Download PDF

Download PDFMarket Overview

The Brazil Fashion Accessories Market is valued at approximately USD ~ billion in 2025, reflecting a robust consumer demand for items such as jewelry, handbags, belts, wallets, eyewear, and watches. This substantial market size is supported by rising discretionary spending, a growing middle‑class population with increasing fashion consciousness, and expanding online and omnichannel retail platforms. Jewelry remains a leading revenue contributor due to its cultural prominence and high unit value.

Within Latin America, Brazil leads the regional fashion accessories market owing to its large population, diversified retail landscape, and strong domestic production of leather goods and jewelry. Major urban centers such as São Paulo, Rio de Janeiro, and Porto Alegre serve as fashion and retail hubs because of high consumer purchasing power, concentration of international and local fashion brands, and extensive retail infrastructure, which collectively enhance market activity and trend adoption.

Market Segmentation

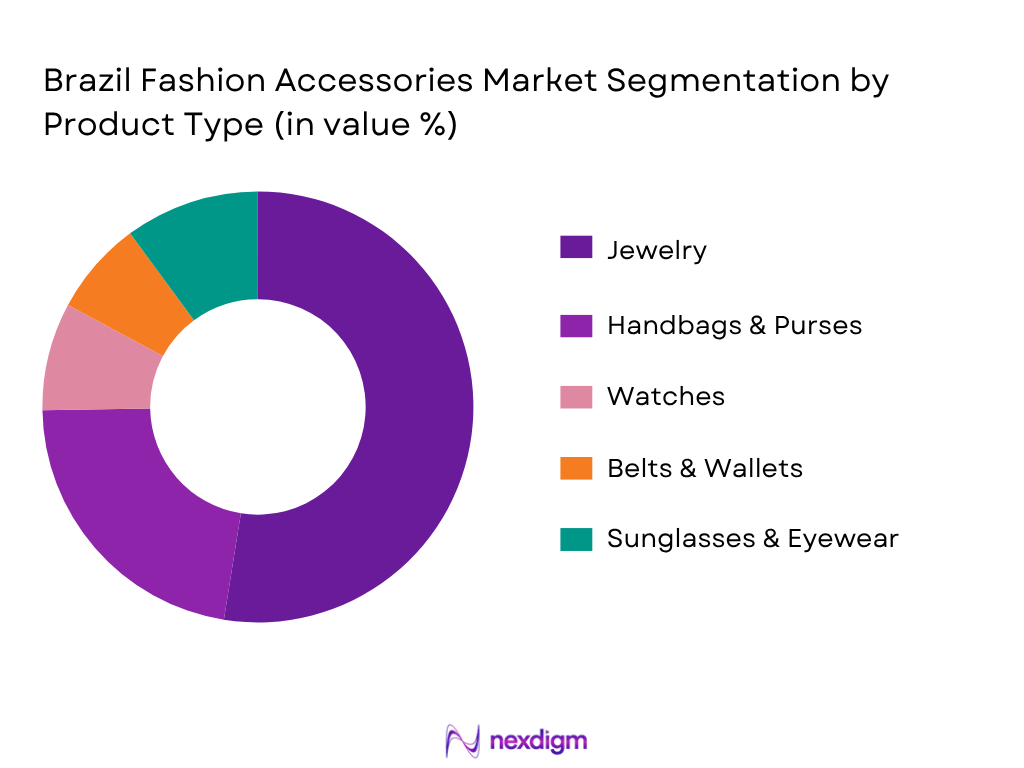

By Product Type

The market is heavily led by Jewelry in Brazil, primarily due to its cultural and socio‑economic significance. Jewelry is deeply entrenched in occasions, gifting practices, and fashion expression, driving substantial retail activity across both mass and premium tiers. Local production of semi‑precious and artisanal jewelry enhances accessibility while established international brands cater to affluent consumers, ensuring sustained demand across demographic groups. In addition, handbags & purses capture significant share by combining functional utility with fashion appeal, particularly in urban metropolitan centers where lifestyle shopping is prominent and smartphone‑driven e‑commerce influences seasonal trends.

