Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Australia semiconductor manufacturing market is valued at approximately USD ~ billion in recent assessments, primarily driven by the increasing demand for advanced chips in sectors such as automotive, telecommunications, and consumer electronics. The market is supported by heavy investments in research and development, as well as government initiatives to bolster the semiconductor production capabilities in the country. Key drivers include the rise in electric vehicle adoption and the growth of IoT devices, which require high-performance semiconductors. These factors contribute significantly to the market’s expansion and technological advancements.

Australia, particularly in cities such as Sydney and Melbourne, is home to a robust semiconductor manufacturing ecosystem, benefitting from its strong infrastructure, skilled workforce, and proximity to Asia-Pacific markets. The government’s push for self-reliance in semiconductor production and global partnerships with key industry players further strengthens the country’s dominance in the semiconductor space. Australia’s strategic location and favorable economic conditions for tech innovations position it as a significant player in the global semiconductor landscape.

Market Segmentation

By Product Type

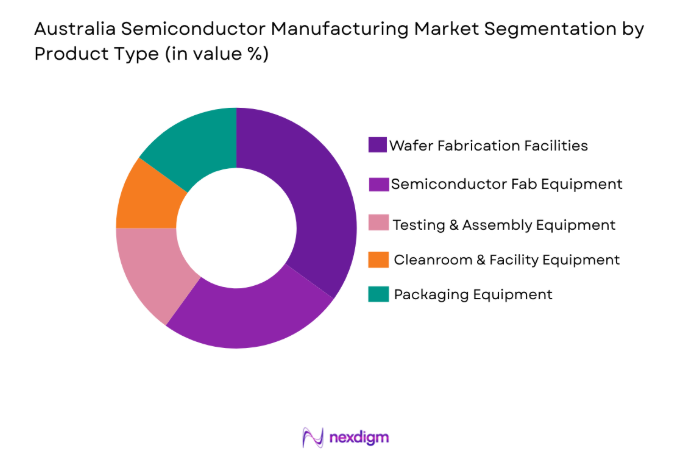

Australia semiconductor manufacturing market is segmented by product type into wafer fabrication, semiconductor fab equipment, testing and assembly equipment, cleanroom & facility equipment, and packaging equipment. Recently, wafer fabrication has a dominant market share due to its critical role in producing high-quality semiconductors required for automotive, consumer electronics, and telecommunications. Demand for smaller and faster chips, along with the adoption of cutting-edge fabrication techniques, continues to bolster the wafer fabrication segment’s growth in the Australian market.

By Platform Type

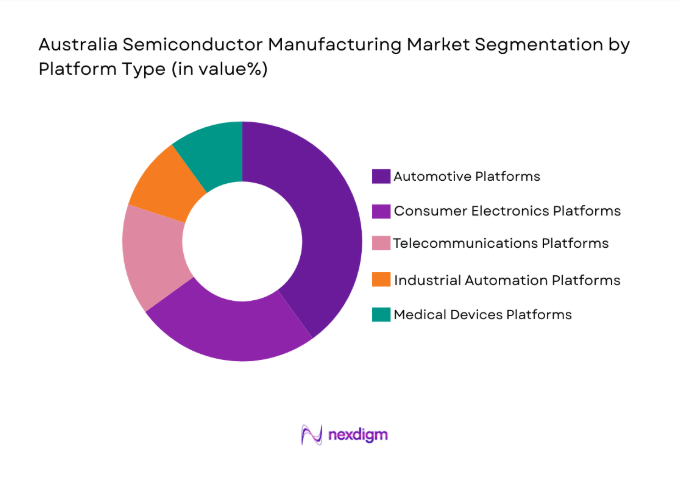

Australia semiconductor manufacturing market is segmented by platform type into automotive platforms, consumer electronics platforms, telecommunications platforms, industrial automation platforms, and medical devices platforms. Recently, automotive platforms have dominated the market share due to the increasing integration of semiconductors in electric vehicles and autonomous systems. With more automakers focusing on electric and connected vehicles, the demand for semiconductors for automotive applications has surged, making this platform type a critical area for growth in Australia.

