Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Australia Telemedicine Market was valued at approximately USD ~ billion, driven by the increasing adoption of digital health solutions and the rising demand for remote healthcare services. This growth is primarily attributed to expanding broadband infrastructure, government-backed telehealth initiatives, and the growing need for accessible healthcare in both metropolitan and remote regions. The market is further supported by healthcare providers’ investment in teleconsultation and remote patient monitoring platforms, contributing to the significant increase in telemedicine adoption.

The dominant cities such as Sydney, Melbourne, and Brisbane lead the market due to their advanced healthcare infrastructures and widespread access to high-speed internet. These cities benefit from well-established hospital networks that are integrating telemedicine technologies into their services. Regional areas also show substantial growth in telemedicine adoption as healthcare providers work to bridge the gap in service availability through virtual consultations, ensuring more inclusive healthcare access across Australia.

Market Segmentation

By Product Type

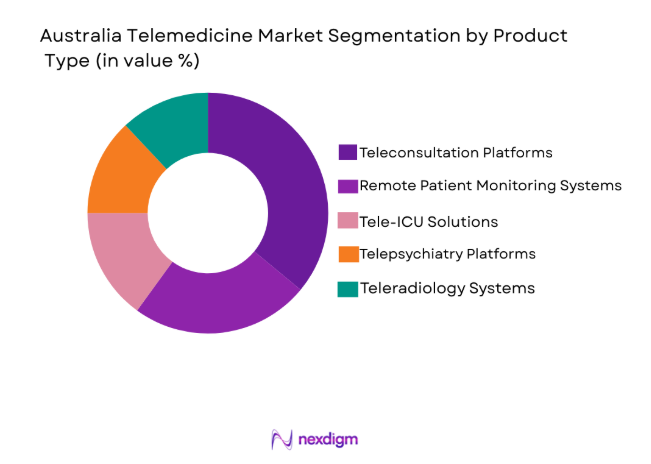

Australia Telemedicine market is segmented by product type into Teleconsultation Platforms, Remote Patient Monitoring Systems, Tele-ICU Solutions, Telepsychiatry Platforms, and Teleradiology Systems. Recently, Teleconsultation Platforms has a dominant market share due to widespread adoption by hospitals, private clinics, and digital healthcare providers. Demand patterns strongly favor real time doctor patient communication platforms supported by secure digital infrastructure and government funded virtual care initiatives. Large healthcare providers increasingly integrate teleconsultation within hospital workflows, while private practitioners rely on these platforms for patient reach expansion. Infrastructure availability, strong broadband penetration, and consumer preference for convenient healthcare access further reinforce the dominance of teleconsultation services across Australia’s telemedicine ecosystem.

By Platform Type

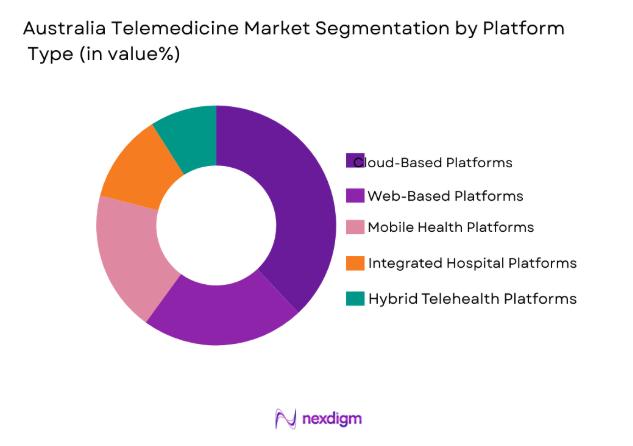

Australia Telemedicine market is segmented by platform type into Cloud-Based Platforms, Web-Based Platforms, Mobile Health Platforms, Integrated Hospital Platforms, and Hybrid Telehealth Platforms. Recently, Cloud-Based Platforms has a dominant market share due to scalability, healthcare data accessibility, and rapid integration across hospital networks and digital health providers. Healthcare institutions increasingly adopt cloud architecture to enable secure patient record management, video consultation delivery, and remote monitoring data processing. Cloud infrastructure allows telemedicine providers to expand services nationwide without heavy physical IT investment. Consumer preference for mobile accessibility and healthcare provider demand for interoperable systems further strengthen adoption of cloud enabled telehealth platforms across Australia’s healthcare ecosystem.

