Download PDF

Download PDFMarket Overview

The Brazil Food Traceability Market was valued at USD ~ Billion in 2024 and is anticipated to expand at a CAGR of ~% during 2026-2035. The market is primarily driven by mandatory livestock traceability requirements introduced under the Ministry of Agriculture, Livestock and Supply’s (MAPA) National Livestock Traceability Plan, launched in December 2024, which establishes a phased rollout of individual animal identification with full mandatory compliance targeted by 2032. The market is further shaped by rising international compliance requirements, including the European Union’s Deforestation Regulation (EUDR), which took effect on December 30, 2025, and requires verifiable geolocation data for cattle, soy, coffee, and other commodities exported to the European Union. Brazil’s position as one of the world’s largest exporters of beef, soybeans, and coffee, combined with growing scrutiny from key trading partners including China and the European Union, continues to drive investment in RFID, blockchain, satellite monitoring, and other traceability technologies across the country’s agricultural export supply chains.

Market Segmentation

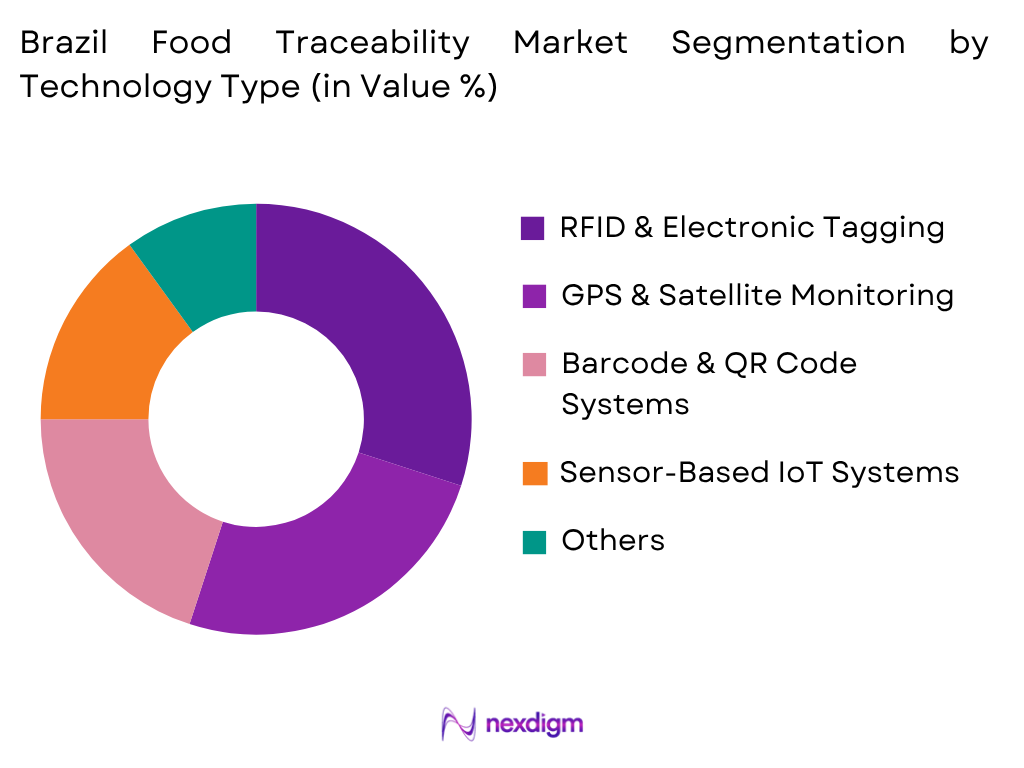

By Technology Type

Among these, RFID & Electronic Tagging holds the largest share of the Brazil Food Traceability Market, driven primarily by the country’s SISBOV (Brazilian System of Individual Identification of Cattle and Buffaloes) program, which relies on implantable microchips, electronic ear tags, and intraruminal boluses for radiofrequency-based animal identification. As MAPA’s National Livestock Traceability Plan advances toward mandatory individual identification for Brazil’s cattle herd, estimated at over 238 million animals, demand for durable, field-tested RFID tags capable of