Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Brazil warehousing market reached approximately USD ~ billion based on a recent historical assessment, according to industry datasets from CBRE and JLL logistics real estate research. The market is driven by strong demand from retail distribution, manufacturing logistics, agricultural exports, and third party logistics providers requiring modern storage and fulfillment infrastructure. Rapid digital commerce growth and expansion of nationwide distribution networks are increasing warehouse leasing demand while large logistics parks and automated fulfillment centers expand capacity across major logistics corridors.

São Paulo remains the dominant logistics hub due to extensive highway connectivity, proximity to industrial clusters, and the presence of Brazil’s largest consumer market. Campinas, Rio de Janeiro, Curitiba, and Belo Horizonte also host significant warehouse clusters supported by port connectivity, manufacturing activity, and regional distribution networks. Major seaports including Santos further strengthen logistics demand as agricultural exports, industrial goods, and consumer imports require large scale storage facilities near transportation corridors.

Market Segmentation

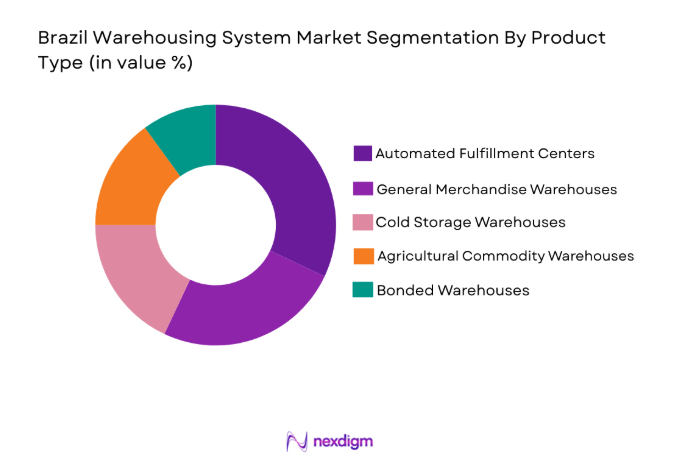

By Product Type

Brazil Warehousing Market is segmented by product type into general merchandise warehouses, cold storage warehouses, automated fulfillment centers, bonded warehouses, and agricultural commodity storage facilities. Recently, automated fulfillment centers has a dominant market share due to the rapid expansion of e commerce distribution and omnichannel retail logistics networks across Brazil. Retail companies and logistics providers increasingly deploy robotics enabled warehouses and automated storage retrieval systems that accelerate inventory handling and order processing efficiency. Large fulfillment hubs positioned near metropolitan regions allow faster distribution across dense consumer markets. As digital retail transactions continue increasing, demand for technologically advanced fulfillment warehouses strengthens their leading position in the national warehousing ecosystem.

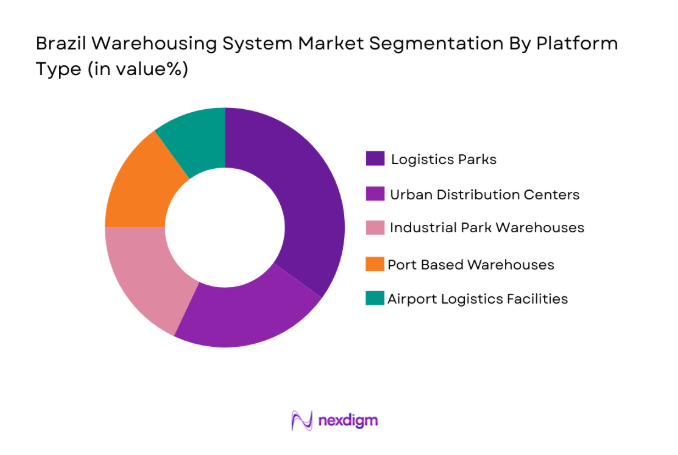

By Platform Type

Brazil Warehousing Market is segmented by platform type into logistics parks, urban distribution centers, port based warehouses, airport logistics facilities, and industrial park warehouses. Recently, logistics parks has a dominant market share due to the growing preference for integrated logistics infrastructure combining storage, transportation access, and value added services. Large logistics parks developed near major highway corridors provide scalable warehousing capacity for manufacturers, retailers, and logistics providers. These complexes support multimodal connectivity while offering modern infrastructure capable of accommodating automated warehouses and large distribution centers. Their ability to consolidate logistics operations within centralized hubs significantly improves supply chain efficiency, supporting their dominant position in Brazil’s warehousing industry.

