Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Brazil’s semiconductor infrastructure market reached approximately USD ~ billion based on a recent historical assessment, driven by expansion of electronics manufacturing, automotive electronics demand, telecommunications equipment production, and growth of data center and AI hardware supply chains. Government semiconductor policy initiatives and incentives for domestic packaging and testing capacity further support infrastructure investment. Rising demand for chips in consumer electronics, industrial automation, and connectivity devices reinforces sustained semiconductor ecosystem development across Brazil.

Campinas and São Paulo dominate Brazil’s semiconductor infrastructure landscape due to electronics manufacturing clusters, research institutions, and proximity to major industrial and automotive production hubs. Southern regions support semiconductor packaging and component assembly linked to electronics and telecom industries, while Manaus free trade zone hosts large-scale consumer electronics manufacturing facilities. Strong logistics networks, skilled engineering workforce, and industrial policy incentives reinforce regional leadership. National technology development programs and supply chain localization efforts further strengthen semiconductor infrastructure growth across Brazil.

Market Segmentation

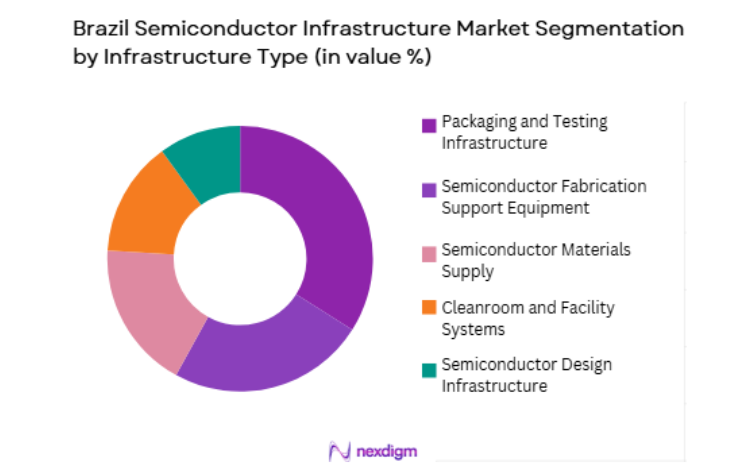

By Infrastructure Type

Brazil Semiconductor Infrastructure market is segmented by infrastructure type into semiconductor fabrication support equipment, packaging and testing infrastructure, semiconductor materials supply, cleanroom and facility systems, and semiconductor design infrastructure. Recently, packaging and testing infrastructure has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference.

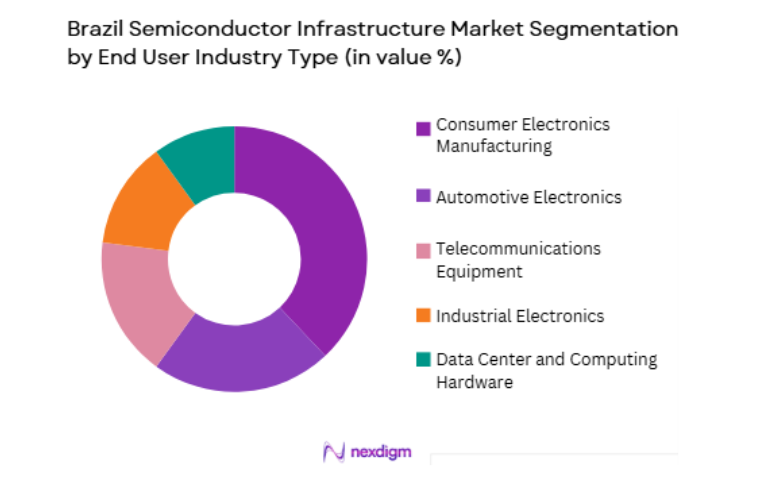

By End User Industry

Brazil Semiconductor Infrastructure market is segmented by end user industry into consumer electronics manufacturing, automotive electronics, telecommunications equipment, industrial electronics, and data center and computing hardware. Recently, consumer electronics manufacturing has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference.

