Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Australian medical devices market has witnessed consistent growth, driven by technological advancements, the aging population, and rising healthcare needs. The market is valued at approximately USD ~ billion, with steady growth propelled by increasing demand for diagnostic, therapeutic, and monitoring devices. These factors are being supported by both government funding and private investments, particularly in health tech innovation and digital health solutions. The market’s development is further boosted by regulatory support aimed at enhancing the healthcare infrastructure.

Australia remains a dominant player in the medical devices market due to its well-established healthcare system, strong regulatory framework, and advanced technological infrastructure. Major cities like Sydney, Melbourne, and Brisbane lead the market, benefiting from their high concentration of healthcare facilities, research institutions, and access to top-tier healthcare professionals. The country’s strategic location in the Asia-Pacific region and robust export policies further cement its role as a significant market leader in the sector.

Market Segmentation

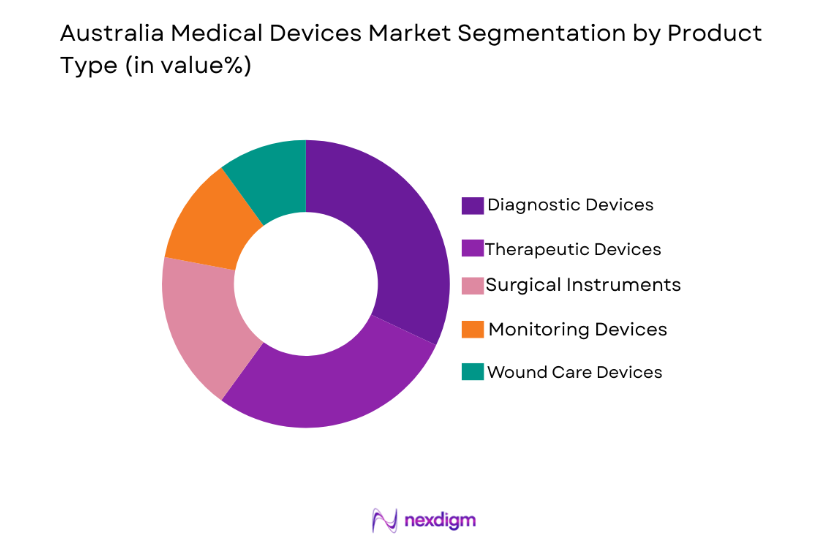

By Product Type

The Australian medical devices market is segmented by product type into diagnostic devices, therapeutic devices, surgical instruments, monitoring devices, and wound care devices. Recently, diagnostic devices have seen the dominant market share due to their increasing use in early detection and prevention of diseases, particularly with the rising demand for non-invasive diagnostic technologies. The growth of diagnostic devices is attributed to technological advancements, government health initiatives, and an increasing focus on early disease detection.

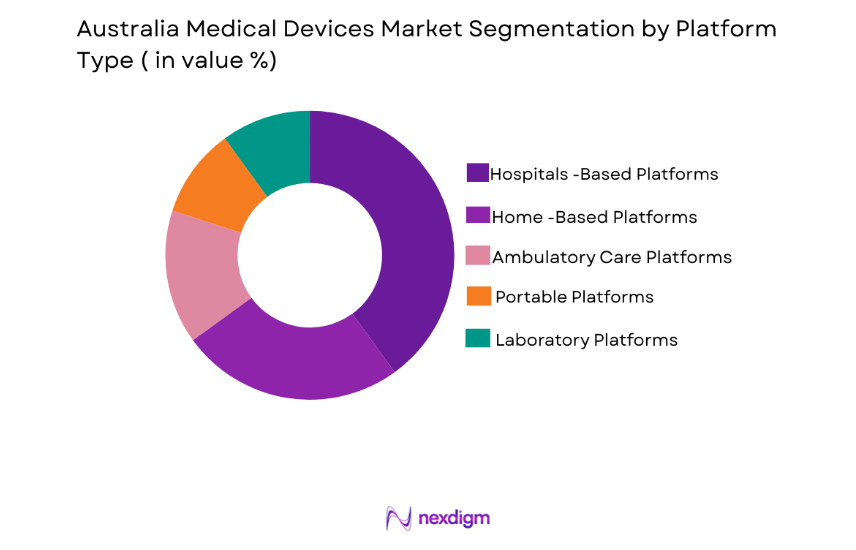

By Platform Type

The market is segmented by platform type into hospital-based platforms, home-based platforms, ambulatory care platforms, portable platforms, and laboratory platforms. Hospital-based platforms have a dominant market share due to the high prevalence of chronic diseases, the increasing number of hospital admissions, and the need for continuous monitoring. This dominance is reinforced by the growing adoption of integrated hospital systems that improve patient outcomes through better diagnostics and treatment tracking.

