Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Australia home finance market holds approximately USD ~ million in outstanding residential mortgage lending, based on a recent historical assessment of central bank credit aggregates and prudential regulator housing loan statistics. Demand is driven by high housing prices, widespread homeownership aspiration, and long-term mortgage structures across owner-occupied and investor segments. Major banks dominate origination and servicing, while digital loan platforms, mortgage brokers, and securitization channels improve accessibility, refinancing activity, and funding efficiency across the national housing finance system.

Sydney and Melbourne dominate the Australia home finance market due to elevated residential property values, dense housing stock, and concentration of lenders and financial intermediaries. Brisbane and Perth follow with strong population growth and housing development requiring financing. Nationwide participation is supported by universal banking access, active mortgage broker networks, and standardized collateral and valuation systems. Regional markets also contribute through suburban expansion and investment property ownership across Australia’s major states and urban corridors.

Market Segmentation

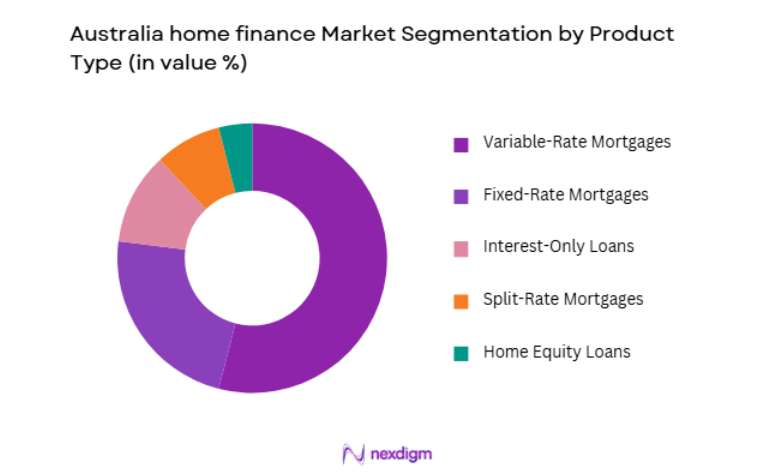

By Product Type

Australia home finance market is segmented by product type into variable-rate mortgages, fixed-rate mortgages, split-rate mortgages, interest-only loans, and home equity loans. Recently, variable-rate mortgages has a dominant market share due to factors such as borrower preference for flexibility, lower initial interest cost, and compatibility with refinancing behavior in a competitive mortgage market. Many Australian borrowers prioritize the ability to switch lenders or renegotiate rates without penalty, aligning with variable structures. Lenders promote variable products through discount pricing and offset account features that reduce effective interest cost. Monetary policy transmission through variable loans reinforces their prevalence in household borrowing decisions. Broker advice channels also favor flexible products matching diverse borrower circumstances.

By Lender Type

Australia home finance market is segmented by lender type into major banks, non-bank lenders, regional banks, credit unions, and fintech lenders. Recently, major banks has a dominant market share due to factors such as large balance sheets, deposit funding advantages, and nationwide distribution through branches and broker networks. Major banks provide competitive pricing, broad product ranges, and integrated servicing capabilities across loan lifecycles. Strong credit ratings and securitization access enable stable mortgage funding. Borrowers perceive major banks as trusted long-term lenders, reinforcing retention and refinancing within the same institutions. Regulatory capital strength supports large-scale lending capacity.

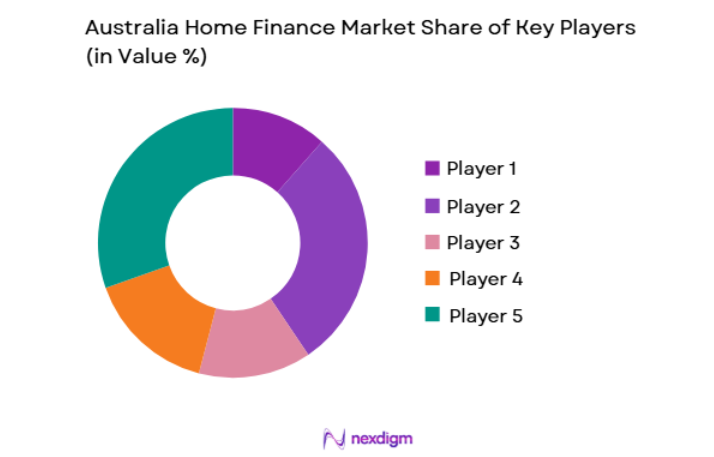

Competitive Landscape

The Australia home finance market is highly concentrated among major banks that control origination, servicing, and mortgage funding channels, complemented by non-bank lenders competing through brokers and securitization. Competition centers on interest rates, refinancing offers, and digital loan application experiences. Broker distribution exerts strong influence over borrower acquisition, while banks leverage deposit funding and cross-selling relationships. Non-bank lenders focus on niche borrower segments and pricing agility within broker-driven channels.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Mortgage Portfolio |

