Download PDF

Download PDFMarket Overview

The Brazil Insecticide Market is valued at approximately USD ~ billion, supported by Brazil’s position as the world’s largest soybean exporter and one of the leading producers of corn, sugarcane, cotton, and coffee. The broader crop protection market generated approximately USD ~ billion in agricultural season sales, while soybean cultivation exceeded 45 million hectares, creating significant demand for insect control solutions. Rising pest resistance, tropical climatic conditions, multiple crop cycles, and increasing adoption of high-yield seed varieties continue to support insecticide consumption across Brazil’s commercial farming sector.

Market Segmentation

By Product Category

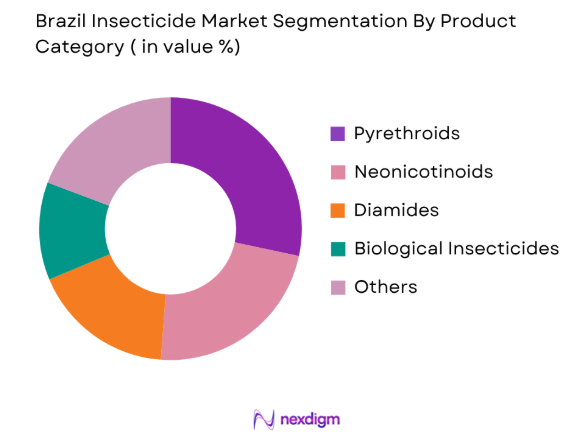

Brazil Insecticide Market is segmented by product class into pyrethroids, neonicotinoids, diamides, organophosphates, biological insecticides, carbamates, insect growth regulators, and other chemistries. Recently, pyrethroids have held the dominant market share in Brazil under product class because they provide broad-spectrum pest control, rapid knockdown performance, and compatibility with major row crops such as soybean, corn, cotton, and sugarcane. Brazil growers frequently utilize pyrethroid-based products for management of caterpillars, stink bugs, armyworms, and sucking pests. Their affordability, established efficacy, widespread dealer availability, and integration into resistance-management programs further support their dominance. While biological insecticides are gaining traction, particularly in soybean-producing states, pyrethroids remain the preferred choice for large-scale commercial farming operations due to operational familiarity and proven field performance.

By Crop Type

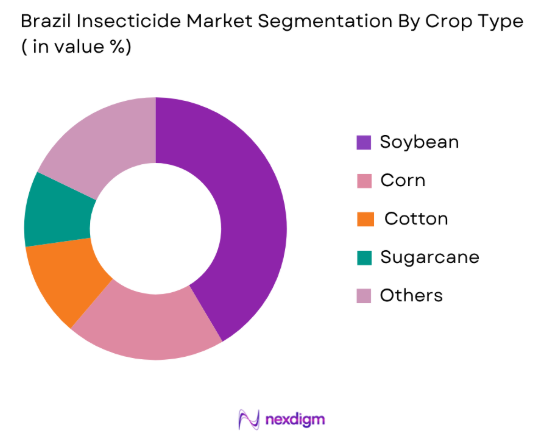

Brazil Insecticide Market is segmented by crop type into soybean, corn, cotton, sugarcane, coffee, citrus, fruits and vegetables, and other specialty crops. Recently, soybean has held the dominant market share under crop type because Brazil remains the largest soybean producer and exporter globally. Soybean cultivation covers extensive agricultural acreage and is highly vulnerable to pests such as stink bugs, caterpillars, whiteflies, and armyworms. Growers invest heavily in insecticide applications to protect yields and maintain export-quality standards. The prevalence of multiple annual crop cycles, tropical climate conditions, and resistance management requirements further increase insecticide demand in soybean cultivation. In addition, the rapid expansion of soybean acreage into agricultural frontiers such as MATOPIBA continues to reinforce soybean’s leadership position within Brazil’s insecticide consumption landscape.