withstanding tropical ranch conditions continues to expand rapidly. Blockchain-Based Traceability represents the fastest-growing technology segment, supported by pilot programs between Brazilian exporters and international partners, including a 2024 Brazil-China beef traceability initiative aimed at aligning emission measurement methodologies and supporting China’s General Administration of Customs (GACC) digital inspection framework. GPS & Satellite Monitoring technologies are also gaining significant traction, driven by the need to verify deforestation-free sourcing under the EU Deforestation Regulation through integration with Brazil’s Rural Environmental Registry (CAR) and environmental embargo databases.

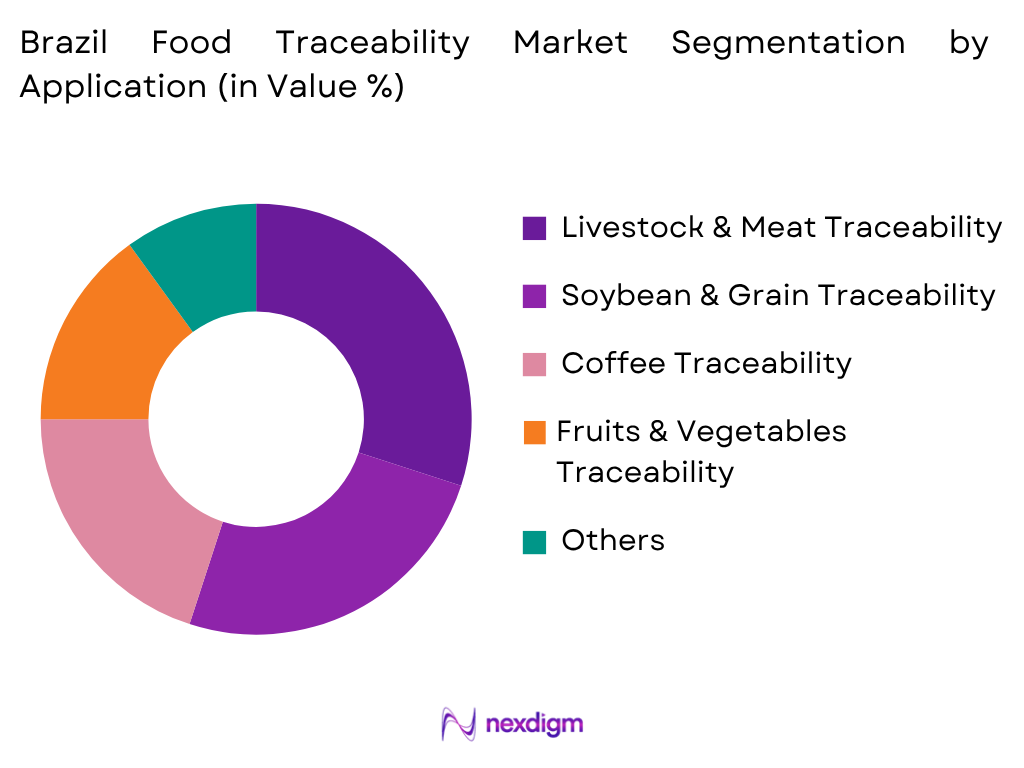

By Application

Livestock & Meat Traceability represents the largest application segment, reflecting the outsized role of Brazil’s cattle industry, which has contributed an average of approximately 30.2% of agribusiness GDP over the past decade and supplies beef to major export markets including China, which accounts for approximately 48% of Brazil’s beef export volume. The segment is directly shaped by MAPA’s SISBOV program and the phased National Livestock Traceability Plan, alongside growing requirements from export destinations for verifiable origin and sanitary documentation. Soybean & Grain Traceability represents the second-largest application, driven by Brazil’s position as a leading global soybean exporter, with the European Union requiring verifiable geolocation data for soy shipments under the EUDR beginning December 2025. Coffee Traceability is also expanding steadily, supported by growing specialty coffee export demand and similar EUDR-driven geolocation and deforestation-free sourcing requirements affecting Brazil’s coffee-growing regions.