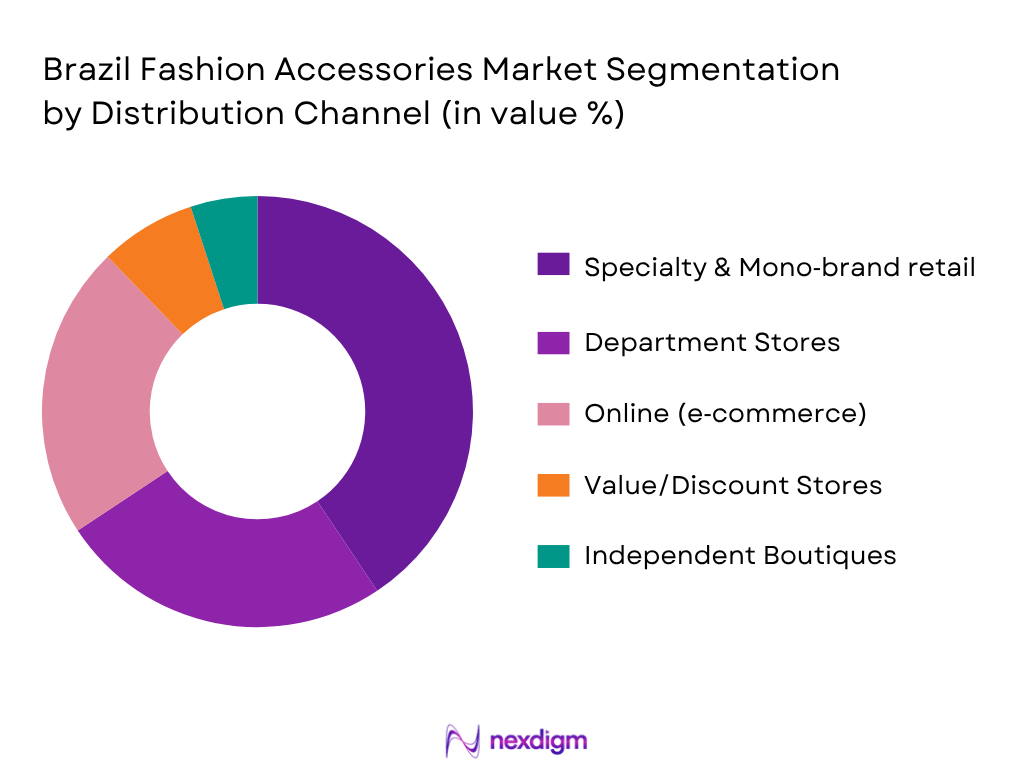

By Distribution Channel

The Specialty & Mono‑Brand Retail segment dominates the Brazil fashion accessories landscape, driven by the presence of standalone brand stores and premium boutiques that offer curated product assortments and experiences. These channels appeal to both fashion‑savvy consumers and tourists in urban centers, supporting strong brand visibility and higher average transaction values. Department stores maintain relevance through broad product offerings and promotional initiatives, while the online channel continues rapid growth as mobile commerce penetration deepens and social commerce expands among younger demographics seeking trendier and more affordable accessory options.

