Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Canada AI servers and GPU hardware market reached approximately USD ~ billion in enterprise and hyperscale accelerator server spending based on a recent historical assessment, driven by rapid deployment of generative AI infrastructure, hyperscale cloud expansion, and national AI compute capacity programs. Demand is concentrated in high-performance GPU servers, AI training clusters, and accelerated data center nodes supporting large language model development, enterprise AI adoption, and sovereign compute initiatives across public and private sectors.

Toronto, Montreal, and Vancouver dominate Canada AI servers and GPU hardware deployment due to hyperscale data center presence, AI research ecosystems, and cloud region concentration. Montreal hosts major AI research institutes and hyperscale compute clusters, Toronto leads enterprise AI adoption and financial sector compute demand, while Vancouver benefits from technology industry growth and Pacific connectivity supporting cloud and GPU infrastructure expansion within Canada’s national AI compute network.

Market Segmentation

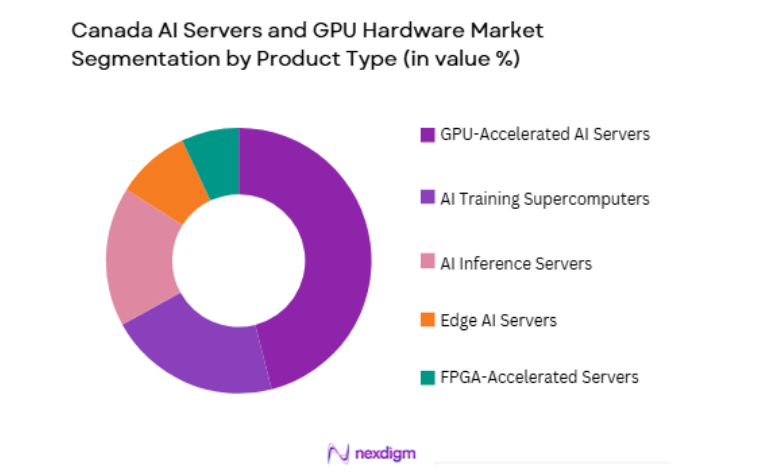

By Product Type

Canada AI Servers and GPU Hardware market is segmented by product type into GPU-accelerated AI servers, AI training supercomputers, edge AI servers, FPGA-accelerated servers, and AI inference servers. Recently, GPU-accelerated AI servers has a dominant market share due to factors such as hyperscale cloud GPU cluster deployment, enterprise generative AI workloads, and large-scale model training infrastructure requirements. NVIDIA-based accelerator platforms dominate AI compute architecture in Canada, supported by hyperscale cloud providers and sovereign AI compute investments, resulting in higher infrastructure spending on multi-GPU server nodes compared with inference-optimized or alternative accelerator systems across national AI data center deployments.

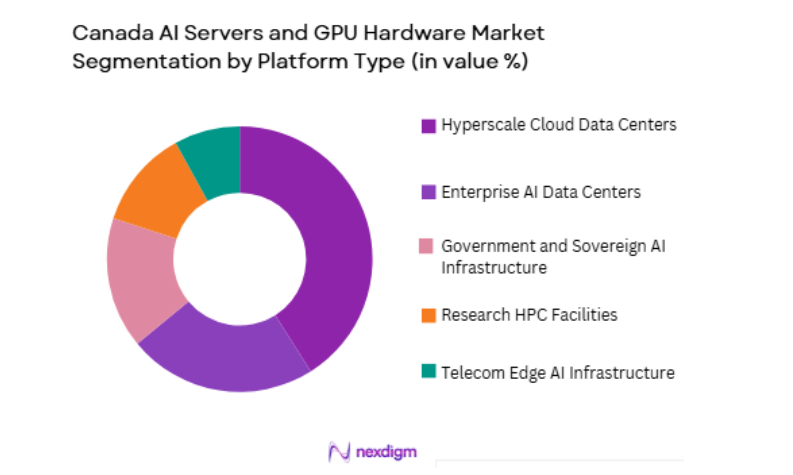

By Platform Type

Canada AI Servers and GPU Hardware market is segmented by platform type into hyperscale cloud data centers, enterprise AI data centers, government and sovereign AI infrastructure, research HPC facilities, and telecom edge AI infrastructure. Recently, hyperscale cloud data centers has a dominant market share due to factors such as large-scale AI cloud service expansion, GPU cluster concentration, and cloud-based generative AI deployment across Canadian enterprises. Global hyperscalers and domestic cloud providers are building GPU-dense data centers in Canada to support AI training and inference services, concentrating server hardware procurement within hyperscale platforms compared with distributed enterprise or research deployments.

