Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Brazil harvesting equipment market for soybean and corn is valued at approximately USD ~ billion based on a recent historical assessment derived from agricultural machinery shipment data and national farm mechanization statistics. Demand is primarily driven by expansion of mechanized soybean and corn cultivation across large commercial farms, replacement cycles of combine harvesters, and adoption of high-capacity harvesting systems to reduce grain loss and improve field productivity across Brazil’s major grain belts.

Dominant production and equipment demand centers include Mato Grosso, Paraná, and Rio Grande do Sul, where extensive soybean–corn rotation farming and large mechanized holdings require advanced harvesting machinery. Mato Grosso leads due to its vast cultivated acreage and industrialized farming model, while southern states sustain demand through established agribusiness infrastructure, dealer networks, and proximity to processing and export logistics corridors supporting high-throughput harvesting operations.

Market Segmentation

By Product Type

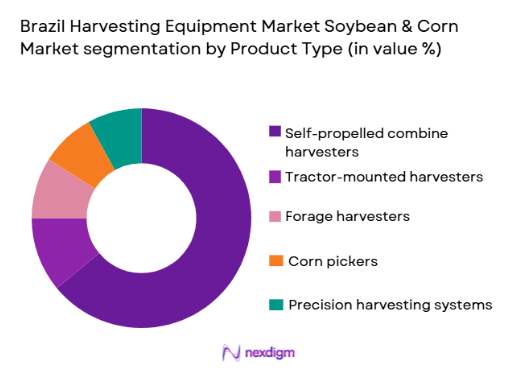

Brazil harvesting equipment market soybean and corn market is segmented by product type into self-propelled combine harvesters, tractor-mounted harvesters, forage harvesters, corn pickers, and precision harvesting systems. Recently, self-propelled combine harvesters has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Large Brazilian soybean and corn farms operate expansive fields requiring high-capacity, mobile harvesting solutions capable of covering wide swaths efficiently during narrow harvest windows. Self-propelled combines integrate threshing, separation, and grain handling functions in a single platform, reducing labor requirements and enabling rapid crop clearance essential in double-cropping systems. Major manufacturers prioritize these models in Brazil with local assembly, financing programs, and service networks, reinforcing adoption. Farmers also prefer them for compatibility with precision yield monitoring and guidance technologies that improve operational efficiency and reduce grain loss. These systems handle both soybean and corn harvesting with interchangeable headers, increasing utilization across seasons. As farm consolidation continues and labor constraints persist, producers favor large autonomous-ready combines over smaller or mounted alternatives, sustaining segment dominance.

By End User

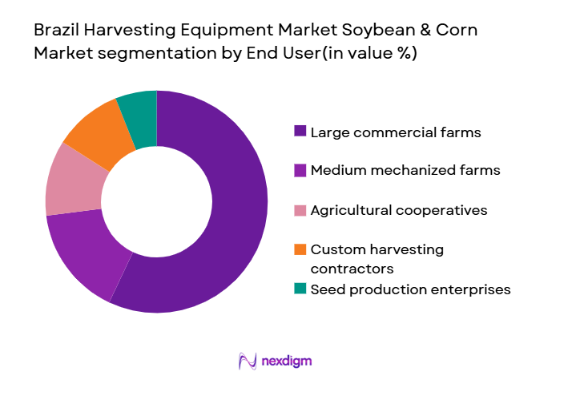

Brazil harvesting equipment market soybean and corn market is segmented by end user into large commercial farms, medium mechanized farms, agricultural cooperatives, custom harvesting contractors, and seed production enterprises. Recently, large commercial farms has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Brazil’s soybean and corn production structure is characterized by extensive agribusiness operations spanning thousands of hectares, particularly in Mato Grosso and Goiás. These enterprises invest heavily in high-capacity combine fleets to ensure timely harvesting across multiple crop cycles and minimize weather-related losses. Their financial scale allows direct procurement from global OEMs and adoption of advanced telematics and automation features. Large farms also drive replacement demand through shorter equipment life cycles due to intensive utilization. Integrated logistics systems connecting farms to storage and export terminals further reinforce mechanization investment. In contrast, smaller farms rely more on contractors or shared equipment, concentrating ownership among large producers. This structural concentration of land and output results in dominant equipment purchasing power within the large commercial farm segment.