Competitive Landscape

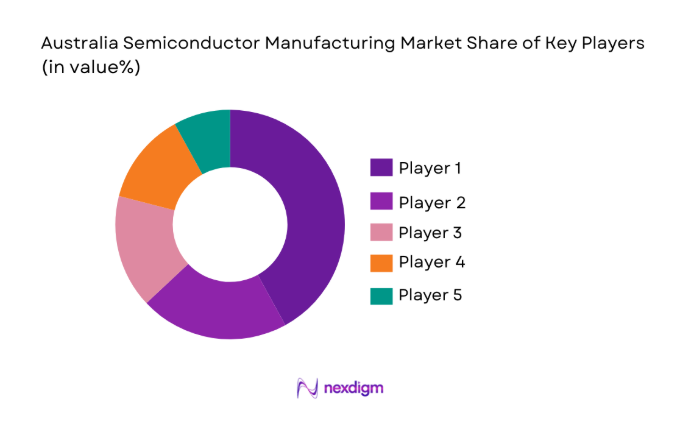

The Australian semiconductor manufacturing market is characterized by strong consolidation, with a few large players dominating the space. These companies have extensive capabilities in research, development, and production, with most key players having global reach. Technological advancements, regulatory support, and collaborations with international companies are expected to shape the competitive dynamics in the coming years. The presence of global giants and local innovators continues to drive market competition and growth, resulting in increased investments and higher production capacities across the country.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Market-Specific Parameter |

| Intel Corporation | 1968 | USA | ~ | ~ | ~ | ~ | ~ |

| TSMC | 1987 | Taiwan | ~ | ~ | ~ | ~ | ~ |

| Samsung Electronics | 1969 | South Korea | ~ | ~ | ~ | ~ | ~ |

| GlobalFoundries | 2009 | USA | ~ | ~ | ~ | ~ | ~ |

| Micron Technology | 1978 | USA | ~ | ~ | ~ | ~ | ~ |

Australia Semiconductor Manufacturing Market Analysis

Growth Drivers

Increasing Demand for Electric Vehicles

The increasing global push for clean energy and reducing carbon emissions has been a major driver in the demand for electric vehicles (EVs). Australia, with its focus on renewable energy and sustainable technologies, is witnessing an uptick in EV adoption. This, in turn, drives the demand for high-performance semiconductors required for electric vehicle components, such as power management, battery management systems, and sensors. As automakers continue to invest heavily in electric vehicle production and expand their EV lineups, the semiconductor industry stands to benefit significantly. The Australian market is expected to see increased production and sales of EV-related semiconductors, which are pivotal to their high performance. Given Australia’s clean energy strategy, the role of semiconductors in supporting the transition to electric vehicles will be crucial. Electric vehicles are expected to continue driving the growth of the semiconductor manufacturing market in Australia over the coming years.

Rise in IoT Devices

The proliferation of the Internet of Things (IoT) is another critical growth driver for the semiconductor manufacturing market in Australia. IoT devices, ranging from consumer electronics to industrial automation systems, are becoming integral to modern life. These devices require specialized semiconductor chips for their sensors, connectivity, and processing needs. With Australia’s growing adoption of smart cities, smart homes, and industrial IoT systems, the demand for semiconductors will increase significantly. The Australian market is witnessing a shift towards next-generation IoT devices that rely heavily on semiconductor advancements, driving the expansion of the semiconductor manufacturing industry. As businesses across sectors adopt IoT solutions to enhance operational efficiency and customer engagement, the need for high-performance semiconductors will continue to soar, creating significant growth opportunities for the semiconductor industry in Australia.

Market Challenges

High Capital Investment in Semiconductor Production

One of the major challenges facing the semiconductor manufacturing market in Australia is the high capital investment required for establishing state-of-the-art semiconductor fabs and research centers. Semiconductor manufacturing involves expensive infrastructure, advanced technology, and specialized workforce training. Establishing these capabilities in Australia requires significant upfront capital, which can be a barrier to entry for many companies. The market also faces challenges related to the costs of maintaining and upgrading fabrication facilities, as the technology continues to advance. Despite the long-term potential for growth in the semiconductor market, high capital investment remains a critical challenge, as companies must secure funding or partnerships to remain competitive in the global market. To overcome this challenge, there needs to be a strong push for government support and private sector investment in the sector.

Supply Chain Vulnerabilities

The Australian semiconductor manufacturing market also faces supply chain vulnerabilities, especially regarding raw materials and key components used in the production process. Semiconductor production relies on specialized materials such as silicon, rare earth metals, and other high-grade raw materials. The global semiconductor supply chain has been under strain due to geopolitical tensions, trade restrictions, and environmental challenges, which have affected material availability. Australia, being heavily reliant on imports for these materials, faces significant supply chain risks, which can disrupt production timelines and increase costs. Furthermore, the limited number of suppliers and manufacturers in Australia further exacerbates the challenge. To mitigate these risks, diversification of supply sources and strengthening of local manufacturing capabilities will be essential for the market’s long-term sustainability.

Opportunities

Government Support and Research Investments

The Australian government’s support for high-tech industries and its focus on innovation in the semiconductor sector present substantial opportunities for market growth. Government funding for research and development (R&D) in semiconductor technologies can facilitate advancements in the field, especially in areas like quantum computing and AI-powered semiconductor devices. Several initiatives, such as grants and tax incentives, are designed to promote innovation and attract investment in the sector. Australia’s focus on increasing domestic semiconductor production and its growing R&D capabilities are expected to strengthen the local market and reduce reliance on international suppliers. These government-backed opportunities can drive substantial growth in the semiconductor manufacturing market over the next few years.

