Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The market size for electric vehicle (EV) batteries in Canada is driven by the increasing adoption of electric vehicles, technological advancements, and the growing demand for sustainable transportation. The market is supported by a combination of federal incentives, environmental regulations, and a growing infrastructure for EV charging. The demand for EV batteries is projected to increase significantly as the Canadian government continues to implement stricter emission standards and supports green initiatives. As of the most recent historical assessment, the market value is estimated to be over USD ~ billion, reflecting a steady rise driven by advancements in energy storage and EV technology.

Canada, particularly cities like Toronto, Vancouver, and Montreal, plays a crucial role in the development of EV battery markets. These areas have seen considerable investments in both public and private sectors aimed at accelerating EV adoption and battery manufacturing. Provinces like British Columbia have adopted progressive policies that encourage EV sales, contributing to their market dominance. The Canadian government has also set ambitious goals to increase EV sales, which strengthens demand for locally produced EV batteries. Factors like proximity to North American automotive giants and the establishment of large-scale manufacturing plants further enhance Canada’s position in the global EV battery market.

Market Segmentation

By Product Type

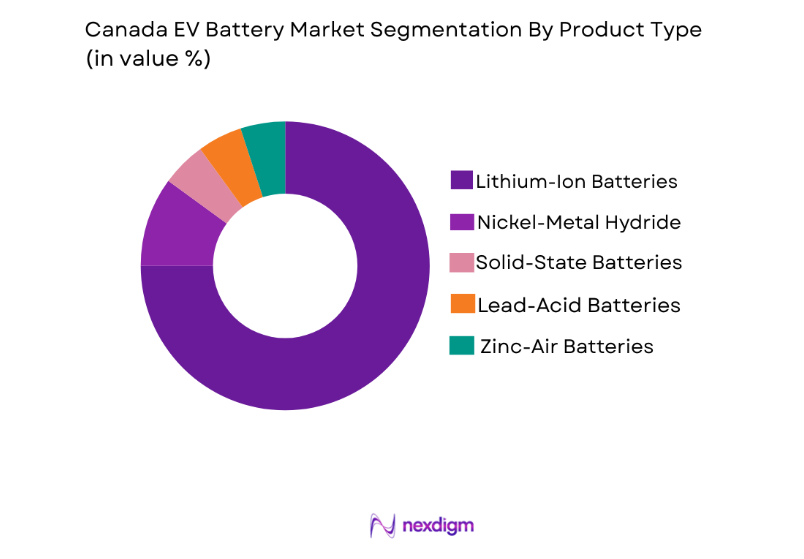

Canada EV battery market is segmented by product type into lithium-ion batteries, nickel-metal hydride batteries, solid-state batteries, lead-acid batteries, and zinc-air batteries. The lithium-ion battery sub-segment holds a dominant market share, attributed to its superior energy density, long cycle life, and growing demand in electric vehicles. As EV manufacturers prioritize performance and cost-efficiency, the lithium-ion battery has become the preferred choice for most applications. Its widespread adoption in both passenger vehicles and commercial fleets drives its continued dominance in the market. The increasing need for higher-performing batteries, especially for long-range EVs, further reinforces the growing demand for lithium-ion batteries across Canada.

