Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Canada agricultural equipment market reached USD ~ billion based on a recent historical assessment, supported by strong mechanization intensity across grain and oilseed production systems and widespread adoption of high-horsepower machinery. Demand is driven by large farm sizes, high labor costs, and precision agriculture integration across seeding, harvesting, and spraying operations. Government-backed farm modernization programs and sustained export-oriented crop cultivation further sustain equipment replacement cycles and technology upgrades across agricultural operations nationwide.

Saskatchewan, Alberta, and Manitoba dominate the Canada agricultural equipment market due to extensive prairie farmland, large-scale cereal and oilseed cultivation, and high mechanization dependency in commercial farming operations. These provinces support high equipment utilization through vast acreage and shorter planting windows requiring efficient machinery. Ontario also contributes significantly through mixed farming and specialty crop production requiring diversified equipment types. Strong dealer networks, grain export logistics, and advanced farming practices reinforce regional equipment demand concentration.

Market Segmentation

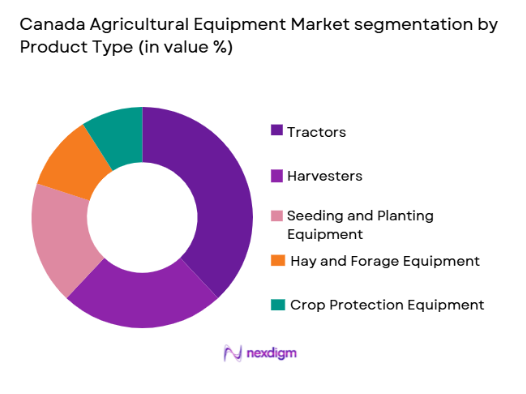

By Product Type:

Canada agricultural equipment market is segmented by product type into tractors, harvesters, seeding and planting equipment, hay and forage equipment, and crop protection equipment. Recently, tractors have a dominant market share due to factors such as universal farm applicability, high replacement frequency, and expanding demand for high-horsepower models suited to large prairie farms. Tractors function as primary power units supporting multiple attachments including seeders, sprayers, and tillage tools, increasing their operational value. Mechanization growth in grain farming and livestock feed production further sustains tractor demand across provinces. Adoption of precision-ready tractors with GPS and telematics capabilities strengthens their position in commercial agriculture. Government-supported farm expansion and consolidation trends also favor higher-capacity tractor procurement across Canadian agricultural regions.

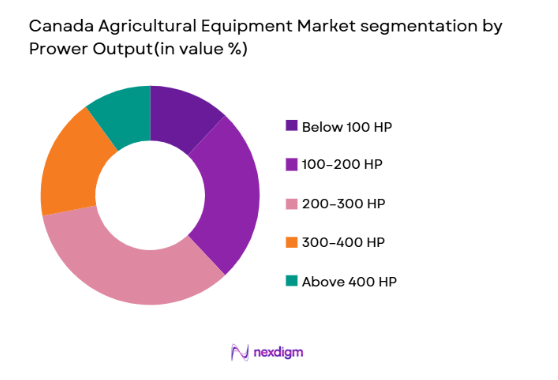

By Power Output:

Canada agricultural equipment market is segmented by power output into below 100 HP, 100–200 HP, 200–300 HP, 300–400 HP, and above 400 HP equipment. Recently, 200–300 HP equipment has a dominant market share due to factors such as suitability for large-scale grain operations, compatibility with advanced implements, and balance between fuel efficiency and field capacity. Prairie farming systems require mid-to-high horsepower machinery capable of pulling wide seeders and tillage tools across extensive acreage. Equipment in this range supports precision agriculture integration and multi-implement operations common in Canadian cereal production. Commercial farms prioritize this horsepower band for versatility across planting, tillage, and hauling applications. Expansion of consolidated farms and contractor services further reinforces demand for this power segment in mechanized agricultural regions.

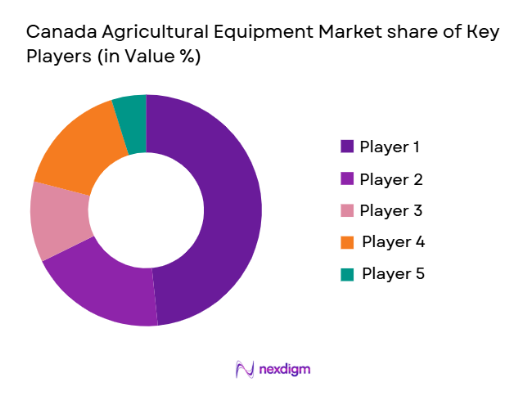

Competitive Landscape

Canada agricultural equipment market exhibits moderate consolidation with strong presence of global manufacturers and specialized domestic implement producers serving prairie agriculture. Large multinational firms dominate tractor and harvester categories, while Canadian companies lead in seeding, tillage, and grain handling equipment. Extensive dealer networks and aftersales support strongly influence market positioning. Technological differentiation through precision agriculture integration and high-capacity machinery platforms defines competitive advantage across commercial farming segments.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Prairie Farming Specialization |

| Deere & Company | 1837 | USA | ~ | ~ | ~ | ~ | ~ |

| CNH Industrial | 2013 | UK | ~ | ~ | ~ | ~ | ~ |

| AGCO Corporation | 1990 | USA | ~ | ~ | ~ | ~ | ~ |

| Kubota Corporation | 1890 | Japan | ~ | ~ | ~ | ~ | ~ |

| Buhler Industries | 1932 | Canada | ~ | ~ | ~ | ~ | ~ |

Canada Agricultural Equipment Market Analysis

Growth Drivers

Expansion of Large-Scale Mechanized Grain Farming:

