Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The market is expected to experience substantial growth, driven by increasing demand across various sectors such as manufacturing, construction, and automotive industries. Based on recent assessments, the market size is poised to reach USD ~ billion by the end of the year, supported by technological advancements and strategic investments from both private and public sectors. As global demand for advanced materials grows, regions with robust industrial bases are seeing accelerated growth. The market is heavily influenced by developments in material science, with high-performance polymers, nanomaterials, and smart materials leading the charge.

The North American market is the dominant region, primarily due to the robust industrial sector in the United States and Canada, along with a strong emphasis on innovation and sustainability. These countries are home to leading companies driving research and development in advanced materials. Additionally, Europe remains a key player, with Germany and France investing heavily in high-performance materials for automotive and aerospace applications. These regions’ dominance is attributed to their focus on high-tech infrastructure, regulatory frameworks that support innovation, and a favorable environment for advanced material adoption.

Market Segmentation

By Product Type:

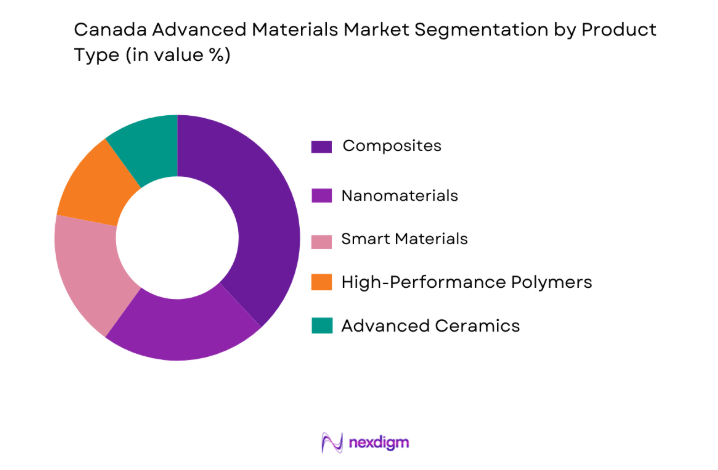

The advanced materials market is segmented by product type into composites, nanomaterials, smart materials, high-performance polymers, and advanced ceramics. The composite materials sub-segment holds the dominant market share due to the growing demand for lightweight, high-strength materials in the automotive and aerospace sectors. This segment benefits from advancements in manufacturing processes, such as 3D printing and automation, which have made composites more accessible and cost-effective. Furthermore, their ability to reduce weight without compromising on durability has led to increased adoption in various applications, ranging from automotive parts to wind turbine blades. As sustainability and efficiency continue to drive market trends, composites are expected to maintain their dominant position.

By End-Use Industry:

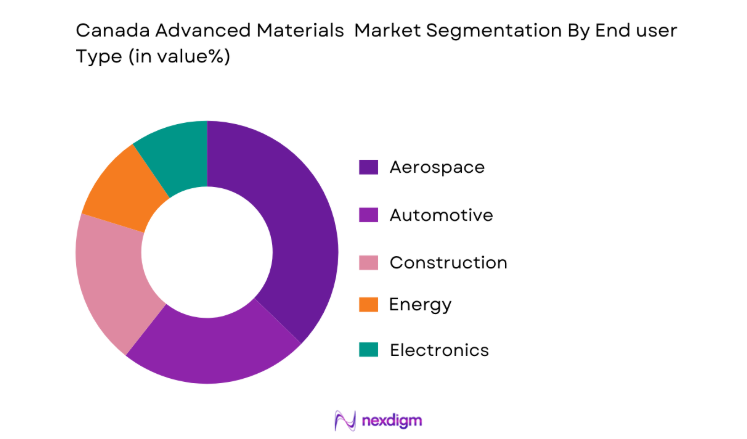

The market is also segmented by end-use industry, which includes sectors such as automotive, aerospace, construction, energy, and electronics. The aerospace industry has shown significant dominance in terms of market share, driven by the growing demand for lightweight materials that can withstand extreme conditions. Advanced materials like composites and high-performance alloys are increasingly used in aircraft manufacturing, contributing to fuel efficiency and overall performance. The automotive industry follows closely, with a surge in demand for sustainable, energy-efficient materials for electric vehicles (EVs). The aerospace sector’s growth is driven by advancements in material technology, regulatory push for environmental sustainability, and a strong focus on reducing manufacturing costs.

