Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Brazil Agricultural Hydraulic Systems market is valued at approximately USD ~billion based on a recent historical assessment, driven by mechanization intensity in soybean, corn, and sugarcane cultivation and sustained replacement demand for hydraulic components in high-horsepower tractors and harvesters. Industry data from Brazil agricultural machinery associations and global hydraulics manufacturers indicates strong equipment production volumes and hydraulic system integration rates across OEM platforms, supporting stable aftermarket consumption and localized assembly activities in major agricultural states.

Dominant regions include São Paulo, Paraná, Rio Grande do Sul, and Mato Grosso due to concentrated agricultural machinery manufacturing clusters, advanced farming operations, and established distribution and service infrastructure. These states host major OEM assembly plants and hydraulic component suppliers while large-scale grain and sugarcane farming creates sustained demand for high-capacity hydraulic systems. Export-oriented agribusiness operations and logistics connectivity further reinforce regional equipment modernization and technology adoption.

Market Segmentation

By Product Type:

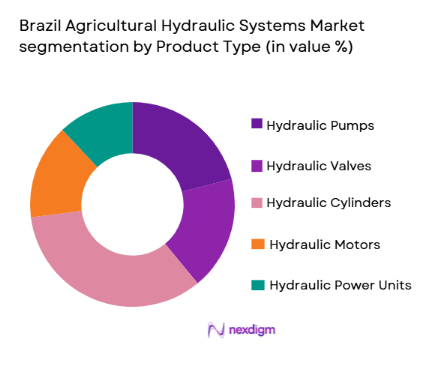

Brazil Agricultural Hydraulic Systems market is segmented by product type into hydraulic pumps, hydraulic valves, hydraulic cylinders, hydraulic motors, and hydraulic power units. Recently, hydraulic cylinders has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Hydraulic cylinders dominate because they are core actuators in tractors, harvesters, and implements, experiencing continuous mechanical load cycles during lifting, steering, and implement control operations. Brazilian farming practices rely heavily on hydraulic lifting and positioning systems for plowing, seeding, spraying, and harvesting, increasing replacement frequency compared to other components. OEM design standardization around cylinder-based actuation also ensures large production volumes. Additionally, harsh field conditions accelerate seal wear and rod damage, generating steady aftermarket demand across agricultural regions with intensive cropping operations.

By Platform Type:

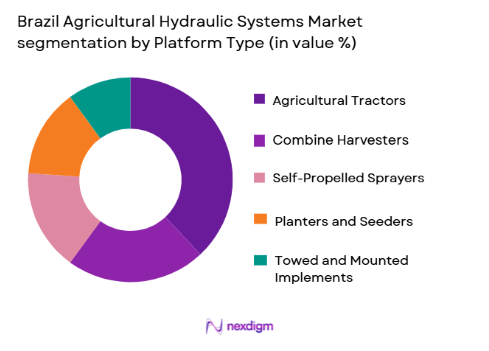

Brazil Agricultural Hydraulic Systems market is segmented by platform type into agricultural tractors, combine harvesters, self-propelled sprayers, planters and seeders, and towed and mounted implements. Recently, agricultural tractors has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Agricultural tractors dominate hydraulic system consumption because they serve as primary power platforms across virtually all Brazilian crop systems including soybean, corn, and sugarcane cultivation. Modern tractors integrate multiple hydraulic circuits for steering, transmission control, hitch actuation, and implement power delivery. Continuous tractor fleet expansion and horsepower upgrades increase hydraulic complexity and component count per unit. Tractors also exhibit high operating hours annually, accelerating wear of hydraulic components and sustaining aftermarket demand across farming regions with mechanized large-scale agriculture.

Competitive Landscape

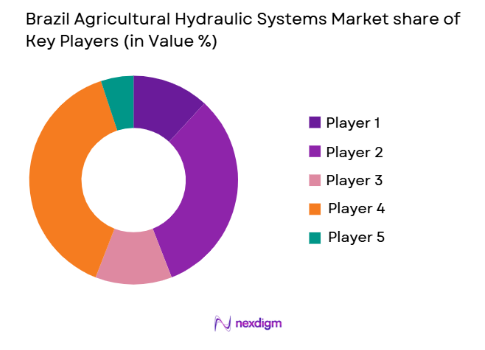

Brazil Agricultural Hydraulic Systems market exhibits moderate consolidation with global hydraulics manufacturers supplying OEM agricultural machinery producers and strong aftermarket networks across key farming states. Multinational firms dominate advanced electrohydraulic and high-pressure components while regional distributors and local assemblers support service, customization, and replacement demand. Partnerships with agricultural equipment OEMs influence technology standards and procurement volumes, reinforcing the presence of established global brands with localized manufacturing and distribution capabilities.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Agricultural OEM Integration |

| Bosch Rexroth | 1795 | Germany | ~ | ~ | ~ | ~ | ~ |

| Parker Hannifin | 1917 | USA | ~ | ~ | ~ | ~ | ~ |

| Danfoss Power Solutions | 1968 | Denmark | ~ | ~ | ~ | ~ | ~ |

| Eaton | 1911 | Ireland | ~ | ~ | ~ | ~ | ~ |

| HYDAC | 1963 | Germany | ~ | ~ | ~ | ~ | ~ |

Brazil Agricultural Hydraulic Systems Market Analysis

Growth Drivers

Expansion of High-Horsepower Agricultural Machinery Fleet:

Brazilian agriculture increasingly relies on large-scale mechanized farming systems requiring tractors and harvesters exceeding 200 horsepower, substantially increasing hydraulic system complexity and component demand per unit. High-horsepower platforms integrate multiple hydraulic circuits for transmission control, implement actuation, steering, and precision agriculture interfaces, expanding pump, valve, and cylinder requirements. Agricultural modernization programs and export-driven crop production incentivize farmers to upgrade machinery fleets toward higher capacity equipment. OEM manufacturers respond by introducing hydraulically intensive models optimized for tropical cropping conditions. Larger machines operate longer hours annually across vast farmland areas, accelerating wear of hydraulic components. This combination of fleet expansion and higher hydraulic intensity per machine structurally increases both OEM installation volumes and aftermarket replacement demand across Brazil’s agricultural regions.

Adoption of Precision Agriculture and Electrohydraulic Control Systems:

Precision agriculture adoption in Brazil requires accurate implement positioning, variable-rate application, and automated machine control, all enabled by electrohydraulic actuation systems. Modern planters, sprayers, and tractors incorporate sensors, electronic control units, and proportional hydraulic valves to enable real-time adjustments based on soil, crop, and terrain data. Hydraulic systems therefore transition from purely mechanical actuation to digitally controlled platforms integrated with GPS guidance and telematics. Equipment OEMs increasingly standardize electrohydraulic architectures across product lines, raising component value and sophistication. Farmers benefit from yield optimization and input efficiency, encouraging technology adoption. This shift toward precision-controlled hydraulics increases demand for advanced valves, pumps, and actuators and expands aftermarket service requirements for electronic-hydraulic integration across Brazil’s mechanized agriculture sector.

Market Challenges

Dependence on Imported High-Precision Hydraulic Components:

Brazil Agricultural Hydraulic Systems market relies heavily on imported high-precision pumps, valves, and electrohydraulic controls due to limited domestic manufacturing capability for advanced fluid power technology. Currency volatility increases procurement costs for OEMs and distributors importing components from Europe and North America. Supply chain disruptions or trade barriers can delay agricultural machinery production and maintenance activities. Domestic farmers face higher equipment and replacement costs when import prices rise. Local manufacturing initiatives remain constrained by technological gaps and investment requirements. This dependence reduces pricing stability and supply resilience within the agricultural hydraulics ecosystem. Market participants must balance localization efforts with global sourcing to maintain competitiveness in Brazil’s price-sensitive agricultural equipment market.

Harsh Operating Conditions Causing Accelerated Hydraulic Wear:

Brazilian agricultural machinery operates in demanding tropical environments characterized by dust, humidity, crop residue, and heavy load cycles that accelerate hydraulic component degradation. Contamination of hydraulic fluids and mechanical stress on cylinders and seals increases failure frequency compared to temperate farming regions. Remote farmland locations limit timely maintenance and skilled servicing, prolonging equipment downtime. Frequent repairs raise operating costs for farmers and contractors. OEMs must design hydraulics with higher durability standards, increasing production costs. Aftermarket distributors face logistical challenges supplying replacement parts across vast agricultural regions. These harsh conditions therefore elevate lifecycle costs and reliability challenges across the Brazil Agricultural Hydraulic Systems market.

Opportunities

Localization of Agricultural Hydraulic Component Manufacturing:

Brazil presents significant opportunity for localized production of agricultural hydraulic components to reduce import dependence and improve supply chain resilience. Government industrial policies and agricultural machinery financing programs encourage domestic manufacturing investment. Establishing local facilities for pumps, cylinders, and valves can lower costs through reduced logistics and currency exposure. OEM manufacturers benefit from shorter lead times and customized design capabilities suited to Brazilian farming conditions. Domestic production also supports aftermarket availability across rural regions. Partnerships between global hydraulics firms and Brazilian industrial groups can accelerate technology transfer and capacity development. Localization therefore offers strategic advantages in pricing stability, market access, and competitive positioning within Brazil Agricultural Hydraulic Systems market.

Integration of Smart Sensors and Predictive Maintenance in Hydraulic Systems:

The integration of sensors and digital monitoring into agricultural hydraulic systems creates opportunities for predictive maintenance and performance optimization in Brazil’s mechanized farming sector. Smart hydraulics can monitor pressure, temperature, and fluid quality to detect early signs of wear or contamination. Telematics-enabled machinery allows remote diagnostics and maintenance scheduling, reducing downtime during critical planting and harvesting periods. OEMs and service providers can offer value-added maintenance contracts based on real-time hydraulic health data. Farmers benefit from improved equipment reliability and lifecycle cost reduction. Adoption of Industry 4.0 technologies in agricultural machinery therefore expands the value proposition of advanced hydraulic systems and supports long-term growth in Brazil Agricultural Hydraulic Systems market.

