Download PDF

Download PDFMarket Overview

The Brazil food acidulants market was valued at USD ~ billion in 2024 and is projected to expand at a CAGR of ~% during the 2026–2035 forecast period. According to industry data published by the Brazilian Food Processors’ Association (ABIA), Brazil’s food and beverage processing sector generated revenues exceeding BRL 1.1 trillion, with food ingredients including acidulants forming an integral part of the country’s industrial food manufacturing base. Data from ANVISA (National Health Surveillance Agency) and the Brazilian Institute of Geography and Statistics (IBGE) indicates that food additive consumption continues to grow in line with rapid expansion of the processed food, beverage, dairy, bakery, and meat processing industries. Growth is supported by rising consumer demand for packaged and convenience food products, increasing urbanization, expanding export of processed foods, and the shift toward natural and bio-based acidulant formulations across the food and beverage industry.

Market Segmentation

By Acidulant Type

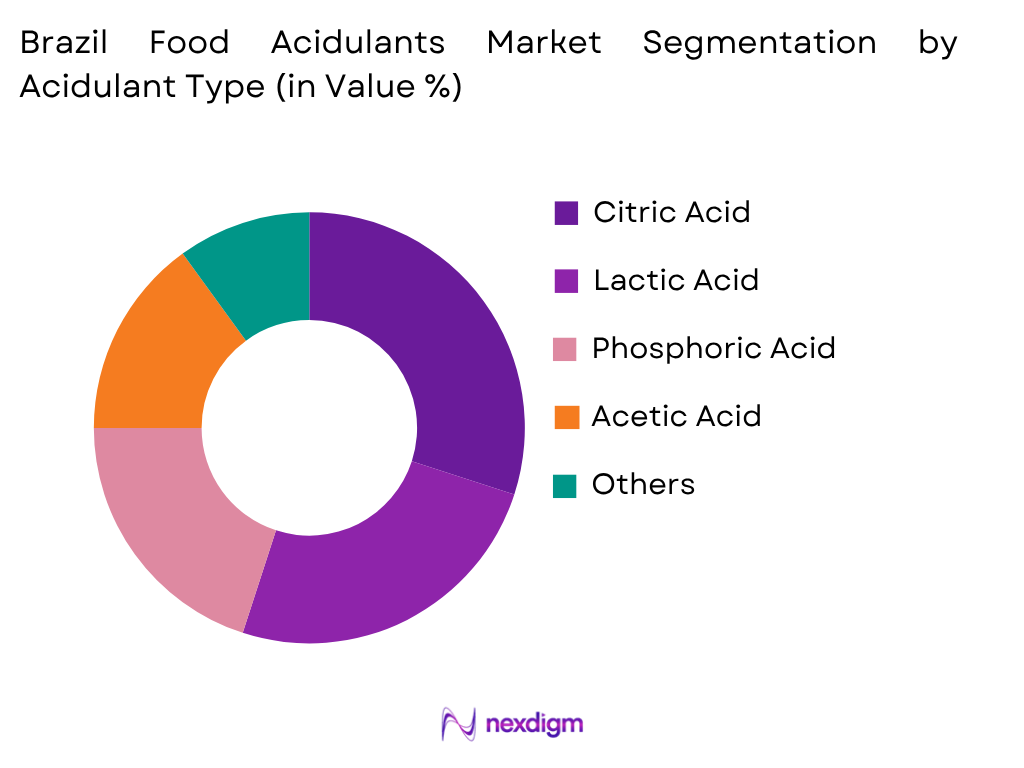

Citric acid dominates the Brazilian food acidulants market owing to its widespread versatility, affordability, and multifunctional properties across the food and beverage sectors. According to market data, citric acid accounts for approximately 45% of the total food acidulants market value, driven by its extensive use in carbonated soft drinks, fruit juices, confectionery, bakery products, dairy items, and processed foods. Its natural occurrence in citrus fruits and its capacity to enhance flavor, regulate pH, act as a preservative, and synergize with antioxidants make it the preferred acidulant across virtually all food processing categories. Brazil’s well-developed sugarcane and molasses supply base supports domestic production of citric acid through fermentation processes, providing cost advantages for local manufacturers. In April 2024, Tate & Lyle announced an expansion of its Brazilian operations specifically focused on increasing citric acid supply to meet growing beverage industry demand, reflecting the segment’s commercial importance. Lactic acid represents the second major segment, used extensively in dairy fermentation, processed meats, bakery leavening, and increasingly in plant-based food formulations. Its mild acidity and compatibility with clean-label positioning have made it a growing choice among food manufacturers seeking natural preservation and flavoring alternatives. Phosphoric acid maintains a significant share primarily within the carbonated beverage segment, while malic, tartaric, and fumaric acids serve specialized applications in confectionery, wine, and bakery.

