Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Australia online insurance market generated approximately USD ~ billion in digitally originated gross written premiums, based on a recent historical assessment of prudential regulator statistics and insurer disclosures. Growth is driven by widespread internet adoption, comparison platforms, and direct-to-consumer insurer channels across motor, home, and travel lines. Digital underwriting, automated claims, and mobile policy servicing reduce acquisition and operating costs, encouraging insurers to shift distribution online and consumers to purchase and manage policies through digital interfaces.

Sydney and Melbourne dominate the Australia online insurance market due to dense insured populations, concentration of insurers, and advanced digital financial ecosystems enabling seamless online purchase and servicing. Brisbane and Perth follow with strong vehicle ownership and property insurance demand supported by urban growth. Nationwide digital adoption is reinforced by high broadband penetration, established price comparison websites, and regulatory acceptance of electronic documentation and remote identity verification across metropolitan and regional Australia.

Market Segmentation

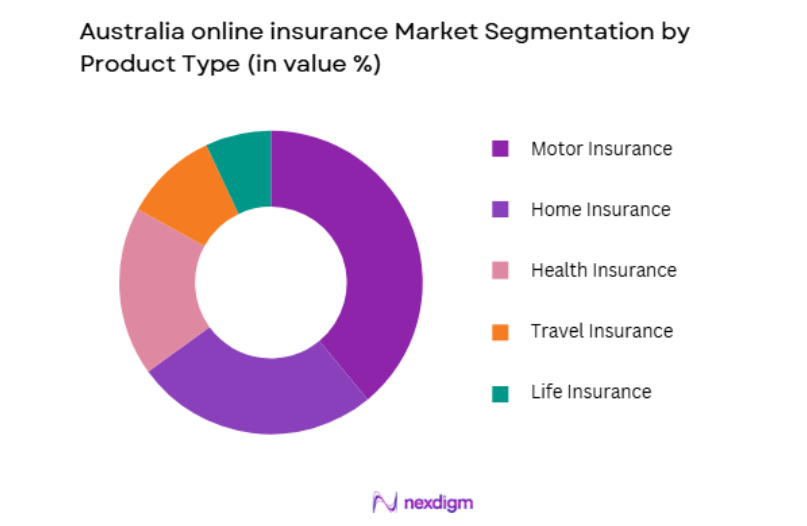

By Product Type

Australia online insurance market is segmented by product type into motor insurance, home insurance, health insurance, travel insurance, and life insurance. Recently, motor insurance has a dominant market share due to factors such as mandatory vehicle coverage requirements, high vehicle ownership rates, and strong price comparison behavior among consumers. Motor policies are standardized and easily comparable, making them well suited to online purchase journeys through insurer websites and aggregators. Insurers prioritize digital motor distribution because claims and underwriting data are structured and automation-ready, enabling rapid quoting and servicing. Frequent renewals and switching cycles further drive online engagement. Younger digitally native drivers prefer self-service purchase and claims submission via mobile platforms. These structural characteristics sustain motor insurance leadership in online distribution within the Australia online insurance market.

