Download PDF

Download PDF Download PDF

Download PDFMarket Overview

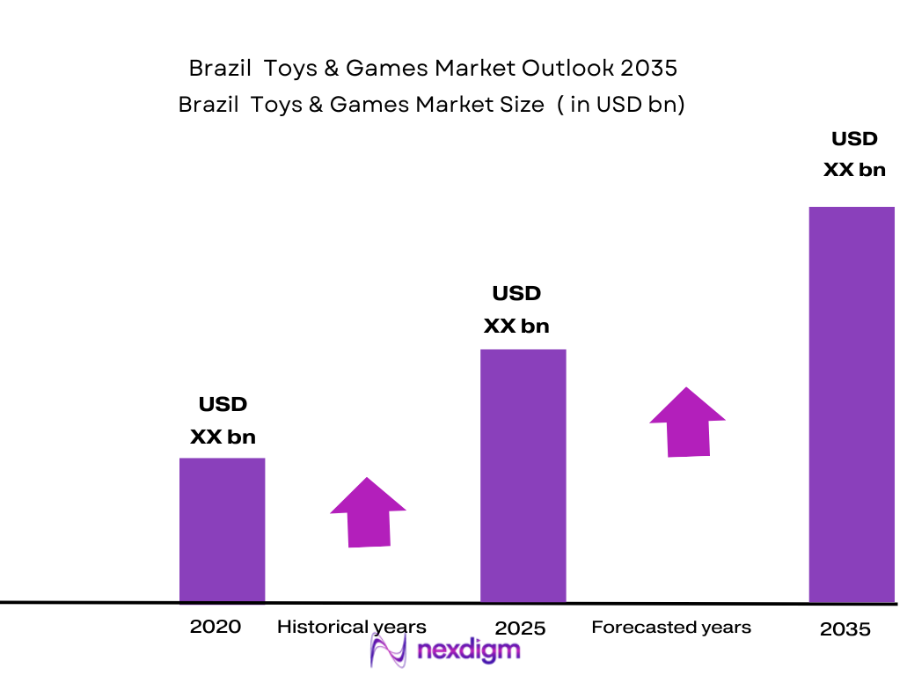

The Brazil toys and games market is valued at approximately USD ~ billion in 2025, reflecting consumer demand for both traditional physical toys and digital gaming experiences. This valuation is backed by Spherical Insights & Consulting industry data, which highlights increasing disposable income among Brazilian households and expanding retail accessibility as key drivers for this consumer category. Urbanization and a large base of households with children support expenditure on toys, games, and interactive entertainment products.

Major cities such as São Paulo and Rio de Janeiro play an outsized role in driving the Brazil toys & games market due to their denser populations, higher household incomes, and stronger retail infrastructure. These urban centers concentrate national distribution networks and serve as hubs for large specialty stores and multimedia entertainment channels, making them dominant consumption and distribution points in the country’s toy ecosystem. Presence of large shopping centers and established omnichannel retail supports this dominance.

The forecast period (2025–2035) suggests the market will grow at a CAGR of around 4.2%, reaching an estimated USD ~ billion by 2035, driven by sustained household spending, rising educational toy demand, and digital gaming integration.