By Application

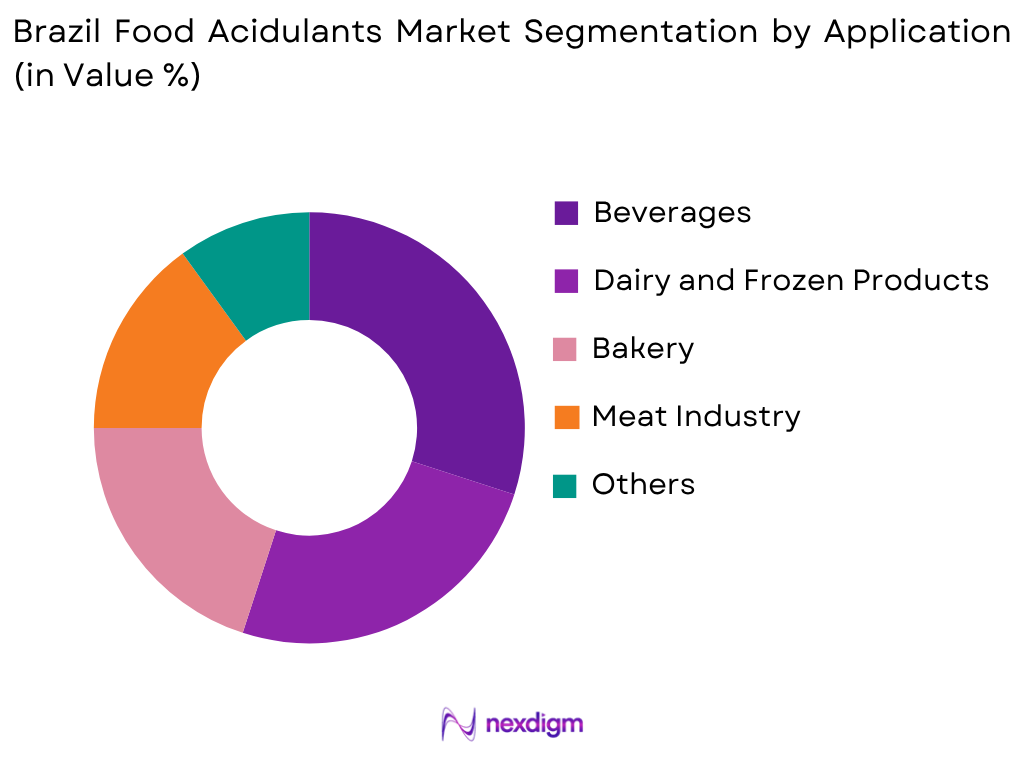

Beverages account for the largest application share of the Brazil food acidulants market, representing approximately 32% of total market value, driven by the extensive use of acidulants for pH regulation, flavor enhancement, and preservation in carbonated drinks, fruit juices, energy drinks, and functional beverages. Brazil’s beverage industry is among Latin America’s largest, with a population exceeding 212 million consumers demanding a wide range of soft drinks, juices, isotonic drinks, and ready-to-drink functional beverages. The growth of premium and functional beverage segments has further accelerated acidulant demand, as manufacturers formulate products with clean-label acids, reduced sugar profiles, and enhanced nutritional content. The dairy and frozen products segment represents the second largest application, with lactic acid used extensively in cheese, yogurt, sour cream, and fermented dairy production. Brazil is among the world’s leading dairy producers, and the continued expansion of value-added dairy products increases industrial demand for specialized acidulants. The bakery segment also relies significantly on acidulants for leavening, pH control, shelf-life extension, and texture modification across bread, cakes, biscuits, and pastry production. Meat processing represents a further important application, with acidulants used to control pH, inhibit microbial growth, extend shelf life, and maintain colour stability in processed and cured meat products.