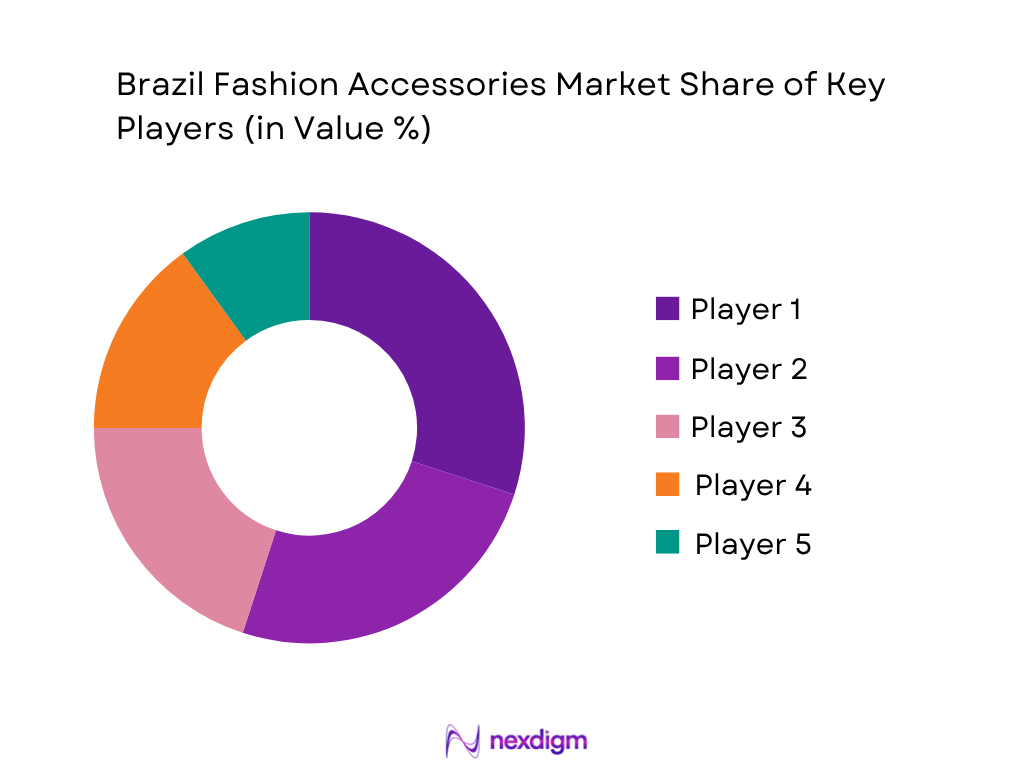

Competitive Landscape

The Brazil fashion accessories market is characterised by a mix of strong domestic brands and major global players. This consolidation underscores the influence of established firms on design trends, pricing power, and retail distribution strategies, while also highlighting significant investment in e‑commerce and omnichannel integration.

| Company | Est. Year | Headquarters | Product Scope | Distribution Reach | Brand Positioning | Digital Presence | Local Production Share |

| Arezzo & Co | 1972 | Brazil | ~ | ~ | ~ | ~ | ~ |

| Havaianas | 1962 | Brazil | ~ | ~ | ~ | ~ | ~ |

| Schutz | 1995 | Brazil | ~ | ~ | ~ | ~ | ~ |

| Louis Vuitton | 1854 | France | ~ | ~ | ~ | ~ | ~ |

| Gucci | 1921 | Italy | ~ | ~ | ~ | ~ | ~ |

Brazil Fashion Accessories Market Analysis

Growth Drivers

Rising Disposable Income

Brazil’s economy supports stronger consumer spending, which feeds directly into discretionary spending such as fashion accessories. In 2024, Brazil’s GDP per capita was approximately USD 10,616, reflecting a sustained capacity for household expenditure on non‑essential goods amid economic growth and labor market improvements. Consumer demand is bolstered by household final consumption expenditure reaching around USD 1.3 million, the market value of all goods and services purchased by households, representing ongoing demand for durable and fashion goods across income groups. In addition, Brazil’s unemployment rate remained low (modeled ILO estimate at 6.0% in 2025) and average wages increased, contributing to greater disposable income available for fashion accessory purchases across urban centers such as São Paulo and Rio de Janeiro, where higher incomes correlate with stronger retail activity and higher lifestyle spending.