Competitive Landscape

The Australia telemedicine market shows moderate consolidation with a combination of telecommunications companies, digital health technology providers, and healthcare platform developers competing for market presence. Major players influence platform development, healthcare integration capabilities, and nationwide telehealth deployment. Partnerships between hospital networks and technology providers accelerate innovation in remote patient monitoring, teleconsultation infrastructure, and digital health record management, strengthening competitive intensity while encouraging rapid technological adoption across the healthcare ecosystem.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Telehealth Capability |

| Telstra Health | 2013 | Melbourne | ~ | ~ | ~ | ~ | ~ |

| Coviu | 2018 | Sydney | ~ | ~ | ~ | ~ | ~ |

| Healthdirect Australia | 2006 | Sydney | ~ | ~ | ~ | ~ | ~ |

| GlobalMed | 2002 | Arizona | ~ | ~ | ~ | ~ | ~ |

| Amwell | 2006 | Boston | ~ | ~ | ~ | ~ | ~ |

Australia Telemedicine Market Analysis

Growth Drivers

Expansion of National Digital Health Infrastructure and Broadband Connectivity

Australia’s rapidly expanding digital healthcare infrastructure significantly strengthens the telemedicine ecosystem by enabling seamless virtual healthcare delivery across metropolitan and rural regions. The widespread availability of high speed broadband networks and mobile internet access allows teleconsultation platforms to operate reliably across geographically dispersed communities. Government supported digital health initiatives promote interoperability between hospitals, healthcare providers, and telehealth platforms, allowing electronic health records and remote consultations to function efficiently. Hospitals increasingly integrate telemedicine into routine care pathways to improve patient access and reduce physical hospital congestion. Telecommunication providers also collaborate with healthcare institutions to deploy secure healthcare data transmission systems and virtual care infrastructure. These developments enable healthcare providers to monitor patients remotely while improving healthcare access for individuals living in remote or underserved regions. Continuous infrastructure investments across Australia’s healthcare and digital communication sectors therefore remain a fundamental driver accelerating telemedicine adoption nationwide.

Rising Demand for Accessible and Remote Healthcare Services

Growing demand for convenient healthcare access across Australia strongly accelerates telemedicine adoption among hospitals, private healthcare providers, and patients. The country’s large geographic landscape creates barriers for patients living in remote communities who must travel long distances for specialized medical care. Telemedicine enables healthcare providers to deliver consultations, diagnostics, and follow up care without requiring physical hospital visits. Increasing prevalence of chronic health conditions further increases the need for continuous patient monitoring and frequent physician interaction. Remote patient monitoring systems and teleconsultation platforms therefore become essential tools for improving patient outcomes and reducing healthcare system pressure. Patients also increasingly prefer virtual healthcare appointments due to convenience, reduced waiting time, and improved scheduling flexibility. Healthcare institutions recognize these advantages and actively integrate telehealth services into standard clinical workflows. As patient awareness and digital healthcare acceptance continue expanding, telemedicine demand across Australia’s healthcare system continues to grow substantially.

Market Challenges

Data Privacy and Healthcare Cybersecurity Concerns in Digital Healthcare Platforms

Telemedicine platforms operate through extensive digital data exchange systems that store and transmit highly sensitive patient information including medical records, diagnostic reports, and consultation histories. Protecting this data presents a major operational challenge for telemedicine providers across Australia. Healthcare organizations must comply with strict national healthcare privacy regulations while simultaneously maintaining secure digital platforms capable of handling large volumes of patient data. Cybersecurity threats such as data breaches, unauthorized access, and digital system vulnerabilities create significant risks for healthcare institutions deploying telemedicine technologies. Healthcare providers therefore require continuous investment in encryption systems, secure authentication protocols, and advanced cybersecurity infrastructure. Implementing these security measures increases operational costs and technical complexity for telemedicine providers. Patient trust in digital healthcare platforms also depends heavily on data protection reliability. Any cybersecurity incident can negatively impact platform credibility and discourage telemedicine adoption. Consequently, maintaining secure healthcare data systems remains a critical operational challenge across the telemedicine market.

Regulatory Compliance Complexity in Virtual Healthcare Delivery Systems

Telemedicine services operate within complex regulatory frameworks designed to protect patient safety, medical practice standards, and digital health data security. Healthcare providers must comply with licensing requirements, medical practice regulations, and healthcare privacy legislation when offering telemedicine services across different Australian states. Regulatory complexity increases when telemedicine platforms deliver services across multiple jurisdictions with varying healthcare practice guidelines. Healthcare providers must also ensure that teleconsultation platforms meet strict clinical safety standards and digital healthcare compliance requirements. Meeting these regulatory obligations often requires specialized legal expertise and administrative oversight. Compliance procedures can increase implementation timelines for telemedicine platforms and discourage smaller healthcare providers from adopting digital healthcare technologies. Telemedicine companies must also adapt to evolving healthcare regulations as governments update digital health policies and patient protection standards. These regulatory complexities create operational uncertainty and increase administrative burdens for telemedicine providers operating within Australia’s healthcare system.

Opportunities

Expansion of Telemedicine Services into Rural and Remote Healthcare Delivery

Australia’s large geographic landscape creates a strong opportunity for telemedicine providers to expand services across rural and remote healthcare markets. Many communities located far from metropolitan hospitals experience limited access to specialized healthcare professionals and advanced medical services. Telemedicine platforms enable physicians and specialists to deliver consultations, diagnostic evaluations, and treatment guidance remotely without requiring patient travel. Healthcare systems increasingly recognize telemedicine as an effective strategy for improving healthcare accessibility while reducing transportation related healthcare barriers. Governments also support rural telehealth deployment through funding programs and digital health infrastructure development. Hospitals and regional clinics collaborate with telemedicine technology providers to expand remote care networks. These initiatives improve healthcare coverage while reducing hospital overcrowding in urban centers. As digital healthcare infrastructure continues expanding nationwide, telemedicine providers gain significant opportunities to deliver specialized medical services across underserved communities throughout Australia.

