Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Canada farm equipment powertrain and mechanical components market reached approximately USD ~ billion based on a recent historical assessment, driven by sustained demand for high-horsepower tractors, combines, and articulated machinery used in large-scale grain production regions. Component replacement cycles for transmissions, axles, and driveline assemblies have accelerated due to heavy field utilization and longer operating hours. Mechanization intensity and precision agriculture adoption continue to expand mechanical complexity, increasing the value of integrated powertrain modules supplied to original equipment manufacturers and aftermarket channels.

Prairie provinces including Saskatchewan, Alberta, and Manitoba dominate equipment powertrain demand due to extensive cereal and oilseed cultivation requiring heavy mechanized field operations across vast farm holdings. Manufacturing and assembly clusters concentrated in Winnipeg, Saskatoon, and Regina support regional supply chains for driveline and transmission components. Strong export-oriented farm machinery production and proximity to United States agricultural equipment markets reinforce Canada’s position as a core North American hub for agricultural powertrain engineering and mechanical component integration.

Market Segmentation

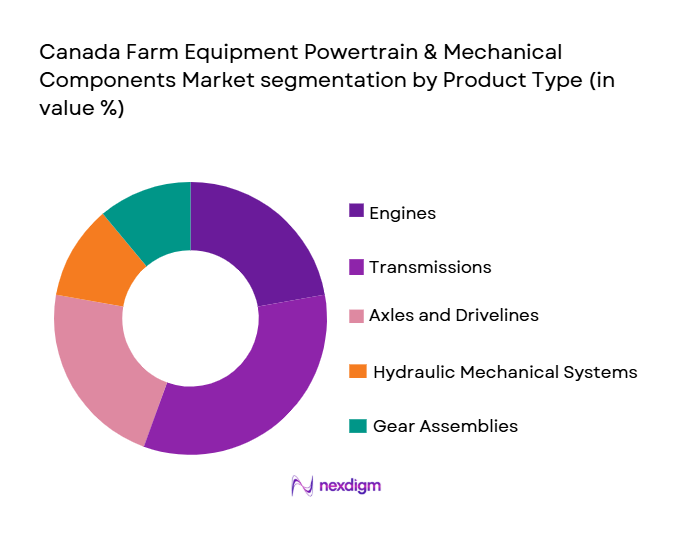

By Product Type:

Canada farm equipment powertrain and mechanical components market is segmented by product type into engines, transmissions, axles and drivelines, hydraulic mechanical systems, and gear assemblies. Recently, transmissions has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. The dominance of transmission systems reflects the increasing adoption of high horsepower tractors and combines operating under heavy torque loads across prairie agriculture, where variable speed field operations require robust mechanical power delivery. Continuously variable and powershift transmission architectures command higher unit values and replacement costs compared with other mechanical components. Canadian equipment manufacturers prioritize advanced transmission engineering to support export-oriented tractor production, strengthening domestic component demand. Extended equipment lifecycles and intensive seasonal utilization accelerate wear in gear trains and clutch assemblies, driving recurrent aftermarket demand. Availability of specialized service networks and remanufacturing facilities further reinforces transmission market leadership within the broader mechanical component ecosystem.

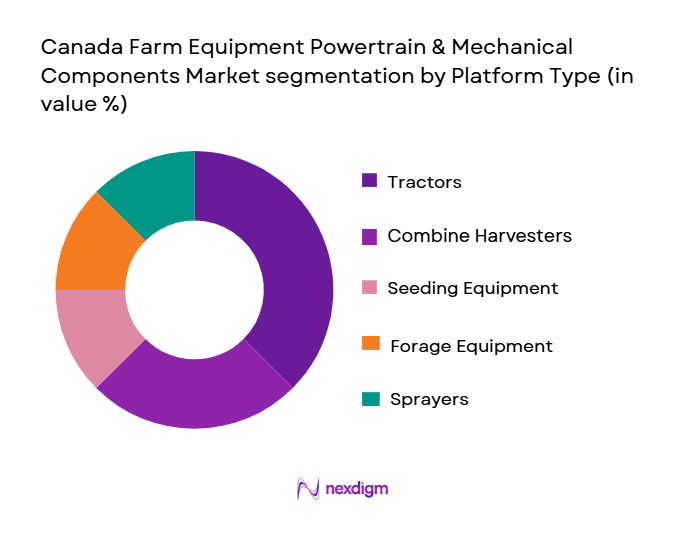

By Platform Type:

Canada farm equipment powertrain and mechanical components market is segmented by platform type into tractors, combine harvesters, seeding equipment, forage equipment, and sprayers. Recently, tractors has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Tractor platforms represent the primary source of mechanical component consumption because they operate year-round across multiple farm functions including tillage, planting, hauling, and harvesting support tasks. High horsepower articulated tractors used in prairie agriculture require complex driveline, transmission, and axle systems with higher material intensity and replacement value. Tractor fleets are also the largest installed base within Canadian agriculture, resulting in sustained aftermarket demand for mechanical refurbishment and component upgrades. OEM production of tractors in Canadian manufacturing centers further concentrates powertrain component integration within this platform, sustaining its leading share across both new equipment assembly and lifecycle maintenance segments.

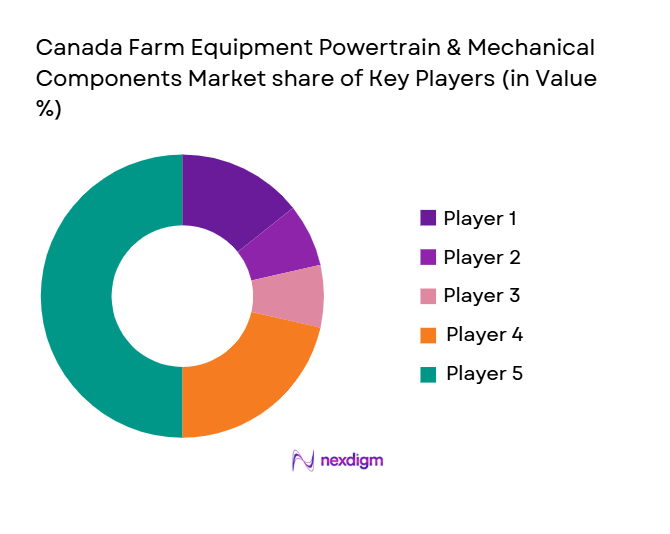

Competitive Landscape

The market exhibits moderate consolidation with a mix of domestic mechanical engineering firms and global agricultural equipment manufacturers controlling supply of integrated powertrain modules and drivetrain subsystems. Large OEM-aligned suppliers maintain strong technological capabilities in transmission, axle, and driveline engineering, while regional component manufacturers compete in remanufacturing and aftermarket distribution. Cross-border integration with United States machinery supply chains intensifies competitive pressures and encourages technological standardization across North American farm equipment platforms.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Platform Integration Capability |

| Linamar Corporation | 1966 | Canada | ~ | ~ | ~ | ~ | ~ |

| Buhler Industries | 1932 | Canada | ~ | ~ | ~ | ~ | ~ |

| Brandt Group | 1932 | Canada | ~ | ~ | ~ | ~ | ~ |

| Dana Incorporated | 1904 | United States | ~ | ~ | ~ | ~ | ~ |

| Magna International | 1957 | Canada | ~ | ~ | ~ | ~ | ~ |

Canada Farm Equipment Powertrain and Mechanical Components Market Analysis

Growth Drivers

High Horsepower Agricultural Mechanization Expansion:

The structural transformation of Canadian agriculture toward large-scale prairie grain operations has significantly increased reliance on heavy tractors and combines equipped with advanced mechanical powertrain architectures. Farms exceeding thousands of hectares require machinery capable of sustained high torque delivery and continuous field operation over extended seasonal windows. Such conditions necessitate sophisticated transmissions, reinforced axles, and durable driveline assemblies with higher material content and engineering complexity. Equipment manufacturers have responded by introducing articulated tractors and high-capacity harvesters that integrate multi-stage mechanical power distribution systems. These machines command substantially greater component value than conventional equipment, directly elevating demand for powertrain modules. Increasing export production of high horsepower tractors in Canada further amplifies domestic component manufacturing activity. Extended equipment utilization intensity accelerates mechanical wear, shortening replacement intervals for transmission and driveline systems. Precision agriculture technologies also require stable mechanical platforms to support automation and load control, reinforcing demand for advanced powertrain engineering. Together these structural shifts in mechanization scale and equipment sophistication underpin sustained expansion of the mechanical components market.

Replacement And Remanufacturing Demand From Aging Equipment Fleet:

A significant portion of Canadian farm machinery has been in operation for extended service lives due to the high capital cost of new agricultural equipment and cyclical farm income conditions. As tractors and harvesters age, mechanical systems such as transmissions, differentials, and gear assemblies experience cumulative wear and fatigue under heavy field loads. Farmers frequently opt for component refurbishment or replacement rather than complete machinery replacement, sustaining aftermarket demand for mechanical modules. Remanufacturing capabilities in Canadian industrial regions enable cost-effective restoration of driveline and axle systems, extending equipment lifecycles. Seasonal agricultural operations concentrate mechanical stress into limited timeframes, intensifying deterioration rates and increasing failure risk. Equipment dealers and service providers therefore maintain inventories of replacement powertrain components to ensure operational continuity. This maintenance-driven consumption pattern generates stable revenue streams independent of new equipment sales cycles. Continuous fleet aging across prairie agriculture ensures persistent mechanical component replacement requirements. The interplay of long equipment lifespans and heavy operational intensity structurally reinforces the aftermarket segment within the Canadian powertrain and mechanical components market.

Market Challenges

Volatility In Steel And Casting Input Costs:

Mechanical powertrain components rely heavily on high-grade alloy steels, cast iron housings, and precision machined gears, all of which are sensitive to fluctuations in global metal markets. Canadian manufacturers face cost instability arising from raw material price swings driven by energy costs, mining output variability, and international trade conditions. Such volatility complicates long-term pricing strategies for transmissions and driveline systems supplied to agricultural equipment manufacturers. OEM contracts often require fixed pricing over production cycles, exposing component suppliers to margin compression during material cost surges. Smaller domestic mechanical firms are particularly vulnerable because of limited hedging capacity and lower procurement volumes. Supply disruptions in specialized casting and forging inputs further intensify production uncertainty. Agricultural equipment demand cycles already exhibit seasonality, and cost instability compounds financial risk during low production periods. Manufacturers may delay capital investment in advanced machining or automation due to uncertain returns under volatile input pricing. This structural exposure to commodity price dynamics constrains profitability and operational planning across the Canadian farm equipment mechanical components sector.

Dependence On Cyclical Agricultural Machinery Demand:

Canadian powertrain and mechanical components market is intrinsically linked to farm income levels and agricultural commodity prices, which influence machinery purchasing and maintenance decisions. Periods of lower crop prices or unfavorable weather conditions reduce farmers’ capital expenditure on equipment upgrades and major mechanical replacements. Equipment manufacturers subsequently scale back production volumes, directly affecting component orders from suppliers. Seasonal concentration of agricultural operations also causes uneven demand for mechanical parts, with peaks during planting and harvest preparation periods. Suppliers must maintain production flexibility and inventory buffers to manage these fluctuations, increasing operational costs. Export-oriented machinery manufacturing introduces additional exposure to international agricultural cycles, particularly in United States markets. Long lead times for mechanical component manufacturing exacerbate forecasting challenges during demand downturns. Financial planning for specialized machining and casting operations becomes difficult under uncertain order pipelines. This cyclical dependence on agricultural equipment demand introduces structural volatility into the Canadian farm equipment powertrain and mechanical components industry.