Competitive Landscape

Brazil warehousing market shows moderate consolidation where global logistics real estate developers and large third party logistics providers control a significant portion of modern grade A warehouse capacity. Companies continue investing in logistics parks, automated distribution centers, and temperature controlled facilities to meet growing demand from e commerce, retail, and manufacturing sectors. Strategic partnerships between industrial real estate developers and logistics operators are expanding large scale logistics parks across Brazil’s primary transportation corridors.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Warehouse Capacity |

| Prologis | 1983 | United States | ~ | ~ | ~ | ~ | ~ |

| GLP | 2009 | Singapore | ~ | ~ | ~ | ~ | ~ |

| LOG Commercial Properties | 2008 | Brazil | ~ | ~ | ~ | ~ | ~ |

| Bresco Investimentos | 2012 | Brazil | ~ | ~ | ~ | ~ | ~ |

| Goodman Group | 1989 | Australia | ~ | ~ | ~ | ~ | ~ |

Brazil Warehousing Market Analysis

Growth Drivers

Expansion of E Commerce Fulfillment Infrastructure Across Brazil

Rapid growth of digital commerce platforms across Brazilian urban populations is increasing demand for modern warehousing networks capable of supporting high volume order processing and nationwide parcel distribution. Online retail marketplaces selling electronics, clothing, groceries, and consumer goods require sophisticated fulfillment centers that integrate automated storage, robotics based sorting systems, and advanced warehouse management software. Retail companies increasingly depend on logistics providers capable of managing high order volumes and fast delivery expectations. Large fulfillment hubs located near major cities reduce delivery times and improve logistics efficiency. Continuous growth of mobile commerce participation among consumers further increases online retail transaction volumes. Logistics companies therefore invest heavily in technologically advanced warehouses equipped with automation systems and predictive inventory management platforms. Expansion of omnichannel retail distribution models also strengthens demand for warehousing infrastructure supporting store replenishment and direct consumer deliveries. As digital retail adoption expands nationwide, large scale fulfillment centers become essential components of Brazil’s logistics ecosystem.

Growth of Export Oriented Agricultural and Industrial Supply Chains

Brazil’s strong position in global agricultural exports and industrial manufacturing significantly increases demand for large scale warehousing facilities supporting complex logistics networks. Agricultural commodities including soybeans, coffee, corn, and sugar require specialized storage infrastructure before shipment through major seaports. Industrial sectors such as automotive manufacturing, machinery production, and consumer goods assembly also require distribution warehouses supporting domestic and international supply chains. Export oriented logistics corridors connecting production regions with seaports strengthen demand for strategically located storage facilities. Warehousing providers therefore develop large logistics parks positioned near transportation corridors supporting agricultural and industrial logistics flows. Modern warehouses integrate advanced inventory systems capable of managing bulk commodity storage and high value manufactured goods simultaneously. Continuous expansion of Brazil’s export trade volumes increases storage requirements throughout logistics networks. As agricultural production and manufacturing exports continue expanding, warehousing infrastructure becomes critical to efficient supply chain management across the national economy.