Expansion of large-scale mechanized grain farming across prairie provinces significantly drives equipment demand in Canada agricultural equipment market. Commercial farms increasingly cultivate thousands of hectares of cereals and oilseeds, requiring high-capacity tractors, seeders, and harvesters capable of covering vast acreage within limited planting and harvesting windows. Short seasonal cycles and climate variability necessitate efficient machinery capable of rapid field operations, encouraging investment in advanced equipment platforms. Farm consolidation trends further increase average farm size, amplifying reliance on mechanization to maintain productivity and profitability. Grain export orientation strengthens equipment utilization rates, as producers aim to maximize yields and operational efficiency. High labor costs and workforce shortages in rural regions also accelerate mechanization adoption across farming operations. Modern prairie agriculture depends heavily on precision-enabled equipment to optimize input application and reduce operational waste. Continuous replacement cycles of aging machinery fleets sustain long-term market growth. Financial incentives and favorable financing programs enable farmers to upgrade to larger and technologically advanced equipment platforms, reinforcing mechanized grain farming expansion.

Adoption of Precision Agriculture and Smart Machinery Technologies:

Adoption of precision agriculture and smart machinery technologies strongly drives Canada agricultural equipment market by enhancing productivity and cost efficiency across farming systems. Farmers increasingly integrate GPS guidance, variable rate application, and telematics into tractors and implements to optimize seeding, fertilization, and crop protection operations. Precision-enabled equipment reduces input wastage and improves yield consistency, supporting profitability under volatile commodity prices. Data-driven decision-making tools embedded in machinery platforms enable real-time field monitoring and operational adjustments. Large commercial farms prioritize smart equipment to manage extensive acreage efficiently and maintain competitive production costs. Equipment manufacturers continuously introduce automation features such as auto-steering and section control, increasing technology penetration. Government sustainability initiatives promoting resource-efficient agriculture further support adoption of precision-enabled machinery. Integration of farm management software with equipment telematics enhances operational planning and fleet coordination. Technological upgrades and digital agriculture transition collectively accelerate equipment replacement demand across Canadian agricultural regions.

Market Challenges

High Capital Cost and Financing Burden of Advanced Equipment:

High capital cost and financing burden of advanced agricultural machinery poses a significant challenge in Canada agricultural equipment market, particularly for small and mid-sized farms. High-horsepower tractors, combines, and precision-enabled implements require substantial upfront investment, often exceeding individual farm capital capacity. Financing costs increase under fluctuating interest rates, raising total ownership expenditure and delaying procurement decisions. Economic volatility in crop prices directly impacts farm income stability, reducing farmers’ ability to invest in new equipment. Seasonal revenue patterns further complicate repayment schedules and financing access. Smaller farms often rely on aging machinery due to affordability constraints, limiting market expansion in lower-scale segments. Maintenance and spare parts costs for advanced equipment also add to operational expenses. Equipment depreciation and rapid technological obsolescence discourage frequent replacement cycles. Financial risk associated with large machinery investment remains a persistent barrier to broader adoption across diverse Canadian farming structures.

Supply Chain Dependence on Imported Components and Parts:

Supply chain dependence on imported components and parts creates operational and cost challenges in Canada agricultural equipment market. Many tractors and advanced implements rely on globally sourced engines, electronics, hydraulics, and precision agriculture modules, exposing manufacturers and dealers to international supply disruptions. Logistics constraints, currency fluctuations, and trade uncertainties affect equipment availability and pricing stability across Canada. Delays in component supply can extend equipment delivery timelines, disrupting seasonal procurement schedules for farmers. Replacement parts shortages also impact machinery maintenance and uptime during critical farming periods. Canadian implement manufacturers face cost pressures when sourcing imported steel and specialized components. Dependence on foreign technology providers limits domestic manufacturing resilience and innovation independence. Transportation costs across long supply chains increase final equipment prices in remote agricultural regions. Supply chain vulnerabilities therefore constrain market stability and operational reliability for both manufacturers and end users.

Opportunities

Electrification and Low-Emission Agricultural Machinery Development:

Electrification and low-emission agricultural machinery development presents a major opportunity in Canada agricultural equipment market as environmental regulations and sustainability goals reshape farm mechanization. Canadian agriculture faces increasing pressure to reduce greenhouse gas emissions from diesel-powered machinery. Development of electric tractors, hybrid drivetrains, and alternative fuel systems aligns with national climate commitments and clean technology programs. Electrified equipment reduces fuel consumption and operational emissions while improving energy efficiency in field operations. Government incentives supporting clean farm technology adoption encourage farmers to transition toward low-emission machinery platforms. Large farms with high fuel consumption represent key early adopters of electrified equipment. Canadian manufacturers and technology firms can innovate localized solutions suited to cold climates and large-field operations. Integration of electric powertrains with precision agriculture systems enhances operational control and automation capabilities. Electrification therefore opens new product segments and technological differentiation opportunities across the agricultural equipment ecosystem.