Market Segmentation

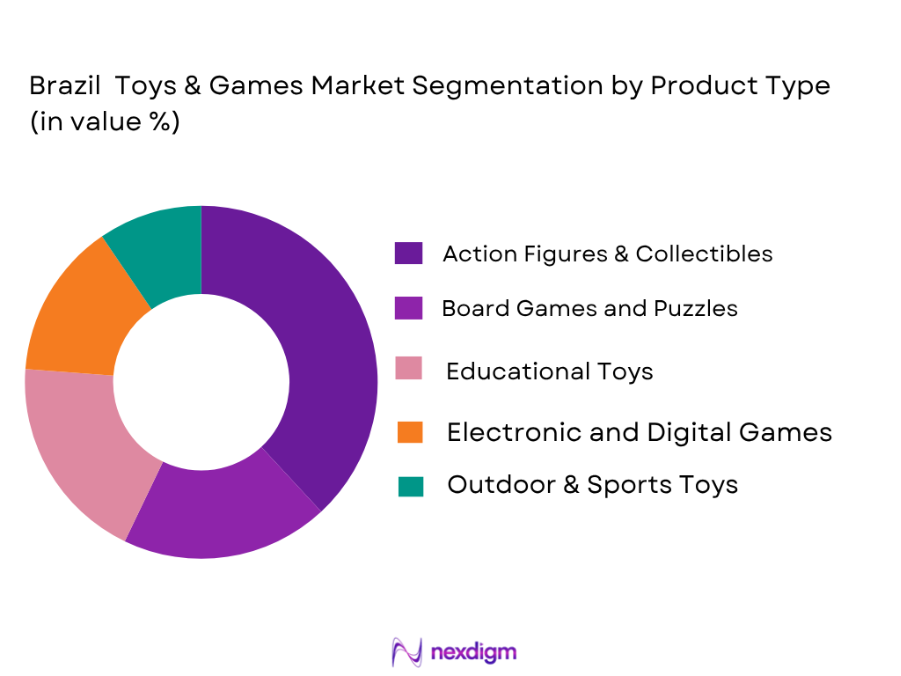

By Product Type

Brazil toys & games market is segmented into video games, board games & puzzles, dolls & figures, outdoor & sports toys, educational toys, and others. The video games sub‑segment currently dominates the product type landscape, driven by widespread smartphone use, affordable mobile data access, and strong internet connectivity that enable rich digital gaming experiences. A large youth and young adult population actively engages with mobile, console, and online gaming, including esports and social play platforms that encourage continual spending. Popular global gaming franchises and frequent content updates further uplift consumer engagement and revenue generation. Additionally, the trend toward digital purchases, downloadable content, and in‑app purchases amplifies video game spending relative to traditional physical toy categories. The strong appeal of gaming across broader age cohorts, not limited to children, reinforces this segment’s leading position in the product mix.

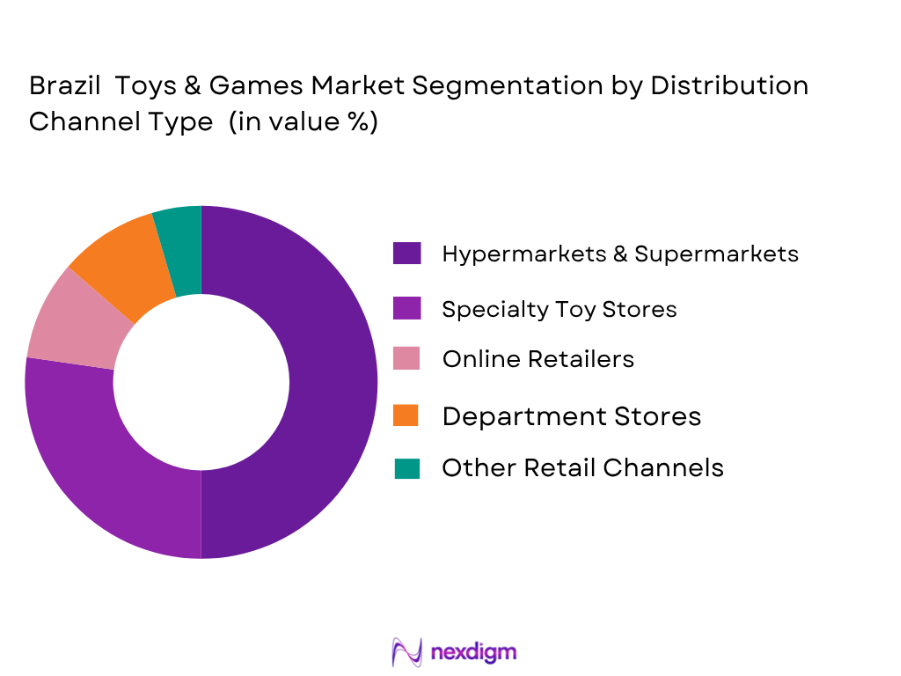

By Distribution Channel

The Brazil toys & games market is segmented by distribution into offline retail, online retail, specialty stores, and other channels. The offline retail channel continues to hold the largest share due to the established presence of supermarkets, hypermarkets, and large department stores across both urban and regional markets. These traditional outlets extend deep geographic coverage and provide consumers with tactile shopping experiences where they can inspect products before purchase. Price‑conscious families often prefer in‑store purchases for toys and games due to promotional pricing, bundling offers, and seasonal sales events that are typical in offline retail. Furthermore, many Brazilian consumers still prefer physical retail formats for toy purchases, especially in smaller towns where e‑commerce infrastructure and delivery reliability may be limited. The offline channel’s entrenched position is reinforced by strong relationships between major toy manufacturers and retailers, which ensure product visibility and distribution breadth.