Competitive Landscape

Brazil’s semiconductor infrastructure market is fragmented with presence of global semiconductor equipment suppliers, materials providers, and local electronics manufacturing infrastructure firms supporting packaging, testing, and assembly operations. Competitive dynamics are influenced by international technology partnerships, government incentives, and localization strategies targeting downstream semiconductor value chain activities rather than advanced wafer fabrication. Multinational electronics manufacturers and OSAT providers anchor infrastructure demand across Brazil.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Brazil Semiconductor Infrastructure Presence |

| ASE Technology | 1984 | Taiwan | ~ | ~ | ~ | ~ | ~ |

| Amkor Technology | 1968 | USA | ~ | ~ | ~ | ~ | ~ |

| Applied Materials | 1967 | USA | ~ | ~ | ~ | ~ | ~ |

| Tokyo Electron | 1963 | Japan | ~ | ~ | ~ | ~ | ~ |

| Merck Electronics | 1668 | Germany | ~ | ~ | ~ | ~ | ~ |

Brazil Semiconductor Infrastructure Market Analysis

Growth Drivers

Electronics Manufacturing Expansion and Localization of Semiconductor Value Chain

Brazil’s large consumer electronics manufacturing base, concentrated in Manaus and southeastern industrial corridors, drives sustained demand for semiconductor packaging, testing, materials, and facility infrastructure supporting assembly and integration of imported semiconductor components into finished electronic products nationwide. Multinational electronics manufacturers producing smartphones, televisions, computing devices, and appliances require local semiconductor backend services to optimize supply chains and reduce import dependence. Government industrial policies incentivize domestic semiconductor ecosystem development through tax benefits and localization programs. Automotive electronics growth in Brazil’s vehicle manufacturing sector increases demand for semiconductor component integration infrastructure. Telecom equipment production supporting national connectivity expansion requires semiconductor packaging and testing capabilities. Industrial automation and IoT device manufacturing further increase semiconductor infrastructure requirements. Expansion of contract electronics manufacturing services strengthens backend semiconductor ecosystem capacity. Localization of semiconductor assembly reduces logistics costs and lead times for electronics producers.

Government Semiconductor Policy and Strategic Technology Development Initiatives

Brazilian government initiatives aimed at strengthening national semiconductor capability through funding programs, tax incentives, and research partnerships are stimulating infrastructure investment in semiconductor design, packaging, materials, and facility development across technology clusters. Public policy recognizes semiconductors as strategic components for digital sovereignty and industrial competitiveness. National semiconductor programs support creation of design centers, packaging facilities, and advanced materials production. Collaboration between universities and industry accelerates semiconductor research infrastructure deployment. Incentives for domestic electronics production indirectly increase semiconductor backend demand. Technology parks and innovation clusters receive funding for semiconductor ecosystem development. Public procurement policies favor local electronics manufacturing, reinforcing infrastructure investment. Partnerships with international semiconductor firms transfer technology and expertise into Brazil.

Market Challenges

Absence of Advanced Wafer Fabrication Capability and High Capital Barriers

Brazil lacks advanced semiconductor wafer fabrication facilities due to extremely high capital requirements, technology complexity, and scale economics, limiting its semiconductor infrastructure market to backend and support segments rather than full value chain participation. Establishing competitive fabrication plants requires multi-billion-dollar investment beyond domestic market scale. Limited domestic demand for advanced nodes constrains economic viability of local fabs. Dependence on imported semiconductor wafers exposes downstream manufacturing to supply chain risks. Technology transfer barriers and intellectual property constraints restrict local fabrication development. Skilled workforce availability for advanced semiconductor manufacturing remains limited. Infrastructure requirements for fabs including ultra-clean facilities and stable utilities present additional barriers. Global competition from established semiconductor regions reduces investment attractiveness.

Import Dependence and Supply Chain Vulnerability in Semiconductor Materials and Equipment

Brazil’s semiconductor infrastructure relies heavily on imported equipment, chemicals, wafers, and advanced materials supplied by global semiconductor firms, creating vulnerability to international trade disruptions, currency fluctuations, and export controls affecting infrastructure expansion and operational continuity. Semiconductor process equipment and materials have limited domestic production alternatives. Import duties increase cost of semiconductor infrastructure development. Supply chain disruptions can delay packaging and testing operations dependent on imported inputs. Currency depreciation increases procurement costs for infrastructure investors. Domestic suppliers lack scale to replace imported semiconductor materials. Logistics delays affect electronics manufacturing schedules. Strategic technology restrictions limit access to advanced semiconductor equipment.

Opportunities

Growth of Automotive Electronics and Electrification Supply Chain

Brazil’s expanding automotive manufacturing sector and transition toward electrification, advanced driver assistance systems, and connected vehicles create new demand for semiconductor packaging, testing, and integration infrastructure supporting automotive electronics production nationwide. Modern vehicles require increasing semiconductor content for power electronics, sensors, and connectivity modules. Local automotive manufacturing clusters require proximate semiconductor backend services. Electric vehicle component production increases semiconductor demand intensity. Automotive safety and control systems rely on specialized semiconductor packaging solutions. Partnerships between automotive OEMs and electronics manufacturers expand infrastructure requirements. Electrification initiatives stimulate power semiconductor integration infrastructure. Localization of automotive electronics supply chains increases semiconductor backend investment. Growth of connected mobility technologies reinforces long-term semiconductor infrastructure demand in Brazil.