Opportunities

Integration Of Electrified Auxiliary Powertrain Systems:

The gradual electrification of agricultural machinery subsystems presents new avenues for mechanical component innovation within the Canadian farm equipment sector. Hybrid and electric auxiliary drives for implements, steering systems, and hydraulic pumps require redesigned gear interfaces and mechanical integration structures. Canadian manufacturers with expertise in precision machining and driveline engineering can supply specialized housings and transmission interfaces for these emerging architectures. Electrified subsystems often operate at higher torque densities, increasing requirements for advanced mechanical materials and heat management components. Equipment producers seeking improved fuel efficiency and reduced emissions are incorporating electric assist functions into tractors and harvesters. Such transitions create demand for hybrid power distribution systems combining mechanical and electric torque delivery. Domestic engineering capabilities in gear manufacturing and mechanical integration position Canadian firms to participate in this technology shift. Collaboration between mechanical suppliers and agricultural OEMs supports development of modular electrified driveline platforms. As electrification expands across agricultural machinery, mechanical component value per unit is expected to rise through increased complexity. This technological transition offers a structural growth pathway for the Canadian mechanical powertrain ecosystem.

Expansion Of Precision Agriculture Compatible Mechanical Platforms:

Precision agriculture technologies such as autonomous steering, variable rate application, and digital load management require mechanically stable and highly responsive powertrain systems. Canadian farms adopting advanced precision equipment demand tractors and implements with driveline assemblies capable of precise torque modulation and minimal mechanical backlash. Mechanical components must therefore achieve tighter tolerances and enhanced durability to maintain positional accuracy under automated operation. Suppliers capable of producing high-precision gears and transmissions can capture increasing demand from equipment manufacturers integrating automation features. Growth of data-driven farming practices also encourages modular mechanical architectures allowing rapid component replacement to minimize downtime. Canadian engineering firms specializing in precision machining and remanufacturing can provide such modular powertrain solutions. Integration of sensors and monitoring hardware within mechanical housings further elevates component complexity and value. As precision agriculture adoption spreads across prairie regions, equipment fleets will progressively shift toward compatible mechanical platforms. This transition expands demand for advanced mechanical components engineered for automation-ready agricultural machinery. Consequently, precision agriculture integration represents a long-term opportunity for the Canadian farm equipment powertrain and mechanical components market.

Future Outlook

The market is expected to expand steadily over the next five years supported by continued mechanization of large-scale prairie farming and replacement demand from aging equipment fleets. Technological shifts toward electrified subsystems and precision-compatible driveline architectures will raise component value per machine. Government policies promoting farm productivity and emissions-efficient machinery will support equipment modernization. Cross-border integration with North American agricultural machinery manufacturing will further sustain component production activity.

Major Players

- Linamar Corporation

- Buhler Industries

- Brandt Group

- MacDon Industries

- Versatile Tractors

- Kubota Canada

- John Deere Canada

- CNH Industrial Canada

- AGCO Corporation

- Dana Incorporated

- Magna International

- BorgWarner

- Aisin Canada

- Gleason Corporation

- Superior Gearbox Company

Key Target Audience

- Agricultural equipment manufacturers

- Powertrain and mechanicalcomponent suppliers

- Farm machinery distributors

- Agricultural cooperatives

- Large commercial farming enterprises

- Investments and venture capitalist firms

- Government and regulatory bodies

- Agricultural equipment service providers

Research Methodology

Step 1: Identification of Key Variables

Demand drivers, mechanical component categories, equipment platform adoption, and regional agricultural activity indicators were identified to structure the analytical framework. Supply chain factors including manufacturing capacity and material inputs were mapped to determine market boundaries.

