Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Australia Farm Equipment Spare Parts & Aftermarket market was valued at USD ~ billion, supported by sustained agricultural output and a large installed base of tractors, harvesters, and seeding equipment across broadacre and mixed farming regions. The market is driven by replacement demand for wear components, hydraulic assemblies, and engine parts, alongside rising mechanization levels and increased reliance on precision farming technologies requiring regular maintenance and component upgrades.

Dominant activity is concentrated in states such as New South Wales, Victoria, and Western Australia, where extensive grain and livestock farming operations generate continuous demand for spare parts and servicing. Regional hubs including Melbourne, Sydney, and Perth host major dealer networks and distribution centers due to strong logistics connectivity and proximity to farming clusters. These locations benefit from established agricultural supply chains, advanced service infrastructure, and higher machinery density compared with remote territories.

Market Segmentation

By Product Type

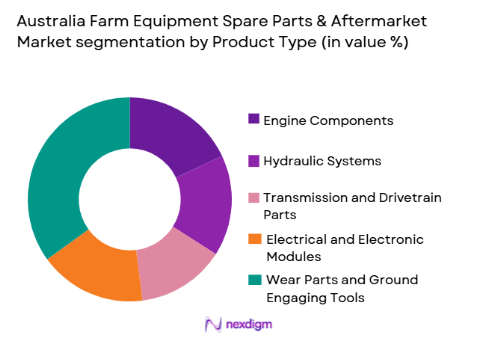

Australia Farm Equipment Spare Parts & Aftermarket market is segmented by product type into engine components, hydraulic systems, transmission and drivetrain parts, electrical and electronic modules, and wear parts and ground engaging tools. Recently, wear parts and ground engaging tools has a dominant market share due to high replacement frequency driven by soil contact, heavy operational loads, and seasonal harvesting cycles. Australian broadacre farming exposes ploughs, blades, discs, and tines to abrasive conditions, accelerating wear rates compared with enclosed mechanical systems. Farmers prioritize immediate availability of these components to avoid downtime during planting and harvesting windows. Dealer inventories are therefore heavily stocked with consumable parts, increasing sales turnover relative to high value but less frequently replaced assemblies such as engines or transmissions.

By End-User Segment

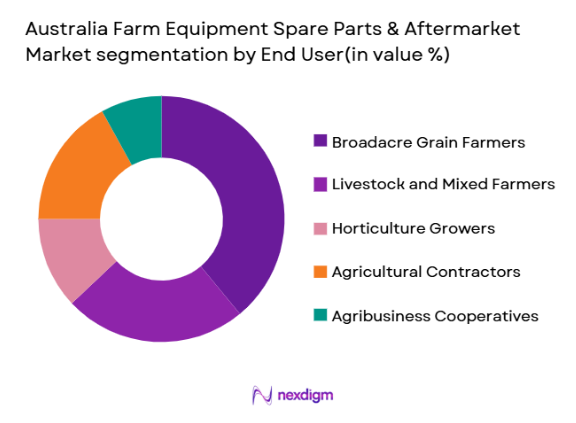

Australia Farm Equipment Spare Parts & Aftermarket market is segmented by end-user segment into broadacre grain farmers, livestock and mixed farmers, horticulture growers, agricultural contractors, and agribusiness cooperatives. Recently, broadacre grain farmers has a dominant market share due to the extensive land under cultivation and high machinery utilization intensity across wheat, barley, and canola production belts. Large scale operations operate multiple tractors and harvesters, resulting in continuous demand for preventive maintenance and component replacement. Seasonal time sensitivity compels these farmers to invest in high quality genuine or compatible spare parts to ensure operational continuity. The scale of mechanization in grain farming exceeds that of smaller horticulture units, thereby contributing to higher aggregate aftermarket expenditure.

Competitive Landscape

The Australia Farm Equipment Spare Parts & Aftermarket market demonstrates moderate consolidation, with established dealership groups and multinational machinery manufacturers exerting significant influence over distribution and pricing structures. Major players benefit from integrated supply chains, localized warehousing, and branded genuine parts portfolios. Independent retailers and aftermarket specialists compete on price and availability, particularly in regional areas. Strategic partnerships with global OEMs, remanufacturing capabilities, and digital inventory platforms shape competitive positioning.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Distribution Network Strength |

| CNH Industrial Australia | 1996 | Melbourne, Australia | ~ | ~ | ~ | ~ | ~ |

| Kubota Australia | 1979 | Sydney, Australia | ~ | ~ | ~ | ~ | ~ |

| RDO Equipment Australia | 1968 | Toowoomba, Australia | ~ | ~ | ~ | ~ | ~ |

| Clark Equipment Australia | 1948 | Hornsby, Australia | ~ | ~ | ~ | ~ | ~ |

| AFGRI Equipment Australia | 2004 | Perth, Australia | ~ | ~ | ~ | ~ | ~ |

Australia Farm Equipment Spare Parts & Aftermarket Market Analysis

Growth Drivers

Expansion of Mechanized Broadacre Farming Operations:

The increasing scale of grain and oilseed cultivation across Australian states has intensified machinery utilization rates, directly driving demand for replacement parts and maintenance components. Large farms operate fleets of tractors, combines, and seeding equipment that accumulate high annual operating hours, accelerating wear and component fatigue. Continuous cropping cycles reduce idle periods, necessitating preventive servicing and scheduled part replacement to avoid costly downtime. Farmers are investing in higher capacity machinery, which incorporates complex hydraulic and electronic systems requiring specialized aftermarket support. Seasonal pressures during planting and harvesting create urgency in spare part procurement, strengthening dealer revenues. Expansion of export oriented agricultural production further supports equipment usage intensity. Regional consolidation of farms into larger operational units has increased average machinery size and complexity. These factors collectively sustain consistent aftermarket demand irrespective of new equipment sales cycles.

Rising Adoption of Precision Agriculture and Smart Components:

The integration of GPS guidance, telematics, and sensor based systems into farm machinery has created additional aftermarket demand for electronic modules and calibration services. Farmers increasingly rely on real time data analytics to optimize seeding rates, fertilizer application, and harvesting efficiency. Such technologies require periodic upgrades, firmware updates, and hardware replacements, expanding revenue streams beyond traditional mechanical parts. As machinery becomes digitally integrated, component compatibility and technical servicing gain strategic importance. Dealers are offering bundled maintenance contracts covering both mechanical and electronic systems. Data driven farm management encourages predictive maintenance, increasing planned part replacement volumes. Precision agriculture adoption also stimulates demand for higher quality branded components to ensure system reliability. The technological shift therefore broadens the scope of the aftermarket beyond consumables toward advanced system integration support.

Market Challenges

Volatility in Agricultural Commodity Prices Affecting Farmer Spending:

The financial capacity of farmers to invest in spare parts is closely tied to commodity price cycles for wheat, barley, and livestock products. Sudden declines in global prices reduce farm profitability and constrain discretionary expenditure on non urgent component replacements. During periods of reduced income, farmers may defer maintenance or opt for lower cost compatible parts, affecting premium segment sales. Climatic variability and drought conditions further amplify income instability, impacting purchasing decisions. Regional disparities in rainfall patterns influence equipment usage intensity and replacement cycles. Financing constraints may limit large scale overhauls of engines or transmissions. Price sensitivity increases competition among independent retailers offering discounted alternatives. These factors introduce revenue fluctuations and reduce predictability in aftermarket demand patterns.

Supply Chain Dependence on Imported Components:

A significant proportion of advanced machinery parts used in Australia originates from global manufacturing hubs, creating exposure to shipping delays and currency fluctuations. Extended lead times can disrupt seasonal maintenance schedules and reduce equipment availability during critical farming periods. Exchange rate movements impact procurement costs for distributors, influencing retail pricing structures. Port congestion and international logistics disruptions have historically constrained spare part inventories. Limited domestic manufacturing capacity for specialized electronic modules restricts local substitution options. Dealers must maintain higher safety stock levels to mitigate supply risk, increasing working capital requirements. Smaller independent retailers face challenges in negotiating favorable import terms. Dependence on foreign supply chains therefore represents a structural vulnerability within the market ecosystem.

Opportunities

Development of Local Remanufacturing and Refurbishment Facilities:

Establishing domestic remanufacturing centers for engines, transmissions, and hydraulic assemblies presents a substantial growth opportunity for the aftermarket. Remanufactured components offer cost effective alternatives while maintaining acceptable performance standards for farmers. Local facilities reduce reliance on imported replacements and shorten turnaround times for major overhauls. Environmental sustainability considerations favor refurbishment over complete component replacement. Government initiatives supporting circular economy practices further strengthen the business case for remanufacturing investments. Dealers can enhance profitability through value added refurbishment services. Skilled technical workforce development would support quality assurance and reliability benchmarks. The strategy can also improve supply chain resilience across regional agricultural hubs.

Digitalization of Spare Parts Distribution Platforms:

adoption of online inventory management and ordering systems can significantly improve market efficiency and transparency. Digital catalogs enable farmers to identify compatible components quickly using machine model and serial number data. Real time stock visibility across dealer networks reduces procurement delays and enhances customer satisfaction. Integration of telematics data with ordering platforms allows predictive part recommendations. E commerce channels expand reach into remote rural areas where physical outlets are limited. Data analytics can support demand forecasting and optimized warehousing strategies. Digital payment solutions simplify transaction processes for agricultural contractors. This technological transformation is expected to strengthen competitive differentiation and operational scalability in the aftermarket landscape.

