Download PDF

Download PDFMarket Overview

The Brazil Energy Drink Market is valued at USD ~ billion, based on latest reported country-level market assessment, while another country outlook reports Brazil energy drinks revenue of USD ~ million in the preceding historical base, showing Brazil’s position as a major Latin American stimulant beverage market. Demand is driven by urban youth consumption, gym culture, nightlife mixers, convenience retail, and the shift from traditional carbonated beverages toward functional ready-to-drink products. The Brazil Energy Drink Market is led by São Paulo, Rio de Janeiro, Belo Horizonte, Brasília, Fortaleza, Recife, Curitiba and Salvador because these cities combine population density, nightlife, universities, organized retail, gyms, petrol stations and event-led beverage demand. IBGE reported São Paulo metropolitan area at 21,518,955 residents, Rio de Janeiro at 12,936,629, Belo Horizonte at 5,997,565, Federal District surroundings at 4,732,087, Fortaleza at 4,137,255, Recife at 3,954,323, Curitiba at 3,697,928, and Salvador at 3,623,647 residents.

Market Segmentation

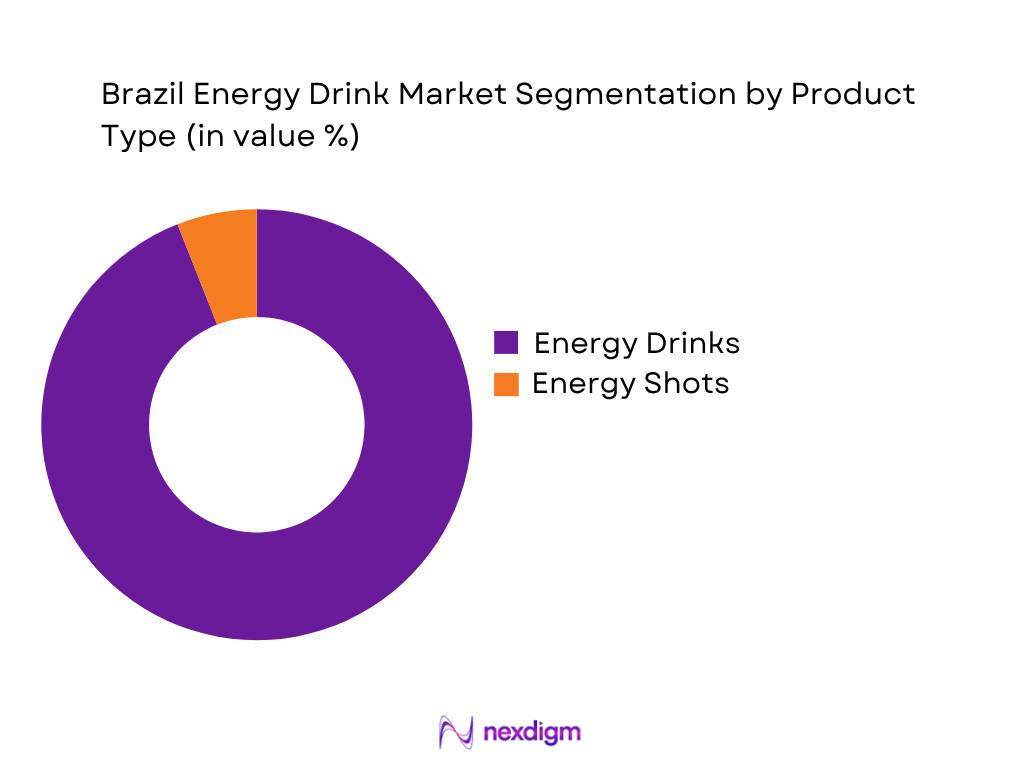

By Product Type

Brazil Energy Drink Market is segmented by product type into non-alcoholic energy drinks, alcoholic energy drinks and energy shots. Recently, non-alcoholic energy drinks have a dominant market share in Brazil under the product type segmentation due to their mass availability across supermarkets, hypermarkets, petrol stations, convenience stores, bars, clubs, gyms and online marketplaces. These products fit Brazil’s main energy-drink occasions: work, study, commuting, nightlife, long-distance driving, gaming and pre workout consumption. The segment benefits from strong brand portfolios such as Red Bull, Monster, TNT, Baly, Flying Horse and Fusion, along with high acceptance of guaraná, caffeine, taurine and B-vitamin formulations. Alcoholic energy drinks and energy shots remain smaller because they serve narrower occasions, face stronger regulatory sensitivity, and have lower shelf visibility than ready-to-drink canned energy products.