Step 2: Market Analysis and Construction

Component demand was quantified by correlating equipment production volumes, installed machinery fleets, and replacement cycles. Value estimates were constructed by integrating OEM production data, aftermarket consumption patterns, and pricing benchmarks across powertrain subsystems.

Step 3: Hypothesis Validation and Expert Consultation

Industry specialists from agricultural machinery manufacturing and mechanical engineering sectors were consulted to validate component usage rates, technology trends, and replacement intervals. Findings were cross-checked with sector publications and trade association data.

Step 4: Research Synthesis and Final Output

Validated datasets were synthesized into market segmentation, competitive analysis, and demand modeling outputs. Consistency checks ensured alignment between equipment platform trends and mechanical component consumption patterns before final reporting.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising mechanization in large scale prairie farming

Replacement demand for aging tractor fleets

Adoption of high horsepower equipment platforms

Expansion of precision agriculture requiring robust drivetrains

Government support for farm productivity modernization - Market Challenges

High cost of advanced transmission systems

Supply chain volatility in steel and cast components

Seasonal demand fluctuations in agricultural machinery

Compatibility issues across multi brand equipment fleets

Skilled labor shortages in mechanical servicing - Market Opportunities

Electrified auxiliary powertrain components in farm machinery

Localized remanufacturing and refurbishment services

Integration of sensor enabled mechanical systems - Trends

Shift toward continuously variable transmissions in tractors

Use of lightweight driveline materials to improve efficiency

Growth of modular powertrain assemblies for quick replacement

Increased durability standards for extreme climate operation

Adoption of condition monitoring in mechanical components - Government Regulations & Defense Policy

Canadian emissions and engine efficiency standards for off road equipment

Occupational safety regulations for mechanical power transmission

Agricultural equipment certification and compliance frameworks - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Engine and Fuel Injection Systems

Transmission and Driveline Assemblies

Hydraulic Powertrain Modules

Mechanical Linkage and Actuation Systems

Thermal Management and Cooling Systems - By Platform Type (In Value%)

Tractors and Utility Vehicles

Harvesting Equipment Platforms

Seeding and Planting Machinery

Spraying and Crop Protection Equipment

Forage and Haying Machinery - By Fitment Type (In Value%)

OEM Factory Installed Components

Aftermarket Replacement Kits

Retrofit Powertrain Upgrades

Remanufactured Mechanical Assemblies

Performance Enhancement Modules - By EndUser Segment (In Value%)

Large Commercial Grain Farms

Mixed Crop and Livestock Farms

Agricultural Contractors and Custom Operators

Agricultural Cooperatives

Government and Institutional Farms - By Procurement Channel (In Value%)

Direct OEM Supply Contracts

Authorized Dealer Networks

Agricultural Equipment Distributors

Aftermarket Parts Retailers

Online B2B Procurement Platforms - By Material / Technology (in Value %)

High Strength Alloy Steel Components

Cast Iron Powertrain Housings

Lightweight Aluminum Driveline Parts

Advanced Polymer Composite Bushings

Precision Machined Gear Systems

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Powertrain System Coverage, Platform Compatibility Range, Material Technology Capability, OEM Integration Depth, Aftermarket Distribution Strength, Remanufacturing Capability, Product Durability Standards, Pricing Tier Positioning, Service Network Reach, Innovation in Mechanical Efficiency)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Linamar Corporation

Buhler Industries

Brandt Group of Companies

MacDon Industries

Versatile Tractors

Kubota Canada

John Deere Canada

CNH Industrial Canada

AGCO Corporation Canada

Gleason Canada

Dana Incorporated Canada

BorgWarner Canada

Magna International

Aisin Canada

Superior Gearbox Company

- Large prairie farms prioritizing high durability drivetrains

- Contractors demanding rapid serviceable mechanical modules

- Livestock farms requiring versatile multi equipment powertrains

- Cooperatives procuring standardized replacement compon

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now