Download PDF

Download PDFMarket Overview

The Brazil home finance market has seen significant growth due to increasing urbanization and rising middle-class households. With a market size of approximately USD ~ billion, the market is driven by the demand for affordable housing solutions, government-backed housing credit programs, and the growing middle-income population. A robust housing finance infrastructure supported by banks and fintech players has also fueled growth. In particular, the implementation of the Minha Casa Minha Vida program has helped bridge the affordability gap and facilitated credit access for low-income groups.

Major cities such as São Paulo, Rio de Janeiro, and Brasília dominate the Brazil home finance market due to their large urban populations and higher income levels. These cities offer the most developed housing markets with robust demand for mortgages, especially in the middle and upper-income segments. The real estate development in these regions is driven by economic stability, improved infrastructure, and government policies supporting homeownership. Other key regions like Minas Gerais and Paraná also play vital roles due to ongoing urbanization and demand for residential housing.

Market Segmentation

By Product Type

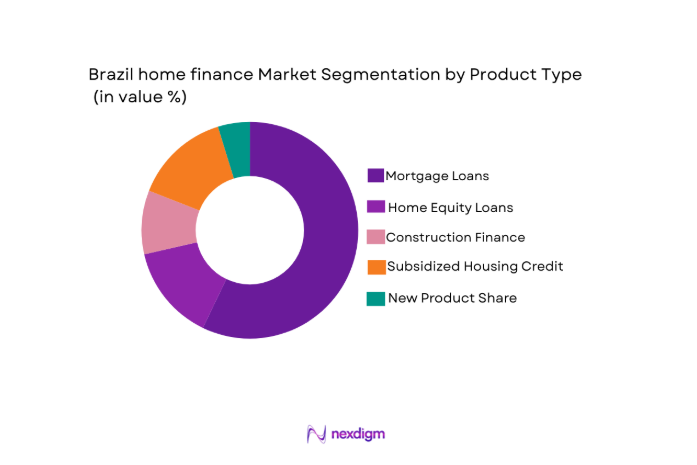

The Brazil home finance market is segmented by product type into mortgage loans, home equity loans, construction finance, and subsidized housing credit. Recently, mortgage loans have a dominant market share due to government-backed programs such as the Minha Casa Minha Vida initiative, which caters to low and middle-income buyers. The widespread availability of long-term, low-interest loans through both public and private banks, along with the growing preference for homeownership, has led to the increased adoption of mortgage loans across Brazil, thus making it the most prominent sub-segment in the market.

By Platform Type

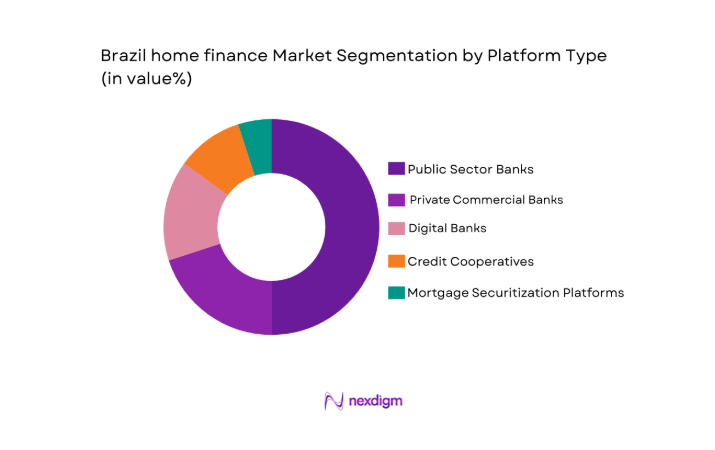

The Brazil home finance market is segmented by platform type into public sector banks, private commercial banks, digital banks, credit cooperatives, and mortgage securitization platforms. Recently, public sector banks have dominated the market due to their extensive government-backed programs, such as the SFH (Sistema Financeiro da Habitação), offering highly affordable home loans with long tenures and low interest rates. Their large branch networks and historical presence have contributed significantly to their market dominance, while newer entrants like digital banks and fintechs are gaining ground in the digital space.