Competitive Landscape

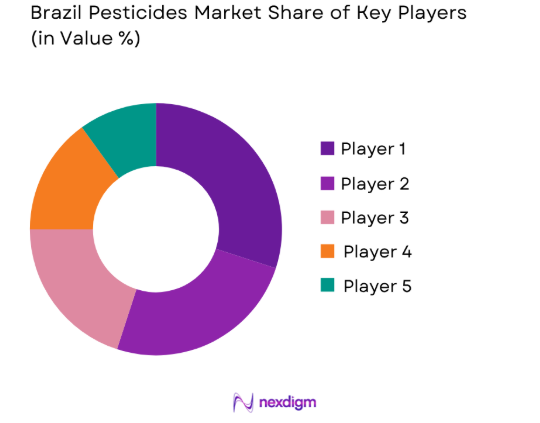

The Brazil Insecticide Market is dominated by a mix of multinational crop protection companies and local agrochemical manufacturers. Global leaders such as Bayer Crop Science, Syngenta, BASF, Corteva, and FMC control a significant portion of insecticide registrations, dealer networks, and crop protection innovation. Competition is driven by active ingredient portfolios, biological product development, dealer reach, agronomic support services, and resistance-management solutions. The growing shift toward biological crop protection is also creating opportunities for specialized biological product manufacturers.

| Company | Establishment Year | Headquarters | Insecticide Portfolio Strength | Biological Portfolio | Key Crop Focus | Dealer Network Strength | Manufacturing Presence | Competitive Position |

| Bayer Crop Science | 1863 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Syngenta Group | 2000 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| BASF Agricultural Solutions | 1865 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Corteva Agriscience | 2019 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

Brazil Insecticide Market

Growth Drivers

Soybean and Corn Acreage Expansion Driving Insecticide Demand

Brazil Insecticide Market is primarily driven by the continuous expansion of soybean and corn cultivation, which increases demand for pest management solutions across major agricultural regions. Brazil produced approximately 169 million metric tons of soybeans and over 130 million metric tons of corn during the latest harvest cycle, maintaining its position as one of the world’s largest agricultural producers. Soybean cultivation exceeded 45 million hectares, creating substantial exposure to caterpillars, stink bugs, whiteflies, and armyworms that require multiple insecticide applications. The broader Brazil crop protection market reached approximately USD 14.3 billion, supported by soybean, corn, sugarcane, and coffee production. Large-scale commercial farming operations and multiple annual crop cycles further strengthen insecticide consumption across Mato Grosso, Paraná, Goiás, and Rio Grande do Sul.

Rising Pest Resistance and Intensification of Crop Protection Programs

Brazil Insecticide Market continues to benefit from increasing pest resistance and the need for more sophisticated crop protection strategies. According to industry data, the area treated with pesticides in Brazil exceeded 1 billion hectares during the first three quarters of 2024, reflecting growing pest pressure and expanded treatment intensity across major crops. Brazil remains one of the world’s largest consumers of crop protection products because tropical climatic conditions support year-round insect activity and multiple pest generations. Soybean, corn, cotton, and sugarcane producers increasingly rely on integrated resistance-management programs involving multiple insecticide classes and biological products. The intensification of commercial agriculture and focus on maintaining export-quality yields continue to drive insecticide adoption across Brazil’s farming sector.

Market Challenges

Resistance Development Among Key Agricultural Pests

Brazil Insecticide Market faces a significant challenge from the growing resistance of major pests to conventional insecticide chemistries. Continuous cultivation of soybean, corn, cotton, and sugarcane across millions of hectares has increased exposure of pests to repeated insecticide applications, accelerating resistance development. Brazil treated more than 1 billion hectares with crop protection products during 2024, highlighting the scale of pest management activities. Resistance among caterpillars, stink bugs, and whiteflies often requires farmers to rotate active ingredients and adopt more expensive integrated pest management programs. This increases operational complexity for growers while creating pressure on manufacturers to develop novel chemistries and biological alternatives capable of maintaining efficacy under evolving field conditions.

Environmental and Regulatory Compliance Requirements

Brazil Insecticide Market faces increasing scrutiny regarding environmental safety, residue compliance, and regulatory oversight. Regulatory agencies including MAPA, ANVISA, and IBAMA continue strengthening evaluation procedures for crop protection products and environmental monitoring requirements. Recent enforcement actions involving pesticide formulations have highlighted the importance of compliance across manufacturing, registration, and distribution activities. Brazil’s position as a major agricultural exporter requires producers to meet international residue standards for soybean, corn, coffee, sugarcane, and cotton exports. Compliance requirements increase development timelines and operational obligations for manufacturers while encouraging investment in safer formulations, biological insecticides, and sustainable crop protection solutions.