Semiconductor Design and Research Ecosystem Development

Expansion of semiconductor design capabilities and research infrastructure in Brazil through university programs, innovation hubs, and government-funded technology centers creates opportunities for development of design tools, prototyping facilities, and semiconductor ecosystem support infrastructure. Fabless semiconductor startups and research teams require design software, testing labs, and prototyping capabilities. National AI and electronics programs support chip design research initiatives. Collaboration with international semiconductor firms enhances local design expertise. Development of application-specific integrated circuits for local industries increases design infrastructure demand. Academic semiconductor research projects stimulate laboratory and testing facility investment. Government innovation funding supports semiconductor startups. Growth of design ecosystem complements packaging and assembly infrastructure.

Future Outlook

Brazil’s semiconductor infrastructure market is expected to expand steadily over the next five years supported by electronics manufacturing growth, automotive electronics demand, and government semiconductor ecosystem initiatives. Packaging and testing capacity will continue expanding to support domestic electronics production. Automotive electrification and connectivity technologies will increase semiconductor integration needs. Design and research infrastructure investment will strengthen ecosystem capability. Brazil will reinforce its role as Latin America’s primary semiconductor backend and electronics manufacturing hub.

Major Players

- ASE Technology

- Amkor Technology

- Applied Materials

- Tokyo Electron

- Merck Electronics

- TSMC

- GlobalFoundries

- Intel

- Samsung Electronics

- STMicroelectronics

- NXP Semiconductors

- Infineon Technologies

- Qualcomm

- Foxconn

- Flex

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Electronics manufacturing companies

- Automotive OEMs

- Semiconductor packaging and testing firms

- Telecom equipment manufacturers

- Industrial electronics producers

- Semiconductor design firms

Research Methodology

Step 1: Identification of Key Variables

Key variables including semiconductor packaging capacity, electronics manufacturing output, automotive electronics demand, semiconductor materials imports, and policy incentives were identified through industry and government data sources.

Step 2: Market Analysis and Construction

Market sizing and segmentation were constructed using semiconductor equipment and materials revenue data, electronics production statistics, and infrastructure investment indicators across Brazil.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings were validated through consultations with semiconductor equipment suppliers, electronics manufacturers, and policy experts to confirm demand drivers and infrastructure trends.

Step 4: Research Synthesis and Final Output

Validated insights were synthesized into structured analysis covering segmentation, market dynamics, competitive landscape, and outlook ensuring coherent conclusions.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Government initiatives to localize semiconductor manufacturing

Rising electronics and automotive semiconductor demand

Expansion of packaging and test capacity in Brazil - Market Challenges

High capital intensity of semiconductor fabs

Limited domestic semiconductor ecosystem and suppliers

Dependence on imported advanced equipment and materials - Market Opportunities

Development of regional semiconductor packaging hubs

Public private partnerships for semiconductor fabs

Growth in specialty and mature node semiconductor production - Trends

Shift toward advanced packaging and heterogeneous integration

Adoption of automation in semiconductor fabs - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Wafer Fabrication Equipment

Semiconductor Assembly and Packaging Equipment

Semiconductor Testing and Metrology Systems

Cleanroom and Fab Facility Infrastructure

Semiconductor Materials Handling Systems - By Platform Type (In Value%)

Front End Wafer Fabrication Facilities

Back End Assembly and Packaging Facilities

Semiconductor R&D and Pilot Lines

Specialty Semiconductor Fabs

Outsourced Semiconductor Manufacturing Facilities - By Fitment Type (In Value%)

New Semiconductor Fab Construction

Fab Expansion and Retrofit Projects

Modular Cleanroom Installations

Integrated Fab Infrastructure Solutions - By End User Segment (In Value%)

Integrated Device Manufacturers

Outsourced Semiconductor Assembly and Test Providers

Research Institutes and Universities

- Market Share Analysis

- Cross Comparison Parameters (Process Node Capability, Fab Scale, Automation Level, Yield Efficiency, Packaging Technology, Equipment Sophistication, Cleanroom Class, Throughput Capacity, Energy Efficiency, Materials Handling Automation, Technology Maturity, Capex Intensity)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

ASML

Applied Materials

Lam Research

KLA Corporation

Tokyo Electron

SCREEN Semiconductor Solutions

ASM International

Teradyne

Advantest

TSMC

Samsung Electronics

Intel

GlobalFoundries

Amkor Technology

ASE Technology

- IDMs exploring local semiconductor production capacity

- OSAT providers expanding packaging and test operations

- Research institutes supporting semiconductor R&D capability

- Manufacturers seeking secure local chip supply

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now