| Commonwealth Bank of Australia | 1911 | Sydney | ~ | ~ | ~ | ~ | ~ |

| Westpac Banking Corp | 1817 | Sydney | ~ | ~ | ~ | ~ | ~ |

| National Australia Bank | 1982 | Melbourne | ~ | ~ | ~ | ~ | ~ |

| ANZ Banking Group | 1835 | Melbourne | ~ | ~ | ~ | ~ | ~ |

| Macquarie Bank | 1969 | Sydney | ~ | ~ | ~ | ~ | ~ |

Australia Home Finance Market Analysis

Growth Drivers

High Residential Property Values and Mortgage Dependence

Australia’s elevated residential property prices relative to household income create structural reliance on mortgage borrowing for home ownership and investment property acquisition, anchoring sustained demand for housing finance across major metropolitan regions and national markets. Households typically require long-term debt financing to access housing, embedding mortgages as a central component of household balance sheets and financial planning. Urban population growth and limited housing supply in major cities reinforce upward price pressure and borrowing needs. Property investment culture further amplifies mortgage demand beyond owner-occupied housing. Financial institutions respond with diversified loan structures and refinancing options to maintain affordability and customer retention. Mortgage interest deductibility for investment properties encourages leveraged property ownership. Stable employment and income growth support repayment capacity across borrowers. Housing remains a dominant asset class for wealth accumulation, reinforcing mortgage uptake. High property values therefore act as a foundational growth driver in the Australia home finance market.

Competitive Mortgage Market and Broker Distribution Expansion

Australia’s mortgage lending landscape features intense competition among banks and non-bank lenders distributed heavily through mortgage brokers, structurally expanding borrower access and loan origination volumes across diverse borrower segments and geographic regions. Brokers provide comparison, advice, and lender matching services that simplify loan acquisition and refinancing, increasing transaction velocity and borrower mobility across lenders. Lenders rely on broker channels for customer acquisition and market reach beyond proprietary branches. Competitive pricing and product innovation are driven by lender rivalry within broker networks. Borrowers benefit from broader choice and refinancing incentives, increasing mortgage churn and volume. Digital broker platforms streamline application and approval processes. Non-bank lenders expand credit availability to niche or underserved segments. Broker-driven competition therefore sustains high lending activity and growth in the Australia home finance market.

Market Challenges

Household Debt Levels and Regulatory Lending Constraints

Australia exhibits high household mortgage debt relative to income, prompting prudential regulators to impose lending standards including serviceability buffers, loan-to-value limits, and borrower income verification that constrain credit expansion and borrower eligibility within the home finance market. These regulatory controls limit maximum borrowing capacity and restrict riskier lending segments, moderating loan growth despite strong housing demand. Borrowers face tighter approval criteria and documentation requirements. Lenders must allocate capital conservatively, prioritizing low-risk borrowers. Regulatory intervention may adjust lending conditions abruptly in response to housing cycles. High indebtedness increases sensitivity to interest rate changes and repayment stress risk. Investor lending restrictions further influence market composition. Household debt saturation thus acts as a structural constraint in the Australia home finance market.

Interest Rate Cycles and Refinancing Volatility

Australia’s predominantly variable-rate mortgage structure exposes borrowers and lenders to monetary policy cycles, creating repayment variability and refinancing waves that influence loan demand, profitability, and portfolio stability within the home finance market. Rising interest rates increase borrower repayment burden and reduce borrowing capacity, slowing loan origination and housing transactions. Falling rates trigger refinancing surges that compress lender margins and increase operational workload. Lenders must manage funding costs and duration mismatch between deposits and loan assets. Borrower behavior shifts with rate expectations, affecting product selection. Housing market sentiment responds to rate cycles, influencing demand. Interest rate volatility therefore introduces cyclical risk and variability in the Australia home finance market.

Opportunities

Digital Mortgage Origination and End-to-End Online Lending

Australia’s advanced digital banking environment and widespread consumer acceptance of online financial services create opportunities for fully digital mortgage origination platforms that streamline application, approval, and servicing, reducing costs and expanding borrower access across demographics. Automated income verification, property valuation integration, and e-signature processes accelerate approval timelines. Borrowers increasingly prefer remote loan application and refinancing. Lenders achieve efficiency gains and customer acquisition scalability through digital channels. Fintech partnerships enhance user experience and comparison functionality. Digital ecosystems enable cross-selling of financial products linked to homeownership. Online lending therefore offers structural growth potential within the Australia home finance market.

