Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Australia’s last-mile delivery market reached approximately USD ~ billion based on a recent historical assessment, supported by strong expansion in e-commerce retail logistics and parcel distribution networks across metropolitan and regional delivery corridors. Rapid digital commerce adoption, high parcel shipment volumes, and widespread online retail participation continue driving logistics demand for courier networks, parcel sorting infrastructure, and urban delivery fleets. Major logistics providers invest heavily in automated fulfilment centers, route optimization technologies, and integrated delivery platforms to support rising parcel volumes generated by online marketplaces and retail distribution networks.

Market Segmentation

By Delivery Type

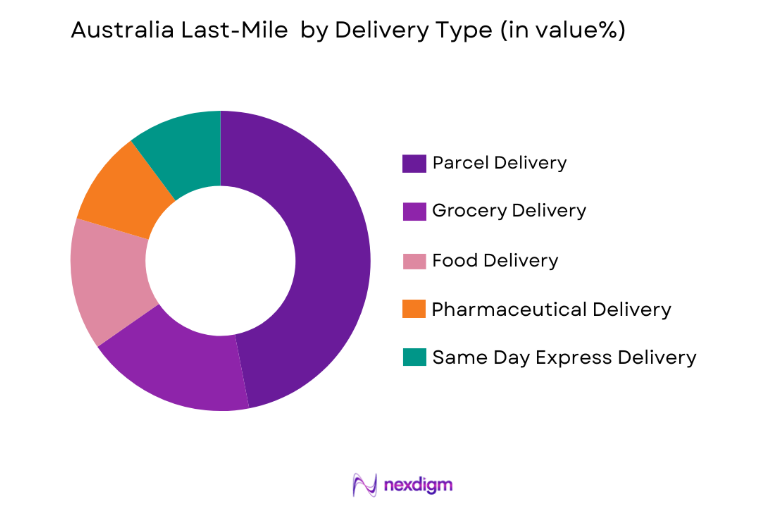

Australia Last-Mile Delivery Market is segmented by delivery type into parcel delivery, grocery delivery, food delivery, pharmaceutical delivery, and same-day express delivery. Recently, parcel delivery has a dominant market share due to strong e-commerce retail activity and growing online shopping participation across Australian consumers. Large digital marketplaces generate extremely high parcel shipment volumes involving electronics, clothing, consumer goods, and household products requiring efficient last-mile distribution networks. Logistics providers therefore expand parcel sorting infrastructure, automated warehouses, and regional fulfillment hubs capable of managing high order volumes. Parcel logistics operations also benefit from strong national courier networks operated by major providers and established third-party logistics companies. Continuous investment in route optimization software, digital tracking platforms, and automated parcel handling systems further improves operational efficiency within parcel delivery networks. These operational advantages combined with strong demand from online retail marketplaces significantly strengthen the dominance of parcel delivery services within Australia’s last-mile delivery market ecosystem.

By Vehicle Type

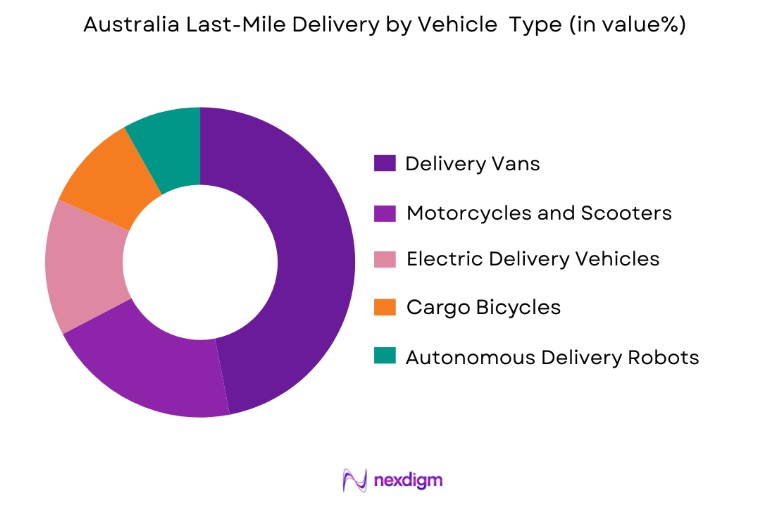

Australia Last-Mile Delivery Market is segmented by vehicle type into delivery vans, motorcycles and scooters, electric delivery vehicles, cargo bicycles, and autonomous delivery robots. Recently, delivery vans have a dominant market share due to their ability to transport high parcel volumes across urban and suburban delivery routes efficiently. Courier companies and logistics providers rely heavily on delivery vans because they support flexible routing, large cargo capacity, and cost-efficient parcel transportation across metropolitan delivery networks. Retail fulfillment centers and parcel distribution hubs typically load bulk shipments onto delivery vans that distribute goods across residential neighborhoods and commercial zones. These vehicles also enable logistics providers to manage multiple deliveries within a single route while maintaining operational productivity and timely shipment distribution. Their operational reliability, cargo capacity, and integration with courier fleet management systems ensure that delivery vans remain the most widely utilized transportation platform within last-mile delivery logistics operations across Australia.

