Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The Canada edge computing market reflects expanding deployment of localized compute infrastructure supporting low-latency data processing across telecommunications, industrial automation, and digital services ecosystems. Based on a recent historical assessment, the market size is approximately USD ~ billion, driven by 5G network rollout, industrial IoT adoption, and enterprise demand for real-time analytics platforms. Telecom operators, hyperscale cloud providers, and enterprises invest in distributed edge nodes and micro data centers across national connectivity networks.

Toronto, Montreal, and Vancouver dominate edge infrastructure deployment due to concentration of telecom networks, hyperscale cloud regions, and digital industries requiring latency-sensitive processing. Toronto’s financial and enterprise technology sectors sustain urban edge demand, while Montreal’s AI and research ecosystem drives distributed computing adoption. Vancouver’s smart city and autonomous systems initiatives expand regional edge nodes. Proximity to major fiber corridors and population density reinforces metropolitan dominance in Canada’s edge computing landscape.

Market Segmentation

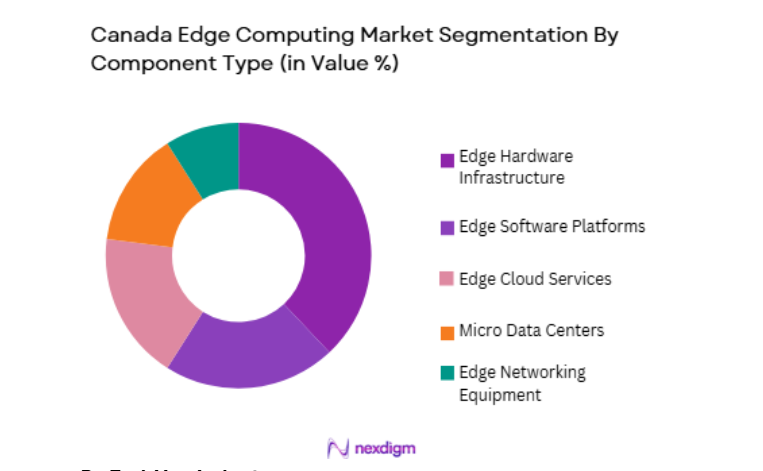

By Component Type

Canada Edge Computing Market is segmented by component type into edge hardware infrastructure, edge software platforms, edge cloud services, micro data centers, and edge networking equipment. Recently, edge hardware infrastructure has a dominant market share due to large-scale deployment of localized servers, accelerators, and gateway devices across telecom networks, industrial sites, and enterprise locations enabling real-time data processing and device connectivity at network peripheries. Telecom operators deploy edge servers at base stations supporting 5G applications. Industrial firms install on-premise edge devices for automation and monitoring. Hardware forms the foundational layer of all edge deployments. Compared with software or services, hardware investment is required upfront in each location.

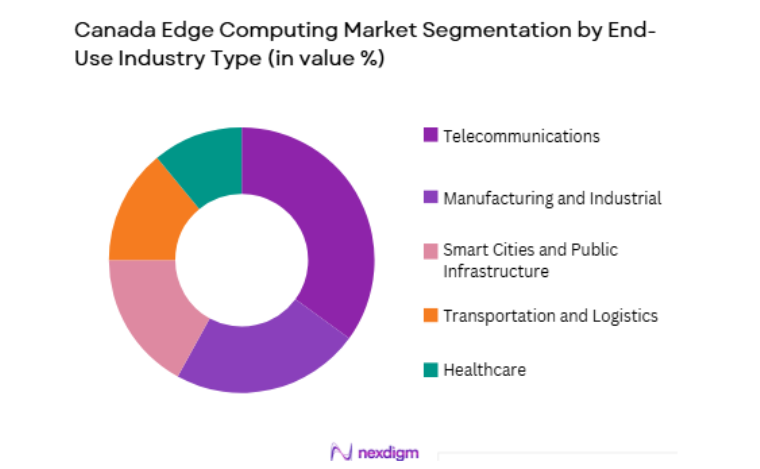

By End-Use Industry

Canada Edge Computing Market is segmented by end-use industry into telecommunications, manufacturing and industrial, smart cities and public infrastructure, transportation and logistics, and healthcare. Recently, telecommunications has a dominant market share due to nationwide 5G deployment and telecom operators’ investment in distributed edge nodes integrated with mobile networks enabling ultra-low-latency services such as network slicing, real-time analytics, and edge cloud platforms supporting enterprise and consumer applications. Telecom infrastructure provides physical locations for edge compute placement. Mobile data traffic growth requires localized processing. Operators partner with cloud providers for edge services. Compared with other sectors, telecom networks deploy edge at scale nationally.