Autonomous and Robotics-Based Field Operation Systems:

Autonomous and robotics-based field operation systems create significant growth opportunities in Canada agricultural equipment market by addressing labor shortages and operational efficiency challenges. Large Canadian farms require continuous field operations across short seasonal windows, often constrained by limited skilled labor availability. Autonomous tractors, robotic seeders, and self-operating sprayers enable extended operating hours and reduce dependence on manual labor. Robotics systems improve precision in seeding, spraying, and harvesting tasks, enhancing crop uniformity and input efficiency. Automation technologies also support remote monitoring and fleet coordination across vast farmland. Canadian prairie agriculture, characterized by large contiguous fields, provides favorable conditions for autonomous equipment deployment. Integration of robotics with precision agriculture data systems enhances decision accuracy and field optimization. Technology partnerships between machinery manufacturers and automation developers accelerate commercialization of autonomous solutions. Adoption of robotics-based equipment therefore represents a transformative opportunity for productivity and mechanization advancement in Canadian agriculture.

Future Outlook

Canada agricultural equipment market is expected to experience steady expansion supported by mechanized grain farming, precision agriculture adoption, and farm consolidation trends. Technological innovation in automation, electrification, and digital farming platforms will reshape equipment design and procurement patterns. Government sustainability initiatives and clean technology incentives will encourage adoption of low-emission machinery. Increasing labor constraints and large-scale commercial farming will sustain demand for high-capacity equipment across prairie provinces.

Major Players

- Deere & Company

- CNH Industrial

- AGCO Corporation

- Kubota Corporation

- Buhler Industries

- MacDon Industries

- Bourgault Industries

- SeedMaster Manufacturing

- Salford Group

- Morris Equipment

- Degelman Industries

- Highline Manufacturing

- Honey Bee Manufacturing

- Rite Way Manufacturing

- Elmer’s Manufacturing

Key Target Audience

- Agricultural equipment manufacturers

- Farm machinery distributors

- Large commercial farming enterprises

- Agricultural cooperatives

- Precision agriculture technology providers

- Farm financing institutions

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Market variables including equipment categories, horsepower segments, regional farming patterns, mechanization intensity, and technology adoption rates were identified through agricultural statistics, equipment sales data, and industry reports.

Step 2: Market Analysis and Construction

Data from trade associations, manufacturer reports, agricultural census information, and import–export statistics were synthesized to construct market size and segmentation frameworks across Canada agricultural equipment market.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultations with farm equipment dealers, agricultural economists, and machinery specialists to confirm demand drivers, technology trends, and regional procurement patterns.

Step 4: Research Synthesis and Final Output

Validated datasets and qualitative insights were integrated to produce final market estimates, segmentation shares, competitive positioning, and forward-looking analysis aligned with Canadian agricultural mechanization dynamics.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Tractors

Harvesters

Seeding and Planting Equipment

Hay and Forage Equipment

Crop Protection Equipment - By Platform Type (In Value%)

Wheeled Equipment

Tracked Equipment

Autonomous and Robotic Platforms

Mounted and Attached Systems

Self-Propelled Systems - By Fitment Type (In Value%)

OEM Factory-Fitted Systems

Aftermarket Retrofit Kits

Modular Attachments

Integrated Smart Equipment Packages

Custom-Built Configurations - By EndUser Segment (In Value%)

Large Commercial Farms

Family-Owned Farms

Agricultural Contractors

Farming Cooperatives

Government and Research Farms - By Procurement Channel (In Value%)

Direct Manufacturer Sales

Authorized Dealer and Distributor Networks

Cooperative Purchasing Programs

Government Subsidy and Tender Programs

Online and Digital Marketplaces - By Material / Technology (in Value %)

Precision GPS Guidance Systems

Telematics and IoT Monitoring

Electric and Hybrid Drivetrains

Advanced Hydraulic Systems

AI-Based Automation and Control

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Product Portfolio Breadth, Power Range Coverage, Precision Agriculture Integration, Dealer Network Strength, Aftermarket Support, Manufacturing Capacity, Export Presence, Technology Partnerships, Pricing Positioning, Customization Capability)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Buhler Industries

MacDon Industries

Bourgault Industries

SeedMaster Manufacturing

Salford Group

Schulte Industries

Degelman Industries

Morris Equipment Ltd.

Rite Way Manufacturing

Highline Manufacturing

Honey Bee Manufacturing

Seed Hawk Inc.

Elmer’s Manufacturing

Mandako Agri-Marketing

REM Manufacturing

- Large grain producers prioritize high-capacity and precision-integrated machinery

- Mixed and livestock farms demand versatile and multi-function equipment

- Custom farming contractors invest in durable high-utilization fleets

- Research and institutional farms adopt advanced automation technologies

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now