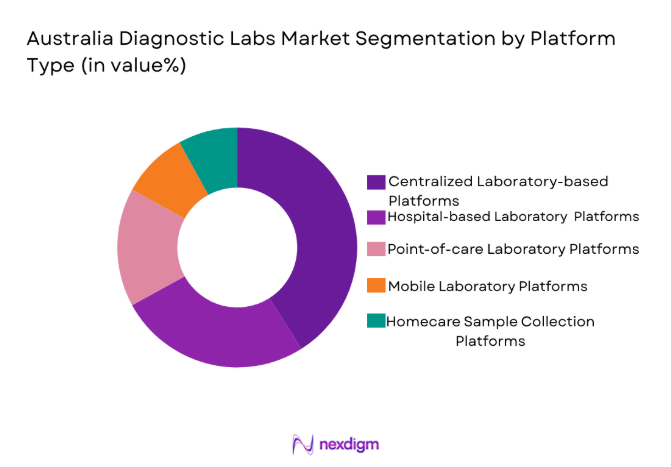

By Platform Type

Australia Diagnostic Labs market is segmented by platform type into centralized laboratory testing platforms, hospital-based laboratory platforms, point-of-care diagnostic platforms, mobile laboratory platforms, and home sample collection platforms. Recently, centralized laboratory testing platforms have a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, and consumer preference. Large pathology providers operate high-capacity automated laboratories capable of processing millions of samples annually. These facilities benefit from economies of scale, integrated logistics networks, and advanced automation systems. Their ability to deliver standardized results and maintain regulatory compliance strengthens their role as the primary testing backbone for healthcare providers nationwide.

Competitive Landscape

The Australia diagnostic labs market is moderately consolidated, with several national pathology providers operating large centralized laboratory networks alongside hospital-based laboratories. Leading companies maintain strong market influence through automated testing infrastructure, nationwide specimen collection networks, and integrated digital reporting platforms. Strategic acquisitions and partnerships between pathology groups and hospitals continue to shape competitive dynamics. Major players also focus on advanced molecular diagnostics, genomic testing services, and laboratory automation to strengthen operational efficiency and expand specialized diagnostic offerings across Australia’s healthcare ecosystem.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Laboratory Network Size |

| Sonic Healthcare | 1987 | Sydney, Australia | ~ | ~ | ~ | ~ | ~ |

| Healius Limited | 1990 | Sydney, Australia | ~ | ~ | ~ | ~ | ~ |

| Australian Clinical Labs | 2002 | Melbourne, Australia | ~ | ~ | ~ | ~ | ~ |

| Laverty Pathology | 1982 | Sydney, Australia | ~ | ~ | ~ | ~ | ~ |

| Douglass Hanly Moir Pathology | 1996 | Sydney, Australia | ~ | ~ | ~ | ~ | ~ |

Australia Diagnostic Labs Market Analysis

Growth Drivers

Expansion of Chronic Disease Diagnostic Testing

The increasing burden of chronic diseases across Australia significantly drives the diagnostic laboratories market. Conditions such as diabetes, cardiovascular disorders, kidney disease, and cancer require continuous monitoring through laboratory testing. Diagnostic labs play a crucial role in disease detection, treatment monitoring, and clinical decision support. Growing demand for early disease detection has expanded routine blood testing and molecular diagnostics across hospitals and outpatient clinics. The national healthcare system promotes preventive screening programs that increase testing volumes. Healthcare providers rely heavily on pathology results to guide treatment decisions and monitor patient progress. Rising awareness of preventive healthcare further increases demand for regular health screening services. Diagnostic laboratories therefore remain central to disease management across both public and private healthcare systems.

Adoption of Laboratory Automation and Advanced Diagnostic Technologies

Technological advancements in diagnostic laboratory automation are transforming operational efficiency and test accuracy across Australia. Modern laboratories increasingly deploy robotic sample processing systems, automated analyzers, and integrated laboratory information systems. These technologies reduce manual intervention while enabling laboratories to process thousands of samples daily with improved accuracy. Automation also lowers operational errors and enhances turnaround times for diagnostic reports. Molecular diagnostics and genomic testing technologies are expanding testing capabilities beyond traditional pathology methods. Hospitals and pathology providers invest heavily in high throughput testing platforms to support increasing patient demand. Digital integration with electronic health records further enhances laboratory reporting efficiency. As laboratories continue modernizing infrastructure, automation and advanced diagnostics significantly strengthen market growth.

Market Challenges

High Operational Costs and Laboratory Infrastructure Investment

Diagnostic laboratories require substantial financial investment to maintain advanced testing infrastructure and operational capabilities. Modern pathology laboratories depend on expensive automated analyzers, high precision instruments, and specialized testing equipment. Maintaining these systems involves continuous calibration, software upgrades, and regulatory compliance costs. Laboratories must also employ highly skilled medical technologists and pathologists to ensure accurate diagnostic interpretation. Increasing reagent costs and laboratory consumables further raise operational expenses. Smaller laboratories often struggle to maintain profitability while competing with large pathology networks. These cost pressures drive consolidation across the diagnostic laboratory industry. Sustaining operational efficiency while maintaining testing accuracy therefore remains a major challenge for laboratory operators.

Regulatory Compliance and Quality Accreditation Requirements

Diagnostic laboratories operate within a strict regulatory framework designed to maintain patient safety and diagnostic accuracy. Accreditation bodies enforce rigorous quality standards covering testing protocols, equipment calibration, and reporting practices. Laboratories must regularly undergo compliance audits to maintain certification and operational approval. Implementing standardized quality management systems increases administrative and operational complexity. Regulatory frameworks also require continuous staff training and documentation for clinical processes. Any deviation from established diagnostic protocols may lead to penalties or operational restrictions. Smaller laboratories often face difficulty maintaining compliance while controlling operational costs. Adhering to regulatory requirements while maintaining testing efficiency therefore presents an ongoing challenge for diagnostic service providers.

