Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Brazil cloud infrastructure market reached approximately USD ~ billion in hyperscale and enterprise cloud infrastructure investment based on a recent historical assessment, driven by rapid cloud migration across banking, retail, and public sectors, hyperscale data center expansion, and national digital transformation initiatives. Demand is concentrated in compute, storage, and networking infrastructure deployed in large-scale data centers supporting SaaS, AI workloads, and enterprise cloud platforms operated by global and regional providers across Brazil.

São Paulo, Rio de Janeiro, and Campinas dominate Brazil cloud infrastructure deployment due to financial sector concentration, submarine cable connectivity, and established data center ecosystems. São Paulo hosts the majority of hyperscale cloud regions and enterprise data centers, Rio de Janeiro benefits from telecom landing stations and energy infrastructure, while Campinas supports technology parks and colocation clusters enabling large-scale cloud infrastructure development serving Brazil’s digital economy.

Market Segmentation

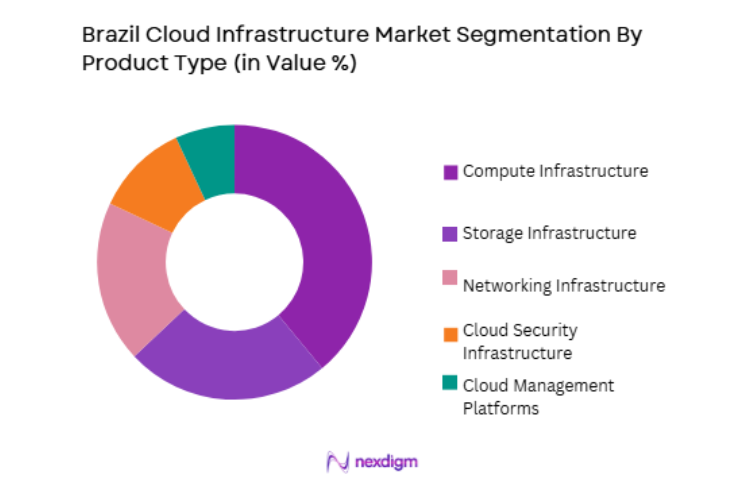

By Product Type

Brazil Cloud Infrastructure market is segmented by product type into compute infrastructure, storage infrastructure, networking infrastructure, cloud security infrastructure, and cloud management platforms. Recently, compute infrastructure has a dominant market share due to factors such as hyperscale data center server deployments, enterprise cloud migration, and AI workload expansion across Brazilian industries. Hyperscale providers and colocation operators are investing heavily in server clusters and virtualization platforms to support SaaS, analytics, and AI applications, resulting in higher capital allocation toward compute hardware compared with storage or networking segments within Brazil’s expanding cloud infrastructure ecosystem.

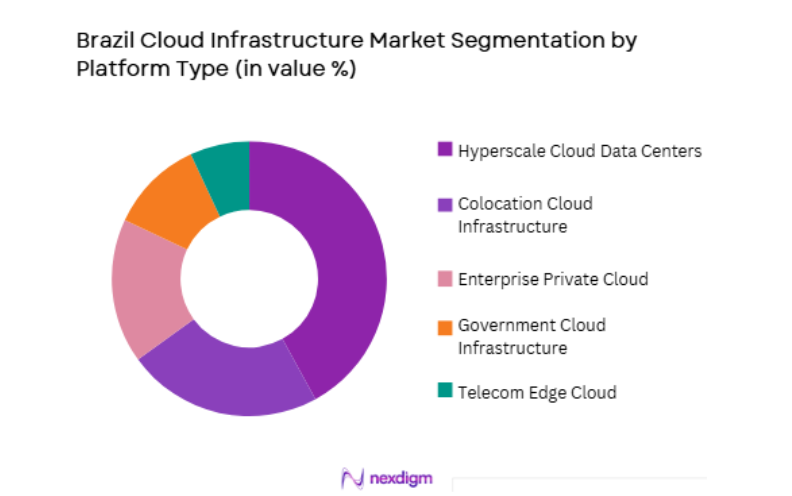

By Platform Type

Brazil Cloud Infrastructure market is segmented by platform type into hyperscale cloud data centers, colocation cloud infrastructure, enterprise private cloud infrastructure, government cloud infrastructure, and telecom edge cloud infrastructure. Recently, hyperscale cloud data centers has a dominant market share due to factors such as global cloud provider region expansion, enterprise public cloud adoption, and large-scale SaaS and AI service deployment. Major hyperscalers are expanding Brazilian cloud regions with GPU-enabled compute clusters and high-density server facilities, concentrating infrastructure spending in hyperscale campuses compared with distributed enterprise or edge deployments across Brazil.