Competitive Landscape

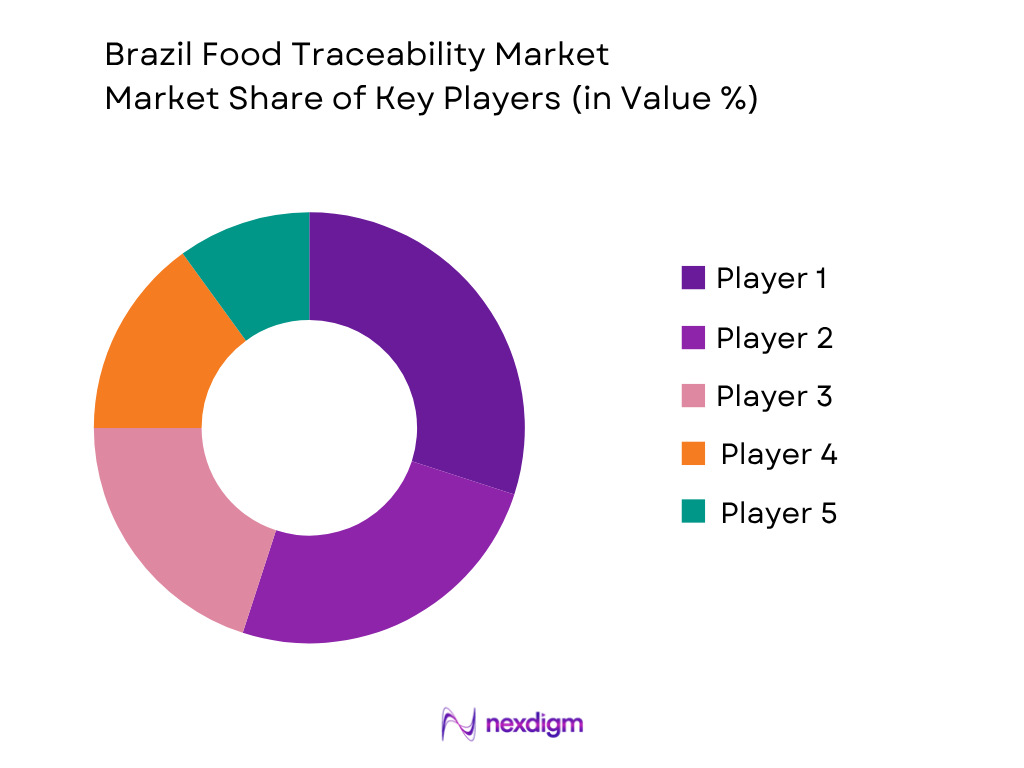

The Brazil Food Traceability Market is moderately fragmented, with global animal health and identification companies, international certification bodies, blockchain technology providers, and Brazilian agtech firms competing across different segments of the traceability value chain. Competition is primarily based on regulatory compliance coverage, technology reliability under field conditions, integration capability with government systems such as MAPA’s Agricultural Management Platform (PGA) and SISBOV, satellite and geolocation accuracy, and the ability to support export documentation for multiple international markets simultaneously. Brazilian agtech companies such as Agrotools have built strong positions in satellite-based deforestation monitoring and CAR database integration, directly addressing EUDR compliance needs, while global players such as Allflex Livestock Intelligence maintain leadership in RFID-based animal identification hardware. International certification and audit firms including SGS and Bureau Veritas continue to expand their traceability verification and supply chain audit services to support Brazilian exporters navigating increasingly complex international compliance requirements.