Competitive Landscape

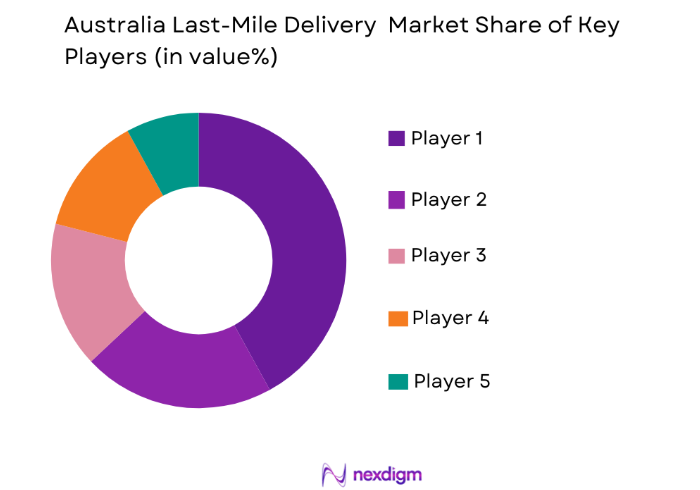

The Australia last-mile delivery market demonstrates moderate consolidation with several major logistics providers controlling significant distribution networks across national delivery corridors. Large courier companies operate extensive parcel sorting facilities, regional fulfillment warehouses, and nationwide transportation fleets capable of managing high parcel shipment volumes. Global logistics operators compete alongside domestic delivery platforms and technology-enabled courier services that offer digital parcel tracking, automated dispatch systems, and flexible delivery solutions. Continuous investment in automation technologies and urban logistics infrastructure strengthens the competitive position of established logistics providers within Australia’s expanding e-commerce delivery ecosystem.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Fleet Size |

| Australia Post | 1809 | Melbourne | ~ | ~ | ~ | ~ | ~ |

| Toll Group | 1888 | Melbourne | ~ | ~ | ~ | ~ | ~ |

| Linfox Logistics | 1956 | Melbourne | ~ | ~ | ~ | ~ | ~ |

| DHL Express Australia | 1969 | Bonn | ~ | ~ | ~ | ~ | ~ |

| FedEx Australia | 1971 | Memphis | ~ | ~ | ~ | ~ | ~ |

Australia Last-Mile Market Analysis

Growth Drivers

Expansion of E-Commerce Retail Logistics Networks

Rapid expansion of digital commerce platforms across Australia significantly strengthens demand for efficient last-mile delivery infrastructure capable of supporting large parcel shipment volumes generated by online retail marketplaces and mobile commerce applications. Consumers increasingly purchase electronics, clothing, groceries, and household goods through digital retail platforms that require reliable logistics networks connecting fulfillment centers with residential delivery destinations across metropolitan regions. Major logistics companies therefore expand automated parcel sorting facilities and robotics-enabled warehouses capable of processing large order volumes efficiently while maintaining consistent delivery timelines for consumers. Retail companies increasingly outsource logistics operations to third-party delivery providers capable of managing complex nationwide distribution networks connecting suppliers, warehouses, and consumers across large geographic areas. Investments in route optimization software and artificial intelligence-driven fleet management technologies further improve operational productivity across urban delivery corridors. Large digital retailers also establish regional fulfillment warehouses located near population centers that reduce delivery distances and accelerate order processing times across distribution networks. Growth in cross-border e-commerce trade involving imports from international retail platforms also increases parcel shipment volumes across courier networks operating within Australia’s consumer logistics ecosystem. Continuous adoption of mobile payment platforms and digital commerce applications further expands online retail participation across consumer segments nationwide.

Consumer Demand for Rapid Delivery Services and Same Day Logistics

Consumer expectations for faster delivery services significantly strengthen operational expansion across Australia’s last-mile logistics networks as online shoppers increasingly demand same-day and next-day delivery services for retail purchases. Retail platforms compete aggressively on delivery speed, which requires logistics providers to develop advanced urban distribution infrastructure capable of accelerating parcel movement between warehouses and residential destinations. Courier companies therefore invest heavily in micro-fulfillment centers and localized distribution hubs located near major urban populations to support rapid parcel dispatch operations. Automated parcel sorting technologies and advanced warehouse robotics enable logistics providers to process large shipment volumes quickly while reducing manual handling requirements across fulfillment operations. Real-time shipment tracking platforms and predictive analytics systems allow logistics operators to optimize delivery routes while reducing transportation delays caused by traffic congestion and urban logistics constraints. Food delivery platforms and grocery retailers also strengthen demand for rapid delivery networks that can distribute perishable goods quickly across metropolitan regions. Integration of digital dispatch platforms connecting courier drivers with parcel shipments further improves fleet productivity and delivery efficiency across nationwide courier operations. These operational innovations significantly strengthen demand for sophisticated last-mile logistics infrastructure capable of supporting Australia’s rapidly expanding e-commerce economy.

