Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Australia edge computing market is valued at approximately USD ~ billion based on a recent historical assessment, driven by 5G network rollout, IoT adoption, and demand for low-latency data processing across industries. Telecommunications operators and cloud providers are deploying distributed edge nodes to support real-time analytics, autonomous systems, and digital services. Growth of smart infrastructure connected devices, and industrial automation further accelerates investment in localized computers, storage, and networking infrastructure across metropolitan and regional environments.

Sydney and Melbourne dominate the Australia edge computing market due to concentration of telecom network hubs, hyperscale data centers, and enterprise demand for low-latency digital services. These cities host major 5G deployments, financial institutions, and technology firms requiring distributed processing capabilities. Brisbane and Perth are emerging edge infrastructure hubs linked to mining, logistics, and resource industries. Proximity to population centers, fiber backbones, and telecom exchanges reinforces regional leadership in edge computing deployment nationwide.

Market Segmentation

By Component Type

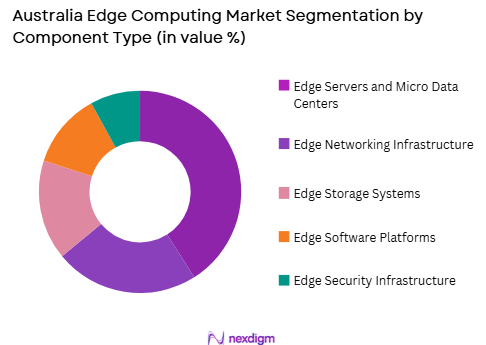

Australia Edge Computing market is segmented by product type into edge servers and micro data centers, edge networking infrastructure, edge storage systems, edge software platforms, and edge security infrastructure. Recently, edge servers and micro data centers has a dominant market share due to factors such as telecom edge deployment, enterprise low-latency computing demand, and distributed AI workloads. Telecom operators install micro data centers at base stations and exchanges to support 5G services and network functions virtualization. Enterprises deploy edge servers for industrial automation and real-time analytics. Cloud providers extend services to edge locations using localized compute nodes. Increasing demand for near-device processing sustains highest capital allocation toward edge servers and micro data center infrastructure in Australia.

By End-Use Industry

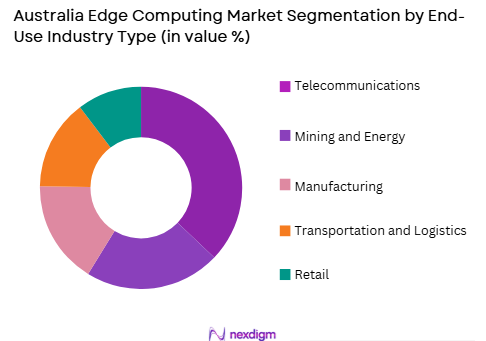

Australia Edge Computing market is segmented by end-use industry into telecommunications, manufacturing, mining and energy, transportation and logistics, and retail. Recently, telecommunications has a dominant market share due to factors such as nationwide 5G rollout, network edge virtualization, and distributed content delivery requirements. Telecom operators deploy edge infrastructure to reduce latency for mobile services and IoT applications. Integration of edge computing with 5G enables real-time analytics and automation. Telecom firms also offer edge platforms to enterprises. These factors position telecommunications as the largest consumer of edge computing infrastructure capacity in Australia.

Competitive Landscape

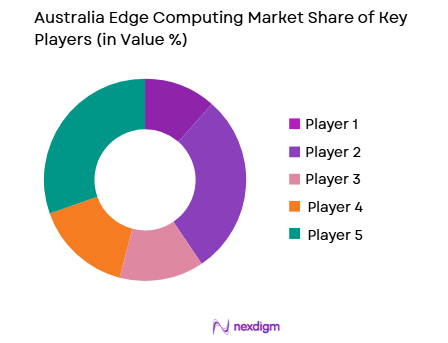

The Australia edge computing market is moderately consolidated with telecom operators, cloud providers, and data center firms leading infrastructure deployment. Telecom networks provide physical distribution for edge nodes, while cloud platforms supply software orchestration and services. Partnerships between telecom and hyperscale firms shape market structure. Equipment vendors and industrial solution providers complement deployments. Competitive positioning depends on network footprint, platform capabilities, and regional infrastructure presence.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Edge Network Footprint in Australia |