Middle Class Fashion Spend

Brazil’s large population of over 211 million people includes a robust middle class with increasing purchasing power for lifestyle and discretionary items. Household consumption has been growing, with final consumption expenditure climbing year‑on‑year to over USD 1.38 trillion, indicating sustained retail demand even amid broader macroeconomic pressures. This expanding middle class prioritizes lifestyle and fashion goods, driving sales of jewelry, handbags, and accessories that combine aesthetic appeal with perceived value. The growth in household consumption also parallels higher labor force participation and real wage increases, which improve spending capacity. Urban centers like São Paulo and Rio de Janeiro exhibit the highest concentration of middle‑income households and retail infrastructure, making them focal points for fashion accessory demand due to deeper retail penetration and trend adoption compared with other regions.

Market Barriers

Import Tariff Pressures & Exchange Risk

Brazil’s import environment presents structural challenges for fashion accessories that rely on imported inputs or finished products. According to the World Bank’s World Integrated Trade Solution data, Brazil’s trade‑weighted average tariff is around 7.86%, with a simple average tariff across product imports near 13.35%, reflecting significant customs duties on various imported goods and raising the landed cost of fashion accessories that depend on foreign materials or components. These tariffs can dampen price competitiveness relative to locally produced alternatives, particularly for imported luxury items or components such as metals and textiles used in jewelry and handbags. Concurrently, the Brazilian real’s exchange rate volatility impacts cost structures for importers and retailers. Businesses active in Brazil must navigate a tariff regime that elevates the cost base for imported accessory inventory while balancing pricing strategies to maintain consumer demand in a price‑sensitive market.

Counterfeit & Grey Market Impact

The fashion accessory market in Brazil faces supply‑side distortions from counterfeit and grey market products, which undermine legitimate retail channels. While formal economic data on the value of these markets is limited, their presence is recognized in urban fashion districts and informal retail segments where lower‑priced accessory knockoffs circulate widely. These unofficial channels erode the pricing power of authentic brands and redirect consumer spend toward untaxed or unregulated merchandise. Counterfeit goods often enter through informal import networks, taking advantage of tariff and enforcement gaps, making it harder for licensed retailers to compete on price and authenticity. The prevalence of these products can also negatively affect brand reputation when consumers mistakenly associate quality issues with legitimate brands, deterring investment in premium accessory segments and complicating efforts to standardize quality and consumer trust across the market.

Opportunities

Sustainability & Ethical Fashion Accessories

Consumer interest in sustainable and ethically produced accessories presents a growth pathway within the Brazil market. While direct national consumer data for fashion sustainability preference is not consistently available, broader indicators show that global and regional consumer segments increasingly value environmentally responsible products. Brazil’s vast renewable resources and industrial base position it to expand production of eco‑friendly leather alternatives and recycled metal jewelry components. Designers and brands like Osklen are pioneering sustainable fashion concepts domestically, emphasizing conscious production and materials that resonate with socially aware consumers. As internet use in Brazil reached 84% of the population, digital platforms enable wider exposure and availability of eco‑centric accessory ranges to a large online audience receptive to ethical brand narratives. This structural digital reach supports consumer discovery and adoption of sustainable products, presenting brands and retailers with an opportunity to differentiate offerings and build loyalty among environmentally and socially conscious buyers.

Omnichannel & AR/VR Retail Experiences

The ongoing digitalization of retail in Brazil creates an opportunity for fashion accessory brands to expand their presence through omnichannel and immersive shopping technologies. Brazil’s internet penetration of 84% and rapid mobile connectivity form the foundation for digital engagement strategies that integrate online discovery with in‑store fulfillment. Retailers can leverage augmented reality (AR) and virtual reality (VR) applications to enhance consumer experience, allowing users to virtually try on accessories and interact with products remotely a particularly appealing feature for high‑engagement categories like eyewear and jewelry. Omnichannel models also improve inventory visibility and conversion by linking physical showrooms with e‑commerce platforms, enhancing customer reach beyond metropolitan centers. As digital commerce continues to mature, retailers that invest in AR/VR and seamless cross‑channel experiences will be better positioned to capture digitally engaged consumers and drive incremental revenue within the Brazil fashion accessories ecosystem.

