Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Brazil agricultural tractor market reached approximately USD ~billion based on a recent historical assessment supported by national agricultural machinery industry association data and international farm equipment trade statistics. Demand is driven by expansion of mechanized soybean and corn production systems, replacement of aging tractor fleets, and increased adoption of higher horsepower machinery for large-scale agribusiness operations. Government-supported rural credit programs and subsidized financing for mechanization also sustain equipment procurement across commercial farming regions.

Dominant production and consumption centers include São Paulo, Paraná, Rio Grande do Sul, and Mato Grosso due to extensive soybean, sugarcane, and grain cultivation supported by export-oriented agribusiness infrastructure. These regions host major tractor manufacturing plants, dealer networks, and service ecosystems that reinforce equipment availability and lifecycle support. Favorable logistics corridors, large contiguous farmland holdings, and mechanized crop systems create sustained demand for high-capacity agricultural tractors across these states.

Market Segmentation

By Product Type:

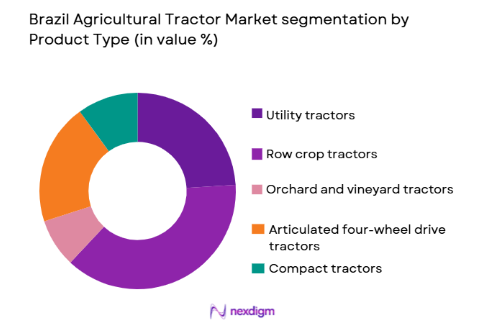

Brazil Agricultural Tractor market is segmented by product type into utility tractors, row crop tractors, orchard and vineyard tractors, articulated four-wheel drive tractors, and compact tractors. Recently, row crop tractors have a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. These tractors are extensively used in soybean, corn, and cotton cultivation across large mechanized farms, offering optimal horsepower ranges and adaptability to precision agriculture technologies. Their compatibility with modern implements and auto-guidance systems aligns with Brazil’s large-scale monocropping practices. Strong domestic manufacturing by global OEMs ensures availability, financing support, and service networks, reinforcing adoption among agribusiness producers and commercial farming operations.

By Horsepower Range:

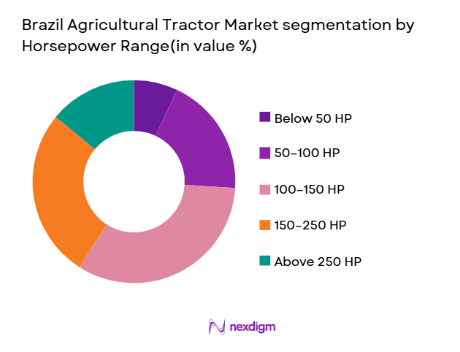

Brazil Agricultural Tractor market is segmented by horsepower range into below 50 HP, 50–100 HP, 100–150 HP, 150–250 HP, and above 250 HP. Recently, 100–150 HP has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. This horsepower class balances versatility and power required for row cropping, tillage, and transport across medium and large farms. It supports precision farming attachments and offers fuel efficiency suitable for long operational hours. OEM product portfolios and financing programs heavily focus on this range, aligning with mechanization levels and crop systems prevalent in major Brazilian agricultural regions.

Competitive Landscape

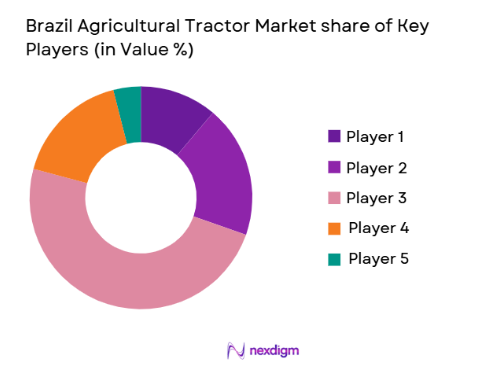

Brazil agricultural tractor market exhibits a moderately consolidated structure dominated by multinational agricultural machinery manufacturers with localized production facilities and extensive dealer networks. Market leadership is influenced by technological capability in precision agriculture, financing partnerships, and aftersales service reach. Domestic manufacturers compete in niche segments and lower horsepower categories, while global OEMs dominate high-capacity tractors and advanced mechanization technologies across commercial farming regions.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Manufacturing Presence in Brazil |

| AGCO Corporation | 1990 | United States | ~ | ~ | ~ | ~ | ~ |

| CNH Industrial | 2013 | United Kingdom | ~ | ~ | ~ | ~ | ~ |

| Deere and Company | 1837 | United States | ~ | ~ | ~ | ~ | ~ |

| Kubota Corporation | 1890 | Japan | ~ | ~ | ~ | ~ | ~ |

| Agrale | 1962 | Brazil | ~ | ~ | ~ | ~ | ~ |

Brazil Agricultural Tractor Market Analysis

Growth Drivers

Mechanization Expansion in Export-Oriented Agribusiness Regions:

Brazil’s agricultural sector is dominated by large-scale commercial farms specializing in soybean, corn, cotton, and sugarcane production for global export markets. These operations require high-capacity tractors capable of continuous field operations across thousands of hectares. Increasing global demand for Brazilian agricultural commodities incentivizes producers to expand cultivated acreage and improve operational efficiency. Mechanization becomes essential to maintain productivity and manage labor constraints in remote farming regions. Adoption of advanced tractors enables faster planting and harvesting cycles aligned with double-cropping systems. Precision agriculture technologies integrated into tractors support yield optimization and input efficiency. Export-driven agribusiness revenues provide capital for machinery investment and fleet modernization. Expansion of logistics corridors and grain terminals further stimulates mechanized production systems. This structural shift toward industrialized agriculture sustains long-term tractor demand growth across Brazil.

Government-Supported Rural Credit and Equipment Financing Programs:

Public agricultural credit programs and subsidized financing initiatives play a central role in Brazil’s farm mechanization adoption. National rural development banks and agricultural financing schemes provide low-interest loans for machinery acquisition. These programs reduce upfront capital barriers for medium and large farmers investing in tractors. Financing availability stimulates replacement of aging equipment fleets with modern high-efficiency tractors. Government policies prioritize mechanization as a productivity enhancement tool within agricultural modernization strategies. Credit programs often include grace periods aligned with crop cycles, improving affordability for producers. Equipment financing partnerships between banks and OEMs expand tractor accessibility across farming regions. Subsidized credit also supports cooperatives and contractor service providers acquiring tractors for shared use. This financial ecosystem significantly accelerates tractor penetration and technological upgrading across Brazil’s agricultural landscape.

Market Challenges

Dependence on Imported Components and Currency Volatility Exposure:

Brazil’s agricultural tractor manufacturing ecosystem relies significantly on imported components such as transmissions, hydraulic systems, electronics, and engine technologies sourced from global supply chains. Exchange rate fluctuations directly impact production costs and tractor pricing in domestic markets. Currency depreciation increases import costs, reducing affordability for farmers and compressing manufacturer margins. Price volatility complicates procurement planning for agricultural producers with seasonal income cycles. Domestic localization of high-precision components remains limited due to technological and scale constraints. Global supply chain disruptions can delay manufacturing and delivery schedules. Import tariffs and logistics costs further elevate tractor prices relative to farm income growth. Manufacturers face challenges maintaining competitive pricing while sustaining technological standards. This structural dependence on imported inputs exposes the tractor market to macroeconomic instability and exchange-rate risk.

High Capital Cost and Uneven Mechanization Penetration Across Farm Sizes:

Agricultural tractors represent significant capital investments relative to farm income, particularly for small and medium producers operating fragmented landholdings. High purchase prices and maintenance costs limit mechanization adoption outside large agribusiness regions. Smallholder farms often rely on older second-hand tractors or manual labor due to affordability constraints. Regional disparities in farm size and income create uneven tractor demand distribution across Brazil. Financing access remains more limited for small producers lacking credit history or collateral. Maintenance infrastructure and spare parts availability are weaker in remote rural areas. High horsepower tractors suitable for large farms are often unsuitable for diversified smallholder systems. This dual-structure agriculture limits overall market expansion potential. Persistent affordability barriers slow mechanization penetration across significant segments of Brazil’s farming population.

Opportunities

Adoption of Precision Agriculture and Connected Tractor Technologies:

Digital agriculture technologies are increasingly integrated into tractor platforms through GPS guidance, telematics, sensors, and data analytics systems. Brazilian large-scale farms are early adopters of precision farming practices to optimize yields and reduce input costs. Connected tractors enable real-time monitoring of field operations, fuel consumption, and machine performance. Integration with farm management software supports data-driven decision-making across planting, fertilization, and harvesting stages. OEMs are expanding smart tractor offerings tailored to Brazil’s cropping systems. Precision agriculture improves operational efficiency across extensive farmland areas. Government and agribusiness sustainability initiatives promote resource-efficient farming technologies. Service providers offer retrofit precision kits for existing tractor fleets. This technological transformation creates substantial demand for advanced tractors equipped with digital capabilities across Brazil’s mechanized agriculture sector.

Expansion of Agricultural Contractor and Equipment-Sharing Service Models:

Agricultural service contractors and machinery rental models are expanding in Brazil to address mechanization affordability gaps among small and medium farmers. Contractors invest in modern tractor fleets and provide mechanized services such as planting, tillage, and spraying on a fee basis. This model spreads capital costs across multiple farms and improves tractor utilization rates. Cooperative ownership structures also enable shared equipment access within farming communities. Digital platforms are emerging to match machinery providers with farmers requiring services. Contractors often adopt high-horsepower tractors to maximize productivity across large service areas. Government programs and rural credit schemes support contractor fleet acquisition. This service-based mechanization model broadens tractor demand beyond direct farm ownership. Expansion of rental and contracting ecosystems creates new market channels for tractor manufacturers in Brazil.