By Platform Type

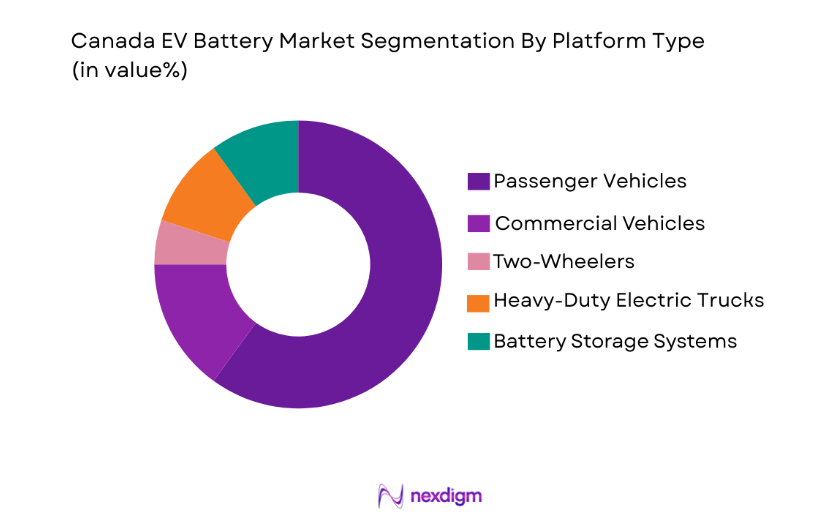

Canada’s EV battery market is also segmented by platform type, including passenger vehicles, commercial vehicles, two-wheelers, heavy-duty electric trucks, and battery storage systems. Among these, passenger vehicles lead the market share due to the rapid growth in the adoption of electric cars. This shift is driven by consumer preference for clean energy, enhanced driving range, and government incentives that promote sustainable transportation. The rising production of electric cars from major automakers like Tesla and GM further boosts the demand for EV batteries, ensuring that passenger vehicles maintain a significant portion of the overall market in Canada.

Competitive Landscape

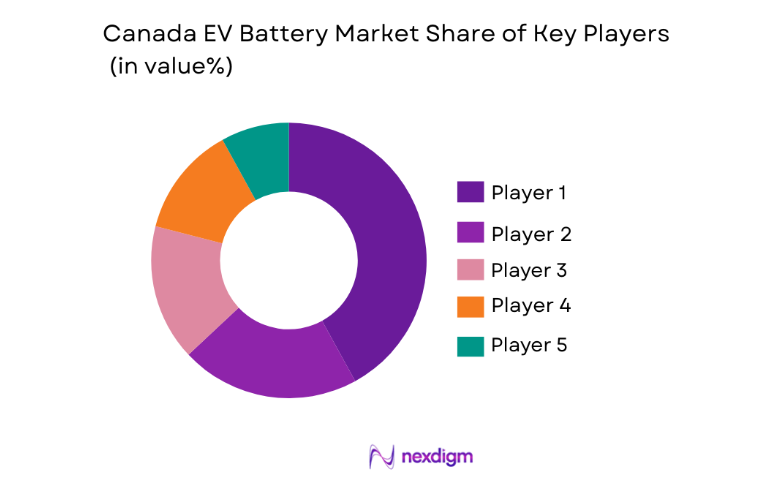

The Canadian EV battery market is highly competitive, with significant consolidation taking place. Several global companies, including battery manufacturers and automakers, dominate the market landscape. The competition is influenced by factors like technological innovation, production capacity, and strategic partnerships with automakers and government entities. Companies such as Tesla, LG Chem, and Panasonic are the main players, but the market is also seeing increased activity from local manufacturers aiming to take advantage of government incentives aimed at increasing domestic EV battery production. The continuous push for more efficient battery technologies and cost reductions will further intensify the competition, leading to greater consolidation among major players.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Parameter |

| Tesla | 2003 | Palo Alto, CA | ~ | ~ | ~ | ~ | ~ |

| LG Chem | 1947 | Seoul, South Korea | ~ | ~ | ~ | ~ | ~ |

| Panasonic | 1918 | Osaka, Japan | ~ | ~ | ~ | ~ | ~ |

| BYD | 1995 | Shenzhen, China | ~ | ~ | ~ | ~ | ~ |

| Northvolt | 2016 | Stockholm, Sweden | ~ | ~ | ~ | ~ | ~

|

Canada EV Battery Market Analysis

Growth Drivers

Government Incentives

Government incentives play a significant role in the growth of the EV battery market in Canada. Federal and provincial subsidies, tax credits, and rebates for electric vehicle purchases and infrastructure development have spurred demand for electric vehicles and, consequently, for EV batteries. The Canadian government has committed to reducing carbon emissions, which includes transitioning to zero-emission vehicles. As a result, consumers are increasingly incentivized to adopt electric vehicles, driving up the need for high-performing, cost-efficient batteries. Government support for battery production, such as funding for Canadian manufacturers and companies involved in R&D, ensures a sustainable market for EV batteries. The promotion of charging infrastructure further facilitates the growth of EVs, thus boosting the demand for EV batteries. This favorable regulatory environment and the push toward a greener future have created a thriving market for EV batteries in Canada. Additionally, support for local manufacturing and technological development is helping to reduce reliance on imports, benefiting both consumers and manufacturers alike.