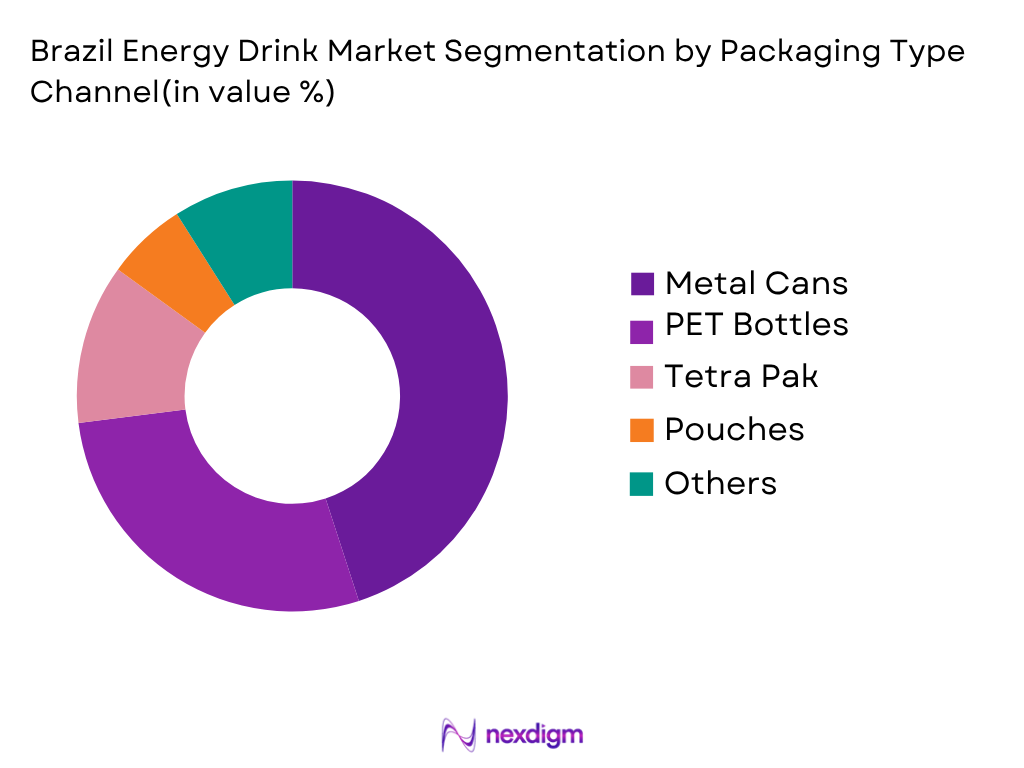

By Packaging Type

Brazil Energy Drink Market is segmented by packaging type into metal cans, PET bottles, glass bottles, Tetra Pak and pouches, and other packaging formats. Recently, metal cans have a dominant market share in Brazil under the packaging type segmentation because cans are strongly associated with premium image, carbonation retention, cold-vault visibility and fast chilling in a hot-climate market. Cans also support single-serve impulse purchase in petrol stations, convenience outlets, supermarkets and nightlife locations, where energy drink consumption is frequently immediate rather than planned. Global and domestic players use cans for flagship SKUs, zero-sugar variants, imported-style premium formats and limited-edition flavors. PET bottles remain important for regional and value-led brands, but cans remain the core pack architecture for mainstream and premium energy drinks.

