Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Canada Agricultural Equipment Large-Scale market is valued at approximately USD ~ billion based on a recent historical assessment, driven by sustained demand for high-horsepower tractors, combine harvesters, and large-scale seeding systems across extensive grain-producing regions. Investment momentum is supported by mechanization needs in prairie agriculture, rising farm consolidation, and equipment replacement cycles. Government-backed precision agriculture initiatives and expanding oilseed and cereal exports further sustain equipment procurement among commercial-scale farms and agribusiness enterprises.

Dominance in the Canada Agricultural Equipment Large-Scale market is concentrated in the prairie provinces, particularly Saskatchewan, Alberta, and Manitoba, where expansive arable land and large farm sizes necessitate high-capacity machinery deployment. These regions host major grain and oilseed production clusters and advanced farming cooperatives, encouraging adoption of precision-enabled large equipment. Strong dealer networks, service infrastructure, and proximity to manufacturing hubs in the Midwest North America region reinforce regional leadership in equipment utilization and fleet modernization.

Market Segmentation

By Product Type:

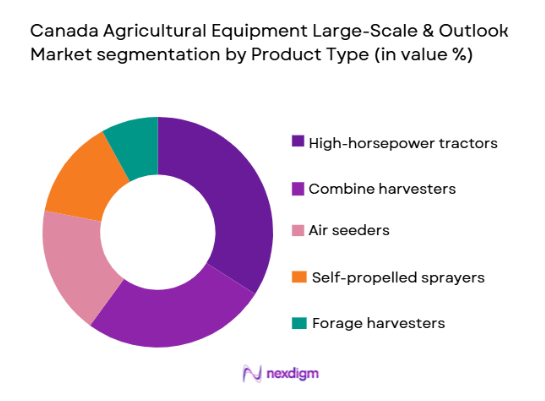

Canada Agricultural Equipment Large-Scale market is segmented by product type into high-horsepower tractors, combine harvesters, air seeders, self-propelled sprayers, and forage harvesters. Recently, high-horsepower tractors has a dominant market share due to factors such as large-acreage farm operations requiring high drawbar power, compatibility with wide-span implements, and increased adoption of precision agriculture systems. Prairie grain producers prioritize tractors exceeding 400 HP to improve field efficiency and reduce operational time across vast land parcels. These machines enable multi-implement operations including seeding, tillage, and hauling, supporting year-round utilization. OEM financing programs and robust resale values further strengthen adoption among commercial farms. Growing farm consolidation also increases demand for fleet standardization around high-capacity tractors, making them the backbone of large-scale mechanized agriculture across Canada.

By Technology Integration:

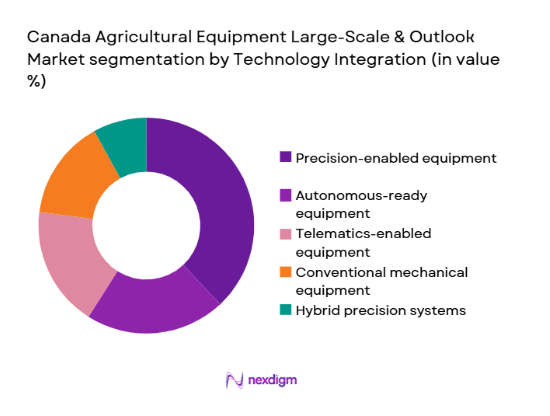

Canada Agricultural Equipment Large-Scale market is segmented by technology integration into precision-enabled equipment, autonomous-ready equipment, telematics-enabled equipment, conventional mechanical equipment, and hybrid precision systems. Recently, precision-enabled equipment has a dominant market share due to factors such as yield optimization requirements, labor efficiency goals, and government-backed digital agriculture programs. Canadian commercial farms increasingly deploy GPS-guided steering, variable rate seeding, and real-time field mapping to maximize productivity across extensive farmland. Precision integration improves fuel efficiency and reduces input costs, supporting profitability under volatile commodity prices. OEMs bundle precision systems with large equipment platforms, accelerating penetration. Dealer training and agronomic advisory services also encourage adoption, positioning precision-enabled machinery as the standard configuration for large-scale operations.