Market Opportunities

Rapid Growth of Biological Insecticides and Sustainable Crop Protection

Brazil Insecticide Market has a major opportunity in biological insecticides and bio-based crop protection technologies. Retail sales of biological inputs reached approximately BRL 5 billion during the 2023/24 season, demonstrating strong farmer acceptance of sustainable pest management solutions. Brazil’s bioinput market has recorded average annual growth substantially above global averages, supported by increasing adoption in soybean, corn, sugarcane, cotton, and coffee cultivation. Mato Grosso alone represents a significant share of biological product utilization due to its large agricultural footprint. Biological insecticides offer resistance-management benefits, lower environmental impact, and compatibility with integrated pest management programs, positioning this segment as one of the most attractive growth opportunities within Brazil’s crop protection industry.

Precision Agriculture and Drone-Based Application Technologies

Brazil Insecticide Market is witnessing growing opportunities from precision agriculture technologies, digital farming platforms, and drone-based pesticide applications. Brazil’s large-scale commercial farms increasingly adopt precision spraying systems to optimize product utilization and improve pest-control efficiency. The country remains one of the largest crop protection markets globally, supported by extensive soybean cultivation exceeding 45 million hectares and large-scale corn, cotton, and sugarcane production. Precision technologies allow growers to target infestations more effectively, reduce application waste, and improve environmental stewardship. Integration of digital monitoring systems, remote sensing technologies, and automated application equipment is creating new opportunities for manufacturers, service providers, and technology suppliers operating within Brazil’s evolving insecticide ecosystem.

Future Outlook

The Brazil Insecticide Market is expected to witness steady growth over the forecast period, supported by expansion of soybean cultivation, increasing pest resistance, adoption of precision agriculture technologies, and the need to improve agricultural productivity. As Brazil continues strengthening its position as a global agricultural powerhouse, demand for effective crop protection solutions is expected to remain strong across major farming regions. Biological insecticides are expected to gain significant traction due to increasing sustainability requirements and regulatory support for environmentally friendly crop protection solutions. Drone-based application technologies, digital pest monitoring systems, and precision spraying equipment are likely to improve application efficiency and optimize insecticide usage. Growth opportunities will also emerge from specialty crops, coffee plantations, citrus orchards, and export-oriented farming operations. Integrated pest management programs and resistance-management strategies are expected to become increasingly important as growers seek to maximize yields while complying with environmental and export regulations.

Major Players

- Bayer Crop Science

- Syngenta Group

- BASF Agricultural Solutions

- Corteva Agriscience

- FMC Corporation

- UPL Limited

- ADAMA Agricultural Solutions

- Sumitomo Chemical

- Nufarm Limited

- Ourofino Agrociência

- IHARA

- Sipcam Nichino Brasil

- Albaugh LLC

- Biotrop Soluções Biológicas

- Koppert Brasil

Key Target Audience

- Crop Protection Chemical Manufacturers

- Biological Crop Protection Companies

- Agricultural Cooperatives

- Commercial Farming Enterprises

- Agrochemical Distributors and Dealers

- Agribusiness Groups and Plantation Operators

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the Brazil Insecticide Market. This includes insecticide manufacturers, biological product suppliers, agricultural retailers, cooperatives, distributors, growers, agronomists, and regulatory agencies. The objective is to identify key variables influencing demand, product adoption, pest management practices, and regional consumption patterns.

Step 2: Market Analysis and Construction

In this phase, historical data pertaining to the Brazil Insecticide Market is compiled and analyzed. This includes insecticide consumption, crop acreage, pest incidence trends, crop protection expenditures, active ingredient demand, and regional agricultural production. Market estimates are validated using top-down and bottom-up methodologies.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and validated through computer-assisted telephone interviews with agrochemical manufacturers, distributors, growers, agricultural cooperatives, crop consultants, and pest management specialists. These consultations provide operational insights into purchasing behavior, product preferences, resistance management strategies, and adoption of biological alternatives.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with industry participants to validate segmentation, competitive positioning, growth drivers, and future opportunities. Secondary research findings are triangulated with primary interviews and industry data to ensure a comprehensive, accurate, and validated assessment of the Brazil Insecticide Market.