Competitive Landscape

The Brazil food acidulants market is moderately fragmented, with multinational ingredient companies competing alongside regional distributors and specialized chemical suppliers. Global companies such as Cargill, ADM, Tate & Lyle, Corbion, and Kemin Industries leverage extensive distribution networks, proprietary fermentation and processing technologies, and comprehensive food ingredient portfolios to maintain strong market positions. Distribution specialists including Brenntag and Univar Solutions play a critical role in expanding the reach of international acidulant producers across Brazil’s diverse geographic market. Continuous investments in natural and bio-based acidulant development, sustainable sourcing, application innovation, and compliance with ANVISA regulatory requirements remain key competitive differentiators across the market.

| Company | Establishment Year | Headquarters | Primary Acidulant Portfolio | Key Application Industries

|

Manufacturing Presence | R&D Capability | Distribution Network | Clean Label Solutions |

| Corbion Brasil | 1919 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Tate & Lyle Brasil | 1921 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Cargill Brazil | 1965 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| ADM Brasil | 1902 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Brenntag Brasil | 1874 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

Brazil Confectionary Market Analysis

Growth Drivers

Rapid Expansion of the Processed Food and Beverage Sector

Brazil’s fast-growing food and beverage processing industry represents the primary structural growth driver for the food acidulants market. According to the Brazilian Food Processors’ Association (ABIA), Brazil’s food processing sector generated revenues exceeding BRL 1.1 trillion during 2024, marking continued robust expansion and reinforcing the country’s position as one of the world’s largest food manufacturing nations. The International Monetary Fund (IMF) estimated Brazil’s nominal GDP at more than USD 2.3 trillion, while the World Bank estimates GDP per capita above USD 10,000, reflecting an economy capable of sustaining substantial consumer demand for packaged and processed food products. According to IBGE, Brazil’s urban population exceeds 185 million, with more than 88% of the total population classified as urban, driving consistent demand for convenience foods, packaged snacks, ready-to-eat meals, and processed beverages that rely heavily on acidulants for flavoring, preservation, and pH management. Acidulants are essential functional ingredients across virtually every processed food category, including carbonated beverages, fruit juices, dairy products, cured meats, bakery items, confectionery, and soups, making market growth in the food acidulants segment closely correlated with the overall expansion of Brazil’s food manufacturing industry. Additionally, Brazil’s strong export performance in processed foods generates further industrial demand for food acidulants, as global buyers increasingly require preserved, shelf-stable products that comply with international food safety standards and extended shelf-life requirements.

Rising Demand for Natural, Bio-Based, and Clean-Label Acidulants

The accelerating shift toward natural, fermentation-derived, and clean-label acidulants is one of the most significant recent structural trends reshaping the Brazil food acidulants market. Brazilian consumers are increasingly demanding transparency in food labeling, with rising health and wellness consciousness driving manufacturers to reformulate products using recognizable, naturally derived ingredients. According to IMARC Group, Brazil’s health and wellness market reached USD 91.3 billion in 2025, reflecting the scale of the consumer movement toward healthier food formulations. ANVISA’s implementation of enhanced front-of-pack nutritional labeling under RDC 843/2024 has further accelerated this trend, requiring food manufacturers to disclose products containing high levels of added sugars, saturated fats, and sodium, indirectly encouraging reformulation efforts that favour natural acidulants over synthetic food additives. Citric acid derived from citrus fermentation processes and lactic acid produced through microbial fermentation of sugar substrates are gaining significant commercial traction as clean-label alternatives to phosphoric acid and synthetic acidulants in beverages, dairy, and confectionery applications. In February 2024, Corbion launched a new line of bio-based food acidulants in Brazil, specifically targeting the growing demand for sustainable, fermentation-derived preservation and flavoring solutions in processed foods. These developments reflect growing commercial momentum behind bio-based acidulants and create premium differentiation opportunities for manufacturers supplying natural and certified ingredient solutions to Brazil’s evolving food and beverage industry.

Market Challenges

Raw Material Price Volatility and Import Dependency

Brazilian food acidulant manufacturers and distributors continue facing significant challenges arising from raw material price volatility and dependency on imported specialty acids and chemical precursors. The production of citric acid relies on fermentation substrates including molasses, corn starch, and sugars, whose prices are influenced by agricultural cycles, climate conditions, and commodity market dynamics. According to IBGE, fluctuations in Brazil’s sugarcane harvests and corn production directly affect the cost base for domestically produced citric acid, creating margin variability for both producers and food manufacturers. Specialty acidulants such as malic acid, tartaric acid, fumaric acid, and certain grades of phosphoric acid continue to be largely imported, exposing Brazilian food manufacturers to foreign exchange volatility. The Brazilian Real’s fluctuation relative to the US Dollar and Euro materially increases the cost of imported acidulant ingredients, creating procurement uncertainty for food and beverage companies managing tight formulation budgets. According to the Central Bank of Brazil, the currency has experienced significant exchange rate movements in recent years, directly affecting the import cost of specialty food ingredients. Additionally, global supply chain disruptions arising from geopolitical tensions, logistics congestion, and manufacturing capacity constraints in major acidulant-producing countries have created supply availability challenges. Food manufacturers must therefore invest in procurement diversification, strategic inventory management, and long-term supply agreements to manage the risks of raw material cost volatility and import dependency.