Competitive Landscape

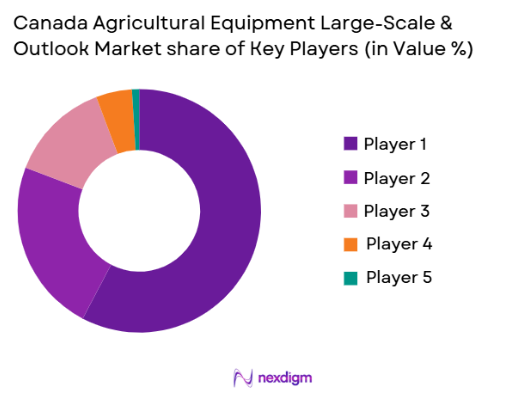

The Canada Agricultural Equipment Large-Scale market exhibits moderate consolidation with global manufacturers and regional specialists dominating equipment supply and dealer distribution networks. Major players leverage advanced precision technology portfolios, extensive service infrastructure, and financing solutions to maintain market leadership. Competitive intensity is shaped by product innovation, horsepower scaling, and integrated digital farming platforms, while regional manufacturers compete through customization for prairie farming conditions and localized dealer relationships.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Dealer Network Strength |

| Deere & Company | 1837 | USA | ~ | ~ | ~ | ~ | ~ |

| CNH Industrial | 2013 | UK | ~ | ~ | ~ | ~ | ~ |

| AGCO Corporation | 1990 | USA | ~ | ~ | ~ | ~ | ~ |

| CLAAS Group | 1913 | Germany | ~ | ~ | ~ | ~ | ~ |

| Buhler Industries | 1932 | Canada | ~ | ~ | ~ | ~ | ~ |

Canada Agricultural Equipment Large-Scale Market Analysis

Growth Drivers

Expansion of Prairie Large-Acreage Farming:

Expansion of prairie large-acreage farming is accelerating demand for Canada Agricultural Equipment Large-Scale machinery as farms consolidate and operational scale increases across Saskatchewan, Alberta, and Manitoba. Larger field sizes require equipment capable of covering more hectares per hour, making high-horsepower tractors and wide-span implements essential for productivity. Commercial grain farms are adopting fleet standardization strategies centered on large equipment platforms to reduce operational complexity and downtime. Mechanization intensity rises as labor availability declines and seasonal windows tighten in northern climates. Farm consolidation also increases capital capacity, enabling investment in advanced machinery systems. Large-scale cereal and oilseed production oriented toward export markets further necessitates efficient harvesting and seeding operations. Equipment manufacturers respond with higher horsepower classes and precision integration tailored to prairie agronomy. Dealer financing and trade-in programs facilitate replacement cycles among expanding farms. These structural shifts in farm size and production intensity continue reinforcing large-scale equipment demand across Canadian agriculture.

Adoption of Precision Agriculture Technologies:

Adoption of precision agriculture technologies is strengthening the Canada Agricultural Equipment Large-Scale market by embedding digital intelligence into tractors, harvesters, and seeding platforms across commercial farms. GPS-guided steering, variable rate application, and yield mapping enable farmers to optimize inputs and maximize output across heterogeneous prairie soils. Precision systems reduce overlap, minimize fuel use, and improve field efficiency, directly enhancing profitability under fluctuating commodity prices. Government-supported digital agriculture initiatives encourage adoption through incentives and advisory programs. Equipment OEMs integrate precision hardware and software as standard features in large-scale machinery, accelerating market penetration. Data-driven farm management platforms enable real-time monitoring and decision support across extensive farmland. Telematics connectivity also supports predictive maintenance and fleet optimization, reducing downtime during critical seasons. Dealers provide agronomic analytics services bundled with equipment sales, reinforcing technology value. As precision agriculture becomes operationally essential, demand for advanced large-scale equipment platforms continues expanding in Canada.

