Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the Canada 3PL market generated approximately USD ~ billion in logistics service revenue according to data published by Transport Canada and the Canadian International Freight Forwarders Association. The market is driven by rising outsourcing of transportation, warehousing, and supply chain management services by retail, manufacturing, and healthcare companies. Expansion of e commerce fulfillment networks, growth in cross border trade logistics with the United States, and increasing deployment of automated warehouse infrastructure continue to strengthen demand for third party logistics services across Canada’s national supply chain ecosystem.

Major logistics activity within the Canada 3PL market is concentrated around Toronto, Vancouver, Montreal, Calgary, and Edmonton due to the presence of international ports, rail freight terminals, and large scale distribution centers. Toronto functions as the primary national logistics hub because of strong retail fulfillment infrastructure and proximity to United States trade corridors. Vancouver benefits from Pacific maritime trade connectivity with Asia Pacific supply chains, while Montreal and Calgary support rail freight networks and industrial distribution operations enabling efficient cargo movement across Canada’s extensive transportation system.

Market Segmentation

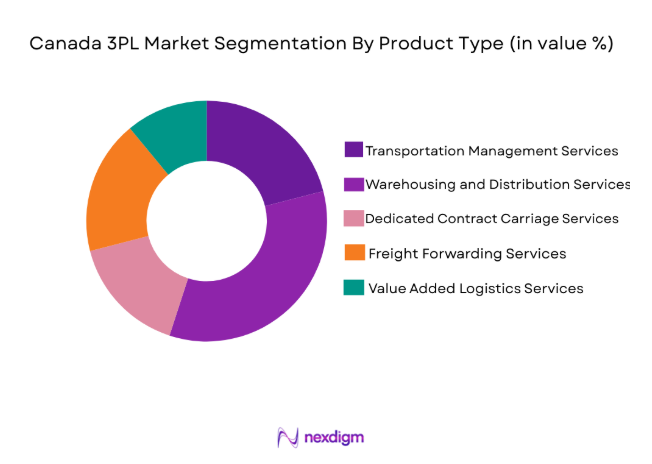

By Product Type

Canada 3PL market is segmented by product type into transportation management services, warehousing and distribution services, dedicated contract carriage services, freight forwarding services, and value added logistics services. Recently, warehousing and distribution services has a dominant market share due to factors such as rapid expansion of e commerce fulfillment networks, demand for inventory storage infrastructure, and increasing outsourcing of distribution management by retailers and manufacturers. Large logistics providers operate automated distribution centers near major urban regions to enable faster order processing and regional delivery. Growth in omnichannel retail strategies also requires integrated warehousing networks capable of managing inventory, order picking, packaging, and reverse logistics operations, further strengthening the importance of distribution focused 3PL solutions across Canada.

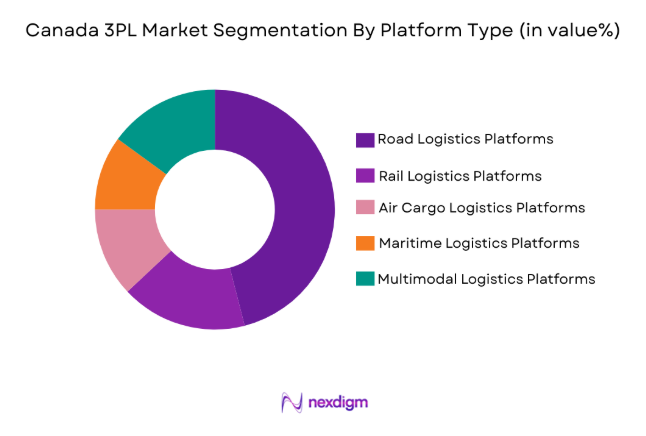

By Platform Type

Canada 3PL market is segmented by platform type into road logistics platforms, rail logistics platforms, air cargo logistics platforms, maritime logistics platforms, and multimodal logistics platforms. Recently, road logistics platforms has a dominant market share due to factors such as extensive highway infrastructure, high domestic freight volumes, and strong demand for truck based cargo transportation connecting warehouses with retail distribution centers. Road transport provides flexible last mile and regional delivery capabilities across large geographic areas where rail and maritime connectivity may be limited. Logistics providers therefore maintain large trucking fleets and partner carrier networks that allow rapid cargo movement between manufacturing zones, ports, airports, and consumer markets across Canada.