| Company | Establishment Year | Headquarters | Primary Product Portfolio | Traceability Solution Portfolio

|

Deployment Presence | Major End-Use Industries | Key Strategic Focus | Certifications & Compliance |

| Allflex Livestock Intelligence | 1975 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| IBM | 1911 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| SGS SA | 1878 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Bureau Veritas | 1828 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Agrotools | 2013 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

Brazil Food Traceability Market Analysis

Growth Drivers

Mandatory Cattle Traceability under MAPA’s National Livestock Traceability Plan

Brazil’s food traceability market is experiencing sustained growth due to the phased implementation of MAPA’s National Livestock Traceability Plan, launched in December 2024, which establishes mandatory individual identification for Brazil’s entire cattle and buffalo herd by 2032. Under the plan’s implementation schedule, a federal traceability system became operational in 2025, with integration of state-level systems planned for 2026 and mandatory individual identification phased in progressively across Brazilian states between 2027 and 2029, expanding to full national coverage by 2032. Decree No. 12,189 has introduced significantly stricter non-compliance penalties, with property owners failing to meet traceability requirements facing fines of up to BRL 50 million, with penalties potentially doubled in more severe cases, creating strong regulatory pressure for ranch operators and meatpacking plants to invest in compliant identification and tracking infrastructure. This regulatory mandate, combined with Brazil’s existing SISBOV program used for animals destined for premium export markets, continues to drive substantial investment in RFID ear tags, electronic identification readers, and integrated database systems throughout the country’s livestock supply chain.

Rising Export Compliance Demands from Key Trading Partners

Brazil’s role as one of the world’s largest exporters of beef, soybeans, and coffee continues to expose the country’s agricultural supply chains to increasingly stringent traceability requirements from major trading partners. The European Union’s Deforestation Regulation, which took effect on December 30, 2025, requires operators and traders exporting cattle, soy, coffee, palm oil, timber, rubber, and cocoa to the EU to provide verifiable production information, including geolocation data of areas of origin, and to demonstrate compliance with environmental and legal requirements in the country of production. China, which accounts for approximately 48% of Brazil’s beef export volume, has also intensified traceability requirements, with a 2024 pilot beef traceability project between Brazilian and Chinese authorities exploring alignment of emission measurement methodologies and integration with China’s General Administration of Customs e-CIQ digital inspection framework. Brazilian beef exports reached record levels in 2025, with export revenue growing approximately 40%, reinforcing the commercial importance of maintaining robust traceability systems capable of satisfying diverse international regulatory requirements simultaneously.

Market Challenges

Fragmented Implementation and Smallholder Cost Burden

Brazil’s food traceability market faces significant implementation challenges stemming from the fragmented and gradual rollout of the National Livestock Traceability Plan across a cattle herd of more than 238 million animals. Industry investigations have found that many Brazilian farmers, particularly smallholders, view the 2032 mandatory compliance timeline as unworkable given the substantial cost and infrastructure requirements associated with individual electronic identification. Animal identification in Brazil has historically relied on ranch branding rather than individual traceability, and current voluntary systems such as SISBOV allow feedlot operators to apply export-eligible tags to animals without verified correlation to their birth location or movement history, undermining the credibility of end-to-end traceability claims. Without strong buy-in from the full spectrum of Brazilian producers, from large-scale commercial operations to smallholder ranches, achieving the traceability coverage required to meet both domestic regulatory targets and increasingly strict export market requirements remains a substantial implementation challenge for technology providers and policymakers alike.