Competitive Landscape

The competitive landscape in the Australian medical devices market is shaped by both local and international companies vying for a share in a growing industry. Major players are focusing on expanding their technological capabilities and investing in R&D to maintain a competitive edge. The market has witnessed a wave of consolidation, with key players entering strategic partnerships and collaborations to expand their product offerings. Players are also strengthening their market presence through mergers and acquisitions to improve their distribution networks and enhance consumer engagement.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Market-Specific Parameter |

| ResMed | 1989 | Sydney, Australia | ~ | ~ | ~ | ~ | ~ |

| Cochlear | 1981 | Sydney, Australia | ~ | ~ | ~ | ~ | ~ |

| Stryker | 1941 | Kalamazoo, USA | ~ | ~ | ~ | ~ | ~ |

| Medtronic | 1949 | Minneapolis, USA | ~ | ~ | ~ | ~ | ~ |

| Philips Healthcare | 1891 | Amsterdam, Netherlands | ~ | ~ | ~ | ~ | ~ |

Australia Medical Devices Market Analysis

Growth Drivers

Increasing Healthcare Expenditure

Healthcare spending in Australia has seen a consistent rise, driven by the aging population and the increasing demand for advanced medical technologies. As the number of elderly individuals grows, there is a corresponding increase in the need for medical devices to manage chronic conditions such as heart disease, diabetes, and joint disorders, improving the overall quality of life. The Australian government’s commitment to expanding healthcare access, as well as funding for medical research, plays a pivotal role in propelling the market. Government-backed health initiatives also support the adoption of advanced technologies, allowing for better infrastructure and enabling patients to receive top-tier treatments utilizing the latest medical devices. Moreover, the introduction of digital health solutions has significantly enhanced the accessibility and delivery of healthcare services, allowing healthcare professionals to offer more efficient, timely, and personalized care. With continued healthcare spending, the market for medical devices in Australia is expected to remain strong as both public and private investments increase, creating a conducive environment for the growth of innovative healthcare technologies.

Technological Advancements in Medical Devices

Technological innovations in medical devices, such as robotic surgeries, telemedicine platforms, and diagnostic imaging systems, are pivotal in driving market growth. These advancements not only provide more accurate diagnoses but also improve treatment outcomes and enhance the quality of patient care—key factors in the evolving healthcare industry. The demand for high-quality diagnostic and monitoring devices has grown as healthcare providers seek to offer quicker, more efficient, and more effective treatments. With the continued development of digital health solutions, such as remote patient monitoring and telehealth services, healthcare systems can better manage chronic diseases, minimize in-hospital stays, and reduce the burden on healthcare facilities. Additionally, the rapid adoption of minimally invasive surgical technologies is improving patient outcomes and reducing recovery times. As the medical device landscape evolves, the Australian market will see sustained growth driven by these technological innovations, which meet the rising demand for precision and improved healthcare outcomes, contributing to the overall market expansion.

Market Challenges

High Regulatory Barriers

The Australian medical devices market faces significant challenges due to the stringent regulatory standards set by the Therapeutic Goods Administration (TGA), which governs the approval of medical devices in the country. The TGA enforces a rigorous approval process to ensure that only safe and effective products reach the market, which can create barriers to entry for new players, especially smaller companies with limited resources. These regulations are vital for consumer safety, but they add complexity and delay to the development process. Moreover, the high costs and time-consuming nature of gaining regulatory approval can result in delayed product launches, which limits the pace of innovation in the market. Companies must navigate not only local regulations but also international standards, further complicating their path to market. This process can result in additional compliance costs, reducing profit margins and deterring smaller companies from entering the market. The ongoing challenge of maintaining compliance with regulatory standards while managing the costs associated with these processes is a critical factor impacting the speed at which new technologies are introduced in Australia’s medical devices market.

Cost of Advanced Medical Devices

The high cost of advanced medical devices remains a significant challenge in the Australian market, particularly for smaller healthcare facilities and patients in rural or underserved areas. While advancements in medical technology have the potential to improve healthcare outcomes, the expense of devices such as diagnostic imaging systems, robotic surgery equipment, and life-saving therapeutic tools can be prohibitive for many healthcare institutions, especially in the public sector. This cost barrier is exacerbated by the limited funding available for health systems in non-urban areas, where healthcare budgets are constrained. Despite the Australian government’s efforts to subsidize the healthcare system and provide financial support to public hospitals, the price of cutting-edge medical devices can still hinder their widespread adoption. These high costs not only affect hospitals and clinics but also place a strain on patients who may be required to bear a portion of the financial burden. This challenge impacts the accessibility of medical devices across the entire healthcare system, slowing the adoption of state-of-the-art technologies, particularly in rural or economically disadvantaged regions.