Integration of Artificial Intelligence and Remote Monitoring Technologies in Telehealth Platforms

The integration of advanced technologies such as artificial intelligence and remote patient monitoring systems creates new opportunities for telemedicine service expansion. AI powered diagnostic tools allow healthcare providers to analyze medical data, imaging results, and patient symptoms more efficiently during virtual consultations. Remote monitoring devices enable continuous tracking of patient health indicators including heart rate, glucose levels, and blood pressure without requiring hospital visits. Healthcare providers increasingly incorporate these technologies into telemedicine platforms to improve clinical decision making and enhance patient care outcomes. Artificial intelligence also assists healthcare professionals by supporting clinical workflow automation and predictive healthcare analytics. These technologies strengthen telemedicine platform capabilities while improving healthcare delivery efficiency. Hospitals and digital health providers actively invest in AI enabled telehealth solutions to enhance remote care services. Technological innovation therefore presents substantial opportunities for telemedicine market growth and healthcare transformation across Australia.

Future Outlook

The Australia telemedicine market is expected to experience continued expansion driven by technological innovation, digital healthcare infrastructure investment, and growing acceptance of virtual healthcare services. Hospitals and healthcare providers increasingly integrate telehealth solutions into standard clinical workflows to improve accessibility and efficiency. Advancements in artificial intelligence driven diagnostics, remote patient monitoring technologies, and cloud healthcare platforms will further enhance telemedicine capabilities. Supportive digital health policies and government initiatives will also encourage broader telehealth adoption across healthcare systems.

Major Players

- Telstra Health

- Coviu

- Healthdirect Australia

- GlobalMed

- Amwell

- Medibank

- DoctorDoctor

- Intelehealth

- Philips Healthcare

- Siemens Healthineers

- Cisco Systems

- Oracle Health

- Athenahealth

- Allscripts Healthcare Solutions

- CareMonitor

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Hospitals and healthcare providers

- Telemedicine platform developers

- Digital healthcare technology companies

- Healthcare insurance companies

- Telecommunications infrastructure providers

Research Methodology

Step 1: Identification of Key Variables

Market variables such as digital healthcare infrastructure, teleconsultation adoption, healthcare expenditure, and telemedicine platform deployment were identified. These variables were mapped against healthcare system dynamics and digital technology penetration across Australia’s healthcare ecosystem.

Step 2: Market Analysis and Construction

Market structure was developed using healthcare infrastructure datasets, digital health adoption statistics, telecommunication network coverage data, and company level information from healthcare technology providers operating in telemedicine services.

Step 3: Hypothesis Validation and Expert Consultation

Healthcare industry specialists, telehealth platform developers, and hospital administrators were consulted to validate telemedicine demand drivers, adoption patterns, and healthcare technology deployment strategies across metropolitan and regional healthcare markets.

Step 4: Research Synthesis and Final Output

All quantitative datasets and qualitative insights were synthesized into structured market analysis. Industry data, healthcare infrastructure information, and technology adoption patterns were consolidated to generate the final telemedicine market assessment.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising Demand for Remote Healthcare

Government Support for Telemedicine Adoption

Technological Advancements in Telecommunication

Increasing Healthcare Costs

Growth of Chronic Disease Management - Market Challenges

Data Privacy and Security Concerns

Regulatory Barriers in Telemedicine Adoption

Limited Infrastructure in Remote Areas

High Initial Investment Costs - Market Opportunities

Integration of Artificial Intelligence in Telemedicine

Expansion of Telemedicine Services in Rural Regions

Increase in Adoption of Telehealth in Post-pandemic Healthcare Systems - Trends

Growth of Virtual Care Models

Shift Towards Preventive Healthcare Solutions - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Teleconsultation Systems

Remote Patient Monitoring Systems

Telehealth Platforms

Mobile Health Applications

Tele-radiology Systems - By Platform Type (In Value%)

Cloud-Based Platforms

On-premise Platforms

Hybrid Platforms

Mobile Platforms

Web-Based Platforms - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Integrated Solutions

Modular Solutions - By End User Segment (In Value%)

Healthcare Providers

Telemedicine Providers

Healthcare Insurers

Patients

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, End User Segment, Fitment Type, Market Value, Installed Units, Average System Price)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Telstra Health

HealthDirect Australia

Medibank

Bendigo and Adelaide Bank

DoctorLink

Coviu

Flare Health

DocMed

Specialist Medical Services

eHealth NSW

Phoenix Medical Solutions

Ramsay Pharmacy

GlobalMed

InteleHealth

Amwell

- Healthcare Providers’ Increasing Investment in Telemedicine

- Telemedicine Providers’ Role in Expanding Access to Healthcare

- Healthcare Insurers’ Shift Towards Telemedicine Coverage

- Patients’ Adoption of Telemedicine Services

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now