Interoperability Gaps Across Federal, State, and Private Systems

Brazil’s food traceability ecosystem currently comprises multiple parallel systems, including MAPA’s SISBOV individual identification program, the Animal Transport Guide (GTA), the Agricultural Management Platform (PGA) used to collect livestock transport data, various state-level Animal Health Agency (OESA) systems, and private supplier-tracking protocols independently developed by major meatpacking companies. This fragmentation creates significant interoperability challenges, as data captured in one system frequently cannot be seamlessly cross-referenced with records in another, complicating efforts to build a unified, auditable traceability record from farm to export. A 2024 European Commission audit found that it could not guarantee that Brazilian beef imports to the EU originated exclusively from hormone-free cattle, highlighting persistent gaps in the verification chain despite Brazil’s existing traceability infrastructure. Reconciling federal, state, and private systems into a coherent, internationally credible traceability framework remains a significant technical and institutional challenge for both government agencies and private technology providers operating in the Brazilian market.

Market Opportunities

Expansion of Satellite-Based Deforestation Monitoring Solutions

The European Union’s Deforestation Regulation, requiring verifiable geolocation data and deforestation-free sourcing documentation for commodities including cattle, soy, and coffee exported to the EU, has created substantial opportunity for Brazilian and international technology providers specializing in satellite-based monitoring and geospatial compliance verification. Companies such as Agrotools have developed platforms that cross-reference Rural Environmental Registry (CAR) data, satellite imagery, and environmental embargo lists maintained by IBAMA to help exporters demonstrate deforestation-free supply chains. The Federal Data Processing Service (SERPRO) has also begun developing platforms intended to organize and standardize access to public compliance databases in support of EUDR alignment. As more Brazilian exporters across the cattle, soy, and coffee sectors seek to maintain access to the European market ahead of and following the EUDR’s December 2025 effective date, demand for integrated satellite monitoring, geolocation verification, and deforestation risk-screening technologies is expected to expand substantially across Brazil’s major agricultural export regions.

China Market Access and Bilateral Traceability Protocol Development

Brazil’s deepening trade relationship with China, which accounts for approximately 48% of the country’s beef export volume, creates significant opportunity for traceability technology providers supporting bilateral compliance protocols. The 2024 pilot beef traceability project between Brazilian and Chinese regulatory authorities, focused on aligning emission measurement methodologies and integrating with China’s General Administration of Customs e-CIQ digital inspection framework, signals growing institutional interest in deeper traceability integration between the two countries. RFID-based systems capable of supporting batch reading at port facilities such as Santos and Paranaguá, combined with tamper-evident cold-chain monitoring for refrigerated exports, are increasingly positioned to meet both MAPA’s SISBOV requirements and China’s import protocols simultaneously. As negotiations progress on joint protocols for meat and soy certification, technology providers capable of delivering interoperable solutions that satisfy multiple export market requirements through a single integrated system are well positioned to capture growing demand from Brazilian exporters seeking to diversify and deepen their access to the Chinese market.

Future Outlook

The Brazil Food Traceability Market is expected to witness sustained expansion over the forecast period, supported by the phased implementation of MAPA’s National Livestock Traceability Plan through 2032, growing compliance requirements under the EU Deforestation Regulation, and deepening bilateral traceability cooperation with China. Continued investment in satellite monitoring, blockchain-based verification, and RFID identification infrastructure will further accelerate market growth as Brazilian exporters work to maintain access to increasingly demanding international markets. The market is also likely to benefit from growing integration between traceability platforms and precision agriculture technologies, as Brazil’s agricultural sector continues to digitalize across both large-scale commercial operations and, gradually, smallholder production.

Major Players

- Allflex Livestock Intelligence

- IBM

- SGS SA

- Bureau Veritas

- Agrotools

- Zoetis

- Datamars

- SAP

- TE-FOOD (FoodChain ID)

- Neogen Corporation

- Where Food Comes From, Inc.