Opportunities

Expanding Home Healthcare Solutions

As Australia’s population continues to age, there is a growing shift toward home-based healthcare solutions, creating new opportunities for the medical device market. Devices that enable remote monitoring, home diagnostics, and telemedicine are increasingly being adopted by both patients and healthcare providers. These devices, which allow patients to monitor chronic conditions, track vital signs, and receive healthcare services from the comfort of their homes, are crucial in managing the increasing burden on hospitals and healthcare systems. As more Australians opt for home healthcare solutions, there is a significant opportunity for medical device manufacturers to develop products tailored for remote care. These solutions not only provide convenience for patients but also help reduce the pressure on healthcare facilities by offering proactive care management and reducing hospital readmissions. The rise of digital health platforms and the increasing integration of telemedicine are expected to drive substantial growth in the home healthcare segment, enhancing patient outcomes and offering a cost-effective alternative to traditional in-hospital care. The market for home healthcare devices is poised to expand as these solutions become more affordable, efficient, and accessible, creating new avenues for growth.

Rise of Wearable Medical Devices

Wearable medical devices are rapidly gaining traction in the Australian market, driven by consumer demand for health and wellness monitoring. Devices such as smartwatches, fitness trackers, and wearable ECG monitors are increasingly popular due to their ability to provide real-time health data and enable proactive care. With advancements in wireless technologies and the Internet of Things (IoT), wearable medical devices are becoming more sophisticated and capable of tracking a wider range of health metrics, from heart rate and sleep patterns to blood oxygen levels and activity levels. The increasing awareness of health and wellness, along with the desire for personalized and continuous health monitoring, has accelerated the adoption of these devices. Wearables allow users to manage chronic conditions, monitor their fitness, and receive alerts for potential health issues before they become critical, offering a convenient way to track and improve overall well-being. The rise of wearable medical devices represents a substantial growth opportunity for the Australian medical device market, as both established manufacturers and new tech companies seek to capitalize on this emerging trend by introducing innovative products that cater to the growing demand for health monitoring on the go.

Future Outlook

Over the next five years, the Australian medical devices market is expected to experience steady growth, driven by ongoing technological advancements and an aging population. The adoption of digital health technologies, coupled with increasing government investment in healthcare infrastructure, will continue to support market expansion. Regulatory frameworks are likely to evolve to accommodate innovative medical devices, while consumer demand for affordable, high-quality healthcare solutions will spur product development and market diversification. New opportunities will emerge in home healthcare and wearable devices, as both consumers and healthcare providers embrace convenience and efficiency.

Major Players

- ResMed

- Cochlear

- Stryker

- Medtronic

- Philips Healthcare

- Siemens Healthineers

- GE Healthcare

- Johnson & Johnson

- Smith & Nephew

- Abbott Laboratories

- Baxter International

- Zimmer Biomet

- Boston Scientific

- Thermo Fisher Scientific

- B. Braun Melsungen AG

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare providers

- Medical device manufacturers

- Pharmaceutical companies

- Insurance providers

- Hospitals and clinics

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves identifying the core variables that influence the medical devices market, such as technological innovations, healthcare policies, and market dynamics.

Step 2: Market Analysis and Construction

In this phase, a thorough market analysis is performed to evaluate the medical devices market’s current landscape, segment structure, and growth potential.

Step 3: Hypothesis Validation and Expert Consultation

Experts from relevant sectors, including healthcare professionals and industry leaders, validate the hypotheses developed in the previous phase, ensuring the findings reflect real-world insights.

Step 4: Research Synthesis and Final Output

Finally, all findings are synthesized into a cohesive report that offers actionable insights and recommendations for stakeholders, guiding them in making informed decisions.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Increasing Healthcare Spending

Technological Advancements in Medical Devices

Aging Population and Chronic Diseases - Market Challenges

Regulatory Compliance Challenges

High Cost of Advanced Medical Devices

Limited Access to Healthcare in Rural Areas - Market Opportunities

Expansion of Home Healthcare Solutions

Growth of Wearable Medical Devices

Technological Integration for Telemedicine and Remote Monitoring - Trends

Adoption of AI and Machine Learning in Diagnostics

Rise in Telehealth and Remote Patient Monitoring - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Diagnostic Devices

Therapeutic Devices

Surgical Instruments

Monitoring Devices

Wound Care Devices - By Platform Type (In Value%)

Hospital-Based Platforms

Home-Based Platforms

Ambulatory Care Platforms

Portable Platforms

Laboratory Platforms - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Integrated Solutions

Wearable Solutions - By End User Segment (In Value%)

Hospitals

Clinics

Home Care Providers

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, End User Segment, Fitment Type, Pricing, Technological Advancements, Regulatory Compliance)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

ResMed

Cochlear

Stryker

Medtronic

Siemens Healthineers

Philips Healthcare

GE Healthcare

Johnson & Johnson

Smith & Nephew

Abbott Laboratories

Baxter International

Zimmer Biomet

Boston Scientific

Thermo Fisher Scientific

B. Braun Melsungen AG

- Increasing Demand for Advanced Diagnostic Devices

- Rise in Home Healthcare Demand

- Growing Focus on Minimally Invasive Surgical Procedures

- Adoption of Remote Monitoring Technologies

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now