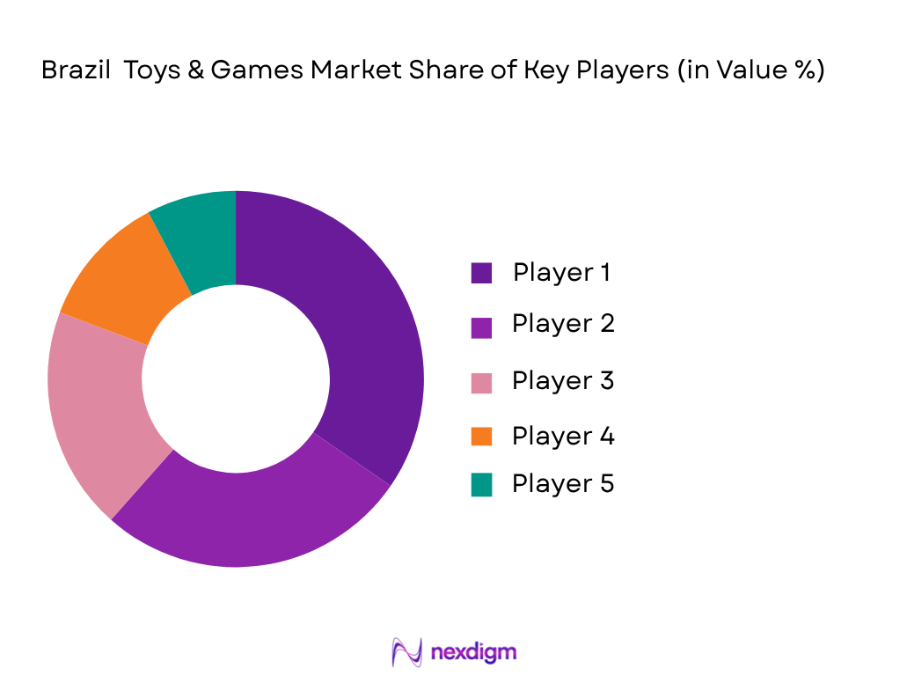

Competitive Landscape

The Brazil toys & games market features a mix of domestic manufacturers and global brands competing across traditional and digital play categories. The Brazil toys & games arena includes both local brands with strong cultural resonance as well as multinational companies leveraging licensing and distribution networks.

| Company | Establishment Year | Headquarters | Product Focus | Primary Channels | Geographic Reach | Licensing Agreements | Digital Integration |

| Manufatura de Brinquedos Estrela S.A. | 1937 | São Paulo, Brazil | ~ | ~ | ~ | ~ | ~ |

| Hasbro, Inc. | 1923 | USA | ~ | ~ | ~ | Brazil Toys & Games Market Outlook to 2035 | ~ |

| Mattel, Inc. | 1945 | USA | ~ | ~ | ~ | ~ | ~ |

| LEGO Group | 1932 | Denmark | ~ | ~ | ~ | ~ | ~ |

| Grow Jogos e Brinquedos S.A. | 1972 | São Paulo, Brazil | ~ | ~ | ~ | ~ | ~ |

Brazil Toys & Games Market Analysis

Growth Drivers

Increasing Adoption of Educational and STEM Toys

The adoption of educational and STEM (Science, Technology, Engineering, and Mathematics) toys is rising steadily in Brazil, reflecting growing parental focus on cognitive and skill development. Families increasingly prefer toys that combine learning with engagement, such as coding kits, robotics sets, and interactive science kits. Educational institutions and extracurricular programs are integrating STEM-oriented activities, reinforcing demand for these products. Leading manufacturers are expanding portfolios to include innovative educational solutions, often tied to technology or gamified learning. This trend is particularly strong in urban centers with higher awareness of global educational standards. Parents perceive these toys as investments in their children’s future, which has increased market penetration and revenue generation for STEM-focused categories.