Competitive Landscape

The Canada 3PL market demonstrates moderate consolidation where global logistics corporations compete alongside established regional service providers specializing in warehousing, freight forwarding, and integrated supply chain solutions. Large multinational firms benefit from advanced logistics technology, extensive international networks, and large scale warehouse infrastructure that enables efficient cargo management across domestic and cross border trade routes. Competitive differentiation is primarily influenced by service integration capabilities, transportation network coverage, digital logistics platforms, and contract logistics expertise supporting retail, manufacturing, and healthcare supply chains.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Logistics Infrastructure Capacity |

| DHL Supply Chain | 1969 | Bonn, Germany | ~ | ~ | ~ | ~ | |

| Kuehne + Nagel | 1890 | Schindellegi, Switzerland | ~ | ~ | ~ | ~ | ~ |

| DB Schenker | 1872 | Essen, Germany | ~ | ~ | ~ | ~ | ~ |

| Ryder System | 1933 | Florida, United States | ~ | ~ | ~ | ~ | ~ |

| GEODIS | 1904 | Levallois Perret, France | ~ | ~ | ~ | ~ | ~ |

Canada 3PL Market Analysis

Growth Drivers

Expansion of E Commerce Fulfillment and Omnichannel Retail Logistics Networks

Rapid expansion of digital commerce and omnichannel retail distribution significantly strengthens demand for third party logistics services across Canada’s supply chain ecosystem. Online retail platforms require large scale logistics networks capable of managing inventory storage, order processing, and last mile distribution across multiple provinces. Retail companies increasingly outsource these operational requirements to specialized logistics providers capable of operating automated warehouses and transportation fleets that efficiently manage high order volumes. Third party logistics companies therefore invest heavily in robotics enabled distribution centers, digital inventory management platforms, and advanced transportation planning software designed to accelerate fulfillment efficiency. Logistics providers also support reverse logistics operations required for product returns generated by online retail transactions, which further expands service demand. Growing cross border e commerce shipments between Canada and the United States require integrated freight forwarding, customs clearance, and transportation coordination services that can be delivered by experienced 3PL operators. As digital retail continues expanding nationwide, logistics outsourcing allows retailers to scale distribution operations without heavy capital investment in warehouses and transportation infrastructure. This structural shift toward outsourced logistics services continues to strengthen revenue growth opportunities for 3PL providers across the national supply chain ecosystem.

Integration of Advanced Supply Chain Technology and Warehouse Automation Systems

Rapid adoption of digital supply chain technologies significantly strengthens operational capabilities across the Canada 3PL market by improving logistics efficiency, visibility, and service reliability. Logistics providers deploy warehouse management systems, transportation management platforms, and predictive analytics tools that enable real time cargo tracking and route optimization across complex distribution networks. Automated picking robots, conveyor sorting systems, and digital inventory platforms improve warehouse productivity while reducing operational errors and labor dependency. Technology integration also enables logistics companies to process large shipment volumes more efficiently while maintaining accurate inventory records and delivery schedules. Data analytics systems help logistics providers forecast shipment demand and allocate transportation capacity accordingly across regional distribution networks. Advanced digital platforms also enable seamless data exchange between manufacturers, retailers, and logistics providers, allowing supply chains to operate more efficiently with improved coordination. As companies increasingly prioritize supply chain visibility and operational resilience, demand for technologically advanced third party logistics services continues expanding across Canada’s logistics industry.