Competitive Landscape

The Canada edge computing market features telecom operators, cloud providers, and infrastructure vendors deploying distributed compute platforms integrated with connectivity networks and enterprise environments. Global technology firms supply edge hardware and software platforms, while telecom operators and data center providers operate edge sites across regions. Partnerships between cloud and telecom firms shape competitive positioning and service ecosystems nationwide.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Edge Deployment Footprint |

| Bell Canada | 1880 | Montreal, Canada | ~ | ~ | ~ | ~ | ~ |

| Rogers Communications | 1960 | Toronto, Canada | ~ | ~ | ~ | ~ | ~ |

| TELUS | 1990 | Vancouver, Canada | ~ | ~ | ~ | ~ | ~ |

| Amazon Web Services | 2006 | USA | ~ | ~ | ~ | ~ | ~ |

| Microsoft Azure | 2010 | USA | ~ | ~ | ~ | ~ | ~ |

Canada Edge Computing Market Analysis

Growth Drivers

5G Network Expansion and Telecom Edge Integration

Canada accelerates edge computing infrastructure through nationwide 5G rollout and telecom operators’ deployment of distributed edge nodes embedded within mobile networks enabling ultra-low-latency data processing, localized content delivery, and real-time application hosting across urban and regional connectivity environments supporting consumer and enterprise digital services. Telecom providers install edge servers at base stations and aggregation sites. 5G architecture inherently supports edge computing functions. Mobile traffic growth requires localized processing capacity. Cloud providers integrate platforms with telecom networks. Enterprises adopt edge for latency-sensitive applications. Smart devices and IoT increase data volumes. Network slicing requires local compute resources. Autonomous connectivity services depend on edge nodes. Continuous 5G densification expands infrastructure footprint nationwide.

Industrial IoT Adoption and Real-Time Data Processing Requirements

Canadian industries increasingly deploy IoT sensors, automation systems, and AI-enabled monitoring platforms across manufacturing, energy, logistics, and infrastructure sectors requiring localized edge computing infrastructure capable of processing high-frequency data streams and enabling real-time decision-making without reliance on centralized cloud latency constraints across geographically distributed industrial environments. Factories deploy edge nodes for predictive maintenance. Energy networks require real-time monitoring. Logistics hubs process sensor data locally. Industrial robotics depends on low latency compute. Remote operations require localized analytics. Safety systems rely on instant processing. Industrial AI workloads grow continuously. Enterprises integrate edge with cloud analytics. These requirements accelerate industrial edge infrastructure expansion nationwide.

Market Challenges

High Deployment Costs and Distributed Infrastructure Management Complexity

Canada faces challenges in scaling edge computing infrastructure due to high capital costs of deploying numerous distributed edge nodes, micro data centers, and networking equipment combined with operational complexity of managing geographically dispersed infrastructure across telecom, industrial, and urban environments requiring specialized orchestration and maintenance capabilities. Each edge site requires hardware investment. Remote sites increase installation costs. Maintenance across locations is complex. Power and connectivity provisioning vary regionally. Hardware lifecycle management adds expense. Software orchestration is challenging. Security monitoring across nodes is difficult. Skilled workforce is required. Return on investment varies by use case. These factors constrain rapid edge scaling nationwide.

Interoperability, Standards, and Ecosystem Integration Barriers

The Canada edge computing ecosystem includes telecom operators, cloud providers, hardware vendors, and enterprises, but lack of unified standards, interoperability frameworks, and seamless integration across platforms and networks complicates deployment of scalable edge services and multi-vendor infrastructure across sectors and regions. Different vendors use proprietary platforms. Cross-network integration is complex. Application portability is limited. Standards for edge orchestration evolve slowly. Telecom-cloud interfaces vary. Enterprise systems integration requires customization. Security frameworks differ. Multi-edge deployments lack consistency. Ecosystem fragmentation reduces scalability. These barriers hinder cohesive edge infrastructure growth nationwide.

Opportunities

Edge AI and Autonomous Systems Infrastructure Expansion

Canada has strong opportunity to expand edge computing infrastructure supporting AI-enabled autonomous systems, robotics, smart transportation, and remote operations across urban and industrial environments requiring localized inference computing integrated with sensors, vehicles, and machines across geographically diverse national landscapes and innovation sectors. Autonomous vehicles require roadside edge nodes. Robotics systems depend on local AI inference. Smart infrastructure uses edge analytics. Remote mining operations deploy edge compute. Defense and surveillance systems adopt edge AI. Real-time vision processing expands demand. AI models run locally at edge. Regional clusters adopt autonomous technologies. Edge-AI convergence drives infrastructure investment nationwide.