Competitive Landscape

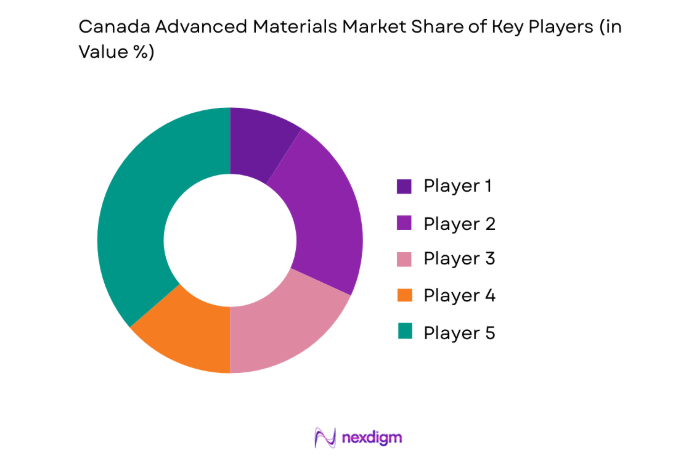

The competitive landscape of the market is characterized by both established players and emerging companies. Key players are increasingly collaborating with research institutions and adopting new manufacturing technologies to stay ahead. Major players are focusing on acquisitions and strategic partnerships to expand their market presence and technological capabilities. As competition intensifies, companies are leveraging innovation to offer more sustainable and cost-effective materials, while also expanding into new geographic markets.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Additional Parameter |

| 3M | 1902 | USA | ~ | ~ | ~ | ~ | ~ |

| BASF | 1865 | Germany | ~ | ~ | ~ | ~ | ~ |

| Toray Industries | 1926 | Japan | ~ | ~ | ~ | ~ | ~ |

| Covestro | 2005 | Germany | ~ | ~ | ~ | ~ | ~ |

| DSM | 1902 | Netherlands | ~ | ~ | ~ | ~ | ~ |

Canada Advanced Materials Market Analysis

Growth Drivers

Technological Advancements in Material Science:

Technological advancements in material science have become a significant driver for the market, particularly with the development of nanomaterials and smart materials. These materials enable industries to improve performance, enhance product durability, and reduce weight, all while achieving sustainability goals. Innovations in 3D printing and manufacturing automation have enabled companies to develop customized materials more efficiently, driving growth in sectors such as aerospace and automotive. The increasing demand for energy-efficient materials, driven by environmental concerns, has further fueled the adoption of advanced materials across various industries. This growth is also supported by ongoing investments in research and development, ensuring a constant stream of innovations that push the boundaries of material capabilities.

Sustainability and Environmental Regulations:

Sustainability has become a major driving force for the advanced materials market, with an increasing emphasis on reducing environmental impact across industries. Governments worldwide are implementing stricter regulations to curb emissions and encourage the use of eco-friendly materials. This has led to the adoption of advanced materials such as high-performance polymers, which offer enhanced durability and lower environmental impact compared to traditional materials. Additionally, industries are embracing materials that contribute to energy efficiency, such as lightweight composites in the automotive and aerospace sectors. The push for sustainability is not only driven by regulatory requirements but also by consumer demand for greener products, which continues to shape material selection and manufacturing processes across the globe.

Market Challenges

High Development Costs:

One of the primary challenges faced by the advanced materials market is the high cost of research, development, and production. The development of new materials often requires substantial investments in research and prototyping, which can be prohibitive for smaller companies. Additionally, advanced materials like composites and nanomaterials require specialized manufacturing processes, which can drive up costs and limit their accessibility for mass adoption. This challenge is particularly significant in industries such as automotive and construction, where cost-efficiency is a key consideration. Despite the long-term benefits of these materials, the initial capital required for their development and production remains a major obstacle to widespread adoption.

Regulatory and Compliance Barriers:

Advanced materials are subject to a range of regulations and certification requirements, which can vary significantly across regions. These regulatory hurdles can slow down the commercialization process and increase the time-to-market for new products. Companies in the advanced materials sector must navigate complex compliance processes, including environmental certifications and safety standards. These challenges are particularly evident in industries such as aerospace, where materials must meet stringent safety and performance standards. The evolving regulatory landscape, combined with the complexity of meeting global compliance requirements, creates a significant barrier for companies looking to expand their market reach.