Market Challenges

Infrastructure Bottlenecks Across National Transportation Networks

Brazil’s warehousing industry faces operational challenges due to transportation infrastructure constraints affecting efficient logistics distribution across the country’s vast geographic territory. Many industrial regions depend heavily on road transportation systems where congestion, poor road conditions, and long travel distances increase transportation costs. These challenges affect supply chain efficiency by slowing cargo movement between production centers, warehouses, and consumer markets. Logistics providers must therefore invest in strategically located warehouses positioned near major transportation corridors to reduce distribution inefficiencies. Limited rail and inland waterway logistics infrastructure further restrict multimodal transportation options for large cargo volumes. Infrastructure bottlenecks also increase logistics costs for companies managing national distribution networks. Government investments in highway modernization and logistics corridor development are gradually improving connectivity but infrastructure gaps remain significant. These operational limitations increase logistics complexity and present ongoing challenges for warehousing operators supporting national supply chains.

High Industrial Real Estate Development Costs and Regulatory Complexity

Development of modern grade A warehousing infrastructure requires substantial capital investment due to rising industrial land prices and construction costs across major logistics regions. Industrial real estate developers must secure large land parcels located near transportation corridors, metropolitan markets, or seaport logistics hubs. Regulatory procedures related to zoning approvals, environmental licensing, and infrastructure permits often extend project timelines and increase development costs. Logistics park developers must also invest heavily in modern infrastructure including automated warehouse systems, transportation access roads, and energy supply networks. These capital intensive requirements increase barriers for smaller developers entering the logistics real estate sector. Additionally, fluctuations in construction material prices and labor costs further increase development expenses. Companies must carefully manage long term investment strategies to maintain financial viability of warehouse construction projects. As demand for modern warehousing grows, balancing infrastructure investment with regulatory compliance remains a critical challenge for developers and logistics operators.

Opportunities

Development of Automated Smart Warehousing Infrastructure

Rapid technological innovation across global logistics industries presents major opportunities for warehousing operators to develop automated smart storage facilities capable of significantly improving operational efficiency. Robotics based sorting systems, automated storage retrieval systems, and artificial intelligence driven inventory management platforms allow warehouses to process thousands of orders per hour with high accuracy. Brazilian logistics companies increasingly invest in advanced digital technologies that improve warehouse productivity while reducing operational costs. Automated fulfillment centers also support rapid order processing for e commerce distribution networks requiring same day or next day delivery services. Technology driven warehouses enable logistics providers to manage growing shipment volumes generated by digital retail platforms. Integration of predictive analytics and real time inventory tracking further enhances operational efficiency within complex supply chains. As technology adoption increases across logistics industries, automated smart warehouses represent a major growth opportunity for Brazil’s warehousing sector.

Expansion of Cold Chain Logistics for Food and Pharmaceutical Supply Chains

Increasing consumption of frozen food products and expanding pharmaceutical distribution networks create strong opportunities for specialized cold storage warehouses across Brazil. Temperature controlled logistics infrastructure is essential for preserving food quality and maintaining pharmaceutical product stability during storage and transportation. Supermarket chains, food manufacturers, and pharmaceutical companies require reliable refrigerated storage facilities capable of maintaining strict temperature conditions throughout logistics operations. Brazil’s large agricultural sector also produces perishable products including meat, dairy, fruits, and seafood requiring refrigerated logistics systems before export. Pharmaceutical supply chains distributing vaccines, biologic medicines, and specialty drugs further strengthen demand for certified cold storage warehouses. Logistics companies therefore invest heavily in refrigerated warehouses equipped with advanced temperature monitoring technologies and energy efficient cooling systems. As healthcare demand and modern food distribution networks expand, cold chain warehousing represents a major investment opportunity within Brazil’s logistics infrastructure sector.

Future Outlook

Brazil warehousing market is expected to experience steady expansion as logistics infrastructure development continues across major transportation corridors and industrial regions. Growth of digital commerce and modernization of retail distribution networks will significantly increase demand for automated fulfillment centers and urban logistics hubs. Government investments in transportation infrastructure and logistics corridors will improve supply chain efficiency across national distribution networks. Expansion of agricultural exports, industrial manufacturing, and cold chain logistics systems will further strengthen long term demand for modern warehousing facilities.