Future Outlook

Over the next decade, the Brazil Fashion Accessories Market is expected to exhibit sustained expansion driven by the maturation of its digital retail ecosystem, rising discretionary consumption, and increasing appetite for branded and premium accessories among millennials and Gen Z. Growth in demand for personalized and sustainable products, combined with enhanced logistics and mobile payment adoption, is likely to reinforce market potential. E‑commerce, social commerce channels, and experiential retail will further shape competitive dynamics as companies adapt product and service models to evolving consumer behaviors. The market is projected to grow at a CAGR of approximately 7.6% from 2026 to 2035, reflecting ongoing expansion across product segments and distribution channels, although growth pace may vary across categories and consumer cohorts.

Major Players

- Arezzo & Co

- Havaianas

- Schutz

- Louis Vuitton

- Gucci

- Michael Kors

- Tiffany & Co.

- Hermes International

- Prada

- Chanel

- Burberry

- Ray‑Ban (Luxottica)

- Fossil Group

- Coach

- Tommy Hilfiger

Key Target Audience

- Retail & Fashion Brands

- E‑commerce Platforms & Marketplaces

- Investments and Venture Capitalist Firms

- Private Equity and Strategic Investors

- Luxury Goods Importers & Distributors

- Government and Regulatory Bodies (Ministry of Industry & Commerce, Ministry of Economy – Foreign Trade)

- Retail Real Estate Developers

- Supply Chain & Logistics Service Providers

Research Methodology

Step 1: Identification of Market Variables

The initial phase involved defining fashion accessory categories, key consumer cohorts, pricing tiers, and distribution channels through comprehensive desk research using credible industry databases. Critical factors influencing market size and growth were identified to ensure analytical precision.

Step 2: Data Collection and Market Construction

Historical sales and revenue data were compiled from proprietary sources, industry reports, and retailer disclosures. Market values and channel contributions were normalized and analyzed to derive comprehensive revenue estimates across segments.

Step 3: Expert Validation and Interviews

Market assumptions and preliminary models were validated through structured consultations with industry practitioners, including brand managers, retail specialists, and fashion industry analysts, enhancing accuracy of interpretation.

Step 4: Synthesis and Forecast Modeling

Final outputs were produced using integrated top‑down and bottom‑up techniques. Forecasts were modeled through statistical projection, incorporating macroeconomic indicators, consumer behavior trends, and competitive positioning dynamics.

- Executive Summary

- Introduction & Research Approach (Market Definitions & Accessory Taxonomy, Assumptions & Abbreviations, Data Sources & Quality Controls, Market Sizing Methodology (Top‑down & Bottom‑up Integration), Forecast Methodology (Scenario & Sensitivity Layers), Limitations & Reliability Matrix)

- Market Genesis & Evolution

- Cultural & Consumption Drivers in Brazil

- Value Chain; Raw Materials to Retail

- Regulatory, Brazil Import/Export Regimes & Duty Impact

- Currency, Inflation & Retail Price Dynamics

- COVID‑19 Aftermath & Digital Acceleration Effects

- Growth Drivers (Rising Disposable Income, Middle‑Class Fashion Spend, Digital & Mobile Commerce Acceleration, Social Media & Influencer‑Driven Trends, Premiumisation & Aspirational Purchases)

- Market Barriers (Import Tariff Pressures & Exchange Risk, Counterfeit & Grey‑Market Impact, Infrastructure Gaps Outside Urban Centers)

- Opportunities (Sustainability & Ethical Fashion Accessories, Omnichannel & AR/VR Retail Experiences, Local Artisanal Craft Integration, Tier‑2/3 City Retail Potential)

- Emerging Trends (Fast Fashion vs Slow Fashion Polarisation, Rise of D2C & Social Commerce, Smart/Tech‑Infused Accessories, E‑commerce Personalisation)

- Regulatory Landscape (Brazil Ministry of Industry & Commerce regulations, Ministry of Economy Foreign Trade tariffs, INMETRO quality certifications, ABNT standards for leather & metal accessories, customs compliance, import/export licensing, environmental regulations for sustainable production)