- FoodLogiQ

- Trustwell

- Solinftec

- GS1 Brasil

Key Target Audience

- Food Traceability Technology Providers

- Meatpacking Plants & Slaughterhouses

- Grain & Soybean Exporters

- Coffee Producers & Cooperatives

- Food Retailers & Supermarkets

- Investment and Venture Capitalist Firms

- Government and Regulatory Bodies (Ministry of Agriculture, Livestock and Supply (MAPA), National Health Surveillance Agency (ANVISA), Federal Data Processing Service (SERPRO))

- Logistics, Cold Chain, and Port Operators

Research Methodology

Step 1: Identification of Key Variables

The research process begins with identifying the complete ecosystem of the Brazil Food Traceability Market, including technology providers, hardware manufacturers, certification bodies, food producers and exporters, logistics operators, and regulatory authorities. Extensive secondary research is conducted using company annual reports, government publications, trade associations, customs statistics, industry journals, and proprietary databases to determine the variables influencing market demand, pricing, deployment volumes, and technological developments.

Step 2: Market Analysis and Construction

Historical market information is collected and analyzed to estimate market size, deployment volumes, export compliance activity, application-wise demand, and pricing trends. A combination of top-down and bottom-up approaches is used to estimate market revenues and validate segment-level performance. Adoption patterns across livestock, grain, coffee, and processed food traceability are evaluated to establish an accurate representation of the industry.

Step 3: Hypothesis Validation and Expert Consultation

The preliminary findings are validated through Computer-Assisted Telephone Interviews (CATIs) and structured discussions with traceability technology providers, export compliance managers, certification auditors, agricultural cooperatives, regulatory experts, and senior executives operating within the Brazilian agribusiness sector. These interviews help verify market assumptions, competitive developments, technology adoption trends, pricing dynamics, and future investment opportunities while refining the overall market estimates.

Step 4: Research Synthesis and Final Output

The final stage integrates insights obtained from primary interviews with quantitative information collected through secondary sources. Data triangulation techniques are applied to reconcile differences between supply-side and demand-side estimates, ensuring robust market forecasting. The report is then reviewed through multiple quality assurance checkpoints to deliver a comprehensive analysis covering market size, segmentation, competitive landscape, future outlook, and strategic recommendations for industry stakeholders.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Sizing Approach, Top-Down Analysis, Bottom-Up Analysis, Demand-Side Assessment, Supply-Side Assessment, Primary Industry Interviews, Secondary Research Validation, Data Triangulation, Forecasting Framework, Limitations and Future Conclusions)

- Definition and Scope

- Market Evolution and Industry Genesis

- Timeline of Major Industry Developments

- Food Traceability Industry Value Chain Analysis

- Supply Chain Analysis

- Growth Drivers (Mandatory Cattle Traceability Requirements, Rising Export Compliance Demands, Expansion of Blockchain-Based Supply Chain Solutions, Growing Deforestation-Free Sourcing Requirements, Increasing Adoption of RFID and IoT Sensors, Growth in Premium and Certified Food Exports)

- Market Challenges (Fragmented Federal, State & Private Systems, Small Producer Cost and Infrastructure Burden, Interoperability Gaps Across Supply Chains, Data Standardization Complexity, Limited Rural Connectivity, Implementation Timeline Uncertainty)

- Market Opportunities (Expansion of Satellite-Based Deforestation Monitoring, China Market Access & Bilateral Traceability Protocols, Growth in Blockchain-Enabled Export Certification, Integration with Precision Agriculture Platforms, SME Digitalization Support Programs, Coffee & Specialty Crop Traceability Expansion)

- Market Trends (Shift Toward Individual Animal Identification, Growth in Geolocation-Based Compliance Tools, Blockchain Pilot Program Expansion, Satellite Monitoring Integration, Cross-Border Digital Inspection Protocols, Consolidation of Private Supplier-Tracking Systems)

- Government Regulations (MAPA National Livestock Traceability Plan, SISBOV Individual Identification Requirements, Decree No. 12,189 Compliance Penalties, EU Deforestation Regulation (EUDR) Alignment, GTA Animal Transport Documentation, ANVISA Food Safety Standards)

- Import and Export Analysis (Trade Volume, Major Export Destinations, Compliance Documentation Requirements, HS Code Analysis, Trade Balance)