ANVISA Regulatory Compliance and Evolving Labeling Requirements

Brazil’s stringent food additive regulatory framework, administered by ANVISA (National Health Surveillance Agency), represents an ongoing compliance challenge for acidulant manufacturers, distributors, and food processing companies operating in the market. ANVISA maintains comprehensive permitted lists of food additives and acidulants under Resolution RDC standards, requiring products to comply with established purity specifications, maximum usage levels, and application-specific authorizations. The process for registering new acidulant ingredients or modifying approved usage parameters involves extensive documentation, laboratory testing, safety assessments, and prolonged regulatory review timelines that increase costs and delay market access for innovative acidulant products. The implementation of ANVISA’s enhanced front-of-pack nutritional warning labeling system under RDC 843/2024 has further increased formulation complexity for food manufacturers, who must evaluate the cumulative impact of acidulants and other functional ingredients on final product nutritional profiles to ensure compliance. According to industry data, compliance with evolving ANVISA requirements can be particularly burdensome for small and medium-sized food processing companies, which may lack dedicated regulatory affairs resources to navigate the complexity of Brazil’s food additive approval framework. Companies investing in regulatory expertise, technical compliance capabilities, and proactive engagement with ANVISA processes are better positioned to maintain uninterrupted market access and develop differentiated product offerings that meet evolving Brazilian food safety and labeling standards.

Market Opportunities

Expansion of Bio-Based and Fermentation-Derived Acidulant Production

Brazil’s well-established sugarcane, corn, and agricultural feedstock base presents significant long-term opportunities for expanding domestic bio-based and fermentation-derived acidulant production. Brazil is the world’s largest sugarcane producer, according to the Ministry of Agriculture and Livestock (MAPA), providing abundant and competitively priced fermentation substrates for the biological production of citric acid, lactic acid, and other organic acids. Investments in advanced fermentation technologies, strain optimization, and bioprocess engineering offer the potential to expand domestic acidulant production capacity while reducing Brazil’s dependence on imported specialty acids. The global trend toward bio-based and sustainably sourced food ingredients is creating premium market opportunities for Brazilian producers able to supply certified, fermentation-derived acidulants that meet the clean-label and sustainability procurement requirements of major food and beverage manufacturers worldwide. Enterprise and research investment in this segment is gaining momentum, with Corbion’s February 2024 launch of a new bio-based acidulant line in Brazil illustrating the commercial viability of this opportunity. Furthermore, growing consumer preference for fermentation-derived lactic acid in plant-based food formulations, probiotic-enriched dairy alternatives, and functional beverages is expected to sustain demand growth for bio-based organic acids across the food processing industry. Companies investing in renewable feedstock procurement, fermentation innovation, and sustainable production infrastructure are well positioned to capture premium market opportunities in Brazil’s evolving food acidulants landscape.

Growing Application in Functional, Fortified, and Plant-Based Food Products

The rapid growth of functional, fortified, and plant-based food categories in Brazil is creating expanding new demand for specialized acidulant applications. According to the Good Food Institute, approximately 26% of Brazilians consume plant-based meat products at least once per month, while 5% identify as vegan or vegetarian, driving sustained demand for plant-based food formulations that require acidulants for pH control, flavor enhancement, preservation, and texture modification. The International Diabetes Federation estimates that Brazil had 16.6 million adults living with diabetes as of 2024, rising to a projected 24.0 million by 2050, creating significant consumer demand for reduced-sugar and functional food products in which acidulants play critical formulation roles. The functional beverage segment is among the fastest-growing categories in Brazil’s food industry, with manufacturers introducing energy drinks, sports hydration products, probiotic beverages, and fortified juices that rely on citric acid, malic acid, and lactic acid for flavor balance, pH optimization, and stability. Brazil’s nutraceutical and dietary supplement market is also expanding, with acidulants used in the production of effervescent tablets, fortified food systems, and functional dairy ingredients. Companies that invest in application-specific acidulant formulation expertise, technical support for food manufacturers, and collaborative innovation with beverage and functional food producers are well positioned to capture premium growth opportunities across Brazil’s evolving health-oriented food and beverage landscape.