Competitive Landscape

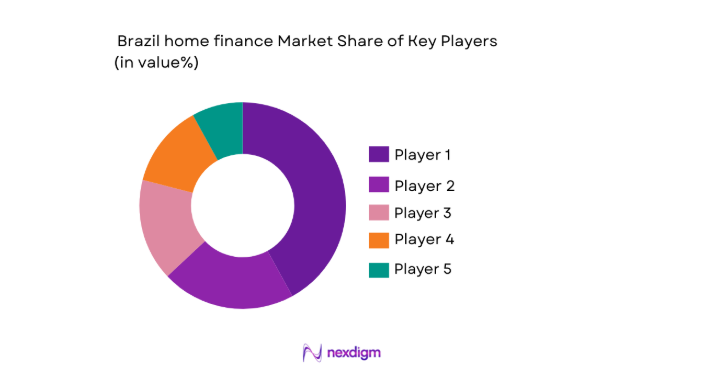

The Brazil home finance market is competitive with a mix of public sector banks, private banks, fintech players, and credit cooperatives. The market is seeing consolidation as larger players are expanding their service offerings and technology platforms to meet the growing demand for home financing. The role of fintech and digital-first platforms has also increased significantly, offering more accessible mortgage options. While public sector banks remain dominant due to government backing, the influence of private banks and digital platforms is rising.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Digital Mortgage Origination |

| Caixa Econômica Federal | 1861 | Brasília, Brazil | ~ | ~ | ~ | ~ | ~ |

| Banco do Brasil | 1808 | Brasília, Brazil | ~ | ~ | ~ | ~ | ~ |

| Bradesco | 1943 | Osasco, Brazil | ~ | ~ | ~ | ~ | ~ |

| Itaú Unibanco | 1945 | São Paulo, Brazil | ~ | ~ | ~ | ~ | ~ |

| Banco Inter | 1994 | Belo Horizonte, Brazil | ~ | ~ | ~ | ~ | ~ |

Brazil Home Finance Market Analysis

Growth Drivers

Government-backed Housing Credit Programs

Government-backed housing programs, such as Minha Casa Minha Vida, have been key drivers in the Brazil home finance market. These initiatives provide affordable housing loans to low and middle-income families who would otherwise be excluded from the formal credit system. The subsidy system and long-term repayment structures offered under these programs have expanded the reach of mortgage finance to underserved populations, contributing to the rapid growth of the home finance market. These programs target first-time buyers and families who have limited access to traditional bank loans, offering them favorable terms such as low interest rates and down payments. In addition, the increasing availability of low-income housing projects funded by both the government and private developers has increased market demand. Moreover, the Brazilian government’s continued commitment to funding these programs helps maintain market stability and incentivizes participation from financial institutions, ensuring sustainable growth. As a result, government policies aimed at enhancing financial inclusion and supporting homeownership are central to the expansion of the home finance market, driving up both demand and participation. Furthermore, the continuation and possible expansion of these programs, particularly in urban areas, are expected to sustain long-term growth. The introduction of new financial products and reforms that improve accessibility to housing finance further strengthens this driver.

Digital Transformation in Mortgage Origination and Underwriting

The ongoing digitalization of Brazil’s mortgage industry has significantly boosted the market. Digital transformation has simplified the mortgage origination process, allowing consumers to apply for loans from the comfort of their homes, reducing paperwork and processing time. Moreover, AI-based platforms are enhancing the efficiency of underwriting, credit scoring, and loan approval processes, ensuring quicker decisions and a smoother customer experience. The growing adoption of mobile apps, online platforms, and automated tools for mortgage applications has made it easier for consumers to access financing options, especially among younger and tech-savvy buyers. Fintech companies and digital-first banks have become important players in this transformation, offering digital-only home loan options, which are increasingly popular due to their lower costs and higher efficiency. This change is especially beneficial for clients who prefer a fully digital experience, including document verification, contract signing, and payments. With the rapid growth of internet penetration and smartphone use across Brazil, digital channels are expected to continue to reshape the home finance market. Additionally, technology-driven solutions such as AI, machine learning, and big data analytics will help improve the accuracy of credit assessments and allow more personalized loan products, further expanding market reach.