- Infrastructure Availability Analysis (RFID Ear Tags & Boluses, Satellite Connectivity, Rural Broadband Access, Cold Chain Sensor Networks, Port Reader Infrastructure, Cloud Data Center Availability)

- Technology Landscape (RFID & UHF Tagging Technologies, Blockchain Ledger Platforms, Satellite Geolocation Technologies, IoT Sensor Networks, DNA-Based Verification Technologies)

- Sustainability Assessment (Deforestation-Free Supply Chain Verification, Carbon Footprint Monitoring, Sustainable Sourcing Certification, Environmental Embargo Screening, Low-Emission Livestock Programs)

- PESTLE Analysis

- SWOT Analysis

- Porter’s Five Forces Analysis

- Stakeholder Ecosystem

- Competition Ecosystem

- By Market Value (2020-2025)

- By Volume of Deployments (2020-2025)

- By Average Selling Price (2020-2025)

- By Technology Type (In Value %)

RFID & Electronic Tagging

Barcode & QR Code Systems

Blockchain-Based Traceability

GPS & Satellite Monitoring

DNA & Biomarker Traceability

Sensor-Based IoT Systems - By Application (In Value %)

Livestock & Meat Traceability

Soybean & Grain Traceability

Coffee Traceability

Fruits & Vegetables Traceability

Dairy Traceability

Seafood Traceability

Poultry Traceability

Processed Foods Traceability

Beverage Traceability

Export Compliance Documentation - By Deployment Mode (In Value %)

Cloud-Based Platforms

On-Premise Systems

Hybrid Deployment Models

Mobile-Based Applications

Integrated ERP Traceability Modules - By End User (In Value %)

Meatpacking Plants & Slaughterhouses

Grain & Soybean Exporters

Coffee Producers & Cooperatives

Food Retailers & Supermarkets

Food Manufacturers & Processors

Logistics & Cold Chain Operators

Government & Certification Bodies - By Region (In Value %)

Southeast Brazil

South Brazil

Center-West Brazil

Northeast Brazil

North Brazil

- Market Share of Major Players (By Value, Deployment Volume, Technology Type, Application Industry, End-Use Category)

- Cross Comparison Parameters (Solution Portfolio Breadth, Regulatory Compliance Coverage, Satellite & Geolocation Capability, Application Technical Support, Deployment Scale, Certifications & Audit Credentials, Export Customer Base, Innovation & New Product Launch Frequency)

- SWOT Analysis of Major Players

- Pricing Analysis by Solution Type and Deployment Scale

- Deployment Capacity Analysis

- Regional Presence Analysis

- Distribution & Partner Network Analysis

- Innovation Benchmarking

- Detailed Profiles of Major Companies

Allflex Livestock Intelligence

IBM

SGS SA

Bureau Veritas

Agrotools

Zoetis

Datamars

SAP

TE-FOOD (FoodChain ID)

Neogen Corporation

Where Food Comes From, Inc.

FoodLogiQ

Trustwell

Solinftec

GS1 Brasil

- Consumption Pattern Analysis (Deployment Scale, System Integration Complexity, Compliance-Driven Adoption, Seasonal Export Demand, Reformulation of Legacy Systems)

- Purchasing Criteria (Regulatory Compliance Coverage, System Interoperability, Cost Efficiency, Data Security, Scalability, Export Market Acceptance)

- Procurement and Vendor Selection Analysis

- Blockchain Adoption Assessment

- Large Producer vs Smallholder Technology Demand

- Solution Attribute Preference Analysis (Real-Time Data Capture, Field Durability, Ease of Integration, Audit Trail Transparency, Geolocation Accuracy, Cross-Border Interoperability)

- Export Compliance Influence on Technology Investment

- Pain Point Analysis

- Decision-Making Process

- By Market Value (2026-2035)

- By Volume of Deployments (2026-2035)

- By Average Selling Price (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now