Competitive Landscape

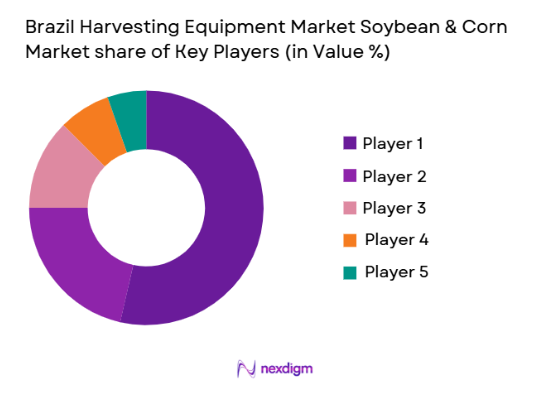

The Brazil harvesting equipment market for soybean and corn is moderately consolidated, dominated by global agricultural machinery manufacturers with localized production and dealer networks. Leading firms compete through high-capacity combine technology, precision agriculture integration, and aftersales support. Market leaders maintain strong penetration in large commercial farms through financing programs and service coverage, while domestic manufacturers compete in niche or mid-range segments. Technological differentiation, header adaptability, and throughput efficiency define competitive positioning across Brazil’s major grain regions.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Brazil Combine Capacity Range |

| John Deere | 1837 | United States | ~ | ~ | ~ | ~ | ~ |

| CNH Industrial | 2013 | United Kingdom | ~ | ~ | ~ | ~ | ~ |

| AGCO | 1990 | United States | ~ | ~ | ~ | ~ | ~ |

| CLAAS | 1913 | Germany | ~ | ~ | ~ | ~ | ~ |

| Jacto | 1948 | Brazil | ~ | ~ | ~ | ~ | ~ |

Brazil Harvesting Equipment Market Soybean & Corn Market Analysis

Growth Drivers

Large-Scale Soybean and Corn Agribusiness Expansion:

Brazil’s agricultural production model is dominated by expansive commercial farms cultivating soybean and corn in rotation across vast tracts of land, particularly in the central-west region. These operations depend on high-capacity harvesting machinery to manage extremely large harvest volumes within short seasonal windows imposed by climate patterns. Mechanized harvesting reduces crop losses and ensures timely planting of subsequent crops in double-cropping systems, directly influencing farm profitability. Continued expansion of cultivated acreage in frontier regions increases demand for combine fleets and replacement cycles. Agribusiness consolidation has produced larger farm units with capital resources for advanced machinery investment. Export-oriented production further incentivizes high throughput and grain quality preservation during harvesting. Manufacturers respond with localized assembly and financing, lowering acquisition barriers. The combination of scale, mechanization intensity, and crop rotation complexity structurally sustains harvesting equipment demand across soybean and corn farming systems.

Adoption of Precision Harvesting and Automation Technologies:

Brazilian soybean and corn producers increasingly integrate precision agriculture technologies into harvesting operations to optimize yield measurement, fuel use, and grain loss control. Modern combine harvesters incorporate telematics, auto-guidance, and sensor-based yield monitoring systems that enable real-time performance management across large fields. Data-driven harvesting allows operators to adjust settings for varying crop conditions, improving grain recovery and operational efficiency. Farms use harvest data for agronomic planning and input optimization in subsequent seasons, reinforcing technology value. Automation features reduce operator fatigue and labor dependency, addressing workforce constraints in remote agricultural regions. OEMs bundle digital platforms with equipment sales, accelerating adoption among large farms. Government incentives for agricultural productivity improvements also encourage precision technology investment. These technological capabilities differentiate new equipment from legacy models, driving replacement demand and expanding market value in Brazil’s soybean and corn harvesting sector.