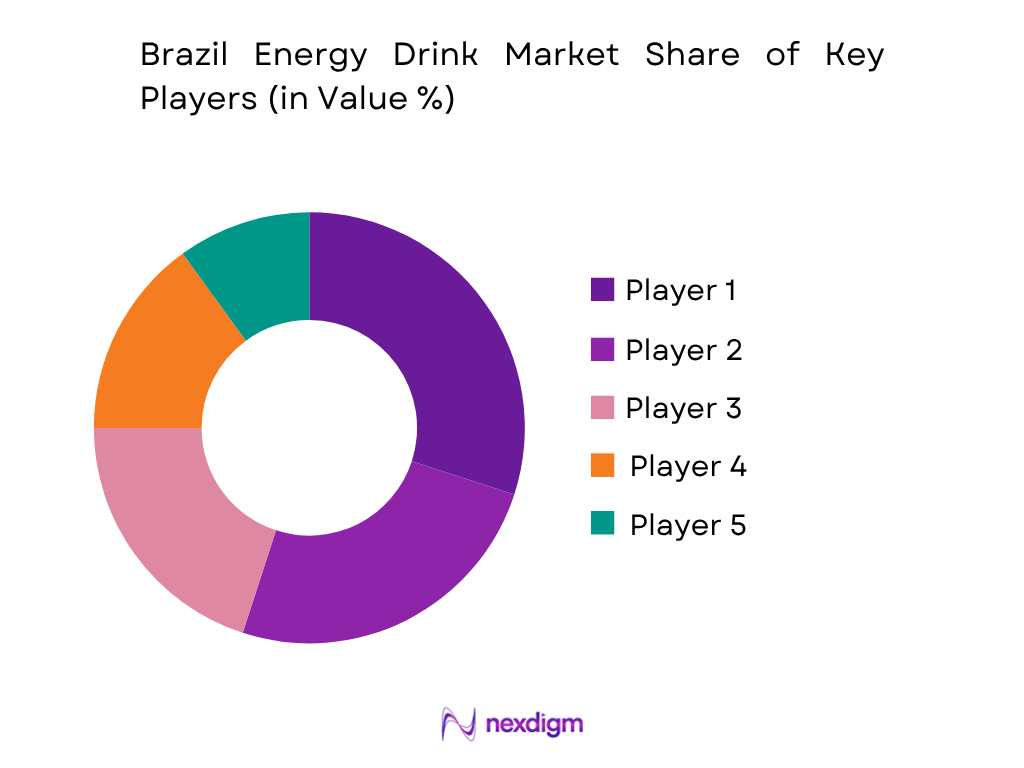

Competitive Landscape

The Brazil Energy Drink Market is led by a mix of global premium brands and domestic mass-market challengers. Red Bull and Monster maintain strong recognition through international brand equity, sports sponsorships, nightlife activation and premium positioning. Local and regional players such as Baly, TNT, Fusion and Flying Horse compete through affordability, larger formats, localized flavors, domestic distribution and strong visibility in supermarkets, cash-and-carry stores and traditional trade. The market concentration is high, but challenger brands are expanding through pack-size innovation, zero-sugar launches, regional penetration and event-led marketing.

| Company | Establishment Year | Headquarters | Core Energy Drink Brands | Brazil Positioning | Packaging Focus | Distribution Strength | Product Innovation Focus | Market-Specific Edge |

| Red Bull GmbH | 1984 | Fuschl am See, Austria | ~ | ~ | ~ | ~ | ~ | ~ |

| Monster Beverage Corporation | 1935 | Corona, California, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Baly Brasil | 2005 | Tubarão, Santa Catarina, Brazil | ~ | ~ | ~ | ~ | ~ | ~ |

| Grupo Petrópolis | 1994 | Petrópolis, Rio de Janeiro, Brazil | ~ | ~ | ~ | ~ | ~ | ~ |

| Britvic Brasil | 1938 / Brazil operations through Britvic | Hemel Hempstead, UK / Brazil operations | ~ | ~ | ~ | ~ | ~ | ~ |

Brazil Energy Drink Market Analysis

Growth Drivers

Urban Concentration and Retail-Ready Consumption Base

Brazil Energy Drink Market is supported by a dense urban consumer base that fits RTD energy drink occasions across supermarkets, cash-and-carry stores, gyms, petrol stations, nightlife and convenience-led retail. Brazil’s urban population reached 186,592,664 people according to World Bank-linked data, creating a large addressable base for chilled single-serve beverages. IBGE reported Brazil’s total population at 212.6 million people, while 42.7 million people lived in cities with more than 1 million inhabitants, strengthening demand clusters in São Paulo, Rio de Janeiro, Brasília, Fortaleza and Salvador. World Bank reported Brazil GDP at USD 2.19 trillion, supporting national beverage retail scale.