Technological Advancements

Technological advancements in battery technology are also a major growth driver for the EV battery market in Canada. With improvements in lithium-ion batteries, including higher energy density, faster charging times, and longer life cycles, EV batteries have become increasingly appealing to both consumers and manufacturers. Research and development into solid-state batteries and other next-generation technologies are paving the way for even more advanced and efficient battery systems. These advancements not only address issues of battery performance but also reduce the overall cost of EV batteries, making them more accessible to a wider range of consumers. As battery prices continue to fall due to technological innovation and economies of scale, more individuals and businesses will be able to adopt electric vehicles, further expanding the EV battery market. The continuous evolution of battery technology ensures that the market will remain dynamic, with new innovations driving further adoption of EVs in Canada.

Market Challenges

Battery Supply Chain Constraints

A significant challenge facing the Canadian EV battery market is the supply chain constraints, particularly the availability and cost of raw materials. Materials like lithium, cobalt, and nickel are crucial for EV battery production, but these resources are often concentrated in a few countries, making them vulnerable to supply disruptions. The global competition for these raw materials can lead to price volatility, which affects the cost of manufacturing EV batteries. Additionally, the mining and extraction of these materials pose environmental and ethical concerns, adding pressure on manufacturers to find more sustainable and socially responsible alternatives. The reliance on foreign supply chains for critical materials also makes the Canadian EV battery market susceptible to geopolitical risks, such as trade disputes or changes in export regulations. To address these issues, Canada is looking to develop its own mining operations for key materials and invest in recycling technologies, but overcoming these supply chain constraints will remain a challenge for the foreseeable future.

Regulatory Hurdles

Regulatory hurdles in Canada present another challenge for the EV battery market. Although the government is committed to reducing emissions and promoting green technologies, regulatory processes related to EV battery production, recycling, and disposal can slow down the adoption of new technologies. For instance, strict regulations on battery recycling and the disposal of hazardous materials can impose additional costs on manufacturers and hinder market expansion. Furthermore, the lack of consistent standards for battery performance, quality control, and safety across the market can lead to confusion and delay the development of new products. While the government is working towards establishing more uniform regulations, navigating the complex regulatory landscape remains a significant challenge for companies operating in the Canadian EV battery market. These hurdles can also discourage investment in new battery technologies, as manufacturers seek clarity and stability before committing to large-scale production.

Opportunities

Battery Recycling

Battery recycling represents a significant opportunity for the Canadian EV battery market. With the rapid growth of electric vehicle sales, the need for effective battery recycling solutions has become increasingly critical. By developing more efficient recycling processes, Canada can reduce its dependence on raw materials and mitigate the environmental impact of used batteries. The government has already taken steps to establish battery collection and recycling programs, which will help create a circular economy for EV batteries. Additionally, advancements in recycling technologies could lead to higher recovery rates of valuable materials like lithium, cobalt, and nickel, further improving the sustainability of EV battery production. Canadian companies that invest in battery recycling technologies and processes could play a key role in reducing the environmental footprint of the EV industry while supporting the long-term growth of the market. This presents an opportunity for both new and existing players to lead in the development of sustainable battery solutions.

Strategic Partnerships with Automakers

Strategic partnerships between battery manufacturers and automakers present another opportunity for growth in the Canadian EV battery market. As automakers ramp up their production of electric vehicles, the demand for reliable and high-performance batteries continues to grow. Battery manufacturers can benefit from establishing partnerships with these automakers to secure long-term contracts and ensure a steady supply of batteries. In turn, automakers can benefit from working directly with battery manufacturers to develop customized battery solutions that meet their specific needs, such as battery packs designed for particular vehicle models or use cases. These partnerships can also help streamline the supply chain, reduce costs, and accelerate the deployment of electric vehicles across Canada. Furthermore, such collaborations can lead to joint ventures focused on developing new battery technologies, which would further strengthen Canada’s position in the global EV battery market. This opportunity is set to expand as the automotive sector shifts toward electric vehicles in the coming years.

