Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Brazil’s AI servers and GPU hardware market reached approximately USD ~ billion based on a recent historical assessment, driven by hyperscale cloud expansion, enterprise artificial intelligence adoption, and increasing demand for accelerated computing across financial services, telecommunications, retail, and public sector analytics workloads. Growth is reinforced by deployment of GPU clusters in data centers, AI research infrastructure investments, and rising generative AI experimentation across enterprises. Expansion of AI-ready cloud regions and high-performance computing programs further stimulates hardware demand nationwide.

São Paulo dominates Brazil’s AI servers and GPU hardware landscape due to hyperscale data center concentration, enterprise demand density, financial sector analytics infrastructure, and proximity to cloud provider regions. Campinas and southern technology corridors support semiconductor design and research computing clusters, while Rio de Janeiro hosts energy and government analytics systems. Strong metropolitan connectivity, innovation ecosystems, and data center availability reinforce regional leadership. National digitalization initiatives and cloud infrastructure expansion further strengthen hardware deployment across Brazil’s primary economic hubs.

Market Segmentation

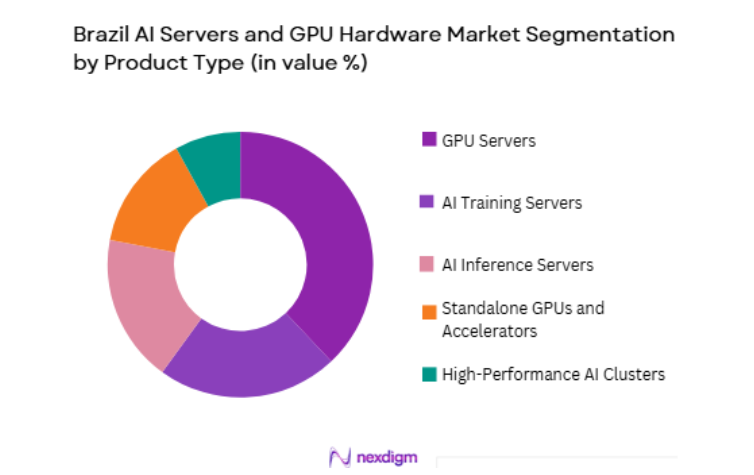

By Product Type

Brazil AI Servers and GPU Hardware market is segmented by product type into GPU servers, AI training servers, AI inference servers, standalone GPUs and accelerators, and high-performance AI clusters. Recently, GPU servers has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference.

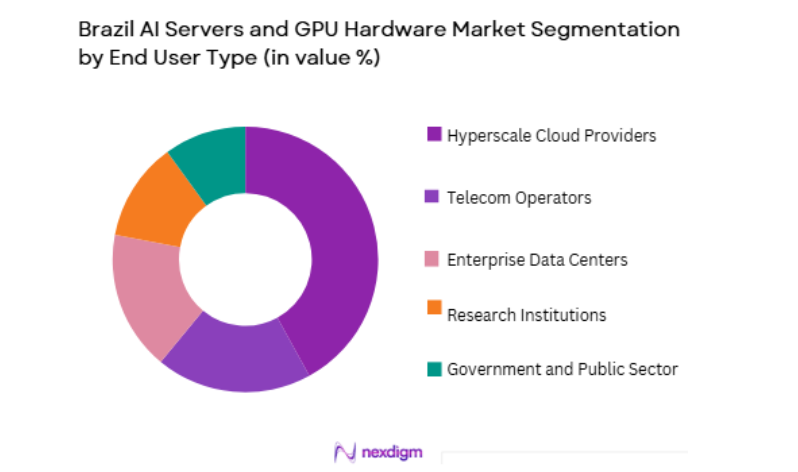

By End User

Brazil AI Servers and GPU Hardware market is segmented by end user into hyperscale cloud providers, telecom operators, enterprise data centers, research institutions, and government and public sector. Recently, hyperscale cloud providers has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference.

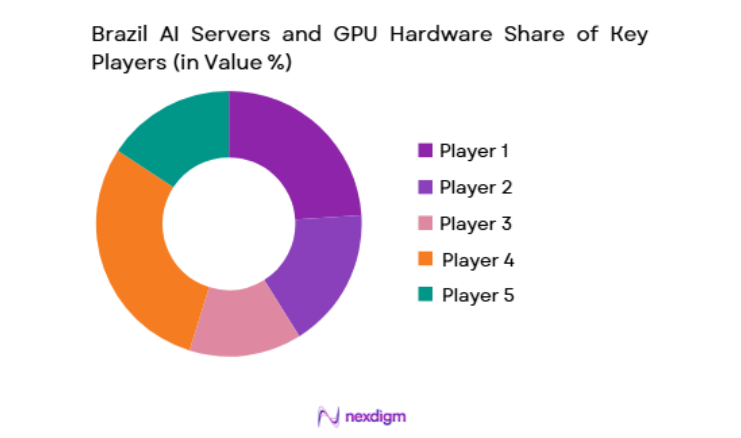

Competitive Landscape

Brazil’s AI servers and GPU hardware market is concentrated among global semiconductor and server manufacturers supplying hyperscale cloud providers and enterprise data centers deploying accelerated computing infrastructure. Competitive positioning depends on GPU architecture leadership, server integration capabilities, and regional distribution partnerships. Hyperscale cloud operators influence procurement volumes and technology adoption, while enterprise AI deployments create secondary demand across telecom, finance, and research sectors.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Brazil AI Hardware Supply Presence |

