Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Australia E-Bomb market has witnessed significant growth, driven by increased defense budgets and the adoption of advanced electronic warfare technologies. The market size is expected to reach USD ~ billion, with a steady rise attributed to military modernization programs and the growing demand for electromagnetic weapons. Australia’s focus on strengthening its defense infrastructure, including strategic partnerships with defense contractors, has propelled the expansion of the market in recent years. As of the latest data, the market is poised to continue growing, with robust investments from both government and private sectors.

Australia remains a dominant player in the E-Bomb market due to its advanced defense sector and strong technological expertise. The country’s geographical location, political stability, and strategic defense policies make it a key player in the Asia-Pacific region. Australia’s defense sector benefits from collaboration with global defense organizations and multinational technology firms. The nation’s proactive stance on defense research and development, along with substantial investments in national security, strengthens its position in the global market.

Market Segmentation

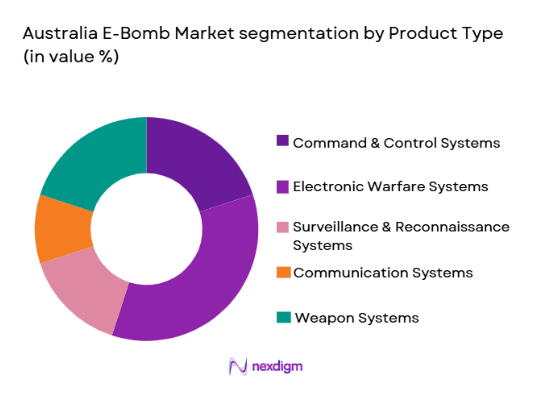

By Product Type

The Australia E-Bomb market is segmented by product type into command & control systems, electronic warfare systems, surveillance & reconnaissance systems, communication systems, and weapon systems. Recently, the electronic warfare systems sub-segment has a dominant market share due to its critical role in modern defense strategies. The demand for electronic warfare systems is growing rapidly, driven by the rising need for countermeasures against cyber threats and electromagnetic attacks. With increasing geopolitical tensions and military modernization, defense agencies are prioritizing these systems, which also align with technological advancements such as AI and machine learning for real-time response. This has led to a significant share in the market, supported by continuous investments in R&D to enhance system capabilities.

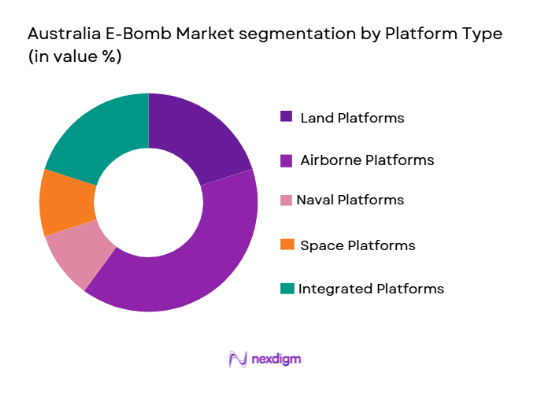

By Platform Type

The market is segmented by platform type into land platforms, airborne platforms, naval platforms, space platforms, and integrated platforms. The airborne platforms sub-segment is currently dominating the market share due to its vast use in modern military operations. Airborne platforms, such as unmanned aerial vehicles (UAVs) and advanced fighter jets, offer superior mobility, range, and precision. These platforms are crucial for intelligence gathering, surveillance, and electronic warfare, which are critical components of modern defense strategies. Their effectiveness in multi-domain operations and the continued advancements in UAV technology contribute significantly to the dominance of airborne platforms in the E-Bomb market.

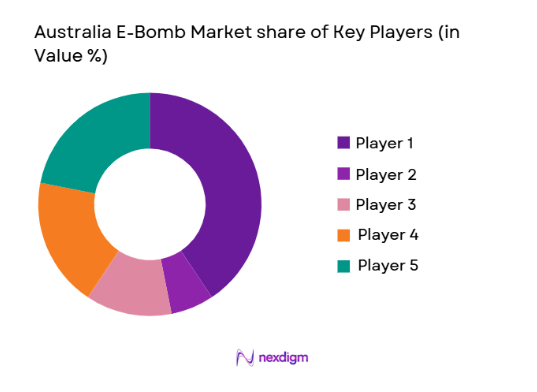

Competitive Landscape

The competitive landscape of the Australia E-Bomb market is marked by the presence of key players in defense technologies, electronic warfare, and electromagnetic weaponry. The market has witnessed significant consolidation, with large multinational defense firms joining forces with smaller specialized companies to enhance their market presence and technological expertise. The influence of these major players continues to shape the development of the E-Bomb market, as they invest heavily in research, innovation, and production capabilities.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Additional Parameter |