Smart City, Connected Infrastructure, and Public Safety Edge Platforms

Growing deployment of smart city systems, intelligent transportation, environmental monitoring, and public safety networks across Canadian municipalities creates opportunities for distributed edge infrastructure embedded in urban infrastructure enabling real-time analytics, surveillance processing, traffic optimization, and emergency response systems integrated with telecom and cloud platforms across metropolitan regions. Cities deploy edge sensors and cameras. Traffic systems need local processing. Public safety analytics run at edge. Environmental monitoring uses distributed compute. Urban mobility platforms require latency control. Municipal IoT networks expand. Edge nodes integrate with 5G. City data platforms decentralize processing. Infrastructure modernization supports edge rollout. These trends enable municipal edge infrastructure expansion nationwide.

Future Outlook

The Canada edge computing market is expected to expand steadily over the next five years, driven by 5G densification, industrial IoT adoption, and AI-enabled autonomous systems deployment. Telecom-cloud partnerships will expand distributed edge nodes nationwide. Smart city and infrastructure modernization programs will increase municipal edge investment. Integration of edge AI and real-time analytics across industries will sustain long-term edge infrastructure growth across Canada.

Major Players

- Bell Canada

- Rogers Communications

- TELUS

- Amazon Web Services

- Microsoft Azure

- Google Cloud

- Cisco Systems

- HPE

- Dell Technologies

- NVIDIA

- Ericsson

- Nokia

- IBM

- Equinix

- Schneider Electric

Key Target Audience

- Telecommunications operators

- Manufacturing and industrial firms

- Transportation and logistics companies

- Smart city and infrastructure agencies

- Healthcare providers

- Technology and AI companies

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Edge infrastructure variables including distributed compute nodes, telecom edge sites, micro data centers, IoT deployments, and latency-sensitive workloads were identified from industry reports, telecom data, and company disclosures. Sectoral edge adoption across telecom, manufacturing, and urban infrastructure was mapped. Technology trends in 5G and edge AI were incorporated.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed using secondary data from telecom infrastructure investments, edge platform deployments, IoT device statistics, and regional connectivity infrastructure announcements. Segment shares were estimated based on deployment patterns across industries and components. Regional infrastructure density was benchmarked across Canada.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultations with telecom engineers, industrial IoT architects, and edge platform specialists across Canada. Infrastructure deployment assumptions and operational challenges were refined through expert input. Technology adoption and sector demand were cross-checked against practitioner insights.

Step 4: Research Synthesis and Final Output

Validated quantitative and qualitative inputs were synthesized into a structured market model integrating edge infrastructure capacity, demand drivers, segmentation shares, and competitive dynamics. Regional connectivity and policy influences were incorporated. Final outputs were reviewed for consistency with telecom and IoT ecosystem realities.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of 5G and telecom edge infrastructure across Canada

Rising demand for low latency computing in industrial and remote operations

Adoption of edge AI in smart city and transportation applications - Market Challenges

Harsh climate and remote geography increasing deployment complexity

Limited edge connectivity and backhaul in rural regions

High operational costs for distributed edge infrastructure management - Market Opportunities

Edge computing for energy and natural resource monitoring in remote sites

Growth of smart city and intelligent transportation edge platforms

Integration of AI inference capabilities in telecom and enterprise edge - Trends

Deployment of modular micro data centers at telecom and industrial sites

Convergence of edge computing with 5G and private wireless networks

Increasing adoption of ruggedized and outdoor edge infrastructure - Government regulations

Canadian telecom and spectrum regulations impacting edge deployment

Data sovereignty requirements for distributed data processing

Public infrastructure and smart city funding programs - SWOT analysis

- Porters Five forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Edge Servers and Micro Data Centers

Edge Networking and Gateways

Industrial Edge Computing Systems

AI Enabled Edge Nodes

Ruggedized Edge Infrastructure - By Platform Type (In Value%)

Telecom Edge Infrastructure

Enterprise On Premise Edge

Cloud Provider Edge Zones

Industrial and Remote Edge Sites

Smart City and Public Edge Platforms - By Fitment Type (In Value%)

Indoor Edge Installations

Outdoor and Harsh Environment Edge

Tower and Telecom Site Edge

Mobile and Vehicle Mounted Edge

Modular Edge Enclosures - By End User Segment (In Value%)

Telecommunications Operators

Manufacturing and Industrial Firms

Energy and Utilities Companies

- Market Share Analysis

- Cross Comparison Parameters (Latency Performance, Ruggedization Level, Deployment Flexibility, Connectivity Integration, Edge AI Capability, Environmental Tolerance, Power Efficiency, Remote Management, Form Factor Modularity, Network Interoperability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Cisco Systems

Hewlett Packard Enterprise

Dell Technologies

Nokia

Ericsson

Huawei

Lenovo

Supermicro

Schneider Electric

Vertiv

Advantech

Siemens

IBM

Fujitsu

NEC

- Telecom operators deploying edge nodes for 5G and low latency services

- Industrial firms adopting edge for automation and predictive maintenance

- Energy companies using edge for remote monitoring and control

- Municipalities implementing smart city edge platforms

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now