Competitive Landscape

Canada AI servers and GPU hardware market is highly concentrated, dominated by global accelerator vendors and hyperscale server manufacturers supplying GPU-dense systems to cloud providers and large enterprises, while domestic system integrators and data center operators support deployment and integration. NVIDIA ecosystem leadership, hyperscale procurement scale, and AI accelerator supply constraints shape competitive positioning and partnership structures across Canadian AI compute infrastructure projects.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | AI Accelerator Platform |

| NVIDIA | 1993 | USA | ~ | ~ | ~ | ~ | ~ |

| Supermicro | 1993 | USA | ~ | ~ | ~ | ~ | ~ |

| Dell Technologies | 1984 | USA | ~ | ~ | ~ | ~ | ~ |

| Hewlett Packard Enterprise | 1939 | USA | ~ | ~ | ~ | ~ | ~ |

| Lenovo | 1984 | China | ~ | ~ | ~ | ~ | ~ |

Canada AI Servers and GPU Hardware Market Analysis

Growth Drivers

Hyperscale Cloud AI Infrastructure Expansion

Canada AI servers and GPU hardware demand is strongly driven by hyperscale cloud providers expanding GPU-dense data centers to support generative AI services, enterprise AI workloads, and sovereign cloud compute initiatives across the country. Hyperscalers are deploying large GPU clusters for model training and inference services accessible to enterprises, startups, and government agencies, concentrating hardware procurement in high-performance AI servers. Canada’s proximity to major US cloud ecosystems and favorable energy profile encourages hyperscale investment in AI data center infrastructure. National AI strategies promote domestic compute capacity to reduce reliance on foreign cloud regions, accelerating server hardware deployment. GPU server demand scales exponentially with model size and training requirements, amplifying infrastructure spending per data center. Enterprise AI adoption across finance, healthcare, and retail sectors drives cloud GPU consumption, reinforcing hyperscale procurement cycles. AI service competition among cloud providers leads to continuous GPU hardware upgrades and cluster expansion. These factors collectively sustain high-growth demand for AI servers and accelerators across Canada’s cloud infrastructure ecosystem.

National Sovereign AI and HPC Compute Programs

Canada AI servers and GPU hardware market growth is propelled by government-backed sovereign AI compute initiatives and high-performance computing modernization programs aimed at strengthening domestic AI research and innovation capacity. Federal and provincial funding supports AI supercomputing clusters, research GPU facilities, and national AI infrastructure networks accessible to academia and industry. Sovereign compute programs require procurement of advanced GPU servers and AI accelerators to maintain competitiveness in global AI development. Public sector investment reduces infrastructure cost barriers for domestic AI companies and startups, increasing overall hardware demand. National HPC upgrades integrate AI accelerators into traditional supercomputing centers, expanding GPU server deployments. Policy emphasis on domestic AI capability encourages localized hardware procurement and deployment. Collaborative AI compute facilities across research and industry sectors multiply infrastructure scale. These initiatives create sustained non-commercial demand streams complementing hyperscale cloud infrastructure expansion in Canada.

Market Challenges

AI Accelerator Supply Constraints and Import Dependence

Canada AI servers and GPU hardware deployment faces significant constraints due to limited global supply of advanced AI accelerators, particularly high-end GPUs, and dependence on imported semiconductor hardware from a small number of global vendors. AI accelerator shortages delay server deployments and increase procurement costs for Canadian infrastructure operators. Export controls and geopolitical restrictions affect availability of leading-edge GPU hardware in global markets. Canada lacks domestic AI chip manufacturing capability, increasing vulnerability to external supply chain disruptions. Hyperscale cloud providers receive priority allocation from vendors, limiting access for smaller Canadian enterprises and research institutions. Hardware lead times extend AI infrastructure rollout schedules across sectors. Dependence on foreign accelerator ecosystems constrains domestic hardware innovation. These factors collectively limit Canada’s ability to scale AI compute infrastructure independently.

High Power Density and Data Center Infrastructure Requirements

Canada AI servers and GPU hardware installations require extremely high power density, cooling capacity, and data center infrastructure readiness, creating challenges in facility upgrades and deployment scalability. GPU servers consume significantly more power per rack than traditional servers, necessitating electrical and cooling retrofits in existing data centers. Liquid cooling and advanced thermal management systems increase infrastructure complexity and cost. Grid connection capacity and energy provisioning constraints affect hyperscale AI data center expansion in some regions. Data center operators must invest in specialized AI-ready facilities to host accelerator clusters. High operational energy costs influence deployment economics for AI infrastructure providers. Infrastructure upgrades lengthen deployment timelines and capital requirements. These factors constrain rapid scaling of AI server installations across Canada.

Opportunities

Expansion of Sovereign AI Cloud Infrastructure

Canada has strong opportunity to expand AI servers and GPU hardware deployment through development of sovereign AI cloud platforms providing domestic AI compute services to government, enterprises, and research organizations. Sovereign AI clouds require large GPU server clusters and national data center infrastructure. Government data residency requirements support domestic AI hardware procurement. National AI startups benefit from accessible local compute resources. Public-private partnerships can finance large AI data center projects. Sovereign cloud initiatives reduce reliance on foreign hyperscale providers. AI service demand across regulated sectors supports infrastructure growth. These developments create sustained demand for AI servers in Canada.