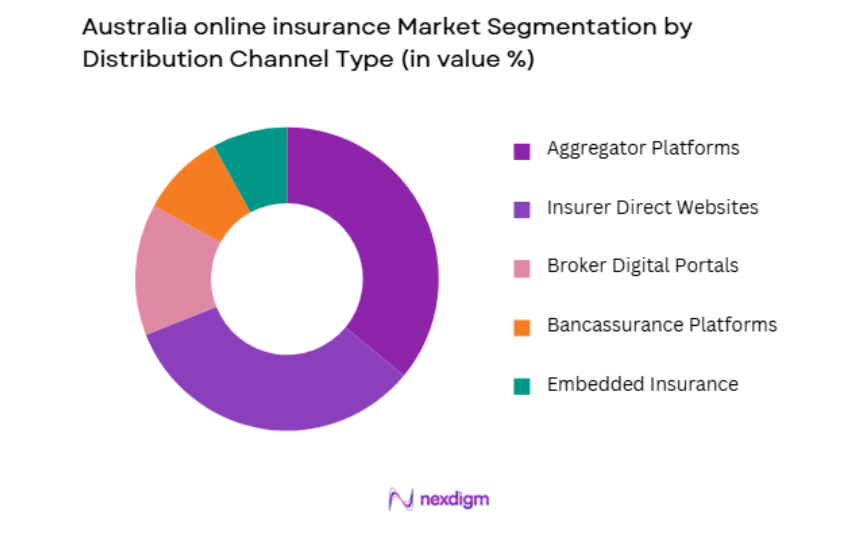

By Distribution Channel

Australia online insurance market is segmented by distribution channel into insurer direct websites, aggregator platforms, broker digital portals, bancassurance platforms, and embedded insurance channels. Recently, aggregator platforms has a dominant market share due to factors such as strong consumer price sensitivity, established comparison culture, and trust in independent quote marketplaces. Comparison websites aggregate multiple insurer quotes, enabling transparent price and feature evaluation that encourages switching and online purchase completion. Insurers rely on aggregators for customer acquisition, particularly in motor and home lines with standardized coverage structures. Digital marketing and search behavior often direct consumers first to comparison platforms before insurer sites. Aggregators also simplify policy management and renewal reminders across providers.

Competitive Landscape

The Australia online insurance market is moderately consolidated among large general insurers and direct insurance brands that operate extensive digital distribution and pricing analytics capabilities. Competition centers on online pricing, user experience, and aggregator presence. Incumbents leverage brand recognition and underwriting scale, while digital-first brands focus on direct online acquisition and simplified products. Comparison platforms exert strong influence over customer acquisition economics and switching behavior.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Online Policy Share |

| Insurance Australia Group | 2000 | Sydney | ~ | ~ | ~ | ~ | ~ |

| Suncorp Group | 1996 | Brisbane | ~ | ~ | ~ | ~ | ~ |

| QBE Insurance | 1886 | Sydney | ~ | ~ | ~ | ~ | ~ |

| Allianz Australia | 1914 | Sydney | ~ | ~ | ~ | ~ | ~ |

| Auto & General Holdings | 1985 | Brisbane | ~ | ~ | ~ | ~ | ~ |

Australia Online Insurance Market Analysis

Growth Drivers

Digital Comparison Culture and Price Transparency Behavior

Australia’s insurance purchasing environment is strongly shaped by widespread consumer use of online comparison platforms and price discovery tools that normalize digital-first policy shopping across motor, home, and travel insurance categories, structurally expanding the online channel’s share of insurance distribution. Consumers routinely compare multiple insurers before purchase, driving competition on price and features within digital marketplaces and encouraging insurers to optimize online acquisition funnels and pricing algorithms. High switching propensity in commoditized lines like motor insurance amplifies renewal-driven online engagement cycles, sustaining digital premium volumes. Comparison platforms invest heavily in marketing and search visibility, capturing initial consumer intent and channeling traffic toward online purchase completion. Insurers align product design and pricing transparency with aggregator requirements, reinforcing digital suitability of offerings. Mobile-friendly interfaces and instant quoting capabilities reduce friction in policy selection and purchase. Regulatory acceptance of electronic disclosure and documentation further legitimizes online-only transactions.

High Internet Penetration and Direct Digital Insurer Strategies

Australia exhibits near-universal internet and smartphone penetration, enabling insurers to deploy direct-to-consumer digital strategies that bypass traditional broker and agent channels, lowering acquisition costs and expanding reach across urban and regional populations. Insurers invest in end-to-end online journeys encompassing quote, bind, payment, and claims, supported by automated underwriting and data-driven risk pricing. Direct brands emphasize simplicity and self-service features aligned with consumer expectations for digital financial products. Cost efficiencies achieved through digital distribution enable competitive premiums that attract price-sensitive online shoppers. Digital servicing platforms facilitate policy changes, renewals, and claims submission without physical interaction, reinforcing channel preference. Younger demographics exhibit strong comfort with online insurance purchasing, accelerating generational shift toward digital distribution. Integration of telematics, property data, and behavioral analytics enhances online risk assessment accuracy. Insurers’ strategic prioritization of direct digital growth thus materially expands the Australia online insurance market.