Competitive Landscape

Brazil cloud infrastructure market is highly concentrated, dominated by global hyperscale cloud providers and data center operators that deploy large compute and storage clusters, while regional colocation providers and telecom firms support enterprise and edge infrastructure deployment. Competitive positioning is shaped by hyperscale capital scale, cloud service ecosystems, and geographic data center coverage across Brazil’s major metropolitan regions.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Brazil Cloud Regions |

| Amazon Web Services | 2006 | USA | ~ | ~ | ~ | ~ | ~ |

| Microsoft Azure | 2010 | USA | ~ | ` | ` | ` | ` |

| Google Cloud | 2008 | USA | |||||

| Equinix | 1998 | USA | |||||

| Ascenty | 2010 | Brazil |

Brazil Cloud Infrastructure Market Analysis

Growth Drivers

Enterprise Digital Transformation and Cloud Migration Acceleration

Brazil cloud infrastructure demand is strongly driven by rapid enterprise digital transformation and migration of mission-critical workloads from on-premise IT systems to scalable cloud platforms across banking, retail, manufacturing, and public sector organizations, resulting in sustained investment in compute, storage, and networking infrastructure deployed in hyperscale and colocation data centers nationwide. Brazilian enterprises are adopting SaaS, analytics, and AI applications requiring elastic cloud infrastructure capacity, accelerating procurement of server clusters and virtualization platforms. Financial institutions and e-commerce firms are leading cloud adoption due to data processing and customer platform requirements. Government digital service initiatives further expand public cloud demand. Hyperscale providers expand local regions to meet latency and compliance requirements. Migration from legacy IT systems increases infrastructure refresh cycles. Cloud-native application development drives demand for scalable infrastructure. These factors collectively sustain strong growth in Brazil’s cloud infrastructure market.

Hyperscale Data Center Expansion and Submarine Connectivity Investment

Brazil cloud infrastructure expansion is propelled by large-scale hyperscale data center construction and submarine cable connectivity investments linking Brazil to global internet backbones, enabling international cloud providers to deploy high-capacity compute and storage infrastructure serving Latin American markets. Brazil’s geographic position and connectivity corridors attract hyperscale investment in multi-megawatt data center campuses. Submarine cable landing stations in coastal cities provide high-bandwidth connectivity for cloud services. Hyperscalers deploy regional cloud zones requiring massive infrastructure capacity. Renewable energy availability supports large data center operations. Colocation ecosystems expand alongside hyperscale facilities. Connectivity investments reduce latency and improve cloud performance.

Market Challenges

Power Availability and Data Center Energy Constraints

Brazil cloud infrastructure deployment faces challenges related to reliable power availability, grid capacity limitations, and energy cost volatility affecting large-scale data center operations that require continuous high-density electricity supply for compute and cooling infrastructure. Hyperscale data centers demand multi-megawatt power connections that strain regional grids. Energy pricing fluctuations impact operating economics. Renewable integration requires infrastructure upgrades. Grid reliability concerns affect facility siting decisions. Backup power and redundancy systems increase capital costs. Environmental permitting for energy infrastructure delays projects. These constraints limit rapid expansion of cloud infrastructure in some regions.

Regulatory Complexity and Data Localization Requirements

Brazil cloud infrastructure growth is affected by regulatory complexity including data protection laws, localization requirements, and telecommunications regulations that impose compliance costs and infrastructure design constraints on cloud providers operating within the country. Data residency requirements necessitate domestic data center deployment. Regulatory approvals for telecom and data center construction extend timelines. Compliance with privacy and cybersecurity standards increases infrastructure costs. Cross-border data transfer restrictions affect architecture. Government procurement rules influence cloud deployment. Legal uncertainty affects investment planning. These regulatory factors create operational challenges for cloud infrastructure expansion.

Opportunities

AI and High-Performance Cloud Infrastructure Expansion

Brazil cloud infrastructure market has major opportunity in deployment of AI-optimized and high-performance cloud infrastructure supporting generative AI, analytics, and machine learning workloads across enterprises and public sector organizations, requiring GPU-enabled servers and high-speed networking systems within hyperscale data centers. AI adoption across finance, retail, and agriculture sectors drives demand for accelerated cloud infrastructure. Hyperscalers are deploying AI clusters in Brazil regions. Enterprise AI platforms require scalable compute. GPU cloud services create new revenue streams. AI startups increase infrastructure utilization. National AI strategies support compute expansion. This opportunity accelerates cloud infrastructure growth.