High Import Dependency and Supply Chain Disruptions

Brazil’s toys and games market relies heavily on imported products, particularly for electronic toys, video games, and licensed merchandise. This dependency exposes the market to global supply chain disruptions, shipping delays, and currency fluctuations, which can impact pricing and availability. Import tariffs and logistics bottlenecks further increase the cost of products, affecting affordability for middle-income households. Disruptions caused by international events, such as port congestion or production delays in Asia and Europe, have a direct impact on inventory levels in Brazilian retailers. Consequently, manufacturers and distributors must manage uncertainties in sourcing and transportation, often requiring buffer stock or alternative suppliers. These factors can slow market expansion and limit timely introduction of high-demand products.

Price Sensitivity Among Consumers

Consumer price sensitivity remains a significant constraint for the Brazil toys and games market, especially among middle and lower-income segments. High-end or imported toys often command premium prices, which can deter purchases in a market with tight discretionary spending. Seasonal promotions and discounts heavily influence buying behavior, with families often waiting for sales periods to purchase high-value products. Price-conscious consumers may also substitute physical toys with lower-cost alternatives, second-hand items, or digital games. Manufacturers face the challenge of balancing quality and affordability while remaining competitive. Pricing pressure is further exacerbated by competition from digital entertainment, which offers high engagement at lower costs, making conventional toys more vulnerable to shifts in consumer preference.

Opportunities

Growth of Edutainment and STEM Toys

The edutainment segment, combining education with entertainment, presents a major opportunity in Brazil’s toys and games market. Increasing parental awareness about skill development, creativity, and learning outcomes drives demand for products like coding robots, puzzle-solving kits, and science experiments. Schools and after-school programs also encourage the adoption of STEM toys, often sourcing them in bulk for classroom use. Manufacturers can leverage technology integration, including augmented reality (AR) and app-connected toys, to enhance interactive learning. International collaborations and licensing agreements allow local brands to introduce innovative educational products at competitive pricing. As a result, edutainment and STEM-focused toys are positioned as both high-value and high-demand segments, offering sustained revenue growth and brand differentiation.

Expansion of Online Gaming and Mobile Gaming

Digital transformation in Brazil has accelerated the adoption of online gaming and mobile gaming, creating new market avenues for toy and game manufacturers. Smartphones, tablets, and internet connectivity allow consumers to engage with mobile games, virtual collectibles, and gamified learning apps. Traditional toy companies are incorporating digital components, such as AR features and companion apps, to bridge physical and digital play. The rise of cloud gaming and subscription-based models further enhances accessibility to high-quality gaming experiences. Online platforms also provide direct-to-consumer sales channels, reducing dependence on physical retail. Expanding digital engagement enables companies to reach broader age groups, increase brand loyalty, and drive recurring revenue streams from digital content linked to physical toys.

Future Outlook

Over the next decade, the Brazil toys & games market is anticipated to expand steadily as consumer preferences evolve toward digital and interactive play. Continued growth in internet penetration and online retail will enhance access to a wider variety of products across geographic regions. Rising parental emphasis on educational value and cognitive development will sustain demand for STEM‑oriented and dual‑purpose toys that blend learning with play.

Increasing investment in digital content, interactive game platforms, and licensing tie‑ins with entertainment media is expected to further diversify product offerings. The market’s resilience will be supported by Brazil’s demographic profile, with a significant base of young consumers and rising discretionary spending among middle‑income households. Expansion of e‑commerce infrastructure and improved logistics will also drive penetration into semi‑urban and rural areas. Innovation in eco‑friendly and sustainable toy designs may further influence consumer choices and competitive dynamics.

Major Players

- Manufatura de Brinquedos Estrela S.A.

- Hasbro, Inc.

- Mattel, Inc.

- LEGO Group

- Grow Jogos e Brinquedos S.A.

- Tectoy S.A.

- Candide Indústria e Comércio Ltda.

- Brinquedos Bandeirante S.A.

- Ri Happy Brinquedos

- Spin Master Corp.

- VTech Holdings Ltd.

- Funko, Inc.

- Ravensburger AG

- Mega Brands

- Jakks Pacific, Inc.

