Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The diagnostic labs market in Canada has seen substantial growth driven by a combination of factors such as increasing healthcare demands and advancements in diagnostic technology. Based on a recent historical assessment, the market size is valued at approximately USD ~ billion, with growth fueled by an aging population and heightened demand for medical testing services. Moreover, improvements in lab technologies, including molecular diagnostics and automation, have supported this market expansion, enhancing testing capabilities and operational efficiency. Government healthcare investments and insurance coverage further contribute to market development.

Cities like Toronto, Montreal, and Vancouver are the major hubs for diagnostic lab services, primarily due to their advanced healthcare infrastructure and large, diverse populations. These cities have established a strong presence in the market due to high patient volume, greater healthcare expenditure, and a focus on medical research and innovation. Additionally, proximity to leading healthcare institutions and universities plays a significant role in fostering technological advancements in diagnostic services. Consequently, these regions maintain a leading position in the country’s diagnostic lab sector.

Market Segmentation

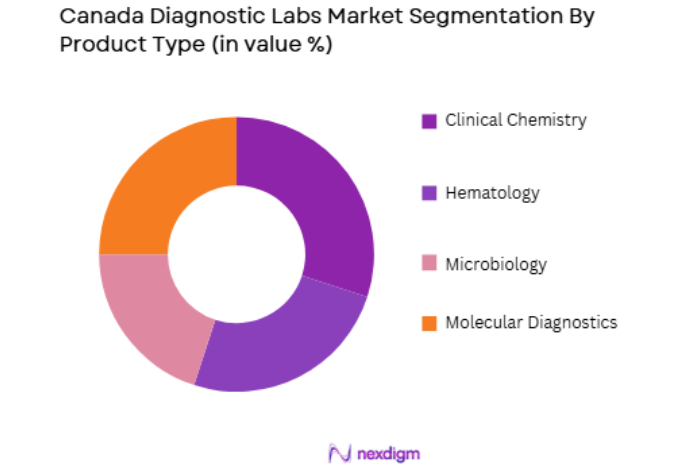

By Product Type

Canada’s diagnostic labs market is segmented by product type into clinical chemistry, hematology, microbiology, and molecular diagnostics. Recently, the molecular diagnostics sub-segment has seen a dominant market share due to the growing adoption of advanced technologies such as PCR and next-generation sequencing. The increasing prevalence of chronic diseases like cancer and genetic disorders has further driven the demand for molecular diagnostics. Additionally, the rising awareness of precision medicine, coupled with the need for rapid, accurate diagnostic results, has contributed to the surge in this sub-segment’s growth. These factors have led to a steady rise in investments towards molecular diagnostic platforms, making it the dominant product category in the market.

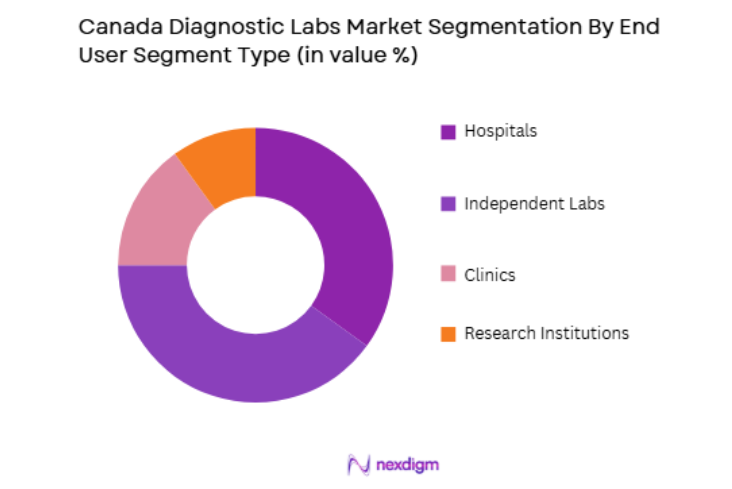

By End-User Segment

Canada’s diagnostic labs market is segmented by end-user into hospitals, independent labs, clinics, and research institutions. Independent labs have recently gained a dominant market share as more patients seek diagnostic services outside of traditional hospital settings. Factors contributing to this trend include the increasing preference for convenience, lower costs, and shorter wait times associated with independent labs. These labs are becoming increasingly popular due to their flexibility and ability to offer specialized testing services. Independent diagnostic labs also benefit from advancements in technology that streamline operations and improve accuracy, further enhancing their appeal to both patients and healthcare providers.