Opportunities

Expansion of Molecular Diagnostics and Genomic Testing Services

Molecular diagnostics and genomic testing represent a major growth opportunity for diagnostic laboratories in Australia. Advances in genetic sequencing technologies have enabled laboratories to offer personalized medicine diagnostics for oncology, rare diseases, and hereditary conditions. Hospitals increasingly rely on genomic testing to support targeted therapies and precision medicine treatment strategies. These advanced diagnostic services command higher clinical value compared with routine laboratory tests. Government healthcare initiatives also encourage genomic research and precision medicine programs. As healthcare providers expand personalized treatment approaches, demand for specialized molecular diagnostics continues increasing. Diagnostic laboratories that invest in genomic technologies gain strong competitive advantage. The rapid evolution of genetic testing capabilities therefore creates significant long term market opportunities.

Growth of Home Sample Collection and Digital Diagnostic Services

The healthcare system is increasingly integrating digital health technologies and remote diagnostic services. Home sample collection services allow patients to submit diagnostic specimens without visiting laboratories or hospitals. Logistics networks and digital reporting platforms enable laboratories to deliver results directly to physicians and patients. Telehealth expansion further supports remote diagnostic consultation and follow up care. Healthcare providers view these services as a convenient method to increase testing compliance and accessibility. Remote diagnostics particularly benefit patients in rural and geographically isolated communities. Diagnostic laboratories investing in digital platforms and sample logistics networks can expand service coverage. These innovations significantly broaden the future potential of the diagnostic laboratory market.

Future Outlook

Australia diagnostic labs market is expected to experience stable expansion driven by increasing diagnostic demand, healthcare modernization, and technological innovation. Automation, genomic diagnostics, and digital laboratory platforms will reshape diagnostic service delivery across hospitals and pathology networks. Government healthcare investment and preventive screening programs will further strengthen laboratory testing volumes. Expansion of molecular diagnostics and personalized medicine will introduce new specialized testing services. Over the coming years, integration of artificial intelligence and digital reporting systems will significantly enhance diagnostic efficiency and clinical decision support.

Major Players

- Sonic Healthcare

- Healius Limited

- Australian Clinical Labs

- Laverty Pathology

- Douglass Hanly Moir Pathology

- Western Diagnostic Pathology

- Clinipath Pathology

- Melbourne Pathology

- QML Pathology

- Sullivan Nicolaides Pathology

- TML Pathology

- Abbott Diagnostics Australia

- Roche Diagnostics Australia

- Siemens Healthineers Australia

- Thermo Fisher Scientific Australia

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Hospitals and healthcare systems

- Diagnostic laboratory networks

- Medical device manufacturers

- Healthcare technology companies

- Health insurance providers

Research Methodology

Step 1: Identification of Key Variables

The research process begins with identifying key market variables including diagnostic testing demand, laboratory infrastructure, healthcare spending, and pathology service utilization across Australia. These variables help establish the foundation for market measurement and segmentation.

Step 2: Market Analysis and Construction

Primary and secondary research sources including healthcare databases, pathology associations, and government publications are analyzed to construct the market structure. Data triangulation ensures consistency in estimating diagnostic testing demand and laboratory service revenue.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including laboratory managers, pathologists, and healthcare administrators are consulted to validate research assumptions. Expert feedback ensures realistic evaluation of industry dynamics and operational trends within diagnostic laboratories.

Step 4: Research Synthesis and Final Output

All data inputs are synthesized into a structured market model outlining demand patterns, competitive positioning, and technological developments. The final report integrates qualitative insights with quantitative analysis to deliver comprehensive market intelligence.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increase in Chronic Disease Prevalence

Technological Advancements in Diagnostic Methods

Government Initiatives to Enhance Healthcare Infrastructure - Market Challenges

Regulatory Hurdles and Compliance Issues

High Operational Costs of Diagnostic Labs

Limited Access in Rural and Remote Areas - Market Opportunities

Expansion of Point-of-care Testing

Integration of AI and Automation in Diagnostics

Increased Focus on Preventive Healthcare - Trends

Rise in At-home Testing Services

Shift Towards Personalized Medicine - Government Regulations

Data Protection and Privacy Regulations

Regulations on Medical Device Approvals

Health Insurance Reimbursement Policies - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Clinical Chemistry

Hematology

Immunology

Molecular Diagnostics

Microbiology - By Platform Type (In Value%)

Laboratory-based Platforms

Point-of-care Testing Platforms

Mobile Diagnostic Platforms

Home-based Testing Platforms

Wearable Diagnostic Devices - By Fitment Type (In Value%)

Standalone Solutions

Integrated Solutions

Modular Solutions

Portable Solutions - By End User Segment (In Value%)

Hospitals

Clinics

Diagnostic Centers

Home Healthcare Providers

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Technology Integration, Pricing Strategy)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Roche Diagnostics

Abbott Laboratories

Thermo Fisher Scientific

Siemens Healthineers

Beckman Coulter

BD Diagnostics

Cepheid

Bio-Rad Laboratories

Ortho Clinical Diagnostics

Medtronic

Fujifilm Holdings

BioMérieux

Danaher Corporation

Mindray

Stryker Corporation

- Increasing Demand for Home Healthcare Solutions

- Expansion of Diagnostic Services in Rural Areas

- Rising Preference for Preventive Healthcare Measures

- Increased Adoption of AI-based Diagnostic Tools

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now