Future Outlook

Brazil agricultural tractor market is expected to experience sustained growth driven by continued expansion of mechanized agribusiness and rising adoption of precision farming technologies. Technological integration in tractors, including automation and connectivity, will accelerate fleet modernization across commercial farms. Government credit programs and export-oriented agriculture policies will reinforce equipment investment. Increasing demand for higher horsepower tractors suited to large-scale cultivation will shape product mix evolution. Contractor-based mechanization models and digital agriculture platforms will further broaden tractor utilization across diverse farming segments.

Major Players

- AGCO Corporation

- CNH Industrial

- Deere and Company

- Kubota Corporation

- Agrale

- Mahindra and Mahindra Farm Equipment

- Yanmar Agricultural Machinery

- CLAAS Group

- Argo Tractors

- SDF Group

- Escorts Kubota Limited

- LS Mtron

- Tafe Motors and Tractors

- Valtra

- Jacto Tractors

Key Target Audience

- Agricultural machinery manufacturers

- Farm equipment distributors

- Agribusiness companies

- Agricultural cooperatives

- Farm mechanization contractors

- Agricultural financing institutions

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Market boundaries, tractor categories, horsepower classes, technology features, regional demand drivers, and pricing structures were defined using agricultural machinery industry datasets and national farm mechanization statistics.

Step 2: Market Analysis and Construction

Supply-side production data, import-export flows, and farm mechanization adoption indicators were analyzed to construct market sizing and segmentation across Brazil’s agricultural regions and tractor categories.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultation with agricultural equipment distributors, farm operators, and mechanization specialists to confirm demand patterns, technology adoption, and pricing dynamics.

Step 4: Research Synthesis and Final Output

Validated datasets and qualitative insights were synthesized into structured analysis covering market size, segmentation, competitive landscape, and growth outlook for Brazil agricultural tractor market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of mechanized soybean and corn cultivation

Government backed rural credit and equipment financing programs

Rising labor scarcity in large scale farming regions

Adoption of precision agriculture practices

Growth of export oriented agribusiness production - Market Challenges

High capital cost of advanced horsepower tractors

Volatility in agricultural commodity prices affecting purchases

Dependence on imported components and currency fluctuations

Limited mechanization penetration in smallholder segments

Maintenance and service infrastructure gaps in remote regions - Market Opportunities

Expansion of smart and connected tractor technologies

Growth of biofuel compatible agricultural machinery

Emergence of rental and shared tractor service models - Trends

Shift toward higher horsepower tractors for large farms

Integration of GPS and auto steer systems

Growth in telematics based fleet management

Increasing demand for fuel efficient engines

Localization of manufacturing by global OEMs - Government Regulations & Defense Policy

National agricultural mechanization incentives

Emission and engine efficiency standards

Rural credit and subsidized equipment schemes - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Utility Tractors

Row Crop Tractors

Orchard and Vineyard Tractors

Articulated Four Wheel Drive Tractors

Compact Tractors - By Platform Type (In Value%)

Open Field Mechanization

Plantation Farming Platforms

Specialty Crop Platforms

Livestock Farm Platforms

Mixed Farming Platforms - By Fitment Type (In Value%)

Two Wheel Drive Tractors

Mechanical Four Wheel Drive Tractors

Hydrostatic Transmission Tractors

Cabin Enclosed Tractors

Precision Guidance Ready Tractors - By EndUser Segment (In Value%)

Smallholder Farms

Medium Commercial Farms

Large Agribusiness Enterprises

Cooperative Farming Groups

Contract Farming Operators - By Procurement Channel (In Value%)

Authorized Dealer Networks

Direct Manufacturer Sales

Agricultural Cooperatives Procurement

Government Subsidy Programs

Leasing and Financing Providers - By Material / Technology (in Value %)

Conventional Diesel Tractors

Electronic Engine Control Tractors

Precision Farming Enabled Tractors

Telematics Integrated Tractors

Alternative Fuel Tractors

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Horsepower Range, Drive Type, Precision Farming Capability, Telematics Integration, Fuel Efficiency, Transmission Type, AfterSales Network Strength, Localization Level, Price Tier Positioning, Financing Support)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

AGCO Corporation

CNH Industrial

Deere and Company

Kubota Corporation

Mahindra and Mahindra Farm Equipment

Yanmar Agricultural Machinery

CLAAS Group

Argo Tractors

SDF Group

Escorts Kubota Limited

LS Mtron

Tafe Motors and Tractors

Valtra

Agrale

Jacto Tractors

- Large agribusiness farms adopting high horsepower tractors for scale efficiency

- Medium farms transitioning from used to new mechanized fleets

- Cooperatives enabling shared ownership of advanced tractors

- Smallholders relying on subsidized procurement and rental access

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now