Market Challenges

Urban Logistics Congestion and Rising Transportation Costs

Increasing urban traffic congestion across major Australian metropolitan regions creates operational challenges for last-mile delivery providers responsible for transporting parcels through densely populated city environments where road capacity and delivery access points remain limited. Delivery vehicles often experience delays when navigating congested transportation corridors that increase delivery times and reduce operational productivity across courier fleet networks operating in large cities. Logistics providers must therefore allocate additional resources including expanded delivery fleets and additional drivers in order to maintain service reliability while meeting customer delivery expectations. Rising fuel costs and vehicle maintenance expenses further increase transportation operating costs across courier companies responsible for managing large commercial delivery fleets across national distribution networks. Delivery providers also face logistical challenges associated with limited parking infrastructure in high-density commercial districts where delivery vehicles must compete with passenger traffic for access space. Urban delivery regulations and restricted loading zones also influence operational scheduling requirements that may limit delivery flexibility during peak retail shipment periods. Increasing parcel volumes generated by expanding e-commerce transactions place additional pressure on courier infrastructure and urban road networks already experiencing congestion constraints. These operational complexities create cost pressures for logistics providers that must continuously invest in fleet management technologies and route optimization systems to maintain efficient last-mile delivery operations.

Labor Shortages and Workforce Availability in Courier Operations

Labor availability challenges represent another major constraint affecting last-mile delivery logistics operations across Australia where courier companies require large numbers of drivers, warehouse workers, and distribution staff to manage rapidly expanding parcel shipment volumes. Courier companies frequently face workforce shortages during peak retail seasons when online shopping demand generates extremely high delivery requirements across metropolitan logistics networks. Recruiting and retaining qualified drivers capable of operating commercial delivery vehicles remains difficult due to demanding work schedules and increasing competition from other logistics employers operating within Australia’s transportation sector. Warehouse staffing challenges also affect parcel sorting operations where automated fulfillment centers still require human oversight for packaging, loading, and operational coordination across distribution facilities. Logistics companies must therefore increase wages, provide training programs, and invest in workforce retention initiatives that increase operating costs across delivery networks. Labor shortages can also cause operational delays when courier providers cannot maintain sufficient staffing levels required to process large shipment volumes efficiently. Growing demand for gig economy delivery services partially addresses workforce shortages but also introduces workforce management complexities associated with flexible contractor employment structures. These labor challenges require logistics providers to continuously adapt workforce strategies and operational technologies to sustain reliable last-mile delivery performance.

Opportunities

Expansion of Sustainable Electric Delivery Fleets and Green Logistics Infrastructure

Increasing environmental sustainability initiatives across Australia create major opportunities for logistics companies to deploy electric delivery vehicles and low-emission transportation systems capable of reducing carbon emissions across last-mile delivery operations. Government environmental policies and corporate sustainability targets encourage logistics providers to transition from conventional fuel powered vehicles toward electric delivery fleets that produce significantly lower emissions across urban distribution networks. Electric vans and compact electric delivery vehicles enable courier companies to operate efficiently across short urban delivery routes while minimizing fuel consumption and environmental impact. Logistics companies also invest in charging infrastructure and energy management systems that support the operational deployment of electric fleets across metropolitan logistics networks. Adoption of sustainable delivery technologies also improves brand reputation among environmentally conscious consumers who increasingly prefer retailers that support environmentally responsible supply chain practices. Green logistics initiatives further encourage companies to develop innovative delivery solutions including cargo bicycle distribution networks and micro-fulfillment hubs located close to residential populations. As environmental regulations continue strengthening across transportation sectors, electric delivery technologies present major investment opportunities for logistics providers expanding sustainable last-mile delivery infrastructure.

Adoption of Automation Technologies and Intelligent Delivery Systems

Technological innovation creates major growth opportunities within Australia’s last-mile delivery market as logistics providers increasingly adopt advanced automation technologies and digital delivery platforms capable of improving operational efficiency across complex distribution networks. Automated parcel sorting systems, robotics enabled warehouses, and artificial intelligence driven logistics platforms allow courier companies to process extremely high parcel volumes while minimizing operational errors and reducing manual handling requirements. Intelligent route optimization software enables delivery providers to analyze traffic conditions and delivery patterns in real time allowing courier fleets to optimize delivery routes and reduce transportation delays across urban distribution corridors. Logistics companies also explore autonomous delivery technologies including robotic delivery vehicles and drone based parcel transportation systems capable of supporting rapid parcel distribution within dense urban environments. Integration of digital logistics platforms connecting retailers, warehouses, and courier fleets further improves supply chain visibility and coordination across nationwide delivery networks. These technological developments create substantial opportunities for logistics providers to expand service capabilities while reducing operational costs across last-mile logistics operations. Continued investment in logistics automation technologies therefore remains a major growth opportunity shaping the long-term evolution of Australia’s delivery infrastructure.