Large Workforce and On-the-Go Energy Occasions

Brazil Energy Drink Market benefits from a large employed population that supports recurring energy occasions linked to work, commuting, delivery, trade, transport, studying and shift-based routines. IBGE reported 103.3 million employed persons in Brazil, including 38.7 million persons with formal contracts and 26.0 million self-employed workers, creating broad demand for portable functional beverages consumed during work breaks and travel. Trade, repair of motor vehicles and motorcycles employed 19.8 million persons, while transportation, storage and mailing employed 5.9 million workers, both directly relevant to convenience-store, petrol-station and roadside beverage consumption.

Market Challenges

Regulatory Authorization and Labeling Complexity

Brazil Energy Drink Market faces compliance pressure because stimulant beverages operate within a strict food and packaging authorization framework. ANVISA states that RDC 843/2024 and IN 281/2024 entered into force on September 1, 2024, creating a formal structure for food and packaging market authorization. RDC 843/2024 establishes 3 regulatory pathways: marketing authorization with ANVISA, notification to ANVISA, and communication to local health authorities before manufacturing or importation. For energy drink brands, this raises execution requirements around caffeine disclosure, functional claims, imported SKU registration, packaging compliance, and distributor-level documentation across Brazil’s 212.6 million consumers.

Regional Distribution and Cold-Shelf Execution Pressure

Brazil Energy Drink Market faces distribution complexity because demand is concentrated in major cities, while national coverage requires managing fragmented retail, long delivery routes, and cold-shelf execution across diverse regions. IBGE reported 48 municipalities with more than 500,000 inhabitants, containing 65.7 million people, while metropolitan regions and urban agglomerations with more than 1 million inhabitants together had more than 100 million people. This creates high-value demand pockets but also requires differentiated route-to-market strategies. São Paulo alone had 46 million people at the state level, making shelf access intense, while smaller municipalities require regional distributors and lower-cost pack formats.

Market Opportunities

Delivery, Platform Work and Mobile Consumption Expansion

Brazil Energy Drink Market has a clear opportunity in delivery, app-based mobility and roadside retail because these workers create repeat functional beverage occasions around alertness, travel, and long working hours. IBGE reported 1.7 million people working through digital platforms and service apps, including passenger transportation, food delivery, product delivery, and professional services. Around 878,000 people worked in private passenger transportation apps, while 485,000 people worked through food and grocery delivery apps. Brazil also had 1.1 million employed motorcycle drivers, with 351,000 using apps, supporting petrol-station, convenience-store, delivery-zone and urban impulse beverage expansion.

Tourism, Events and Nightlife-Led Energy Drink Demand

Brazil Energy Drink Market has future growth opportunity through tourism, festivals, nightlife, airport retail and event-led consumption because energy drinks are strongly aligned with late-night, mixer, travel and social occasions. Brazil received 6.621 million international tourists, the highest result since the historical series began in 1970, according to the federal government. The same source reported 7.48 million international flight seats for the Southern Hemisphere summer season, strengthening travel-retail and horeca beverage opportunities. Large tourism and nightlife hubs overlap with major population centers, including São Paulo at 11.9 million residents and Rio de Janeiro at 6.7 million residents.

Future Outlook

The Brazil Energy Drink Market is expected to grow at a forecast CAGR of 8.40% in the available country-specific forecast period, while global long-term energy drink outlooks place the broader category CAGR near 8.16% during 2026–2035. Brazil’s long-term market expansion will be driven by functional beverage adoption, growing demand for alertness and stamina, stronger convenience retail access, nightlife consumption, and the normalization of energy drinks as daily beverages rather than niche stimulant products.

Over the next several years, market development will be shaped by three demand shifts. First, sugar-free, low-calorie and zero-sugar energy drinks will gain stronger traction among urban consumers, gym users and calorie-conscious buyers. Second, local flavor systems such as guaraná, açaí, tropical fruit, citrus and berry profiles will remain important for domestic differentiation. Third, regional players will continue competing against multinational brands by using larger pack formats, price-accessible positioning and deeper penetration in traditional retail.

Channel expansion will also define the market’s next phase. Supermarkets, hypermarkets and cash-and-carry stores will remain critical for multipacks and household purchase, while petrol stations, convenience stores and nightlife venues will continue supporting single-serve consumption. E-commerce and delivery platforms will expand assortment discovery, imported SKUs, bundles and limited-edition trials. Brazil’s large urban population and regional beverage culture provide a strong base for brands that can combine functional claims, affordability, taste localization and reliable distribution.