Market Challenges

High Capital Cost and Financing Constraints:

High capital cost and financing constraints significantly challenge adoption in the Canada Agricultural Equipment Large-Scale market because advanced tractors and harvesters require substantial upfront investment exceeding affordability for many farms. Equipment prices rise with horsepower scaling, precision integration, and emissions compliance technologies. Although large commercial farms possess stronger balance sheets, mid-sized operations face barriers to scaling mechanization capacity. Interest rate fluctuations influence financing costs, affecting purchasing decisions and replacement cycles. Seasonal revenue patterns in agriculture further complicate repayment structures for high-value equipment loans. Leasing and rental models remain limited in rural regions, reducing access flexibility. Commodity price volatility also weakens investment confidence among producers. Maintenance and service contracts add lifetime ownership costs beyond acquisition price. These financial pressures collectively restrain broader adoption of large-scale machinery across Canada’s agricultural sector.

Seasonal Utilization and Operational Risk Exposure:

Seasonal utilization and operational risk exposure create challenges in the Canada Agricultural Equipment Large-Scale market because machinery is used intensively only during seeding and harvesting windows while remaining idle for extended periods. Harsh weather variability in northern climates compresses fieldwork timelines, increasing pressure on equipment reliability and uptime. Short utilization cycles reduce return on investment compared to year-round industrial equipment. Unexpected breakdowns during peak seasons can cause significant yield losses and financial risk. Storage, maintenance, and winterization requirements add operational overhead outside active periods. Insurance and depreciation costs continue regardless of usage intensity. Contractors mitigate utilization risk through multi-farm operations, but individual farms face underutilization challenges. Limited diversification of crop types in prairie agriculture also concentrates machinery demand into narrow seasonal windows. These operational constraints reduce perceived economic efficiency of large-scale equipment ownership.

Opportunities

Autonomous and Semi-Autonomous Field Machinery Deployment:

Autonomous and semi-autonomous field machinery deployment represents a major opportunity in the Canada Agricultural Equipment Large-Scale market because large prairie farms provide ideal operating environments for driverless tractors and harvesters. Extensive, obstacle-free fields allow efficient autonomous navigation and route optimization. Labor shortages and rising wages increase economic incentives for automation adoption. OEMs are integrating machine vision, GPS guidance, and remote supervision capabilities into high-horsepower platforms. Autonomous equipment enables extended operating hours, including night operations during short seasonal windows. Precision tasks such as seeding and spraying benefit from consistent automated accuracy. Data integration with farm management systems enhances operational planning across vast farmland. Government innovation programs and test corridors support pilot deployments. As regulatory frameworks evolve, autonomous machinery adoption could substantially expand productivity in Canadian large-scale agriculture.

Equipment-as-a-Service and Leasing Model Expansion:

Equipment-as-a-service and leasing model expansion offers significant opportunity in the Canada Agricultural Equipment Large-Scale market by reducing capital barriers and improving utilization economics for high-value machinery. Subscription or seasonal leasing models allow farms to access advanced equipment without full ownership costs. Contractors and cooperatives can deploy shared fleets across multiple farms, maximizing annual utilization rates. Financial institutions and OEMs increasingly explore outcome-based financing tied to productivity metrics. Digital telematics enables usage monitoring and billing transparency for service-based equipment access. Leasing also accelerates technology refresh cycles, ensuring farms operate modern precision-enabled machinery. Smaller expanding farms gain access to large-scale equipment previously unaffordable under ownership models. Dealers benefit from recurring revenue and stronger customer retention. This transition toward service-based mechanization could reshape procurement dynamics in Canadian agriculture.

Future Outlook

The Canada Agricultural Equipment Large-Scale market is expected to maintain steady growth supported by ongoing farm consolidation, rising precision agriculture adoption, and expansion of export-oriented grain production. Technological evolution toward autonomous and digitally integrated machinery will enhance productivity across large prairie farms. Regulatory emphasis on emissions efficiency and digital agriculture support programs will reinforce modernization. Demand will also be driven by replacement cycles of aging fleets and increasing mechanization intensity across commercial-scale operations.