Future Outlook

The future of the Canadian EV battery market looks promising, with continued growth driven by technological advancements, supportive government policies, and increasing consumer demand for electric vehicles. As battery technology improves, energy density increases, and costs decrease, EVs will become more affordable and accessible, further expanding the market. With the ongoing push towards sustainability and decarbonization, Canada’s strategic investments in the EV industry will drive further demand for advanced battery solutions. The focus on local battery production and recycling will also play a critical role in ensuring long-term market stability, while the development of new infrastructure and charging solutions will support the widespread adoption of electric vehicles across the country.

Major Players

- Tesla Inc.

- LG Chem Ltd.

- Panasonic Corporation

- BYD Company

- Northvolt AB

- General Motors

- Ford Motor Company

- BMW Group

- Volkswagen Group

- Honda Motor Co.

- Toyota Motor Corporation

- Nissan Motor Co.

- Rivian Automotive

- Lucid Motors

- Stellantis

Key Target Audience

- Investments and venture capitalist firm

- Government and regulatory bodies

- Automakers

- Battery manufacturers

- Charging infrastructure providers

- Raw material suppliers

- EV fleet operators

- Public sector energy companies

Research Methodology

Step 1: Identification of Key Variables

In this step, the key variables that influence the EV battery market are identified, such as technological advancements, government regulations, and consumer adoption rates. The data collected helps in shaping the direction of the research.

Step 2: Market Analysis and Construction

Data from primary and secondary sources is analyzed to construct the market model. This involves assessing current market conditions, growth trends, and identifying market leaders.

Step 3: Hypothesis Validation and Expert Consultation

The developed hypotheses are tested and validated through consultations with industry experts, including battery manufacturers, EV producers, and government representatives.

Step 4: Research Synthesis and Final Output

The findings are synthesized, and the final market report is produced, detailing market size, growth drivers, challenges, and opportunities, along with actionable insights for stakeholders.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Increasing Adoption of Electric Vehicles

Government Incentives and Subsidies for EV Battery Development

Growing Demand for Sustainable Transportation

Advancements in Battery Technologies

Rising Environmental Concerns and Emission Regulations - Market Challenges

High Cost of EV Batteries

Limited Battery Recycling Infrastructure

Supply Chain Constraints for Raw Materials

Technological Barriers in Battery Efficiency

Regulatory Hurdles in Battery Production and Disposal - Market Opportunities

Expansion of EV Charging Infrastructure

Partnerships Between Automakers and Battery Manufacturers

Advances in Battery Recycling Technologies - Trends

Shift Towards Sustainable and Eco-Friendly Batteries

Integration of Battery Management Systems (BMS) in EVs

Rise in Solid-State and Lithium-Sulfur Batteries - Government Regulations & Defense Policy

Battery Recycling and End-of-Life Regulations

Government Funding for EV Battery Research

Policies to Promote EV Battery Manufacturing in Canada - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Lithium-Ion Batteries

Nickel-Metal Hydride Batteries

Solid-State Batteries

Lead-Acid Batteries

Zinc-Air Batteries - By Platform Type (In Value%)

Passenger Vehicles

Commercial Vehicles

Two-Wheelers

Heavy-duty Electric Trucks

Battery Storage Systems - By Fitment Type (In Value%)

Original Equipment Manufacturer (OEM) Batteries

Aftermarket Batteries

Integrated System Batteries

Modular Batteries

Hybrid Batteries - By End User Segment (In Value%)

Automotive Manufacturers

Battery Manufacturers

EV Fleet Operators

- Market share of major players

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Tesla Inc.

Panasonic Corporation

LG Chem Ltd.

Samsung SDI Co.

BYD Company

CATL (Contemporary Amperex Technology Co.)

Northvolt AB

SK Innovation Co.

General Motors

Ford Motor Company

Volkswagen Group

BMW Group

Honda Motor Co.

Toyota Motor Corporation

Nissan Motor Co.

- Automotive Manufacturers’ Investment in EV Battery Technology

- Battery Manufacturers’ Role in Supply Chain Optimization

- EV Fleet Operators’ Focus on Battery Performance

- Government’s Strategic Focus on EV Battery Infrastructure

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now