- Executive Summary

- Research Methodology (Market definitions and assumptions, abbreviations, Brazil insecticide taxonomy, active ingredient classification, crop protection scope, agricultural and non-agricultural insecticide inclusion, MAPA registration framework, ANVISA toxicological classification, IBAMA environmental assessment framework, market sizing approach, top-down and bottom-up triangulation, manufacturer interviews, distributor validation, grower surveys, agronomist consultations, pest incidence analysis, treated acreage assessment, limitations and future conclusions)

- Definition and Scope

- Overview Genesis

- Timeline of Major Players

- Business Cycle

- Supply Chain and Value Chain Analysis

- Growth Drivers (Soybean acreage expansion, corn cultivation growth, tropical pest pressure, export-oriented agriculture, crop yield protection demand, pest resistance development, precision agriculture adoption, biological insecticide penetration)

- Market Challenges (Resistance management issues, counterfeit agrochemicals, regulatory approval timelines, environmental compliance requirements, climatic variability, supply chain dependence, rising input costs, pest adaptation)

- Opportunities (Biological crop protection, integrated pest management programs, drone spraying adoption, precision agriculture technologies, specialty crop expansion, sustainable farming initiatives, digital pest monitoring, regenerative agriculture practices)

- Market Trends (Biological insecticide adoption, precision application technologies, resistance management programs, digital agriculture integration, drone-based spraying, reduced-risk chemistries, sustainable crop protection, data-driven farming)

- Government Regulation (MAPA registrations, ANVISA toxicological assessments, IBAMA environmental approvals, residue compliance standards, pesticide registration requirements, export crop standards, sustainable agriculture policies, environmental monitoring requirements)

- SWOT Analysis

- Stakeholder Ecosystem

- Porter’s Five Forces

- By Market Value (2020-2025)

- By Volume Consumption (2020-2025)

- By Active Ingredient Consumption (2020-2025)

- By Product Categories (In Value %)

Pyrethroids

Neonicotinoids

Organophosphates

Diamides

Carbamates

Biological Insecticides

Insect Growth Regulators (IGRs)

Spinosyns

Other Novel Chemistries - By Crop Type (In Value %)

Soybean

Corn

Cotton

Sugarcane

Coffee

Citrus

Fruits and Vegetables

Other Specialty Crops - By Application Method (In Value %)

Foliar Spray

Seed Treatment

Soil Application

Aerial Application

Drone-Based Application

Chemigation - By Pest Type (In Value %)

Caterpillars and Lepidopteran Pests

Whiteflies

Aphids

Stink Bugs

Armyworms

Borers

Beetles and Coleopteran Pests

Other Insect Pests

- Market Share of Major Players (Market value, volume sales, active ingredient portfolio, treated acreage coverage, crop penetration, biological product portfolio, dealer network, regional footprint)

- Cross Comparison Parameters (Registered active ingredients, biological insecticide portfolio, soybean and corn crop penetration, dealer and cooperative network strength, manufacturing and formulation capacity, R&D investment in crop protection, resistance management solutions, precision agriculture integration capability)

- SWOT Analysis of Major Players

- Pricing Analysis Basis SKUs (Lambda-cyhalothrin formulations, Imidacloprid formulations, Chlorantraniliprole formulations, Bifenthrin formulations, Spinosad products, Biological insecticides, Seed treatment insecticides, Whitefly control products, Armyworm control products, Caterpillar control products)

- Detailed Profiles of Major Companies

Bayer Crop Science

Syngenta Group

BASF Agricultural Solutions

Corteva Agriscience

FMC Corporation

UPL Limited

ADAMA Agricultural Solutions

Sumitomo Chemical

Nufarm Limited

Ourofino Agrociência

IHARA

Sipcam Nichino Brasil

Albaugh LLC

Biotrop Soluções Biológicas

Koppert Brasil

- Soybean Grower Analysis

- Corn Producer Analysis

- Cotton Farmer Analysis

- Sugarcane Plantation Analysis

- Agricultural Cooperative Analysis

- Large Agribusiness Group Analysis

- By Market Value (2026-2035)

- By Volume Consumption (2026-2035)

- By Active Ingredient Consumption (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now