Growth of Data Centers and Cloud Computing

The expansion of data centers and the growing reliance on cloud computing services are key opportunities for the Australian semiconductor manufacturing market. As businesses continue to digitize and adopt cloud-based solutions, the demand for powerful semiconductors that support data storage, processing, and transmission will rise. The Australian market is increasingly seeing investment in large-scale data centers that require advanced semiconductor components to handle vast amounts of data efficiently. With the ongoing growth in cloud computing, particularly in sectors like finance, healthcare, and telecommunications, the semiconductor industry in Australia will see an uptick in demand for components like processors, memory chips, and networking equipment. This shift towards cloud infrastructure presents a lucrative opportunity for the semiconductor manufacturing sector, boosting both local production and exports.

Future Outlook

The Australian semiconductor manufacturing market is poised for significant growth in the next five years, driven by technological innovations in semiconductor fabrication, increasing demand for electric vehicles, and advancements in IoT and AI technologies. The market will benefit from government support in R&D and investment in domestic production capabilities. Technological developments such as 5G and the growth of cloud computing will further fuel the demand for high-performance semiconductors. With continued investments and strategic initiatives in place, Australia is expected to solidify its position as a key player in the global semiconductor industry.

Major Players

- Intel Corporation

- TSMC

- Samsung Electronics

- GlobalFoundries

- Micron Technology

- Broadcom

- Qualcomm

- Texas Instruments

- NXP Semiconductors

- STMicroelectronics

- Infineon Technologies

- Analog Devices

- ASML

- Applied Materials

- KLA Corporation

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Semiconductor manufacturers

- OEMs in automotive and electronics

- Cloud service providers

- Telecommunications firms

- Industrial automation companies

Research Methodology

Step 1: Identification of Key Variables

Identification of key market drivers, trends, and challenges based on secondary research, expert opinions, and industry reports.

Step 2: Market Analysis and Construction

Analysis of historical data and market forecasts to construct a detailed market model considering various product and platform segments.

Step 3: Hypothesis Validation and Expert Consultation

Validation of the market model through interviews with industry experts, key stakeholders, and market participants.

Step 4: Research Synthesis and Final Output

Synthesis of data into actionable insights and the creation of the final report, ensuring accuracy and consistency in market forecasts.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increasing Demand for Electric Vehicles

Rising Need for Advanced Telecommunication Networks

Growth of Consumer Electronics and Wearables

Government Investment in R&D for Semiconductor Technologies

Expansion of Industrial Automation - Market Challenges

High Capital Investment for Semiconductor Fabrication

Complexity in Manufacturing Processes and Technology Integration

Supply Chain Disruptions and Component Shortages

Intense Global Competition in Semiconductor Production

Regulatory and Environmental Constraints - Market Opportunities

Expansion of Semiconductor Manufacturing Ecosystem in Australia

Growing Demand for IoT and Edge Computing Solutions

Investment in Semiconductor Research and Innovation - Trends

Adoption of AI and Machine Learning in Semiconductor Design

Increased Focus on Sustainable Semiconductor Manufacturing - Government Regulations

Data Protection and Privacy Regulations

Export Control and Compliance Policies

Government Funding and Grants for Semiconductor R&D - SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Semiconductor Fab Equipment

Wafer Fabrication

Testing & Assembly Equipment

Cleanroom & Facility Equipment

Packaging Equipment - By Platform Type (In Value%)

Automotive Platforms

Consumer Electronics Platforms

Telecommunications Platforms

Industrial Automation Platforms

Medical Devices Platforms - By Fitment Type (In Value%)

On-site Solutions

Outsourced Solutions

Integrated Solutions

Modular Solutions - By End User Segment (In Value%)

Semiconductor Manufacturers

Original Equipment Manufacturers (OEMs)

Tier-1 Suppliers

Distributors

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type, Technology Integration, Supply Chain Efficiency)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Intel Corporation

TSMC

Samsung Electronics

GlobalFoundries

Micron Technology

Broadcom

Qualcomm

Texas Instruments

NXP Semiconductors

STMicroelectronics

Infineon Technologies

Analog Devices

ASML

Applied Materials

KLA Corporation

- Semiconductor Manufacturers’ Adoption of Advanced Materials

- OEMs’ Focus on Miniaturization and Efficiency in Components

- OEMs’ Shift Towards Custom Semiconductor Solutions

- Increased Collaboration Between Government and Industry Players

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now