Market Challenges

High Capital Cost and Financing Constraints for Advanced Combines:

Modern soybean and corn harvesting equipment represents a substantial capital investment, with high-capacity combines incorporating advanced electronics, automation, and powerful engines that elevate purchase prices. Although large agribusinesses possess financing access, medium-scale producers face constraints in acquiring new machines without subsidized credit. Brazil’s agricultural machinery financing programs fluctuate with fiscal policy and interest rate environments, affecting purchasing cycles. Currency volatility increases import-linked component costs, raising equipment prices in local currency terms. Maintenance and spare parts expenses for sophisticated combines further increase total ownership cost. Seasonal utilization patterns reduce annual operating hours compared to industrial machinery, affecting return on investment for some users. Producers may extend equipment life cycles during unfavorable commodity price periods, dampening replacement demand. Dealers must provide financing and service packages to offset affordability barriers. These economic factors limit broader adoption across smaller farm segments despite technological benefits.

Logistical and Operational Constraints in Remote Grain Regions:

Major soybean and corn production zones such as Mato Grosso are geographically remote from industrial centers and ports, creating logistical challenges for harvesting equipment deployment and support. Transporting large combines and headers across long distances over constrained infrastructure raises delivery costs and delays. Limited availability of skilled technicians in frontier regions complicates maintenance and repair during critical harvest windows. Seasonal rains and soil conditions can restrict machine mobility and accelerate wear, increasing downtime risk. Farms require localized parts inventories and service teams, but dealer networks are less dense in expanding agricultural frontiers. Operational disruptions during harvest can result in significant crop loss and financial impact, making reliability paramount. Infrastructure bottlenecks also affect movement of harvested grain, reducing effective harvesting efficiency. These logistical and environmental constraints increase operational risk and ownership cost for soybean and corn harvesting machinery in Brazil’s interior agricultural regions.

Opportunities

Expansion of Custom Harvesting Service Providers in Mid-Scale Farming:

A growing number of mid-scale soybean and corn producers in Brazil rely on specialized custom harvesting contractors rather than owning high-capacity combines. This service model reduces capital expenditure for farmers while ensuring access to advanced machinery during harvest periods. Contractors invest in large, technologically advanced combine fleets optimized for multi-farm operations across regions. Increasing consolidation of service providers allows efficient machine utilization throughout the harvesting season by moving equipment geographically following crop maturity patterns. Equipment manufacturers can target contractors with high-specification machines, telematics platforms, and fleet management tools. Financing institutions also support contractor models due to predictable utilization and revenue streams. This structural shift expands addressable demand beyond ownership markets and increases equipment turnover rates. As mid-scale farms expand but remain capital constrained, contractor-driven harvesting demand will grow, creating sustained opportunities for soybean and corn combine manufacturers in Brazil.

Development of Dual-Crop Optimized Harvesting Platforms for Soybean and Corn:

Brazil’s dominant soybean–corn rotation system creates demand for harvesting machinery capable of efficient operation across both crops with minimal reconfiguration. Equipment manufacturers can develop dual-crop optimized combines and headers that maximize throughput, grain quality, and fuel efficiency for soybean and corn conditions. Such platforms reduce equipment redundancy and improve annual utilization, improving economic viability for farm operators. Advances in adaptive threshing systems, adjustable concaves, and automated crop detection enable seamless transitions between crops. Producers value machines that maintain low grain loss and kernel integrity across differing crop characteristics. OEMs integrating crop-specific software presets and automatic adjustments can enhance operational efficiency and operator simplicity. Localization of design for Brazilian crop varieties and field conditions further differentiates offerings. Growing adoption of dual-crop platforms will stimulate replacement demand and technological upgrading across Brazil’s soybean and corn harvesting equipment market.

Future Outlook

Brazil’s soybean and corn harvesting equipment market is expected to expand steadily over the next five years supported by continued agribusiness scale growth, mechanization intensity, and precision technology adoption. Demand will rise for high-capacity, fuel-efficient, and automation-enabled combines tailored to dual-crop systems. Government agricultural financing and productivity initiatives will support modernization. Expansion of cultivated acreage in central-west regions and contractor harvesting models will further sustain equipment purchases and replacement cycles.