Major Players

- Red Bull Brasil

- Monster Energy Brasil

- Baly Brasil

- Grupo Petrópolis

- Ambev

- Britvic Brasil

- Coca-Cola Brasil

- PepsiCo Brasil

- Integralmedica

- Max Titanium

- Probiótica

- Bad Boy Energy Drink

- 220V Energy Drink

- Vibe Energy Drink

- Shark Energy Drink Brasil

Key Target Audience

- Energy drink manufacturers and brand owners

- Functional beverage companies

- Carbonated soft drink and non-alcoholic beverage companies

- Supermarket, hypermarket and cash-and-carry retail chains

- Convenience store, petrol station and travel retail operators

- Packaging manufacturers and aluminum can suppliers

- Investments and venture capitalist firms

- Government and regulatory bodies (ANVISA, Ministério da Agricultura e Pecuária, Ministério da Saúde, Conselho Administrativo de Defesa Econômica, Receita Federal do Brasil)

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map covering Brazil Energy Drink Market stakeholders, including brand owners, beverage manufacturers, importers, co-packers, distributors, retailers, gyms, nightlife venues, petrol stations, e-commerce platforms and regulators. Critical variables include retail sales, product type, packaging type, pack size, sugar profile, caffeine positioning, channel penetration and regional demand concentration.

Step 2: Market Analysis and Construction

In this phase, historical market data for Brazil Energy Drink Market is compiled and analyzed through company portfolios, retail availability, public market indicators, product claims, packaging formats and channel structure. The analysis assesses how supermarkets, cash-and-carry outlets, traditional trade, petrol stations, nightlife and online platforms contribute to revenue generation and brand visibility.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and validated through computer-assisted telephone interviews with beverage distributors, supermarket buyers, category managers, gym retailers, convenience operators, nightlife suppliers and co-packers. These consultations provide operational and commercial insights on SKU velocity, shelf placement, regional distribution, pack-size performance, promotional activity and formulation trends.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with energy drink manufacturers, beverage distributors and retail stakeholders to verify product segmentation, sales behavior, pricing architecture, consumer preferences and regional availability. Bottom-up findings are triangulated with top-down market indicators to ensure a validated assessment of Brazil Energy Drink Market size, segmentation, competition and future outlook.

- Executive Summary

- Research Methodology (market definitions and assumptions, RTD energy drink classification, stimulant beverage scope, non-alcoholic energy drink inclusion, caffeine and taurine formulation mapping, retail scan triangulation, distributor interviews, store audits, consumer occasion mapping, top-down and bottom-up market sizing)

- Definition and Scope

- Overview Genesis

- Timeline of Major Players

- Business Cycle

- Supply Chain and Value Chain Analysis

- Growth Drivers (urban youth consumption, nightlife culture, gym participation, functional beverage adoption, convenience retail expansion, guaraná familiarity)

- Market Challenges (caffeine scrutiny, sugar concerns, regulatory labeling, regional logistics, tax complexity, SKU saturation)

- Market Opportunities (zero sugar, natural caffeine, local flavors, protein energy, hydration energy, regional expansion, e-commerce, nightlife premiumization)

- Market Trends (functional stacking, flavor localization, large PET formats, sugar-free launches, influencer marketing, lifestyle sponsorships)

- SWOT Analysis

- Porter’s Five Forces

- By Value (2020-2025)

- By Volume (2020-2025)

- By Unit Sales (2020-2025)

- Market Share of Major Players on the Basis of Value and Volume

- Cross Comparison Parameters (caffeine mg per serving, sugar-free SKU mix, guaraná and botanical ingredient positioning, aluminum can and PET pack coverage, supermarket and cash-and-carry penetration, nightlife and event activation strength, regional distributor network, price-per-liter ladder)

- SWOT Analysis of Major Players

- Detailed Profiles of Major Companies

Red Bull Brasil

Monster Energy Brasil

Baly Brasil

Grupo Petrópolis

Ambev

Britvic Brasil

Coca-Cola Brasil

PepsiCo Brasil

Integralmedica

Max Titanium

Probiótica

Bad Boy Energy Drink

220V Energy Drink

Vibe Energy Drink

Shark Energy Drink Brasil

- Market Demand and Utilization

- Purchasing Power and Budget Allocation

- Needs, Desires and Pain Point Analysis

- Decision-Making Process

- Consumer Cohort Analysis

- By Value (2026-2035)

- By Volume (2026-2035)

- By Unit Sales (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now