Market Challenges

Aggregator Dependency and Margin Compression Pressure

The Australia online insurance market is heavily influenced by comparison platforms that control significant customer acquisition flow, creating dependency among insurers that must compete aggressively on price and commissions to secure prominent listing positions and conversion rates. Aggregators’ bargaining power compresses insurer margins as carriers absorb referral fees and discount pricing to remain competitive within comparison rankings. Brand differentiation is reduced when consumers focus primarily on price rather than service or coverage nuances, commoditizing core insurance products. Insurers face limited control over customer relationships when acquisition occurs through third-party platforms, reducing cross-sell and retention potential. Marketing costs escalate as insurers bid for digital visibility and aggregator placement. Smaller insurers may struggle to sustain economics within aggregator-driven acquisition models. Regulatory scrutiny of comparison practices can alter channel dynamics abruptly. Dependence on aggregators therefore represents a structural profitability challenge within the Australia online insurance market.

Fraud Risk and Digital Claims Vulnerability

Increased online policy issuance and automated claims processing expose insurers in the Australia online insurance market to heightened fraud risk, identity misuse, and opportunistic claims behaviors facilitated by digital anonymity and rapid transaction execution. Fraudulent policy purchases, staged accidents, and exaggerated claims can be submitted remotely with limited physical verification, increasing loss ratios and investigation costs. Insurers must invest heavily in advanced fraud detection analytics, identity verification systems, and claims monitoring tools to mitigate digital exposure. False information in online applications may bypass traditional agent scrutiny, affecting underwriting accuracy. Organized fraud rings exploit standardized online products and fast settlement expectations. Consumer demand for instant claims resolution pressures insurers to balance speed with verification rigor. Regulatory obligations on fair claims handling constrain denial or investigation actions. Digital fraud vulnerability thus imposes operational and financial challenges on the Australia online insurance market.

Opportunities

Embedded Insurance in E-Commerce and Mobility Platforms

Australia’s mature digital commerce and mobility ecosystems create opportunities for embedded insurance offerings integrated into online transactions such as travel booking, car rental, device purchase, and parcel delivery, enabling contextual coverage purchase at the point of need without separate acquisition journeys. E-commerce platforms and service providers seek value-added offerings to enhance customer experience and revenue, making them receptive partners for insurers providing API-based microinsurance products. Consumers benefit from convenience and relevance when insurance is bundled with primary purchases, increasing uptake among digitally engaged segments. Embedded offerings expand reach beyond traditional comparison channels into new transaction contexts. Insurers gain granular behavioral data improving risk selection and pricing. Partnerships with platforms enable scalable distribution with minimal marketing cost. Embedded models can convert users into broader policyholders through follow-up engagement. Embedded insurance thus represents a significant growth avenue in the Australia online insurance market.

AI-Driven Personalization and Usage-Based Insurance Expansion

Advances in telematics, data analytics, and artificial intelligence enable insurers in Australia to offer usage-based motor and personalized home insurance products aligned with individual behavior and risk profiles, enhancing differentiation within competitive online markets. Telematics-enabled policies reward safe driving and enable dynamic pricing communicated through digital platforms. Smart home data integration supports risk monitoring and preventive services for property insurance. Personalized dashboards and feedback loops increase customer engagement and retention. Data-driven underwriting improves pricing accuracy and reduces adverse selection. Consumers perceive value in fair pricing linked to behavior, encouraging online adoption. Regulatory acceptance of consent-based data use supports scalable deployment. AI-driven personalization therefore creates innovation-driven growth potential for the Australia online insurance market.