| NVIDIA | 1993 | USA | ~ | ~ | ~ | ~ | ~ |

| Intel | 1968 | USA | ~ | ~ | ~ | ~ | ~ |

| AMD | 1969 | USA | ~ | ~ | ~ | ~ | ~ |

| Dell Technologies | 1984 | USA | ~ | ~ | ~ | ~ | ~ |

| Hewlett Packard Enterprise | 2015 | USA | ~ | ~ | ~ | ~ | ~ |

Brazil AI Servers and GPU Hardware Market Analysis

Growth Drivers

Hyperscale AI Cloud Expansion and Accelerated Computing Demand

Hyperscale cloud providers operating in Brazil are rapidly expanding artificial intelligence infrastructure capacity requiring large-scale procurement of GPU servers and accelerated computing platforms to support machine learning training, inference, and generative AI workloads across regional cloud regions. São Paulo data center campuses host dense GPU clusters enabling AI cloud services consumed by enterprises nationwide. Growth of AI-as-a-service platforms and managed machine learning environments increases demand for high-performance GPU hardware within hyperscale facilities. Enterprises adopting AI applications rely on hyperscale providers rather than on-premise deployments, concentrating hardware demand within cloud operators. Continuous scaling of AI model size and dataset volume requires next-generation GPU architectures and high-bandwidth memory systems. Hyperscale procurement cycles create predictable large-volume hardware demand across server manufacturers and semiconductor vendors. Cloud region expansion across Latin America positions Brazil as a regional AI compute hub requiring sustained hardware deployment.

Enterprise Generative AI Adoption and High-Performance Computing Modernization

Brazilian enterprises across banking, telecommunications, retail, energy, and manufacturing are adopting generative AI, advanced analytics, and high-performance computing workloads requiring deployment of GPU-accelerated servers and AI hardware platforms within enterprise and hybrid cloud environments. Financial institutions deploy deep learning models for fraud detection and risk analytics requiring GPU clusters. Telecom operators implement AI-driven network optimization and customer analytics supported by accelerated servers. Retail platforms adopt recommendation and demand forecasting models relying on GPU inference systems. Energy and industrial firms deploy simulation and predictive maintenance workloads requiring high-performance computing modernization. Enterprise data centers are upgrading legacy CPU-centric architectures toward heterogeneous GPU-accelerated infrastructure. System integrators and OEM vendors provide AI-ready server platforms tailored to enterprise deployments. Growth of private and hybrid AI environments increases hardware procurement beyond hyperscale clouds. Expansion of enterprise data lakes and analytics pipelines generates sustained demand for GPU hardware.

Market Challenges

High Import Dependence and Currency-Driven Hardware Cost Volatility

Brazil’s AI server and GPU hardware market depends heavily on imported semiconductor devices and server systems sourced from global manufacturers, exposing procurement costs to exchange rate fluctuations, tariffs, and international supply chain disruptions affecting affordability and deployment planning. High-end GPUs and AI accelerators remain scarce and expensive due to global demand concentration and export controls impacting availability. Import duties and taxation increase landed cost of AI hardware relative to global markets. Enterprises face capital constraints deploying GPU clusters due to elevated acquisition costs. Domestic manufacturing capability for advanced semiconductors and AI servers is limited, constraining local supply resilience. Currency depreciation periods significantly increase hardware procurement budgets for Brazilian buyers. Financing constraints affect smaller enterprises adopting AI infrastructure.

Infrastructure Readiness and Skilled AI Hardware Integration Constraints

Deployment of AI servers and GPU clusters requires advanced data center infrastructure including power density, cooling capacity, and high-speed networking not uniformly available across Brazilian enterprise facilities, creating barriers for on-premise AI hardware adoption. Many enterprise data centers lack sufficient electrical and thermal design to host dense GPU servers. Skilled workforce shortages in AI infrastructure engineering, cluster orchestration, and HPC operations limit effective hardware utilization. Integration of GPU systems with legacy IT architectures creates complexity. Software optimization and workload orchestration expertise remain limited in certain sectors. Operational management of distributed GPU clusters increases technical burden for enterprises. Research institutions face funding limitations for large HPC infrastructure. Hardware lifecycle management and upgrades add operational cost.