Major Players

- Deere & Company

- ‘CNH Industrial

- AGCO Corporation

- CLAAS Group

- Buhler Industries

- Kubota Corporation

- Rostselmash

- Horsch Maschinen

- SeedMaster Manufacturing

- MacDon Industries

- Versatile Tractors

- Bourgault Industries

- Morris Equipment

- New Holland Agriculture

- Case IH

Key Target Audience

- Agricultural equipment manufacturers

- Precision agriculture technology providers

- Farm machinery distributors and dealers

- Large commercial farming enterprises

- Agricultural cooperatives

- Equipment leasing and financing companies

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key market variables including equipment categories, horsepower classes, precision integration levels, farm size distribution, and regional mechanization intensity were identified to define analytical boundaries and segmentation structure for the Canada Agricultural Equipment Large-Scale market.

Step 2: Market Analysis and Construction

Historical equipment sales data, farm mechanization trends, regional agricultural production patterns, and OEM shipment information were synthesized to construct market size estimates and competitive positioning frameworks for large-scale agricultural machinery.

Step 3: Hypothesis Validation and Expert Consultation

Industry specialists including farm equipment dealers, agronomists, and machinery manufacturers validated adoption drivers, technology penetration trends, and procurement behavior across prairie agricultural operations and commercial farms.

Step 4: Research Synthesis and Final Output

All validated data, regional insights, and technology adoption trends were integrated into structured market analysis, segmentation modeling, and strategic outlook to produce the final Canada Agricultural Equipment Large-Scale market report.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of large-acreage grain farming operations in prairie provinces

Rising adoption of high-capacity machinery to address labor shortages

Government incentives supporting precision agriculture investment

Need for higher field productivity and reduced operational time

Growth in export-oriented cereal and oilseed production - Market Challenges

High capital cost of large-scale agricultural machinery

Seasonal utilization limiting return on investment

Complex maintenance requirements and service availability

Financing constraints for mid-sized farms scaling up

Volatility in crop prices affecting equipment purchases - Market Opportunities

Integration of autonomous and semi-autonomous field equipment

Expansion of equipment leasing and equipment-as-a-service models

Growth of data-driven precision farming ecosystems - Trends

Shift toward ultra-high horsepower tractors above 500 HP

Increasing adoption of track-based mobility systems

Integration of telematics and remote diagnostics

Demand for wide-span seeding and spraying equipment

Adoption of controlled traffic farming machinery configurations - Government Regulations & Defense Policy

Emissions standards for off-road diesel engines in agricultural equipment

Federal safety regulations for autonomous farm machinery testing

Subsidy programs for precision agriculture technology adoption - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

High-horsepower tractors

Self-propelled combine harvesters

Large-scale air seeders

Forage harvesters

Precision sprayers - By Platform Type (In Value%)

Wheeled equipment platforms

Tracked equipment platforms

Articulated platforms

Autonomous-ready platforms

Integrated precision platforms - By Fitment Type (In Value%)

Factory-integrated systems

Dealer-installed upgrades

Aftermarket retrofits

Modular attachments

Telematics-enabled kits - By EndUser Segment (In Value%)

Large commercial grain farms

Corporate farming enterprises

Agricultural contractors

Cooperative farming groups

Research and institutional farms - By Procurement Channel (In Value%)

OEM dealer networks

Direct manufacturer sales

Agricultural equipment auctions

Leasing and financing providers

Digital procurement platforms - By Material / Technology (in Value %)

Precision GPS guidance systems

ISOBUS-compatible electronics

Advanced hydraulics systems

Autonomous operation modules

Variable rate application technology

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Horsepower Range, Header Width Capacity, Precision Integration Level, Autonomy Capability, Fuel Efficiency, Telematics Features, Track vs Wheel Configuration, Dealer Network Strength, Financing Options, Aftermarket Support)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Deere & Company

CNH Industrial

AGCO Corporation

Kubota Corporation

CLAAS Group

Buhler Industries

Morris Equipment

SeedMaster Manufacturing

MacDon Industries

Versatile Tractors

Rostselmash

Horsch Maschinen

Fendt

New Holland Agriculture

Case IH

- Large prairie grain farms prioritizing scale and operational efficiency

- Corporate farming enterprises investing in fleet standardization

- Agricultural contractors demanding multi-crop versatility

- Institutional farms adopting advanced precision technologies

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now