Opportunities

Integration of Nanomaterials in Electronics:

Nanomaterials present a significant opportunity for growth in the electronics industry. As devices become smaller, more powerful, and energy-efficient, the need for materials that can enhance performance at a microscopic scale has increased. Nanomaterials, with their unique properties such as high strength and conductivity, are particularly well-suited for use in electronic devices, including semiconductors, batteries, and displays. Their integration can improve the performance and longevity of electronic components while reducing energy consumption, making them an attractive option for the electronics industry. As consumer demand for more powerful and efficient devices grows, the adoption of nanomaterials is expected to increase, offering significant market opportunities.

Expansion in Aerospace Applications:

The aerospace sector continues to be a major driver for the advanced materials market, with increasing demand for lightweight, durable materials that can withstand extreme conditions. The growing adoption of composites and high-performance alloys in the manufacture of aircraft components is a key trend in the industry. These materials help reduce the weight of aircraft, improving fuel efficiency and reducing emissions. Additionally, the rise of commercial space travel and satellite technologies has further boosted demand for advanced materials in aerospace applications. As the aerospace industry continues to innovate, the demand for advanced materials is expected to grow, creating new opportunities for market players in this sector.

Future Outlook

The market is poised for steady growth in the next five years, driven by technological advancements, increasing demand for energy-efficient solutions, and stringent environmental regulations. Companies are expected to continue investing in R&D to develop next-generation materials that offer better performance and sustainability. Regulatory support from governments will likely facilitate this growth, encouraging the adoption of advanced materials across industries such as aerospace, automotive, and electronics. Technological innovations such as 3D printing and automation are also expected to make production more cost-effective, further driving the market’s expansion.

Major Players

- 3M

- BASF

- Toray Industries

- Covestro

- DSM

- Dow

- DuPont

- Hexcel Corporation

- Solvay

- Owens Corning

- Mitsubishi Chemical

- SGL Carbon

- Huntsman Corporation

- AkzoNobel

- Arkema

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Aerospace manufacturers

- Automotive manufacturers

- Energy and utilities companies

- Electronics and semiconductor companies

- Chemical and material suppliers

- Research and development organizations

Research Methodology

Step 1: Identification of Key Variables

Key variables impacting market growth, such as technological advancements, consumer trends, and regulatory developments, are identified and analyzed to form a comprehensive market model.

Step 2: Market Analysis and Construction

A thorough analysis of historical data and current trends is performed to construct a reliable market model that predicts future growth and identifies key drivers.

Step 3: Hypothesis Validation and Expert Consultation

Expert consultations and market hypothesis testing are conducted to validate assumptions and refine the model, ensuring accuracy and reliability in the results.

Step 4: Research Synthesis and Final Output

Data and insights gathered are synthesized into the final report, which includes actionable market insights, forecasts, and strategic recommendations for stakeholders.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Technological Innovations in Material Science

Increased Demand for Sustainable Solutions

Rising Investments in Aerospace and Automotive Sectors - Market Challenges

High Initial Development Costs

Complex Regulatory Standards

Supply Chain Disruptions - Market Opportunities

Integration of Nanomaterials in Electronics

Expansion of Aerospace Applications

Growth in Renewable Energy Systems - Trends

Rising Use of Smart Materials

Increasing Focus on Sustainability

Advances in Nanotechnology for Industrial Applications - Government Regulations

- SWOT Analysis of Key Competitors

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Composite Materials

Nanomaterials

Smart Materials

High-Performance Polymers

Advanced Ceramics - By Platform Type (In Value%)

Automotive Platforms

Aerospace Platforms

Electronics Platforms

Construction Platforms

Energy Platforms - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Hybrid Solutions

Modular Solutions

Integrated Solutions - By EndUser Segment (In Value%)

Manufacturing Industry

Energy Sector

Electronics and Semiconductor Industry

Construction Sector

- Market Share Analysis

- CrossComparison Parameters (System Type, Platform Type, Procurement Channel, EndUser Segment, Fitment Type)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

3M

BASF

DuPont

Hexcel Corporation

Covestro AG

Toray Industries

SABIC

DSM

Momentive Performance Materials

Saint-Gobain

Alcoa

ArcelorMittal

Huntsman Corporation

Owosso Motor Company

Celanese Corporation

- Growing Demand for High-Performance Materials in Manufacturing

- Shifting Trends in Aerospace Materials

- Electronics Industry Pushing for Advanced Materials

- Construction Sector Focusing on Sustainable Materials

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now