Future Outlook

Over the next five years, the Australia Farm Equipment Spare Parts & Aftermarket market is expected to experience stable expansion supported by sustained agricultural exports and continued mechanization. Increasing penetration of smart farming technologies will elevate demand for advanced electronic modules and predictive maintenance services. Regulatory emphasis on sustainability may encourage remanufacturing and environmentally compliant component development. Improved digital distribution networks and localized inventory strategies are likely to enhance supply reliability across remote farming regions.

Major Players

- CNH Industrial Australia

- Kubota Australia

- RDO Equipment Australia

- Clark Equipment Australia

- AFGRI Equipment Australia

- Emmetts Group

- Wideland Group

- Brown and Hurley

- Bare Co Australia

- Agriparts Australia

- Intersales

- Agrison

- Gason

- MacDon Australia

- John Deere Australia

Key Target Audience

- Agricultural machinery manufacturers

- Farm equipment dealers and distributors

- Broadacre farming enterprises

- Livestock farming companies

- Agribusiness cooperatives

- Investments and venture capitalist firms

- Government and regulatory bodies

- Logistics and warehousing operators

Research Methodology

Step 1: Identification of Key Variables

Key variables such as installed machinery base, replacement cycles, dealer density, and agricultural output were identified through secondary sources and industry databases. These variables formed the foundation for market estimation models.

Step 2: Market Analysis and Construction

Quantitative and qualitative data were consolidated to construct a structured market framework covering product categories, end users, and regional demand clusters. Cross validation was performed using trade statistics and company disclosures.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings were validated through consultations with industry experts, dealership managers, and supply chain professionals. Feedback was incorporated to refine demand assumptions and segmentation accuracy.

Step 4: Research Synthesis and Final Output

All validated insights were synthesized into a comprehensive analytical framework. Data triangulation ensured consistency across segments, leading to the final structured report output.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Aging agricultural machinery fleet requiring regular part replacement

Expansion of large scale farming operations across Australia

Rising mechanization in grain and livestock farming

Increased adoption of precision agriculture technologies

Growing focus on equipment uptime and operational efficiency - Market Challenges

Volatility in agricultural commodity prices impacting farmer spending

Supply chain disruptions affecting part availability

Counterfeit and low quality aftermarket components

High logistics costs across remote farming regions

Dependence on imported machinery brands and components - Market Opportunities

Development of localized remanufacturing facilities

Digital platforms for spare parts sourcing and inventory management

Integration of IoT enabled smart replacement components - Trends

Growth of online spare parts marketplaces

Shift toward predictive maintenance solutions

Increasing demand for remanufactured components

Expansion of dealer service and maintenance contracts

Adoption of telematics driven diagnostics - Government Regulations & Defense Policy

Biosecurity and quarantine regulations affecting imported parts

Australian Design Rules compliance for machinery components

Environmental standards on emissions related replacement systems - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Engine Components and Overhaul Kits

Hydraulic Systems and Pumps

Transmission and Drivetrain Parts

Electrical and Electronic Modules

Wear Parts and Ground Engaging Tools - By Platform Type (In Value%)

Tractors

Combine Harvesters

Sprayers and Spreaders

Balers and Forage Equipment

Planting and Seeding Equipment - By Fitment Type (In Value%)

OEM Replacement Parts

Genuine Branded Parts

Aftermarket Compatible Parts

Remanufactured Components

Upgraded Performance Parts - By EndUser Segment (In Value%)

Broadacre Grain Farmers

Livestock and Mixed Farmers

Horticulture Growers

Agricultural Contractors

Agribusiness Cooperatives - By Procurement Channel (In Value%)

Authorized Dealer Networks

Independent Spare Parts Retailers

Online E commerce Platforms

Direct From Manufacturer

Agricultural Machinery Workshops - By Material / Technology (in Value %)

High Strength Alloy Steel Components

Precision Cast Iron Parts

Advanced Polymer and Composite Parts

Sensor Integrated Smart Components

Additive Manufactured Replacement Parts

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Product Portfolio Breadth, Distribution Network Strength, Pricing Strategy, Local Inventory Availability, Remanufacturing Capability, Technology Integration Level, After Sales Service Support, Brand Recognition, Supply Chain Resilience, Digital Platform Integration)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

AFGRI Equipment Australia

Emmetts Group

Wideland Group

RDO Equipment Australia

Clark Equipment Australia

Brown and Hurley

Intersales

Agriparts Australia

Bare Co Australia

Agrison

Gason

Tutt Bryant Equipment

MacDon Australia

Kubota Australia

CNH Industrial Australia

- Broadacre farmers prioritize durability and rapid availability of wear parts

- Livestock operators demand reliable engine and hydraulic replacements

- Contractors focus on minimizing downtime during peak seasons

- Horticulture growers prefer precision compatible electronic modules

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now