| Lockheed Martin | 1912 | USA | ~ | ~ | ~ | ~ | ~ |

| Thales Group | 1893 | France | ~ | ~ | ~ | ~ | ~ |

| BAE Systems | 1999 | UK | ~ | ~ | ~ | ~ | ~ |

| Northrop Grumman | 1939 | USA | ~ | ~ | ~ | ~ | ~ |

| Raytheon Technologies | 1922 | USA | ~ | ~ | ~ | ~ | ~ |

Australia E-Bomb Market Analysis

Growth Drivers

Increased Government Investment in Defense

Increased government spending on defense and national security is one of the primary growth drivers for the Australia E-Bomb market. With rising geopolitical tensions and the need for advanced defense systems, Australia has prioritized strengthening its military capabilities. The government has allocated substantial funds for the development of cutting-edge technologies, including electronic warfare systems. These systems are integral to countering emerging threats, such as cyber-attacks and electromagnetic warfare, which have become central to modern military strategies. Furthermore, Australia’s close defense ties with global powers have led to an inflow of investments in technological advancements. These investments have facilitated the development of next-generation E-Bomb systems, making the sector more robust and responsive to emerging security challenges. With a favorable regulatory environment and increased public and private sector support, the market for electronic warfare systems, including E-Bombs, is expected to continue its growth trajectory. This trend is expected to support the rise in market share for Australia’s defense sector and solidify its position as a key player in the Asia-Pacific region.

Technological Advancements in Electronic Warfare

Technological advancements in electronic warfare have been a significant driver of growth in the Australia E-Bomb market. The development of sophisticated systems that can jam, disrupt, or deceive adversary communications and radar systems has revolutionized modern defense tactics. With the advent of AI, machine learning, and enhanced sensor technologies, the effectiveness of E-Bomb systems has greatly improved. These technological innovations enable the deployment of more precise and efficient electronic warfare solutions, which are crucial for military operations. Furthermore, the ability to integrate advanced technologies such as the Internet of Things (IoT) and 5G networks into military equipment has propelled the demand for these systems. Australia’s defense sector has capitalized on these advancements, focusing on increasing the operational efficiency of its electronic warfare capabilities. By developing E-Bombs with advanced threat detection and mitigation capabilities, Australia is positioning itself as a leader in electronic warfare, thereby driving market growth.

Market Challenges

High Capital Investment Requirements

The high capital investment required for the development, production, and maintenance of E-Bomb systems remains a significant challenge for the Australia E-Bomb market. Developing sophisticated electronic warfare systems requires substantial financial resources for research, development, and testing. Moreover, the complexity of these systems means that the cost of procurement, installation, and operational management remains high, which could deter some smaller defense contractors or government entities from investing in them. This capital intensity often results in long project timelines and high barriers to entry for new market players. While major defense contractors benefit from economies of scale and established relationships with defense ministries, smaller companies face considerable financial strain. As a result, the cost factor could limit the growth potential of the market, especially in the face of competing priorities for limited government defense budgets.

Technological Integration and Interoperability Issues

Technological integration and interoperability between various defense systems pose a major challenge to the E-Bomb market in Australia. Electronic warfare systems, including E-Bombs, require seamless integration with existing military infrastructure to ensure maximum effectiveness. However, the complexity and diversity of legacy systems in use by the Australian Defense Force often complicate this integration. Interoperability issues arise when new technologies fail to work efficiently with older systems, leading to potential operational inefficiencies and delays in deployment. Furthermore, the rapid pace of technological advancement in the electronic warfare space means that regular upgrades and system improvements are required to maintain effectiveness. This continuous need for integration and upgrades poses a logistical challenge for the Australian defense sector, making it more difficult to maintain long-term system reliability and performance.

Opportunities

Strategic Collaborations with Global Defense Contractors

One of the major opportunities in the Australia E-Bomb market is the potential for strategic collaborations with global defense contractors. Australia’s defense sector benefits from its close relationships with leading defense manufacturers worldwide, including the USA, the UK, and France. These collaborations bring advanced technologies, specialized knowledge, and expertise to the Australian market. By partnering with global firms, Australia can gain access to the latest in defense technology and innovations in electronic warfare systems. Additionally, these partnerships can facilitate the transfer of technology, knowledge, and resources, which can accelerate the development of domestic capabilities. Australia’s active participation in international defense alliances and its growing focus on defense innovation make it an attractive partner for such collaborations, opening up new avenues for growth in the E-Bomb market.