Market Challenges

High Interest Rates and Affordability Concerns

One of the primary challenges faced by Brazil’s home finance market is the volatility of interest rates. Despite government-backed programs offering subsidized rates, many individuals still find it challenging to secure home loans due to high interest rates, especially in the private sector. The Central Bank of Brazil’s monetary policy, which aims to control inflation, often leads to fluctuations in the base interest rate (Selic), making it difficult for potential homeowners to commit to long-term mortgage agreements. The rise in inflation and economic instability also affects the affordability of homes and the ability of borrowers to meet mortgage repayments. As a result, many families, particularly in lower-income brackets, are unable to access home financing or are burdened with higher-than-expected monthly payments. Furthermore, despite efforts to promote financial inclusion, the inability to secure a steady income or credit history still prevents a large portion of the population from participating in the home finance market. With the demand for housing continuing to grow, these affordability issues pose a significant barrier to widespread homeownership.

Bureaucratic and Administrative Barriers

Brazil’s home finance market is also hindered by bureaucratic and administrative challenges that delay the processing of loans and property transactions. The complex documentation process required for home loan applications and property purchases often leads to long waiting periods for approvals. Legal procedures, property appraisals, and registration processes are also time-consuming, especially in rural areas. These delays can discourage potential homebuyers from pursuing loans and lead to a backlog in housing market transactions. Additionally, the lack of a standardized property registry system across the country further complicates the process, particularly in regions with less infrastructure. While there have been efforts to digitalize property transactions, many local governments still rely on traditional, paper-based systems, which can delay homeownership opportunities. As the demand for home loans rises, these administrative inefficiencies pose a significant challenge to the expansion of the market.

Opportunities

Expansion of Green and Sustainable Home Financing Products

As environmental concerns become increasingly important to consumers and governments, there is a growing demand for green and sustainable homes. This trend is leading to a rise in the development of financing products specifically aimed at eco-friendly housing, such as energy-efficient homes and buildings with sustainable materials. Brazil’s growing awareness of environmental sustainability presents a major opportunity for the home finance sector to tap into this market by offering financing options tailored for green homes. These products can include lower interest rates or additional subsidies for properties that meet certain environmental standards, such as energy efficiency or the use of sustainable building materials. Government initiatives supporting green housing projects and energy-efficient homes, combined with consumer demand for environmentally responsible living, provide a fertile ground for financial institutions to expand their product offerings. Furthermore, these products could attract the younger generation, which is more likely to prioritize sustainability when making purchasing decisions. The growth of this niche market segment can help diversify the home finance industry, attract a new pool of customers, and meet the changing preferences of modern homebuyers.

Partnerships with Fintechs and Digital Platforms

The rise of fintech companies and digital platforms has transformed the home finance market, opening up new opportunities for financial institutions. By partnering with fintech firms that specialize in digital mortgage origination, credit scoring, and loan management, traditional banks can enhance their customer offerings and streamline the loan application process. These collaborations provide opportunities to reach underserved populations, including young professionals, low-income groups, and individuals without traditional credit histories. Fintech platforms also offer the potential for lower operational costs, faster loan processing times, and improved customer experiences. By leveraging digital channels, banks and financial institutions can offer personalized, flexible mortgage solutions that better align with consumer needs. As the digital adoption rate in Brazil continues to rise, particularly in urban areas, these partnerships will become a crucial avenue for banks to expand their market reach and capitalize on the growing demand for home loans.

Future Outlook

The future of the Brazil home finance market looks promising, with continued growth expected in the next five years. This growth will be supported by government-backed housing initiatives, increasing digitalization of mortgage origination, and rising consumer demand for affordable housing solutions. As more fintech companies enter the market, offering innovative digital mortgage products, competition will intensify, driving further enhancements in service offerings and customer experience. Regulatory frameworks are expected to adapt to the evolving market, encouraging more private sector participation and providing additional incentives for sustainable housing finance. The continued urbanization of Brazil’s major cities will further fuel the demand for home loans, while initiatives like green home financing will create new market opportunities.