| Telstra | 1975 | Melbourne, Australia | ~ | ~ | ~ | ~ | ~ |

| Optus | 1991 | Sydney, Australia | ~ | ~ | ~ | ~ | ~ |

| Amazon Web Services | 2006 | Seattle, USA | ~ | ~ | ~ | ~ | ~ |

| Microsoft | 1975 | Redmond, USA | ~ | ~ | ~ | ~ | ~ |

| Nokia | 1865 | Espoo, Finland | ~ | ~ | ~ | ~ | ~ |

Australia Edge Computing Market Analysis

Growth Drivers

5G Network Expansion and Telecom Edge Virtualization Infrastructure

Nationwide deployment of 5G networks in Australia is driving extensive investment in distributed edge computing infrastructure embedded within telecom networks to enable ultra-low latency services and real-time data processing capabilities. Telecom operators deploy edge servers at base stations, aggregation points, and exchanges to support network functions virtualization and mobile edge computing platforms. Applications such as autonomous vehicles, smart cities, augmented reality, and IoT analytics require localized compute resources close to users. Integration of edge computing with 5G architecture reduces latency and backhaul bandwidth consumption. Telecom firms monetize edge platforms by offering enterprise services and application hosting. Content delivery and video streaming services rely on edge nodes for performance optimization. Industrial IoT deployments use telecom edge for real-time control. Expansion of 5G coverage across urban and regional areas increases number of edge sites. Continuous growth of latency-sensitive applications sustains demand for telecom edge infrastructure nationwide.

Industrial Automation, IoT, and Real-Time Analytics Adoption Across Sectors

Rapid adoption of industrial automation, connected devices, and real-time analytics across mining, manufacturing, logistics, and energy sectors in Australia is accelerating deployment of enterprise edge computing infrastructure near operational environments. Mining operations deploy edge servers at remote sites to process sensor data and autonomous equipment control locally. Manufacturing plants use edge analytics for predictive maintenance and quality monitoring. Logistics hubs apply edge computing for fleet tracking and warehouse automation. Energy utilities deploy edge nodes for grid monitoring and smart infrastructure management. Local processing reduces latency and connectivity dependence. Edge AI applications enable on-site decision making and safety systems. Enterprises integrate edge with cloud platforms for hybrid analytics. Growth of IoT device deployments increases data volume requiring local processing. Operational efficiency and reliability requirements sustain long-term enterprise edge infrastructure demand across industries.

Market Challenges

Geographic Dispersion and Connectivity Limitations Across Remote Regions

Australia’s vast geography and dispersed industrial operations create challenges for deployment and connectivity of edge computing infrastructure, particularly in remote mining and energy regions lacking high-capacity fiber networks and reliable power supply. Edge sites in remote areas require satellite or microwave backhaul, increasing latency and cost. Limited infrastructure availability complicates installation and maintenance of edge nodes. Harsh environmental conditions affect equipment reliability. Workforce availability for remote operations is constrained. Power supply instability affects edge system uptime. Integration with centralized cloud platforms becomes complex. Capital expenditure for remote connectivity infrastructure is high. These factors slow deployment and scalability of edge computing across non-urban Australia.

Interoperability, Management Complexity, and Security Risks in Distributed Edge Environments

Distributed edge computing infrastructure across numerous sites introduces operational complexity in management, orchestration, and cybersecurity for enterprises and telecom operators in Australia. Heterogeneous hardware and software platforms create interoperability challenges. Managing thousands of edge nodes requires advanced orchestration tools. Security risks increase due to expanded attack surface across distributed locations. Data protection and compliance must be maintained at each edge site. Software updates and maintenance across remote nodes are complex. Integration with cloud and enterprise systems requires standardized interfaces. Monitoring performance and reliability across distributed infrastructure is challenging. Lack of unified management frameworks increases operational cost. These issues complicate large-scale edge infrastructure deployment.

Opportunities

Edge AI and Autonomous Systems Deployment in Mining and Resource Industries

Australia’s globally significant mining and resource sector offers substantial opportunity for deployment of edge AI infrastructure enabling autonomous vehicles, robotics, and real-time operational analytics at remote industrial sites. Edge computing supports local processing of sensor and machine data for safety and productivity. Autonomous haulage and drilling systems rely on low-latency edge AI control. Environmental monitoring and predictive maintenance require on-site analytics. Integration of edge AI with industrial IoT enhances efficiency. Resource firms invest heavily in automation infrastructure. Remote operations favor localized computing to reduce connectivity dependence. Collaboration with technology vendors accelerates deployment. Expansion of autonomous mining ecosystems increases demand for ruggedized edge systems. This opportunity positions edge computing as core digital infrastructure in resource industries.