Future Outlook

The Australia last-mile delivery market is expected to experience sustained expansion driven by continued growth in e-commerce retail distribution and digital commerce adoption. Logistics providers will increasingly invest in automation technologies, smart warehouse infrastructure, and advanced fleet management platforms to improve delivery efficiency across urban logistics networks. Government sustainability initiatives will encourage deployment of electric delivery fleets and environmentally responsible logistics infrastructure. Rapid development of autonomous delivery technologies and urban micro-fulfillment centers will further transform parcel distribution capabilities while supporting faster delivery services across major metropolitan regions.

Major Players

- Australia Post

- Toll Group

- Linfox Logistics

- DHL Express Australia

- FedEx Australia

- UPS Australia

- StarTrack

- Aramex Australia

- CouriersPlease

- Sendle

- Team Global Express

- ANC Delivers

- Sherpa

- Zoom2u

- Direct Couriers

Key Target Audience

- Logistics and supply chain companies

- E-commerce retail platforms

- Investments and venture capitalist firms

- Government and regulatory bodies

- Courier and parcel service providers

- Retail distribution companies

- Transportation infrastructure operators

- Technology providers forlogistic sautomation

Research Methodology

Step 1: Identification of Key Variables

The research process begins by identifying major variables influencing the Australia last-mile delivery market including parcel volumes, e-commerce activity, logistics infrastructure development, and transportation network capacity across urban and regional distribution corridors.

Step 2: Market Analysis and Construction

Market data is analyzed through a combination of logistics industry reports, transportation statistics, and corporate disclosures from major courier operators to construct a structured representation of market demand and operational supply chains.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including logistics executives, transportation analysts, and supply chain specialists are consulted to validate key market assumptions regarding parcel shipment volumes, operational challenges, and technological innovation shaping delivery infrastructure.

Step 4: Research Synthesis and Final Output

All validated information is synthesized into structured market insights combining quantitative logistics data with qualitative industry expertise to produce a comprehensive assessment of the Australia last-mile delivery market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of E Commerce Retail Distribution Networks

Growing Demand for Same Day and Next Day Delivery Services

Investment in Urban Fulfillment Infrastructure and Parcel Automation - Market Challenges

Urban Traffic Congestion Affecting Delivery Efficiency

High Operational Costs in Last Mile Logistics

Labor Shortages Across Courier and Delivery Workforce - Market Opportunities

Adoption of Electric Delivery Fleets and Sustainable Logistics

Expansion of Micro Fulfillment Centers in Urban Areas

Growth of Drone and Autonomous Delivery Technologies - Trends

Integration of AI Based Route Optimization Platforms

Expansion of Parcel Locker Networks Across Urban Locations

Adoption of Real Time Shipment Tracking Technologies - Government Regulations

- SWOT Analysis of Key Competitors

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Parcel Delivery Services

Grocery and Food Delivery

Retail Goods Delivery

Pharmaceutical and Healthcare Delivery

Express and Same Day Delivery Services - By Platform Type (In Value%)

Road Based Delivery Fleets

Electric Delivery Vehicles

Autonomous Delivery Robots

Drone Delivery Systems

Hybrid Urban Delivery Platforms - By Fitment Type (In Value%)

Dedicated Delivery Networks

Third Party Logistics Integration

Crowdsourced Delivery Networks

Urban Micro Fulfillment Integration

Hub and Spoke Distribution Models - By EndUser Segment (In Value%)

E Commerce Retailers

Food Delivery Platforms

Healthcare and Pharmaceutical Providers

Consumer Electronics Retailers

- Market Share Analysis

- CrossComparison Parameters (Service Coverage, Delivery Speed, Fleet Technology, Pricing Strategy, E Commerce Integration)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

Australia Post

Toll Group

Linfox Logistics

Aramex Australia

StarTrack

CouriersPlease

Fastway Couriers

Sendle

DHL Express Australia

FedEx Australia

UPS Australia

Team Global Express

Zoom2u

Sherpa

ANC Delivers

- Retailers Increasing Reliance on Outsourced Delivery Networks

- Food Delivery Platforms Expanding Urban Distribution Operations

- Healthcare Sector Requiring Rapid Pharmaceutical Deliveries

- Supermarket Chains Investing in Home Grocery Delivery Infrastructure

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now