Opportunities

National AI Research Infrastructure and Academic HPC Expansion

Brazil’s national artificial intelligence strategy and research funding initiatives support expansion of academic high-performance computing clusters and AI research infrastructure requiring GPU servers and accelerators across universities and national laboratories. Government-funded AI centers deploy GPU-accelerated computing environments for scientific research and innovation projects. Academic collaboration with industry increases demand for shared AI computing platforms. Expansion of open science and data initiatives requires scalable HPC infrastructure. Research applications in climate modeling, agriculture analytics, and health sciences rely on GPU clusters. Public funding programs stimulate procurement of AI hardware for educational and research institutions. Partnerships with global technology vendors support technology transfer and infrastructure deployment. Development of national AI computing facilities reduces dependence on foreign cloud resources.

Edge AI and Telecom Infrastructure Integration

Deployment of artificial intelligence processing at telecom and edge computing sites across Brazil requires compact GPU-enabled servers and accelerators integrated into distributed infrastructure supporting real-time analytics, video processing, and network intelligence applications nationwide. Telecom operators deploy GPU servers at edge data centers for AI-driven network optimization and low-latency services. Smart city and surveillance analytics systems require edge AI hardware deployments. Industrial automation and IoT applications process data locally using embedded GPU platforms. Autonomous mobility and logistics platforms require distributed AI inference hardware. Integration of AI servers with 5G infrastructure expands distributed hardware footprint. Edge-to-cloud AI architectures increase total GPU deployment across networks. Hardware vendors are developing ruggedized and energy-efficient GPU systems for edge environments.

Future Outlook

Brazil’s AI servers and GPU hardware market is expected to grow rapidly over the next five years supported by hyperscale AI cloud expansion, enterprise generative AI adoption, and national research computing investments. Data center modernization and edge AI deployment will increase distributed GPU hardware demand. Government AI initiatives and digitalization programs will reinforce infrastructure procurement. Semiconductor vendor partnerships and regional cloud growth will sustain hardware deployment.

Major Players

- NVIDIA

- Intel

- AMD

- Dell Technologies

- Hewlett Packard Enterprise

- Lenovo

- Cisco Systems

- Supermicro

- IBM

- Huawei

- Inspur

- Oracle

- Amazon Web Services

- Microsoft

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Hyperscale cloud providers

- Telecom operators

- Enterprise data center operators

- Research institutions and HPC centers

- Financial services institutions

- Industrial AI solution providers

Research Methodology

Step 1: Identification of Key Variables

Key variables including GPU shipment volumes, AI server deployment capacity, hyperscale procurement cycles, enterprise AI adoption rates, and data center infrastructure readiness were identified through secondary research and vendor disclosures.

Step 2: Market Analysis and Construction

Market sizing and segmentation were constructed using semiconductor revenue data, server shipment statistics, cloud region capacity indicators, and enterprise infrastructure investment trends across Brazil.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings were validated through consultations with AI hardware vendors, hyperscale operators, system integrators, and research infrastructure specialists to confirm demand drivers and supply dynamics.

Step 4: Research Synthesis and Final Output

Validated insights were synthesized into structured analysis covering segmentation, competitive landscape, market dynamics, and outlook ensuring coherent research conclusions.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Rapid enterprise adoption of AI and machine learning workloads

Expansion of hyperscale AI cloud regions in Brazil

Government and academic investment in AI computing capacity - Market Challenges

High cost and limited availability of advanced GPUs

Power and cooling constraints for dense AI hardware

Dependence on imported semiconductor and server components - Market Opportunities

Growth of sovereign AI infrastructure initiatives

AI adoption across agritech finance and healthcare sectors

Local assembly and integration of AI servers - Trends

Shift toward high density GPU clusters for AI training

Adoption of liquid cooling in AI server deployments - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

GPU Accelerated AI Servers

AI Training Servers

AI Inference Servers

Multi GPU High Density Servers

AI Optimized Rack Scale Systems - By Platform Type (In Value%)

Hyperscale Cloud AI Platforms

Enterprise AI Data Centers

Research and Academic AI Clusters

Telecom AI Infrastructure

Edge AI Server Deployments - By Fitment Type (In Value%)

New AI Server Deployments

Data Center AI Retrofits

Modular AI Server Racks

Integrated AI Infrastructure Systems - By End User Segment (In Value%)

Cloud Service Providers

Enterprises

Government and Research Institutions

Telecom Operators

- Market Share Analysis

- Cross Comparison Parameters (GPU Density, Compute Performance, Power Efficiency, Cooling Architecture, Interconnect Bandwidth, Memory Bandwidth, Scalability, Rack Power Density, AI Framework Optimization, Deployment Flexibility, Supply Chain Availability, Total Cost of Ownership)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

NVIDIA

AMD

Intel

Dell Technologies

Hewlett Packard Enterprise

Lenovo

Supermicro

Gigabyte

ASUS

IBM

Cisco

Oracle

Microsoft

Amazon Web Services

Google

- Cloud providers scaling GPU clusters for AI services

- Enterprises deploying private AI compute infrastructure

- Research institutions expanding high performance AI labs

- Telecom operators enabling AI driven network optimization

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now