Future Outlook

The Australia online insurance market is expected to expand steadily as digital comparison culture and direct insurer platforms deepen penetration across insurance lines. Embedded insurance and AI-driven personalization will broaden product reach and differentiation. Regulatory frameworks supporting digital transactions will sustain online growth. Competition will remain intense, with pricing and user experience central to market positioning. Technological integration will continue reshaping acquisition and servicing models.

Major Players

- Insurance Australia Group

- Suncorp Group

- QBE Insurance

- Allianz Australia

- Auto & General Holdings

- Youi Insurance

- Budget Direct

- Hollard Australia

- AAMI

- NRMA Insurance

- RACQ Insurance

- RACV Insurance

- Bingle Insurance

- Coles Insurance

- Woolworths Insurance

Key Target Audience

- General insurers

- Digital insurers

- Insurance aggregators

- Investments and venture capitalist firms

- Government and regulatory bodies

- E-commerce platforms

- Automotive and mobility companies

- Fintech platforms

Research Methodology

Step 1: Identification of Key Variables

Key variables included digital gross written premiums, online policy share by line, channel distribution, and consumer digital adoption. Regulatory provisions on electronic disclosure and identity verification were mapped. Insurer digital strategy and aggregator influence were assessed.

Step 2: Market Analysis and Construction

Prudential regulator statistics, insurer reports, and industry data were synthesized to quantify online insurance premiums. Segmentation by product and channel derived from insurer and aggregator disclosures. Competitive structure assessed through digital penetration and pricing strategies.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions on comparison platform dominance, embedded insurance growth, and digital consumer behavior validated with insurance distribution and underwriting practitioners. Channel economics cross-checked with aggregator stakeholders. Iterative reconciliation ensured consistency.

Step 4: Research Synthesis and Final Output

Quantitative and qualitative insights integrated into structured sections aligned with outlook requirements. Tables standardized with verified data points. Final narrative refined for clarity and analytical coherence.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

High internet penetration and digital purchasing behavior

Mature comparison website ecosystem driving online policy sales

Insurer investment in digital direct channels and automation - Market Challenges

Price competition compressing online policy margins

Complex underwriting for high-value risks in digital channels

Customer trust and data privacy concerns - Market Opportunities

Usage-based and on-demand digital insurance products

Embedded insurance in e-commerce and mobility ecosystems

AI-driven underwriting and personalized pricing - Trends

Growth of direct-to-consumer digital insurers

Automation of claims and policy servicing - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Online Motor Insurance

Online Home and Contents Insurance

Online Health Insurance

Online Travel Insurance

Online Life Insurance - By Platform Type (In Value%)

Direct Insurer Digital Platforms

Aggregator and Comparison Websites

Mobile Insurance Applications

Broker Digital Portals

Embedded Insurance Platforms - By Fitment Type (In Value%)

Direct-to-Consumer Online

Broker-assisted Digital

Aggregator-based Distribution

Embedded Insurance - By End User Segment (In Value%)

Individual Consumers

Small and Medium Enterprises

Gig Economy Workers

- Market Share Analysis

- Cross Comparison Parameters (Product Type, Distribution Channel, Digital Platform Capability, Customer Segment Focus, Pricing Model, Underwriting Automation Level, Claims Processing Speed, Ecosystem Partnerships, Data Analytics Utilization, Customer Experience Design)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

IAG Direct Insurance

Suncorp Direct Insurance

Allianz Australia

QBE Direct Insurance

TAL Direct

AIA Australia

Zurich Australia Direct

Budget Direct Insurance

Youi Insurance

Hollard Insurance Australia

HCF Insurance

Medibank Private

Bupa Australia Insurance

NRMA Insurance Online

RACQ Insurance Online

- Consumers preferring comparison-led digital policy purchase

- SMEs adopting simple online commercial insurance products

- Gig workers seeking flexible and short-term coverage

- Affluent clients using digital channels for standard policies

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now