Major Players

- Caixa Econômica Federal

- Banco do Brasil

- Itaú Unibanco

- Bradesco

- Santander Brasil

- Banco Inter

- BTG Pactual

- Banco Safra

- BRB Banco de Brasília

- Sicredi

- Sicoob

- Banco PAN

- C6 Bank

- Creditas

- MRV&Co

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Real estate developers

- Banks and financial institutions

- Homebuyers and consumers

- Mortgage brokers

- Insurance companies

- Property investors

Research Methodology

Step 1: Identification of Key Variables

We identify essential variables impacting the market, such as demand patterns, financial policies, and consumer preferences.

Step 2: Market Analysis and Construction

A comprehensive analysis of market drivers, challenges, and opportunities is performed using primary and secondary research.

Step 3: Hypothesis Validation and Expert Consultation

We validate our findings through expert interviews, ensuring the accuracy of the market model.

Step 4: Research Synthesis and Final Output

Our final output synthesizes data and expert opinions to offer an accurate forecast of the home finance market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of subsidized housing programs for low-income households

Digital transformation across mortgage origination and underwriting processes

Urbanization and housing deficit in metropolitan regions

Declining inflationary pressures supporting credit expansion

Growth in mortgage-backed securities and secondary markets - Market Challenges

High interest rate volatility impacting borrower affordability

Lengthy property registration and documentation processes

Regional income disparities limiting uniform credit penetration

Credit risk exposure amid macroeconomic uncertainty

Dependence on public sector funding mechanisms - Market Opportunities

Expansion of green mortgage products for sustainable housing

Growth of digital-only mortgage origination platforms

Development of secondary mortgage markets through securitization - Trends

Increased adoption of IPCA-indexed mortgage products

Rising integration of open banking frameworks in credit assessment

Growth in remote property valuation and digital documentation

Partnerships between fintechs and traditional banks

Expansion of affordable housing finance through public-private partnerships - Government Regulations & Defense Policy

Central Bank of Brazil housing credit regulations under SFH and SFI frameworks

FGTS-linked housing finance policy adjustments

Regulatory oversight of mortgage-backed securities issuance - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Mortgage Loans

Mortgage Loans

Home Equity Loans

Construction Finance

Subsidized Housing Credit (Minha Casa Minha Vida) - By Platform Type (In Value%)

Public Sector Banks

Private Commercial Banks

Digital Banks and Fintech Lenders

Credit Cooperatives

Mortgage Securitization Platforms - By Fitment Type (In Value%)

Fixed Rate Mortgages

Floating Rate Mortgages

Hybrid Rate Structures

Indexed Loans (TR/IPCA linked)

Balloon Payment Structures - By End User Segment (In Value%)

First-Time Homebuyers

Middle-Income Urban Households

Low-Income Subsidized Beneficiaries

Real Estate Developers

Property Investors and Landlords - By Procurement Channel (In Value%)

Direct Bank Branch Lending

Online Mortgage Portals

Real Estate Developer Tie-ups

Mortgage Brokers

Government Housing Agencies

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Loan Portfolio Size, Interest Rate Structure, Loan Tenure Flexibility, Digital Origination Capability, Geographic Presence, Funding Source Diversification, NPL Ratio, Government Program Participation, Securitization Activity)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Caixa Econômica Federal

Banco do Brasil

Itaú Unibanco

Bradesco

Santander Brasil

Banco Inter

BTG Pactual

Banco Safra

BRB Banco de Brasília

Sicredi

Sicoob

Banco PAN

C6 Bank

Creditas

MRV&Co

- Rising demand for long-tenure mortgage products among urban salaried professionals

- Increased participation of low-income households through subsidy-backed credit

- Growing investor interest in rental housing assets

- Developers leveraging structured finance for project execution

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now