Market Challenges

High Transportation Costs Across Canada’s Large Geographic Distances

Canada’s vast geographic landscape presents significant logistical challenges for third party logistics providers responsible for transporting goods across long distances between production zones, distribution centers, and consumer markets. Large transportation distances increase fuel consumption, labor expenses, and vehicle maintenance costs for trucking fleets operating nationwide cargo distribution networks. Logistics companies must also coordinate shipments across remote and sparsely populated regions where freight volumes may be lower but delivery requirements remain essential for maintaining national supply chain connectivity. Seasonal weather conditions including severe winter storms can disrupt transportation schedules and reduce fleet productivity across northern and rural regions. These factors increase operational complexity for logistics providers attempting to maintain consistent service levels across the country’s diverse transportation corridors. Infrastructure limitations in certain regions may further slow cargo movement and increase transit times for long distance shipments. As logistics providers attempt to maintain competitive pricing while managing rising transportation expenses, cost management remains a significant operational challenge across Canada’s third party logistics sector.

Labor Shortages in Warehousing and Logistics Operations

The Canada 3PL market faces persistent labor availability challenges that affect warehouse operations, cargo handling efficiency, and transportation fleet management across the logistics industry. Distribution centers require a large workforce capable of managing inventory processing, packaging operations, loading activities, and transportation coordination across complex supply chains. However, labor shortages within logistics occupations create operational bottlenecks that slow warehouse throughput and increase order fulfillment times. Logistics companies increasingly compete with other industries for skilled workers capable of operating automated warehouse systems, logistics software platforms, and heavy transportation equipment. Workforce shortages may also increase labor costs as companies attempt to attract and retain employees through higher wages and training investments. To address these challenges, logistics providers increasingly adopt warehouse automation technologies and robotics systems that reduce dependence on manual labor while improving operational efficiency. Despite these technological improvements, workforce availability remains an important factor influencing productivity across Canada’s rapidly expanding logistics infrastructure.

Opportunities

Expansion of Cross Border Trade Logistics Between Canada and the United States

Strong trade integration between Canada and the United States creates substantial growth opportunities for third party logistics providers managing cross border cargo flows between the two economies. Manufacturing supply chains frequently require transportation of intermediate goods, raw materials, and finished products across the international border, generating consistent demand for specialized logistics services. Third party logistics companies capable of managing customs documentation, regulatory compliance, and cross border transportation coordination are therefore positioned to capture significant service demand. Integrated logistics solutions that combine freight forwarding, warehousing, and customs brokerage services provide valuable operational support for manufacturers and retailers engaged in international trade. Logistics providers continue investing in cross border transportation infrastructure and digital documentation systems that streamline cargo clearance procedures and reduce shipping delays. Growing trade flows across North American manufacturing supply chains further increase demand for logistics companies capable of providing reliable and efficient cross border cargo movement services. These developments create long term growth opportunities for advanced 3PL providers operating across Canada’s international logistics networks.

Growth of Temperature Controlled Logistics for Healthcare and Food Supply Chains

Increasing demand for temperature controlled logistics services presents significant expansion opportunities within the Canada 3PL market as healthcare and food supply chains require specialized transportation and storage infrastructure. Pharmaceutical manufacturers and biotechnology companies require highly controlled distribution systems that maintain strict temperature conditions during product storage and transportation. Logistics providers therefore invest in refrigerated warehouses, insulated packaging technologies, and specialized transportation fleets capable of maintaining precise environmental conditions. Growth in grocery retail distribution and frozen food consumption further increases demand for cold chain logistics infrastructure supporting nationwide food supply networks. Third party logistics companies capable of offering integrated cold chain services including storage, transportation, and monitoring systems gain competitive advantages within specialized logistics segments. Technological innovations such as real time temperature monitoring sensors and automated cold storage facilities improve operational efficiency while maintaining strict regulatory compliance standards. These developments significantly expand market opportunities for logistics providers specializing in temperature-controlled supply chain solutions.

Future Outlook

The Canada 3PL market is expected to experience sustained expansion driven by rising supply chain outsourcing, increasing cross border trade activity, and continuous growth in e commerce logistics demand. Technological innovation in warehouse automation, digital freight platforms, and real time supply chain visibility systems will further strengthen operational efficiency across logistics networks. Government investment in transportation infrastructure and trade facilitation initiatives will support improved cargo movement across major logistics corridors. Growing demand for specialized logistics solutions including cold chain services and integrated supply chain management will continue shaping the evolution of the market.