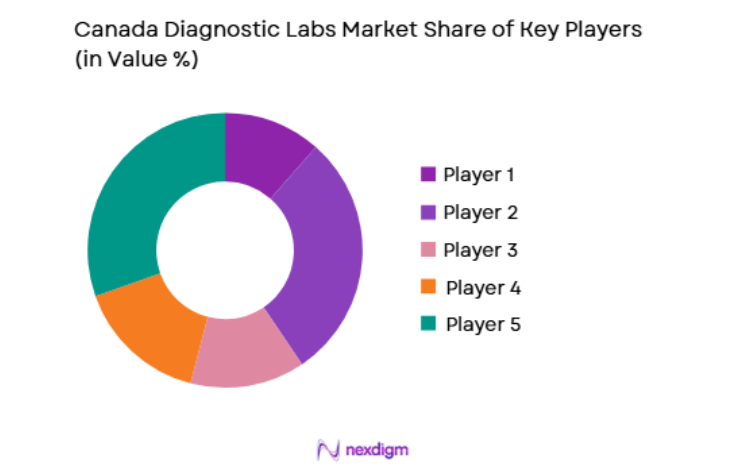

Competitive Landscape

The competitive landscape of Canada’s diagnostic labs market reflects a mix of large multinational companies and smaller, specialized regional players. Market consolidation has been a key trend, with major players acquiring regional labs to expand their geographic footprint and service offerings. Technological innovations, such as automation and AI-driven diagnostics, have further intensified competition. These companies focus on improving efficiency, reducing turnaround times, and enhancing diagnostic accuracy to maintain a competitive edge in a growing and evolving market.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Additional Parameter |

| LabCorp | 1978 | Burlington, NC | ~ | ~ | ~ | ~ | ~ |

| Quest Diagnostics | 1967 | Madison, NJ | ~ | ~ | ~ | ~ | ~ |

| LifeLabs | 1969 | Toronto, Canada | ~ | ~ | ~ | ~ | ~ |

| Dynacare | 1974 | Brampton, Canada | ~ | ~ | ~ | ~ | ~ |

| Bio-Rad Laboratories | 1952 | Hercules, CA | ~ | ~ | ~ | ~ | ~ |

Canada Diagnostic Labs Market Analysis

Growth Drivers

Aging Population

The aging population in Canada is one of the primary growth drivers for the diagnostic labs market. As people age, they become more susceptible to chronic diseases and require frequent diagnostic testing to manage their health conditions. This demographic shift leads to an increase in demand for routine medical testing, diagnostics for age-related conditions, and long-term monitoring of chronic illnesses such as diabetes, cardiovascular diseases, and cancer. The rising number of elderly citizens in Canada means that healthcare systems must adapt to the growing demand for diagnostic services. Consequently, diagnostic labs are seeing increased volumes of testing, which propels market expansion. Technological advancements in diagnostic methods, including genetic testing and molecular diagnostics, also cater to this demographic’s need for personalized treatment plans, further boosting market growth.

Technological Advancements

Technological advancements in diagnostic equipment and methods have significantly contributed to the growth of Canada’s diagnostic labs market. The development of molecular diagnostics, automation, and AI-powered diagnostic tools has improved the accuracy and speed of diagnostic testing. Innovations like next-generation sequencing and PCR-based testing allow for more precise detection of diseases at earlier stages, enhancing patient outcomes. These technologies also enable diagnostic labs to handle larger volumes of tests more efficiently, meeting the increasing demand for healthcare services. Automation has streamlined lab workflows, reducing human error and increasing throughput. Additionally, the adoption of digital health technologies and telemedicine has expanded access to diagnostic services, especially in remote areas, further supporting market growth.

Market Challenges

Regulatory Compliance

One of the major challenges facing the diagnostic labs market in Canada is navigating the complex regulatory environment. Diagnostic labs are subject to strict regulations that govern the quality and safety of testing procedures, particularly in areas such as patient data protection, lab certifications, and accreditation. Compliance with these regulations requires significant investments in quality control systems, employee training, and lab infrastructure. Failure to meet regulatory standards can result in costly fines and damage to the lab’s reputation. Additionally, the evolving nature of healthcare regulations, especially with new technologies like AI and genomic data, creates a moving target for compliance, adding further complexity to lab operations.

Workforce Shortages

Canada’s diagnostic labs are also facing workforce shortages, particularly in specialized areas like molecular diagnostics and pathology. The demand for highly skilled professionals is increasing, but there are not enough qualified workers to meet the needs of the expanding market. This shortage has led to increased pressure on existing staff, longer turnaround times for test results, and potential delays in patient diagnosis. Additionally, the competition for skilled labor is fierce, as diagnostic labs must offer competitive wages and benefits to attract top talent. Addressing these workforce challenges is crucial for maintaining operational efficiency and meeting the growing demand for diagnostic services.