Expansion of Autonomous Systems and Robotics in Electronic Warfare

The expansion of autonomous systems and robotics in electronic warfare presents a significant opportunity for the Australia E-Bomb market. As military forces continue to explore the potential of autonomous platforms in combat and surveillance, the integration of robotic systems in electronic warfare is becoming increasingly important. These systems can be deployed for various tasks such as jamming, intercepting communications, and disabling enemy equipment. Australia is well-positioned to capitalize on this trend, as the country already has a strong presence in the development and deployment of autonomous systems. The use of unmanned aerial vehicles (UAVs) and robotic systems in electronic warfare applications will reduce human risks and enhance operational efficiency, driving the demand for more advanced E-Bombs. This opportunity, coupled with Australia’s focus on increasing its technological expertise in autonomous systems, will significantly contribute to the growth of the E-Bomb market.

Future Outlook

The future outlook of the Australia E-Bomb market looks promising, with expected growth driven by advancements in defense technology and an increasingly volatile global security environment. The adoption of autonomous systems, along with innovations in AI and machine learning, is expected to enhance the effectiveness of electronic warfare systems. Additionally, increased government investment in defense technologies and international collaborations will support the market’s expansion. Over the next five years, the demand for advanced E-Bombs is anticipated to rise, driven by the need for robust defense strategies that address evolving threats.

Major Players

- Lockheed Martin

- Thales Group

- BAE Systems

- Northrop Grumman

- Raytheon Technologies

- L3 Technologies

- Leonardo

- Harris Corporation

- Elbit Systems

- Rheinmetall AG

- Boeing

- Saab Group

- General Dynamics

- Hewlett Packard Enterprise

- Sikorsky Aircraft

Key Target Audience

- Military Forces

- Defense Contractors

- Government and Regulatory Bodies

- Security Services

- Private Sector / Technology Firms

- Investment Firms

- Aerospace Manufacturers

- Defense R&D Agencies

Research Methodology

Step 1: Identification of Key Variables

The key variables that influence the market were identified, including technological advancements, regulatory changes, and defense spending patterns.

Step 2: Market Analysis and Construction

The market was analyzed using both primary and secondary research, focusing on trends, drivers, and challenges.

Step 3: Hypothesis Validation and Expert Consultation

The initial market model was validated by consulting industry experts, including military professionals and technology specialists.

Step 4: Research Synthesis and Final Output

The final report synthesizes the research findings, providing a comprehensive overview of the market, key drivers, challenges, and opportunities.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increased Defense Spending

Technological Advancements in Electromagnetic Technologies

Geopolitical Tensions and National Security Concerns

Growing Demand for Precision Electronic Warfare

Emerging Threats in Cybersecurity and Communications - Market Challenges

High Development and Production Costs

Regulatory Hurdles in Military Technology

Security and Privacy Concerns in Electronic Systems

Limited Technological Expertise in Emerging Markets

Complex Integration into Existing Defense Systems - Market Opportunities

Rising Demand for Autonomous Electronic Warfare Systems

Strategic Partnerships with Private Tech Firms for Innovation

Government Investment in Cybersecurity and Defense Solutions - Trends

Surge in Development of Anti-Satellite and Counter-UAV Technologies

Integration of AI and Machine Learning in Electronic Warfare

Increased Investment in Electronic Warfare Simulation Systems

Shift Toward Multi-domain Operations

Advancement in High-Power Microwave and Laser Technology - Government Regulations & Defense Policy

Export Control and Compliance Policies

Government Funding for Next-Generation Defense Technologies

Strengthened Cybersecurity Legislation - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Command & Control Systems

Electronic Warfare Systems

Surveillance & Reconnaissance Systems

Communication Systems

Weapon Systems - By Platform Type (In Value%)

Land Platforms

Airborne Platforms

Naval Platforms

Space Platforms

Integrated Platforms - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Hybrid Solutions

Modular Solutions

Integrated Solutions - By EndUser Segment (In Value%)

Military Forces

Defense Contractors

Government Agencies

Security Services

Private Sector / Technology Firms - By Procurement Channel (In Value%)

Direct Procurement

Government Tenders

Private Sector Procurement

Online Bidding Platforms

Third-party Distributors - By Material / Technology (In Value%)

Semiconductor Materials

Microwave Technology

Power Amplifiers

Microelectronics

Electromagnetic Shielding

- Market share snapshot of major players

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type, Market Value, Installed Units, Average System Price, System Complexity Tier, Technology Integration)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Lockheed Martin

Thales Group

BAE Systems

Northrop Grumman

Rheinmetall AG

Raytheon Technologies

L3 Technologies

General Dynamics

Leonardo

Saab Group

Elbit Systems

Harris Corporation

Hewlett Packard Enterprise

Boeing

Sikorsky Aircraft

- Rising Demand from Military Forces for Electronic Warfare Systems

- Government Agencies’ Role in Regulatory and Procurement Decisions

- Defense Contractors Driving Technological Innovation and Development

- Technology Firms Providing Advanced Solutions for Electronic Warfare

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now