Future Outlook

The Brazil food acidulants market is expected to witness sustained growth throughout the forecast period, supported by continued expansion of the food and beverage processing industry, rising consumer demand for natural and clean-label ingredients, and increasing application of acidulants in functional, fortified, and plant-based food products. Manufacturers are increasingly investing in bio-based fermentation technologies, sustainable raw material sourcing, and innovative multifunctional acidulant systems to meet evolving food manufacturer and consumer requirements. Growing penetration of premium functional beverages, expansion of the dairy processing sector, and ongoing product innovation in bakery, confectionery, and meat processing are expected to create additional demand across acidulant categories. Continued compliance with ANVISA regulatory developments and investments in sustainable production infrastructure will further strengthen long-term market competitiveness.

Major Players

- Cargill Brasil

- Tate & Lyle Brasil

- ADM Brasil

- Corbion Brasil

- Brenntag Brasil

- Kemin Industries Brasil

- Ingredion Brasil

- Kerry Brasil

- BASF Brasil

- DuPont Nutrition & Biosciences Brasil

- Univar Solutions Brasil

- Jungbunzlauer Brasil

- Prinova Brasil

- Naturex Brasil

- Parchem Brasil

Key Target Audience

- Food and Beverage Manufacturers and Industrial Processors

- Food Ingredient Distributors and Specialty Chemical Distributors

- Pharmaceutical and Nutraceutical Manufacturers

- Dairy, Meat, and Bakery Processing Companies

- Beverage Producers and Functional Food Manufacturers

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies (ANVISA, Ministry of Agriculture and Livestock (MAPA), Brazilian Institute of Geography and Statistics (IBGE), Brazilian Food Processors’ Association (ABIA))

- Research Institutions and Food Technology Innovation Centres

Research Methodology

Step 1: Identification of Key Variables

The research begins by identifying the major stakeholders across the Brazil food acidulants value chain, including raw material suppliers, acidulant producers, specialty ingredient distributors, food and beverage manufacturers, end-user industry associations, and regulatory authorities. Extensive secondary research is conducted using government publications, ANVISA regulatory databases, industry association reports, trade publications, and proprietary databases to establish the key variables influencing market performance.

Step 2: Market Analysis and Construction

Historical market information is compiled and evaluated to estimate the overall market size, acidulant type penetration, application volumes, consumption trends, pricing dynamics, and revenue generation across major categories. Both demand-side and supply-side indicators are analyzed using bottom-up and top-down market sizing approaches to ensure comprehensive market coverage across Brazil’s diverse food processing sectors.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary market estimates and analytical assumptions are validated through Computer Assisted Telephone Interviews (CATIs) and structured discussions with acidulant producers, ingredient distributors, food and beverage manufacturers, procurement specialists, regulatory affairs experts, and industry consultants. These interviews provide valuable commercial insights that strengthen the reliability and accuracy of market estimates.

Step 4: Research Synthesis and Final Output

The final stage integrates primary research findings with secondary information to develop a comprehensive assessment of market size, segmentation, competitive landscape, end-user behaviour, and future opportunities. Multiple validation techniques, including data triangulation and cross-verification, are employed to ensure the consistency, accuracy, and credibility of the final market report.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Taxonomy, Market Sizing Approach, Top-Down Analysis, Bottom-Up Analysis, Demand-Side Assessment, Supply-Side Assessment, Primary Industry Interviews, Secondary Research Validation, Data Triangulation, Forecasting Framework, Limitations and Future Conclusions)

- Definition and Scope

- Market Evolution and Industry Genesis

- Timeline of Major Industry Developments

- Industry Value Chain Analysis

- Supply Chain Analysis

- Growth Drivers (Rapid Expansion of Processed Food Sector, Rising Beverage Industry Demand, Growing Ultra-Processed Food Consumption, Urbanization and Changing Lifestyles, Clean-Label and Natural Acidulant Trend, Expansion of Functional & Fortified Foods, Growing Dairy and Meat Processing Industry, Strong Export of Processed Foods)

- Market Challenges (Raw Material Price Volatility, ANVISA Regulatory Compliance Burden, Import Dependency for Specialty Acidulants, Currency Volatility Impacting Input Costs, Competition from Acidulant Substitutes, Side Effects Awareness Limiting Demand in Certain Segments)