Major Players

- Prologis

- GLP

- LOG Commercial Properties

- Bresco Investimentos

- Hines

- Goodman Group

- DHL Supply Chain

- CEVA Logistics

- Kuehne+Nagel

- DB Schenker

- JSL Logistica

- Tegma Gestao Logistica

- VLI Logistica

- Sanca Galpoes

- Fulwood Logistica

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Logistics infrastructure developers

- E-commerce retail companies

- Third party logistics providers

- Industrial real estate investors

Research Methodology

Step 1: Identification of Key Variables

Key market variables including warehouse capacity expansion, logistics infrastructure investment, e commerce shipment volumes, and industrial real estate development were identified to determine primary demand drivers influencing Brazil’s warehousing market.

Step 2: Market Analysis and Construction

Industry databases, logistics real estate reports, trade publications, and company financial statements were analyzed to construct the market structure, identify major participants, and evaluate distribution infrastructure trends.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultation with logistics professionals, warehouse developers, and supply chain analysts to confirm demand patterns, infrastructure investment trends, and competitive market positioning.

Step 4: Research Synthesis and Final Output

Collected datasets and validated insights were integrated into a structured analytical framework to produce a comprehensive evaluation of Brazil’s warehousing industry including segmentation, competition, and future outlook.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

- Expansion of E Commerce Fulfillment and Omnichannel Retail Distribution Networks

Growth of Export Oriented Agricultural and Industrial Supply Chains

Infrastructure Development in Logistics Parks and Industrial Corridors - Market Challenges

- High Land Acquisition and Industrial Real Estate Development Costs

Transportation Bottlenecks and Regional Infrastructure Constraints

Complex Regulatory Procedures for Industrial Construction and Zoning - Market Opportunities

- Development of Automated Smart Warehousing Facilities

Expansion of Cold Chain Warehousing for Food and Pharmaceutical Logistics

Growth of Integrated Logistics Parks Near Major Urban Centers - Trends

- Adoption of Robotics and Automated Storage Retrieval Systems

Expansion of Urban Micro Fulfillment Centers Supporting Rapid Delivery - Government Regulations

- National Logistics Plan and Infrastructure Investment Programs

Industrial Zoning and Environmental Compliance Regulations

Tax Incentives for Logistics Park Development - SWOT Analysis

Strengths Related to Expanding Consumer Market and Industrial Base

Weaknesses Associated with Infrastructure Inefficiencies

Opportunities Created by Digital Commerce Expansion

Threats from Economic Volatility and Regulatory Complexity - Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

- Automated Fulfillment Warehouses

Cold Storage Warehouses

General Merchandise Distribution Warehouses

E Commerce Fulfillment Centers

Bonded Warehouses - By Platform Type (In Value%)

- Urban Distribution Centers

Regional Logistics Parks

Port Based Warehousing Facilities

Industrial Park Warehousing Complexes

Airport Logistics Warehouses - By Fitment Type (In Value%)

- Built to Suit Warehouses

Speculative Grade A Warehouses

Retrofit Industrial Warehouses

Modular Warehousing Facilities - By End User Segment (In Value%)

- E Commerce and Retail Companies

Manufacturing and Industrial Firms

Third Party Logistics Providers

- Market Share Analysis

- Cross Comparison Parameters (Warehouse Capacity, Automation Level, Geographic Coverage, Cold Storage Capability, Client Industry Focus, Logistics Integration Services, Industrial Real Estate Portfolio)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

- Prologis Brazil

GLP Brazil

LOG Commercial Properties

Bresco Investimentos

Hines Brasil

Goodman Group Brazil

DHL Supply Chain Brazil

CEVA Logistics Brazil

Kuehne+Nagel Brazil

DB Schenker Brazil

JSL Logistica

Tegma Gestao Logistica

VLI Logistica

Sanca Galpoes

Fulwood Logistica

- Retail and E Commerce Companies Increasing Demand for Large Fulfillment Centers

- Manufacturing Firms Requiring Integrated Storage and Distribution Infrastructure

- Third Party Logistics Providers Expanding National Distribution Networks

- Food and Pharmaceutical Supply Chains Increasing Demand for Specialized Warehousing

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now