Edge AI and Telecom Infrastructure Integration

Canada AI servers and GPU hardware market can grow through integration of AI accelerators into telecom edge networks and distributed computing infrastructure supporting real-time AI applications. Telecom operators are deploying edge data centers requiring compact GPU servers. Autonomous systems, smart cities, and industrial AI applications need localized compute nodes. 5G network expansion supports edge AI deployment. Edge inference workloads expand beyond centralized cloud AI. Telecom infrastructure modernization includes AI hardware integration. Distributed AI architectures increase server unit demand. This opportunity expands AI hardware deployment beyond hyperscale data centers.

Future Outlook

Canada AI servers and GPU hardware market is expected to expand rapidly over the next five years as hyperscale cloud GPU clusters, sovereign AI compute programs, and enterprise generative AI adoption accelerate infrastructure deployment. Continued government funding for national AI compute capacity, advances in accelerator technology, and rising enterprise AI workloads will sustain demand. Expansion of AI data centers and edge AI infrastructure will further strengthen Canada’s position in global AI computing ecosystems.

Major Players

- NVIDIA

- Supermicro

- Dell Technologies

- Hewlett Packard Enterprise

- Lenovo

- Cisco Systems

- Inspur

- AMD

- Intel

- ASUS

- Gigabyte

- Penguin Solutions

- Lambda Labs

- Oracle Cloud Infrastructure

- Amazon Web Services

Key Target Audience

- Hyperscale cloud providers

- Enterprise data center operators

- Telecom network operators

- Investments and venture capitalist firms

- Government and regulatory bodies

- AI software companies

- Semiconductor hardware distributors

- Industrial automation firms

Research Methodology

Step 1: Identification of Key Variables

AI server shipment volumes, GPU accelerator demand, hyperscale data center expansion, sovereign AI funding, and enterprise AI adoption indicators were identified from industry reports and infrastructure disclosures. Key variables included accelerator density per server and regional data center capacity.

Step 2: Market Analysis and Construction

Canada AI servers and GPU hardware market size was constructed using server hardware spending, GPU procurement data, hyperscale and enterprise AI data center investments, and national HPC infrastructure upgrades across segments. Platform deployment patterns were mapped to hardware demand.

Step 3: Hypothesis Validation and Expert Consultation

Market assumptions were validated through consultation with AI infrastructure engineers, cloud architects, and data center operators in Canada. Accelerator supply trends and AI workload demand were cross-checked with industry experts and procurement data.

Step 4: Research Synthesis and Final Output

All quantitative and qualitative insights were synthesized into structured market analysis covering segmentation, competitive landscape, growth drivers, and outlook. Findings were consolidated into a comprehensive Canada AI servers and GPU hardware market report.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of AI compute capacity across Canadian enterprises and research

Strong national AI research ecosystem driving GPU infrastructure demand

Rising adoption of generative AI and data intensive workloads - Market Challenges

Dependence on imported advanced GPUs and accelerators

High energy and cooling requirements of dense AI clusters

Limited domestic large scale AI cloud infrastructure ownership - Market Opportunities

Development of sovereign Canadian AI compute infrastructure

Expansion of AI clusters for natural resources and climate analytics

Growth of liquid cooled and energy efficient AI server deployments - Trends

Shift toward GPU dense and accelerator rich AI server architectures

Adoption of hybrid cloud and on premise AI compute environments

Increasing deployment of liquid cooled and rack scale AI systems - Government regulations

Canadian data sovereignty and privacy regulations for AI hosting

Federal AI and digital infrastructure funding initiatives

Energy efficiency and sustainability standards for data centers - SWOT analysis

- Porters Five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

GPU Accelerated AI Servers

AI Training Supercomputers

AI Inference Optimized Servers

Hybrid CPU GPU AI Systems

High Density Rack Scale AI Platforms - By Platform Type (In Value%)

Hyperscale Cloud AI Infrastructure

Enterprise Private AI Clusters

Research and Academic AI HPC

Edge AI Compute Platforms

Government Sovereign AI Systems - By Fitment Type (In Value%)

Rack Integrated AI Servers

Blade AI Server Modules

Preconfigured AI Appliances

Custom AI Cluster Deployments

Liquid Cooled AI Systems - By End User Segment (In Value%)

Cloud and Technology Providers

Financial Services Institutions

Healthcare and Life Sciences Organizations

- Market Share Analysis

- Cross Comparison Parameters (Compute Performance, GPU Architecture, Cooling Technology, Interconnect Bandwidth, Scalability, Memory Bandwidth, Power Efficiency, Form Factor Density, Software Stack Compatibility, Deployment Flexibility)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

NVIDIA

Advanced Micro Devices

Intel

Hewlett Packard Enterprise

Dell Technologies

Lenovo

Supermicro

Cisco Systems

IBM

Fujitsu

Atos

NEC

Inspur

Gigabyte Technology

Graphcore

- Cloud providers scaling GPU clusters for AI services

- Financial institutions deploying private AI compute for analytics

- Energy sector using AI compute for exploration and optimization

- Universities expanding AI supercomputing infrastructure

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now