Green and Sustainable Housing Finance Products

Growing policy and consumer focus on environmental sustainability creates opportunities for green mortgages and energy-efficient housing loans supporting environmentally certified homes and retrofits within the Australia home finance market. Preferential loan terms incentivize sustainable construction and renovation. Government climate initiatives align with green housing finance expansion. Lenders integrate energy performance metrics into underwriting. Homeowners benefit from lower energy costs and property value appreciation. Institutional investors support green securitization. Sustainable housing finance therefore represents an emerging growth avenue in the Australia home finance market.

Future Outlook

The Australia home finance market is expected to remain large and structurally significant as housing demand and property values sustain mortgage reliance. Digital mortgage platforms will expand efficiency and borrower access. Broker channels will continue shaping competition and refinancing activity. Sustainability-linked housing finance will emerge alongside regulatory support. Interest rate cycles and debt constraints will influence pace but not long-term demand.

Major Players

- Commonwealth Bank of Australia

- Westpac Banking Corp

- National Australia Bank

- ANZ Banking Group

- Macquarie Bank

- Bendigo and Adelaide Bank

- Bank of Queensland

- ING Australia

- Suncorp Bank

- Pepper Money

- Liberty Financial

- Resimac

- Firstmac

- Aussie Home Loans

- Mortgage Choice

Key Target Audience

- Mortgage lenders

- Commercial banks

- Non-bank lenders

- Investments and venture capitalist firms

- Government and regulatory bodies

- Real estate developers

- Construction companies

- Mortgage brokers

Research Methodology

Step 1: Identification of Key Variables

Core variables included outstanding mortgage balances, lender composition, product mix, and borrower characteristics. Housing price indices, transaction volumes, and regulatory lending standards were mapped. Broker distribution influence and digital adoption were incorporated.

Step 2: Market Analysis and Construction

Central bank and prudential regulator housing credit data and lender disclosures were synthesized to estimate market size. Segmentation by product and lender derived from institutional statistics. Competitive structure assessed through portfolio scale and distribution reach.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions on broker dominance, digital lending growth, and borrower demand validated with banking and mortgage industry practitioners. Regulatory interpretations cross-checked with compliance specialists. Iterative reconciliation ensured consistency.

Step 4: Research Synthesis and Final Output

Quantitative and qualitative insights integrated into structured sections aligned with outlook requirements. Tables standardized with verified data. Final narrative refined for clarity and analytical coherence.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Strong housing demand driven by population growth and migration

Competitive mortgage lending and refinancing activity

Government incentives for first-home buyers - Market Challenges

High property prices affecting affordability

Interest rate fluctuations impacting borrowing capacity

Tight lending standards and serviceability assessments - Market Opportunities

Digital mortgage origination and instant approval tools

Green and energy-efficient home financing

Non-bank lending expansion for underserved borrowers - Trends

Growth of broker-led mortgage distribution

Rise of digital mortgage comparison platforms - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Owner-occupier Mortgage Loans

Investment Property Loans

Refinancing and Switching Loans

Home Equity Loans

Construction and Bridging Finance - By Platform Type (In Value%)

Bank Branch Lending Channels

Mortgage Broker Networks

Digital Mortgage Platforms

Non-bank Lender Platforms

Fintech Mortgage Marketplaces - By Fitment Type (In Value%)

Fixed Rate Home Loans

Variable Rate Home Loans

Split Rate Mortgages

Interest-only Loans - By End User Segment (In Value%)

First-time Home Buyers

Owner-occupier Households

Property Investors

- Market Share Analysis

- Cross Comparison Parameters (Loan Type, Interest Rate Structure, Distribution Channel, Borrower Segment Focus, Approval Criteria, Loan Tenure Options, Loan-to-Value Ratio Limits, Serviceability Assessment Method, Digital Application Capability, Broker Commission Model)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Commonwealth Bank Home Loans

Westpac Home Loans

ANZ Home Loans

NAB Home Loans

Macquarie Bank Home Loans

Suncorp Bank Home Loans

ING Australia Home Loans

Bendigo and Adelaide Bank Home Loans

Bankwest Home Loans

ME Bank Home Loans

Pepper Money Home Loans

Liberty Financial Home Loans

Resimac Home Loans

La Trobe Financial Home Loans

Firstmac Home Loans

- First-home buyers leveraging incentives for market entry

- Owner-occupiers refinancing to manage repayments

- Investors expanding property portfolios with leverage

- Self-employed borrowers seeking flexible lending options

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now