Major Players

- John Deere

- CNH Industrial

- AGCO

- CLAAS

- Jacto

- SLC Máquinas

- Stara

- TATU Marchesan

- Baldan

- Indústrias Colombo

- New Holland Agriculture

- Case IH

- Massey Ferguson

- Valtra

- GTS do Brasil

Key Target Audience

- Agricultural machinery manufacturers

- Soybean producers

- Corn producers

- Agricultural cooperatives

- Custom harvesting contractors

- Farm equipment distributors

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Demand drivers, mechanization levels, combine fleet size, crop acreage, replacement cycles, and technology adoption variables specific to soybean and corn harvesting equipment in Brazil were identified through agricultural statistics and machinery shipment datasets.

Step 2: Market Analysis and Construction

Market size was constructed using combine harvester production, import, and sales data triangulated with crop acreage and mechanization intensity across Brazil’s major soybean and corn producing states.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions on equipment utilization, replacement cycles, and technology penetration were validated through consultations with dealers, agronomists, and farm operators across Mato Grosso, Paraná, and Rio Grande do Sul.

Step 4: Research Synthesis and Final Output

All quantitative and qualitative insights were synthesized into market estimates, segmentation, and competitive analysis to produce a structured assessment of Brazil’s soybean and corn harvesting equipment market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of soybean and corn cultivation areas in central-west Brazil

Rising demand for high-capacity harvesters to reduce field losses

Increased mechanization in large-scale row crop farming - Market Challenges

High capital cost of advanced combine harvesters

Seasonal utilization constraints affecting equipment ROI

Dependence on imported precision components - Market Opportunities

Adoption of precision harvesting and yield analytics solutions

Growth of custom harvesting service businesses

Demand for fuel-efficient and low-loss harvesting technologies - Trends

Shift toward larger header widths for soybean and corn harvesting

Integration of telematics and remote diagnostics in harvesters

Adoption of track-based mobility systems in wet soil regions

Use of automation and guidance in harvesting operations

Demand for dual-crop optimized combine configurations - Government Regulations & Defense Policy

Agricultural machinery financing subsidies and rural credit policies

Emission and engine compliance standards for off-road equipment

Local manufacturing incentives for agricultural machinery - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Self-propelled combine harvesters for soybean

Self-propelled combine harvesters for corn

Axial flow harvesters

Hybrid threshing harvesters

Tracked combine harvesters - By Platform Type (In Value%)

Large-scale commercial farms

Mid-size mechanized farms

Contract harvesting fleets

Cooperative-owned machinery pools

Research and seed production farms - By Fitment Type (In Value%)

Factory-fitted harvesting systems

Header-attach retrofit kits

Precision agriculture integrated fitment

Telematics-enabled fitment

Crop-specific adjustment packages - By EndUser Segment (In Value%)

Soybean commercial producers

Corn commercial producers

Integrated soybean-corn rotation farms

Agricultural cooperatives

Custom harvesting service providers - By Procurement Channel (In Value%)

Direct OEM sales

Dealer and distributor networks

Cooperative procurement programs

Government-supported credit purchases

Leasing and rental providers - By Material / Technology (in Value %)

High-capacity threshing and separation systems

Precision yield monitoring sensors

Autonomous and guidance systems

Low-loss grain handling mechanisms

Fuel-efficient powertrain technology

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Engine Power Range, Header Width Capacity, Grain Tank Size, Automation Level, Fuel Efficiency, Telematics Integration, Crop Adaptability, Throughput Capacity, Maintenance Interval, Dealer Network Strength)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

John Deere Brasil

CNH Industrial Brasil

AGCO do Brasil

CLAAS América Latina

SLC Máquinas

Stara S/A

Jacto Máquinas Agrícolas

Baldan Implementos Agrícolas

Case IH Brasil

New Holland Agriculture Brasil

Valtra Brasil

Massey Ferguson Brasil

GTS do Brasil

TATU Marchesan

Indústrias Colombo

- Large soybean-corn rotation farms prioritize high-throughput harvesters

- Cooperatives focus on shared machinery utilization efficiency

- Custom harvesters demand versatile multi-crop configurations

- Seed producers require precision and low-loss harvesting systems

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now