Major Players

- DHL Supply Chain Canada

- Kuehne + Nagel Canada

- DB Schenker Canada

- GEODIS Canada

- Ryder System

- UPS Supply Chain Solutions

- FedEx Logistics

- CEVA Logistics Canada

- DSV Global Transport and Logistics

- C.H. Robinson

- Maersk Logistics

- VersaCold Logistics Services

- Lineage Logistics

- CJ Logistics America

- XPO Logistics

Key Target Audience

- Retail and e-commerce companies

- Manufacturing and industrial companies

- Pharmaceutical and biotechnology companies

- Food and beverage manufacturers

- Logistics and supply chain service providers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key operational variables influencing the Canada 3PL market were identified including logistics outsourcing trends, transportation infrastructure development, trade flows, and digital supply chain technology adoption across major industry sectors.

Step 2: Market Analysis and Construction

Industry datasets from trade authorities, logistics associations, and corporate disclosures were analyzed to construct the market structure and evaluate revenue generation across transportation, warehousing, and integrated logistics services.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings were validated through consultation with logistics professionals, supply chain managers, and transportation analysts who provided operational insights regarding market demand and technology adoption.

Step 4: Research Synthesis and Final Output

All validated data and expert insights were consolidated into a structured analytical framework to produce comprehensive market insights and industry projections supporting strategic decision making.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of E Commerce and Omni Channel Retail Logistics Networks

Growing Cross Border Trade Between Canada and the United States

Rising Demand for Integrated Supply Chain and Distribution Solutions - Market Challenges

High Transportation Costs Across Large Geographic Distances

Labor Shortages in Logistics and Warehouse Operations

Supply Chain Disruptions and Infrastructure Bottlenecks - Market Opportunities

Investment in Automated Warehousing and Robotics Technologies

Growth of Cold Chain and Healthcare Logistics Services

Expansion of Cross Border E Commerce Fulfillment Networks - Trends

Adoption of Digital Freight Platforms and Real Time Shipment Visibility

Expansion of Sustainable Logistics and Green Transportation Initiatives - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- \By System Type (In Value%)

Transportation Management Services

Dedicated Contract Carriage Services

International Freight Management Services

Integrated Supply Chain Solutions

Value Added Logistics Services - By Platform Type (In Value%)

Road Freight Logistics Platforms

Rail Freight Logistics Platforms

Air Cargo Logistics Platforms

Maritime Freight Logistics Platforms

Multimodal Logistics Platforms - By Fitment Type (In Value%)

Inhouse Logistics Outsourcing

Fully Outsourced Logistics Contracts

Hybrid Logistics Partnerships

On Demand Logistics Solutions - By End User Segment (In Value%)

Retail and E Commerce Companies

Manufacturing and Industrial Companies

Healthcare and Pharmaceutical Companies

- Market Share Analysis

- Cross Comparison Parameters (Service Portfolio, Transportation Network Coverage, Warehousing Capacity, Technology Integration, Pricing Strategy, Cross Border Logistics Capability, Value Added Services)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

DHL Supply Chain Canada

Kuehne + Nagel Canada

DB Schenker Canada

CEVA Logistics Canada

XPO Logistics

FedEx Logistics

UPS Supply Chain Solutions

Ryder System

Lineage Logistics

CJ Logistics America

Maersk Logistics

DSV Global Transport and Logistics

C.H. Robinson

GEODIS Canada

VersaCold Logistics Services

- Retail and E Commerce Companies Increasing Outsourcing of Fulfillment and Distribution

- Manufacturers Seeking Integrated Transportation and Warehousing Solutions

- Healthcare and Pharmaceutical Firms Expanding Temperature Controlled Logistics

- Automotive and Industrial Producers Requiring Just In Time Supply Chain Services

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now