- Market Opportunities (Bio-Based and Fermentation-Derived Acidulant Innovation, Functional Beverage Expansion, Organic & Clean-Label Product Reformulation, Citric Acid Capacity Expansion, Export Market Growth, Application in Plant-Based Foods)

- Market Trends (Shift Toward Natural and Fermentation-Derived Acidulants, Clean-Label Formulation, Reduced Sugar and Acid Product Innovation, Bio-Acidulant R&D Investment, Sustainable Sourcing Practices, Multifunctional Acidulant Formulations)

- Government Regulations (ANVISA Food Additive Standards, RDC 843/2024 Front-of-Pack Labeling, Nutritional Labeling Requirements, Permitted Additive and Acidulant Lists, Import Regulations for Food Ingredients, Food Safety and Good Manufacturing Practice (GMP) Requirements)

- Raw Material Supply Analysis (Citrus Fruit & Molasses Availability, Corn & Starch Feedstock Supply, Import-Dependency for Specialty Acids, Pricing Dynamics, Domestic Agricultural Input Costs)

- Application Demand Analysis (Beverage Industry Demand, Dairy Sector Usage, Bakery & Confectionery Demand, Meat Processing Volumes)

- Innovation Landscape (Bio-Based Acidulant Launches, Multifunctional Ingredient Systems, Clean-Label Reformulation, Encapsulated Acidulants, Sustainable Production Technologies)

- Sustainability Analysis (Fermentation-Based Production, Sustainable Raw Material Sourcing, Carbon Footprint Reduction, Biodegradable Packaging for Acidulant Products)

- SWOT Analysis

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Stakeholder Ecosystem

- Competition Ecosystem

- By Market Value (2020-2025)

- By Volume Consumption (2020-2025)

- By Average Selling Price (2020-2025)

- By Acidulant Type (In Value %)

Citric Acid

Lactic Acid

Phosphoric Acid

Acetic Acid

Malic Acid

Tartaric Acid

Fumaric Acid

Other Acidulant Types - By Source (In Value %)

Natural / Bio-Based Acidulants

Synthetic Acidulants

Fermentation-Derived Acidulants

Mineral-Derived Acidulants

Organic & Clean-Label Acidulants - By Application (In Value %)

Beverages

Dairy and Frozen Products

Bakery

Meat Industry

Confectionery

Snacks & Convenience Foods

Other Applications - By End User (In Value %)

Food & Beverage Manufacturers

Pharmaceutical Companies

Foodservice & Industrial Processors

Nutraceutical Producers

Export-Oriented Processors - By Region (In Value %)

Southeast Brazil

South Brazil

Northeast Brazil

Central-West Brazil

North Brazil

- Market Share Analysis (By Value, Volume, Acidulant Type, Application Sector, Price Segment)

- Cross Comparison Parameters (Acidulant Portfolio Breadth, Bio-Based Product Range, Annual New Product Launches, Fermentation & Processing Capability, Distribution Reach Across Brazil, Application-Specific Portfolio Strength, Premium Product Mix, Manufacturing Capacity)

- SWOT Analysis of Major Players

- Pricing Analysis (By Acidulant Type, Purity Grade, Source, Application, Pack Size)

- Detailed Profiles of Major Companies

Cargill Brasil

Tate & Lyle Brasil

ADM Brasil

Corbion Brasil

Brenntag Brasil

Kemin Industries Brasil

Ingredion Brasil

Kerry Brasil

BASF Brasil

DuPont Nutrition & Biosciences Brasil

Univar Solutions Brasil

Jungbunzlauer Brasil

Prinova Brasil

Naturex Brasil

Parchem Brasil

- End-User Demand Pattern Analysis (Application Frequency, Formulation Preference, Functional Requirement, Seasonal Usage)

- Demographic End-User Analysis (Company Size, Industry Sector, Geographic Concentration, Processing Scale)

- Procurement Expenditure Analysis

- Premium vs Standard Acidulant Preference

- Brand Loyalty and Supplier Relationship Analysis

- Health & Clean-Label Purchase Behaviour

- Product Attribute Preference Analysis (Purity, Solubility, pH Range, Source, Regulatory Compliance, Price, Consistency)

- Bulk vs Packaged Procurement Behaviour

- Online vs Offline Procurement Behaviour

- Procurement Pain Point Analysis

- Supplier Selection Decision-Making Process

- By Market Value (2026-2035)

- By Volume Consumption (2026-2035)

- By Average Selling Price (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now