Telecom-Cloud Edge Platform Integration and Enterprise Edge Services

Integration of telecom edge infrastructure with hyperscale cloud platforms in Australia creates opportunity to deliver enterprise edge computing services combining low-latency network access with scalable cloud capabilities. Telecom operators partner with cloud providers to deploy multi-access edge computing platforms. Enterprises access localized compute integrated with cloud services. Edge-cloud integration supports real-time analytics, AI inference, and content delivery. Telecom firms monetize infrastructure through platform services. Cloud providers extend application ecosystems to edge locations. Industry vertical solutions emerge across manufacturing, healthcare, and logistics. Unified orchestration enables hybrid deployment models. Expansion of enterprise edge applications increases service demand. This opportunity accelerates commercialization of edge infrastructure nationwide.

Future Outlook

Australia edge computing market is expected to expand steadily as 5G coverage, industrial automation, and IoT adoption accelerate demand for distributed low-latency computing infrastructure. Telecom-cloud integration will enable scalable edge platforms. Growth of autonomous systems and real-time analytics will drive enterprise deployment. Regional digitalization and smart infrastructure programs will further expand edge computing capacity across urban and remote environments.

Major Players

- Telstra

- Optus

- Amazon Web Services

- Microsoft

- Nokia

- Ericsson

- Cisco Systems

- HPE

- Dell Technologies

- IBM

- Huawei

- Juniper Networks

- Schneider Electric

- Vertiv

- Edge Centres

Key Target Audience

- Telecommunications operators

- Mining and energy companies

- Manufacturing enterprises

- Logistics and transportation firms

- Data center operators

- Investments and venture capitalist firms

- Government and regulatory bodies

- Industrial automation providers

Research Methodology

Step 1: Identification of Key Variables

Key variables include edge node deployments, 5G coverage expansion, industrial IoT adoption, telecom infrastructure investment, and enterprise edge spending. Variables are mapped across components and industries to define market structure.

Step 2: Market Analysis and Construction

Supply-side analysis evaluates telecom and enterprise edge infrastructure deployment, while demand-side analysis examines industry automation and latency-sensitive application adoption. Data triangulation constructs market size and segmentation estimates.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts from telecom operators, industrial firms, and technology vendors validate assumptions on edge deployment growth, technology integration, and operational constraints. Feedback refines segmentation shares and competitive positioning.

Step 4: Research Synthesis and Final Output

Validated datasets and qualitative insights are synthesized into market forecasts, competitive analysis, and strategic outlook. Consistency checks ensure alignment across market size, segmentation, and trend narratives.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

5G and low-latency network expansion across Australia

Edge AI adoption in mining, energy, and transport sectors

Demand for localized compute in remote operations - Market Challenges

High deployment cost across vast geographic regions

Power and connectivity limitations in remote sites

Interoperability across telecom and enterprise systems - Market Opportunities

Edge AI for autonomous mining and energy operations

Low-latency edge for immersive media and gaming

Smart infrastructure and transport edge platforms - Trends

Convergence of telecom and enterprise edge architectures

Adoption of modular and containerized edge data centers

Integration of AI accelerators into edge nodes - Government regulations

Critical infrastructure and data sovereignty policies

National digital and connectivity programs

Smart infrastructure and transport initiatives - SWOT analysis

- Porters five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Edge Data Centers

Micro Edge Nodes

On-Premise Edge Servers

Edge AI Gateways

Ruggedized Edge Platforms - By Platform Type (In Value%)

Telecom Network Edge

Enterprise Campus Edge

Industrial Edge Systems

Autonomous Systems Edge

Content Delivery Edge - By Fitment Type (In Value%)

New Edge Deployment

Retrofit Edge Enablement

Integrated OEM Edge Systems

Modular Edge Units

Cloud-Managed Edge Integration - By EndUser Segment (In Value%)

Telecommunications Operators

Mining and Energy Companies

Transport and Logistics Operators

Media and Content Platforms

Government and Smart Infrastructure Agencies - By Procurement Channel (In Value%)

Direct OEM Procurement

Telecom Operator Contracts

System Integrator Deployment

Cloud Service Bundling

Public Sector Tenders

- Market Share Analysis

- Cross Comparison Parameters (Latency Performance, Edge Compute Density, Power Efficiency per Node, Network Proximity and Coverage, Scalability Architecture, Edge AI Acceleration Capability, Orchestration and Management Platform, Ruggedization and Environmental Tolerance, Interconnect Bandwidth, Deployment Flexibility, Remote Operations Support, Energy Autonomy Capability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Telstra

Optus

TPG Telecom

NextDC

Equinix Australia

AirTrunk

Schneider Electric Australia

Vertiv Australia

Dell Technologies Australia

Hewlett Packard Enterprise Australia

Cisco Systems Australia

Nokia Australia

Ericsson Australia

Fujitsu Australia

DXC Technology Australia

- Telecom operators deploying edge for 5G services

- Mining and energy firms using edge for automation

- Transport and logistics deploying real-time edge

- Government implementing smart infrastructure edge

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now