Opportunities

Expansion of Personalized Medicine

One of the key opportunities in Canada’s diagnostic labs market is the expansion of personalized medicine. As the healthcare industry increasingly shifts towards tailored treatments based on individual genetic profiles, diagnostic labs are positioned at the forefront of this trend. Advanced diagnostic tools, such as genetic testing and molecular diagnostics, enable labs to provide more accurate diagnoses and treatment plans. Personalized medicine offers significant potential for improved patient outcomes and cost-effective healthcare by targeting specific disease mechanisms. As public and private healthcare systems continue to prioritize personalized medicine, diagnostic labs can expand their service offerings and invest in technologies that support this growth.

Telemedicine Integration

The integration of telemedicine with diagnostic labs presents a significant opportunity for growth. With the rise of telehealth services, there is an increasing demand for remote diagnostic testing that can be integrated into virtual consultations. Diagnostic labs can collaborate with telemedicine providers to offer remote testing kits and services, expanding their reach and improving patient convenience. This opportunity is particularly valuable in rural and underserved areas, where access to traditional healthcare facilities may be limited. Additionally, the ongoing COVID-19 pandemic has accelerated the adoption of telemedicine, further driving demand for remote diagnostic services and creating new revenue streams for diagnostic labs.

Future Outlook

The future outlook for Canada’s diagnostic labs market is promising, with expected growth driven by technological innovations, increased healthcare spending, and a shift toward personalized medicine. In the next five years, we expect significant developments in AI-driven diagnostic tools, automation, and molecular diagnostics, improving efficiency and accuracy. Regulatory support for these advancements will likely continue, promoting wider adoption of advanced diagnostic technologies. Additionally, as the population ages, demand for diagnostic services will remain high, particularly in urban centers. Overall, the market is set to grow steadily as labs continue to innovate and meet evolving healthcare needs.

Major Players

- LabCorp

- Quest Diagnostics

- LifeLabs

- Dynacare

- Bio-Rad Laboratories

- Abbott Laboratories

- Siemens Healthineers

- Roche Diagnostics

- Thermo Fisher Scientific

- Beckman Coulter

- Hologic

- PerkinElmer

- GE Healthcare

- Philips Healthcare

- Canon Medical Systems

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Healthcare providers

- Hospitals and clinics

- Pharmaceutical companies

- Diagnostic equipment manufacturers

- Insurance providers

- Medical research organizations

Research Methodology

Step 1: Identification of Key Variables

Key variables such as market size, growth rates, product categories, and market trends are identified through both primary and secondary research.

Step 2: Market Analysis and Construction

Comprehensive market data is gathered and analyzed using statistical models to build a detailed market forecast.

Step 3: Hypothesis Validation and Expert Consultation

Insights and assumptions are validated through consultations with industry experts, ensuring data reliability.

Step 4: Research Synthesis and Final Output

The final report synthesizes all collected data, providing a comprehensive analysis and clear insights into the diagnostic labs market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Increasing Prevalence of Chronic Diseases

Technological Advancements in Lab Diagnostics

Government Support for Healthcare Infrastructure - Market Challenges

Regulatory Compliance and Certification Challenges

High Operational Costs

Shortage of Skilled Technicians - Market Opportunities

Rise in Demand for Genetic and Molecular Diagnostics

Expansion of Point-of-Care Diagnostic Solutions

Integration of AI and Automation in Diagnostics - Trends

Growing Adoption of Digital Health Solutions

Advancements in Personalized Medicine - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Clinical Labs

Pathology Labs

Genetic Testing Labs

Immunoassay Labs

Microbiology Labs - By Platform Type (In Value%)

Automated Platforms

Manual Platforms

Hybrid Platforms

Cloud-Based Platforms

Point-of-Care Platforms - By Fitment Type (In Value%)

On-premise Solutions

Cloud-based Solutions

Hybrid Solutions

Integrated Solutions - By End User Segment (In Value%)

Hospitals

Clinics

Research Institutes

Private Diagnostic Centers

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Technology Integration, Market Penetration, Regulatory Compliance, Service Availability, Competitive Pricing)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

LifeLabs

Dynacare

Laboratoire Dr. Bédard

BioTest Laboratories

Glenmark Diagnostics

Medcan

CML HealthCare

MedeAnalytics

LabCorp Canada

Quest Diagnostics Canada

Apex Diagnostics

Canadian Medical Laboratories

Sonic Healthcare

Molecular Diagnostic Services

Alere Canada

- Hospitals Expanding Diagnostic Services

- Research Institutes Increasing Diagnostic Investments

- Private Diagnostic Centers Offering Advanced Testing

- Clinics Embracing Diagnostic Innovation

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now