Future Outlook

Brazil Agricultural Hydraulic Systems market is expected to expand steadily driven by continued mechanization of large-scale farming and adoption of precision agriculture technologies. Increasing horsepower of tractors and harvesters will raise hydraulic complexity and component value per machine. Localization initiatives and smart electrohydraulic integration will improve supply resilience and technological capability. Regulatory focus on machinery safety and environmental compliance will influence hydraulic design standards. Sustained agricultural export demand will continue to support equipment modernization and aftermarket replacement cycles.

Major Players

- Bosch Rexroth

- Parker Hannifin

- Danfoss Power Solutions

- Eaton

- HYDAC

- Bucher Hydraulics

- Casappa

- Bondioli & Pavesi

- Walvoil

- Kawasaki Precision Machinery

- Hawe Hydraulik

- Sun Hydraulics

- HydraForce

- Linde Hydraulics

- Poclain Hydraulics

Key Target Audience

- Agricultural machinery OEM manufacturers

- Hydrauliccomponent distributors

- Farm equipment dealers

- Agricultural contractors and service providers

- Agribusiness machinery leasing companies

- Investments and venture capitalist firms

- Government and regulatory bodies

- Precision agriculture technology providers

Research Methodology

Step 1: Identification of Key Variables

Demand drivers, machinery production volumes, hydraulic component integration rates, and aftermarket replacement cycles were identified through industry publications, agricultural machinery associations, and manufacturer disclosures.

Step 2: Market Analysis and Construction

Market size estimation combined OEM hydraulic system value per machinery unit with installed fleet size and replacement frequency across major Brazilian agricultural regions and equipment categories.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultation with hydraulic component suppliers, agricultural equipment distributors, and technical service professionals operating within Brazil’s mechanized farming sector.

Step 4: Research Synthesis and Final Output

Data triangulation and consistency checks were applied to produce structured insights on market segmentation, competitive dynamics, and technological trends within Brazil Agricultural Hydraulic Systems market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising mechanization across large-scale soybean and corn farming

Expansion of precision agriculture requiring advanced hydraulics

Increased demand for high-capacity harvesting and spraying equipment

Growth in agricultural exports driving equipment upgrades

Adoption of automation-ready electrohydraulic platforms - Market Challenges

High import dependence for advanced hydraulic components

Exposure to currency volatility affecting system costs

Limited local technical servicing capabilities in rural regions

Wear and contamination issues in harsh field conditions

Price sensitivity among mid-size farm operators - Market Opportunities

Localization of hydraulic component manufacturing in Brazil

Integration of smart sensors into hydraulic systems

Retrofit demand from aging agricultural machinery fleets - Trends

Shift toward electrohydraulic and digitally controlled systems

Adoption of load-sensing hydraulics in high-horsepower tractors

Integration of hydraulics with precision farming technologies

Growth of modular hydraulic kits for implement upgrades

Increasing durability standards for tropical operating environments - Government Regulations & Defense Policy

Brazil NR-12 machinery safety compliance requirements

IBAMA environmental regulations affecting hydraulic fluids

BNDES financing incentives for locally manufactured machinery - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Hydraulic Pumps

Hydraulic Valves

Hydraulic Cylinders

Hydraulic Motors

Hydraulic Power Units - By Platform Type (In Value%)

Agricultural Tractors

Combine Harvesters

Self-Propelled Sprayers

Planters and Seeders

Towed and Mounted Implements - By Fitment Type (In Value%)

OEM Factory Installed Systems

Aftermarket Retrofit Kits

Replacement Hydraulic Components

Integrated Hydraulic Modules

Modular Add-on Systems - By EndUser Segment (In Value%)

Large Commercial Farms

Mid-Size Mechanized Farms

Agricultural Contractors

Farming Cooperatives

Agricultural Equipment OEMs - By Procurement Channel (In Value%)

Direct OEM Supply Agreements

Authorized Distributor Networks

Regional Equipment Dealers

Online Industrial Marketplaces

Cooperative Purchasing Programs - By Material / Technology (in Value %)

Electrohydraulic Control Systems

Load-Sensing Hydraulic Systems

Variable Displacement Technology

High-Pressure Steel Hydraulics

Corrosion-Resistant Coated Components

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Product Range Depth, Pressure Rating Capability, Electrohydraulic Integration, Local Manufacturing Presence, Distribution Network Strength, OEM Partnerships, Customization Capability, Aftermarket Support, Pricing Tier, Technology Innovation)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Bosch Rexroth

Parker Hannifin

Eaton

Danfoss Power Solutions

HYDAC

Bucher Hydraulics

Casappa

Bondioli & Pavesi

Walvoil

Kawasaki Precision Machinery

Hawe Hydraulik

Sun Hydraulics

HydraForce

Linde Hydraulics

Poclain Hydraulics

- Large farms prioritizing high-efficiency hydraulic automation

- Contractors demanding durable high-cycle hydraulic systems

- Cooperatives standardizing hydraulic components across fleets

- OEMs integrating advanced hydraulics into new machinery lines

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now