Edge Cloud and Telecom Infrastructure Integration

Brazil cloud infrastructure market can expand through integration of cloud compute and storage nodes into telecom networks and edge data centers enabling low-latency digital services, IoT platforms, and real-time analytics across urban and industrial environments. Telecom operators deploy edge cloud facilities near population centers. 5G expansion supports distributed cloud architectures. Smart city and industrial IoT applications require local compute. Edge nodes complement hyperscale infrastructure. Telecom-cloud partnerships drive deployment. Regional edge data centers increase infrastructure footprint. This opportunity broadens cloud infrastructure beyond hyperscale campuses.

Future Outlook

Brazil cloud infrastructure market is expected to expand strongly over the next five years as hyperscale data center construction, enterprise cloud adoption, and AI workload deployment accelerate across industries. Continued submarine connectivity investments, regulatory support for digital transformation, and growth of edge and AI cloud platforms will sustain infrastructure demand. Expansion of cloud regions and colocation capacity will strengthen Brazil’s role as Latin America’s primary cloud infrastructure hub.

Major Players

- Amazon Web Services

- Microsoft Azure

- Google Cloud

- Equinix

- Ascenty

- Huawei Cloud

- IBM Cloud

- Oracle Cloud

- Scala Data Centers

- ODATA

- Telefonica Tech

- Claro Cloud

- TIVIT

- Lumen Technologies

- UOL Diveo

Key Target Audience

- Hyperscale cloud providers

- Enterprise IT departments

- Telecom network operators

- Investments and venture capitalist firms

- Government and regulatory bodies

- Data center operators

- SaaS providers

- AI platform companies

Research Methodology

Step 1: Identification of Key Variables

Cloud data center capacity, server deployments, storage installations, network infrastructure expansion, and hyperscale investment indicators were identified from industry and infrastructure sources. Variables included regional cloud regions, enterprise cloud adoption levels, and connectivity infrastructure.

Step 2: Market Analysis and Construction

Brazil cloud infrastructure market size was constructed using data center investment values, cloud hardware spending, hyperscale and colocation infrastructure deployment, and enterprise cloud adoption patterns across sectors. Platform segmentation was mapped to infrastructure spending.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions were validated through consultation with cloud infrastructure engineers, data center operators, and telecom infrastructure specialists in Brazil. Connectivity and hyperscale investment trends were cross-checked with industry experts.

Step 4: Research Synthesis and Final Output

All validated quantitative and qualitative insights were synthesized into structured market analysis covering segmentation, competitive landscape, drivers, challenges, and opportunities. Findings were consolidated into a comprehensive Brazil cloud infrastructure market report.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of hyperscale cloud regions in Brazil

Enterprise migration to hybrid and multi cloud architectures

Rising demand for AI and digital services infrastructure - Market Challenges

High energy and land costs for data center development

Power grid and connectivity constraints in some regions

Regulatory and data sovereignty compliance requirements - Market Opportunities

Renewable powered green data center development

Edge cloud expansion for 5G and IoT applications

Public sector sovereign cloud modernization programs - Trends

Adoption of high density cloud infrastructure

Shift toward modular prefabricated data centers - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Compute Server Infrastructure

Storage Systems

Networking Equipment

Data Center Power Systems

Cooling and Thermal Management Systems - By Platform Type (In Value%)

Hyperscale Cloud Data Centers

Enterprise Private Cloud Infrastructure

Colocation Data Center Infrastructure

Edge Cloud Infrastructure

Government and Sovereign Cloud Platforms - By Fitment Type (In Value%)

New Data Center Builds

Data Center Retrofits and Upgrades

Modular Containerized Data Centers

Integrated Turnkey Cloud Facilities - By End User Segment (In Value%)

Cloud Service Providers

Telecom Operators

Government and Public Sector

- Market Share Analysis

- Cross Comparison Parameters (Deployment Scale, Energy Efficiency, Infrastructure Density, Cooling Technology, Network Connectivity, Scalability, Power Utilization Effectiveness, Geographic Presence, Renewable Energy Adoption)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Amazon Web Services

Microsoft Azure

Google Cloud

Oracle

IBM

Huawei Cloud

Equinix

Digital Realty

Ascenty

Scala Data Centers

Odata

Tecto Data Centers

Lumen Technologies

Telefónica

Claro

- Cloud providers expanding hyperscale campuses in major metros

- Telecom operators integrating cloud with 5G networks

- Government agencies prioritizing secure sovereign cloud

- Enterprises modernizing legacy IT to hybrid cloud

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now