- Value Chain and Supply Chain Analysis (raw material sourcing (local vs imported), converter and artisan workshops, manufacturing & finishing nodes, distribution to retail & e-commerce, quality assurance protocols, logistics network coverage, inventory turnover and seasonal demand alignment)

- SWOT Analysis of Industry

- Stakeholder Ecosystem (Suppliers, Retailers, Distributors, Government)

- Porter’s Five Forces Analysis

- Competitive Landscape Overview

- By Total Market Value (2020-2025)

- By Volume & Unit Sales (2020-2025)

- By Average Retail Pricing Movements (2020-2025)

- By Price Index (2020-2025)

- By Product Type (In Value%)

Jewelry

Handbags & Purses

Eyewear

Watches

Belts & Wallets

Scarves, Hats & Fashion Add‑ons - By End‑User Demographic (In Value%)

Women

Men

Unisex Essentials

Children & Teens

Age Cohorts - By Distribution Channel (In Value%)

Specialty Fashion Retailers

Department Stores & Luxury Shops

E‑commerce

Value Retail

Independent Boutiques

Omnichannel Integration - By Price Positioning (In Value%)

Mass Market

Mid‑Tier

Premium

Luxury/Limited Editions - By Region (In Value%)

Southeast

South

Northeast

Central West

North

- Competitive Landscape and Market Concentration (top domestic & international brands’ market dominance, market fragmentation, pressure from emerging local & online-first brands, portfolio depth across jewelry, handbags, belts, eyewear)

- Market Share of Major Players by Value and Volume (overall retail value share, segment-wise share (jewelry, bags, eyewear), channel-specific share (offline vs online), branded vs private label penetration)

- Cross‑Comparison Parameters (Brand Positioning & Price Tier, Product Portfolio Depth & SKU Strategies, Channel Penetration & Digital Strategy, Distribution & Retail Footprint, Marketing & Social Engagement Index, Local Sourcing & Import Ratio, Supply Chain Resilience & Lead Times, Sustainability & ESG Footprint)

- Category-Claim Benchmarking (luxury, premium, mid-tier, artisanal/craft, eco-conscious, tech-enabled/smart accessories, urban streetwear, traditional leather & metal products)

- SKU Pricing and Pack Architecture Analysis (price per unit/accessory type, promotion depth, product range ladder (entry to premium), product sizing & bundling, seasonal price adjustments)

- SWOT Analysis (strengths, weaknesses, opportunities, threats of major competitors in Brazil fashion accessories market)

- Certifications, Claims, and Innovation Benchmarking (“Made in Brazil” claims, eco-sustainability certifications, artisanal authenticity proofs, innovation cadence, hero product launches, limited-edition or custom offerings)

- Detailed Profiles of Key Competitors

Arezzo & Co

Havaianas

Schutz

Le Postiche

Baggage

Cartier

Louis Vuitton

Gucci

Michael Kors

Tiffany & Co.

Ray‑Ban

Fossil Group

H&M

Shein

Temu

- Buyer Cohort Profiling (age groups, income brackets, gender, urban/rural residence, fashion-consciousness level, lifestyle & cultural orientation, aspirational purchasing behavior)

- Purchase Drivers and Barriers (brand perception, design & trend relevance, price sensitivity, material quality, durability, authenticity, accessibility across channels, counterfeit risk)

- Shopper Journey and Decision Process (social media, influencers, fashion shows, trial triggers (limited editions, discounts), peer reviews & word-of-mouth influence, conversion friction (price, availability, fit), repurchase motivation)

- Channel Behavior Analysis (discovery channels, purchase channels, replenishment behavior, basket mission)

- Basket Composition and Repurchase Economics (cross-sell of complementary accessories, attach rate of small items with high-ticket items, seasonal purchase cycles, bundle uptake, average ticket size, purchase frequency)

- By Total Market Value (2026-2035)

- By Volume & Unit Sales (2026-2035)

- By Average Retail Pricing Movements (2026-2035)

- By Price Index (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now