Key Target Audience

- Potential buyers and stakeholders

- Strategic Investors and Private Equity Firms

- Investments and Venture Capitalist Firms

- Consumer Goods Corporations

- Retail and Distribution Chain Executives

- Toy and Game Manufacturers

- Marketing and Brand Licensing Departments

- Government and Regulatory Bodies

- Supply Chain and Logistics Operators

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves mapping all relevant stakeholders in the Brazil toys & games market, including manufacturers, retailers, distributors, and consumers. Secondary research from reputable industry databases, trade publications, and government statistics is used to establish key influencing variables.

Step 2: Market Analysis and Construction

This stage compiles historical sales, revenue, and distribution channel data to understand penetration levels and revenue generation. Offline and online sales data are evaluated to ensure accuracy and a complete picture of market structure and growth drivers.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are formulated and validated through interviews with industry experts, toy manufacturers, retail executives, and category managers. These consultations provide practical insights into operational challenges, consumer preferences, and competitive dynamics.

Step 4: Research Synthesis and Final Output

Final output involves integrating primary and secondary data using bottom‑up and top‑down approaches. Direct engagement with market participants helps refine segment forecasts, validate market drivers, and ensure the resulting analysis reflects real‑world market conditions.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Sizing Approach, Consolidated Research Approach, Understanding Market Potential Through In-Depth Industry Interviews, Primary Research Approach, Limitations and Future Conclusions)

- Definition and Scope

- Market Dynamics Overview

- Market Genesis

- Major Players and Market Timeline

- Business Cycle and Trends

- Supply Chain and Value Chain Analysis

- Growth Drivers

Rising Disposable Income and Urbanization

Increasing Adoption of Educational and STEM Toys

Digital Transformation and E-Gaming Popularity

Expansion of Online Retail Channels - Market Challenges

High Import Dependency and Supply Chain Disruptions

Price Sensitivity Among Consumers

Competition from Alternative Entertainment Modes

Regulatory Compliance and Safety Standards - Opportunities

Growth of Edutainment and STEM Toys

Expansion of Online Gaming and Mobile Gaming

Licensing and Character-Branded Toys

Increase in Subscription Box Services - Trends

Popularity of Interactive and Smart Toys

Sustainability and Eco-Friendly Toy Materials

Integration of AR/VR in Games

Rise of Collectibles and Limited Edition Toys - Government Regulations

Product Safety and Certification Requirements

Import and Customs Regulations

Consumer Protection Policies

Environmental and Recycling Regulations - SWOT Analysis

- Porter’s Five Forces Analysis

- By Value, 2020-2025

- By Volume, 2020-2025

- By Average Price, 2020-2025

- By Product Type (In Value %)

Action Figures & Collectibles

Board Games & Puzzles

Educational Toys

Electronic & Digital Games

Outdoor & Sports Toys - By Age Group (In Value %)

Infants & Toddlers

Children (3-12 Years)

Teenagers (13-18 Years)

Adults - By Distribution Channel (In Value %)

Hypermarkets & Supermarkets

Specialty Toy Stores

Online Retailers

Department Stores

Other Retail Channels - By Price Tier (In Value %)

Economy / Entry-Level

Mid-Tier

Premium / High-End

- Market Share of Major Players by Value/Volume

- Market Share of Major Players by Product Type

- Market Share of Major Players by Distribution Channel

- Cross Comparison Parameters (Company Overview, Business Strategies, Recent Developments, Strengths, Weaknesses, Organizational Structure, Revenues, Revenues by Product Type, Number of Retail Outlets, Distribution Channels, Number of Dealers and Distributors, Margins, Production Capabilities, Unique Value Offering)

- SWOT Analysis of Major Players

- Pricing Analysis Based on Product Categories for Major Players

- Detailed Profiles of Major Companies

Mattel, Inc.

Hasbro, Inc.

LEGO Group

Spin Master Corp.

Funko, Inc.

Bandai Namco Holdings Inc.

Ravensburger AG

VTech Holdings Ltd.

Playmobil

Jakks Pacific, Inc.

Tomy Company, Ltd.

Fisher-Price, Inc.

Mega Brands

K’NEX Brands

Cayro Toys

- Market Demand and Utilization

- Purchasing Power and Budget Allocations

- Regulatory and Compliance Requirements

- Needs, Desires, and Pain Point Analysis

- Decision-Making Process

- By Value, 2026-2035

- By Volume, 2026-2035

- By Average Price, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now